Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 61 / What to expect Sept 15, 2025 thru Sept 19, 2025

Weekly Market-On-Close Report

We came in on Friday with index futures already leaning higher, the mood still buoyant from a week that steadily re-priced the path of policy easing. The open did what opens do at new highs: it tested resolve. The S&P 500 and Nasdaq 100 punched out fresh intraday records early, but by the close the tone had cooled—S&P off a hair, Dow heavier, Nasdaq 100 up modestly. That rollover wasn’t a mystery. The 10-year Treasury yield climbed about five basis points to roughly 4.06%, and the University of Michigan’s September sentiment slipped to 55.4—lowest in four months—while longer-run inflation expectations in that survey perked up to 3.9% from 3.5%. When the cost of money lifts and consumer mood sours in the same hour, equity longs take a little off.

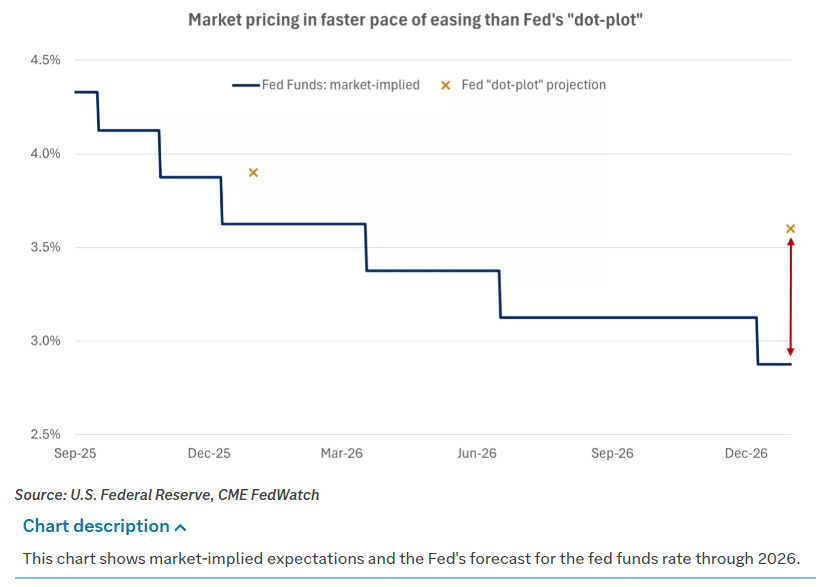

Context matters, and the broader context all week was simple: the market locked onto the idea that the Fed is back in the cutting business. The labor tape has cooled just enough, and the inflation data—while still too warm for comfort—has been “manageable” by a market that wants a pivot. Futures markets treated that mix like an engraved invitation: a quarter-point cut at the September 16–17 meeting is effectively priced as a sure thing, with a non-zero chance of a larger move, and traders spent the back half of the week nudging up odds of an encore 25 bps in late October. Add it all up and the strip now sketches roughly 70 bps of easing into year-end, which would put the policy rate closer to 3.6% from the current 4.3% area. You could see it in the way cash rotated—cyclical appetite into midweek, then a little de-risk on Friday once long rates ticked.

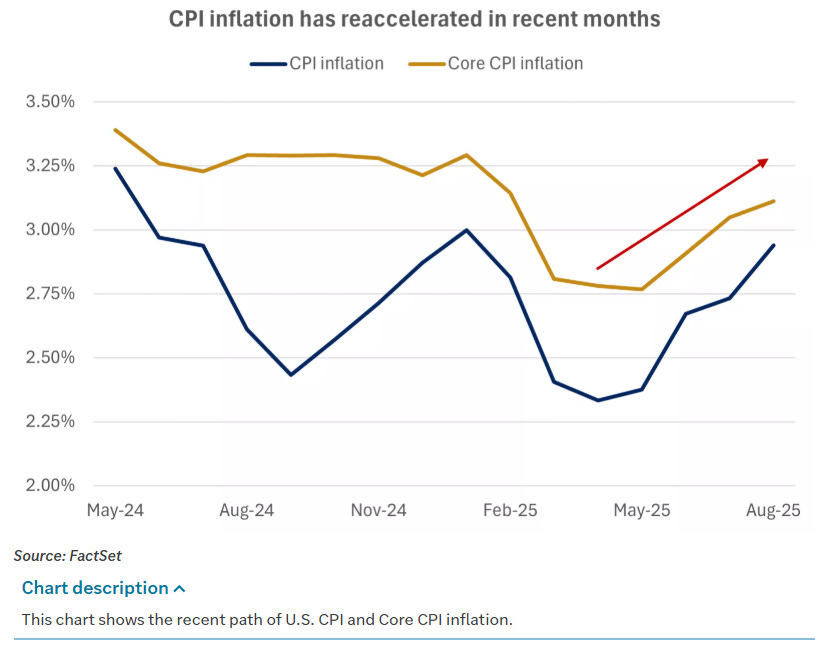

Under the surface, the week had the feel of a classic late-cycle, policy-dependent advance. That’s not a euphemism for “fragile”; it’s an observation about what’s actually powering the tape. Soft-ish data helped rather than hurt because of where we are on the policy curve. Consumer prices were not a shocker—headline CPI around 2.9% year-over-year with core unchanged near 3.1%.

Producer prices cooled harder than expected, both headline and underlying, which the market read as a sign that wholesale pass-through pressure may be fading at the margin. At the same time, the jobs ledger continues to retrace the too-rosy counts of the last year. The quarterly employment census knocked about 911,000 off previously reported gains through March, and weekly claims jumped to 263,000, the highest in years. If you’re managing risk, you recognize that combination: inflation still above target, but growth momentum softening. For an equity investor who believes we’re gliding, not stalling, it’s a green light for the “policy easing without an immediate earnings shock” narrative. For a bond investor, it’s a duration bid with a steepening bias—until a sentiment wobble or an energy headline moves the goalposts for a day, like Friday.

That framework explains the index action as well as anything. New highs for most U.S. benchmarks during the week, a little give-back into the weekend when yields perked. The Dow was the laggard on Friday, the Nasdaq 100 the only one to finish up, and the S&P virtually unchanged after the intraday fade. If you prefer your scoreboard tidy: Dow around 45,800, S&P hovering near 6,580, Nasdaq heavyweights still doing enough to keep the runway intact. Breadth wasn’t euphoric, but it was good enough to keep the advance credible most sessions. The places that led told you what the market wanted to fund: the AI complex, anything that looked like infrastructure for that complex, and the parts of discretionary that benefit when mortgage rates bleed lower.

You could see the AI axis everywhere you looked. Oracle’s blowout bookings number and big-ticket AI deal chatter turned the stock into a weekly protagonist, and the halo effect was broad.

Broadcom stayed on a tear after its own string of catalysts, memory names pushed higher, and even the “plumbing” plays around datacenter and networking caught a bid. Microsoft’s multibillion compute push stayed in the background as a narrative accelerant. It wasn’t just one or two winners; it was a cluster of enablers that the tape wants to own into an easing cycle. That’s how you get a Nasdaq 100 that refuses to sag even on a higher-rate Friday close.

The other standout was housing-adjacent discretionary. Homebuilder complex had been on rails the prior few months as long yields eased; this week the theme paused when the long end ticked up Friday, but the message remains: a gentler path for policy plus some relief at the back end is exactly the cocktail that props up volume-sensitive discretionary demand. When 30-year mortgage proxies compress, you see it in order books and in the multiple investors are willing to pay for cyclicals that earn their keep with throughput rather than hype. We had a bout of profit-taking, not a thesis break.

On the other end of the leaderboard were the groups that hate a one-day spike in yields or a headline that muddies the growth picture. Staples were soft across the board, with beverages feeling more of the pinch after guidance cuts in prior weeks and a few downgrades. Healthcare lagged, as it often does when political noise creeps in—one press report about linking pediatric events to vaccines was enough to yank a handful of the COVID-era beneficiaries lower.

Energy chopped: crude bounced after OPEC+ offered a smaller-than-feared production increase, then spent the rest of the week struggling to hold traction as the dollar and macro headlines wrestled for control. It felt like position-squaring more than a change in trend.

Single-name tape told its own story. Warner Bros Discovery ripped higher for a second straight session on fresh M&A chatter—Paramount Skydance reportedly circling—which is exactly the kind of catalyst that forces under-positioned funds to chase beta and the peer group to re-rate takeout optionality. Tesla surged on a very specific operational headline—Nevada gave the green light for AV testing—reminding everyone that the stock can still trade like an option on future business models. Micron extended a strong run as the market extrapolated AI-linked demand into calendar ’26. Super Micro ticked up after detailing deliveries of the newest Nvidia systems, which is the sort of operational follow-through that reinforces the “picks-and-shovels” idea rather than the “one chipmaker to rule them all” myth. Gartner popped on a bigger buyback authorization; Microsoft edged higher on the back of a détente-style update to its OpenAI partnership structure; a broker upped its target on AppLovin and bulls waved it around as proof that adtech with real pipes can command a premium. On the downside, Oracle gave back a chunk of the midweek euphoria. Lululemon slipped after a big bank trimmed its target and kept the debate alive about mid- to high-end U.S. apparel demand. Homebuilders and building-products names leaked with the backup in yields. A few downgrades on beverages and a whiff of insider selling elsewhere kept the “defensive at a discount” pitch alive for patient money.

Rates deserve more than a footnote. Earlier in the week, the curve bull-steepened—front-end anchored by the imminent cut, long end grinding lower as growth repriced and auctions went better than feared. Then Friday arrived, oil perked, Michigan inflation expectations edged higher, and you got a modest bear move in the belly and long end. Net-net, the week kept the 10-year in a 4.0%–4.5% lane, with frequent intraday excursions toward the lower bound. The 2-year sat near 3.56% by week’s end, which is basically the market saying “show me the dots, then we’ll talk.” The 30-year eased over the week even as Friday blipped it higher, a reminder that liability matchers and global duration tourists are still very alive at these levels. Treasury auctions were healthy—threes and tens priced below when-issued with solid bid metrics, thirties respectable if not spectacular—which tells you there’s real appetite for duration as long as the growth scare stays in “gentle landing” territory. Credit rode the wave: investment-grade outperformed duration-matched Treasuries, and high yield printed gains on the back of the coming-cuts narrative.

Across the pond, the message was similar but a shade less enthusiastic. Core European yields rose into Friday, with bunds up about six basis points and gilts a bit more. The ECB chorus stayed mixed: one governor arguing that current settings are appropriate and easing risks the inflation goal, another saying additional cuts remain possible given downside inflation risks. UK manufacturing output shocked to the downside on a monthly basis, the biggest drop in a year, keeping growth concerns simmering even as markets weigh a peaking-rates story. Asian equities were a tale of two exposures: Japan up again—records beget records—while China’s mainland indices paused after a powerful run, with Hong Kong leaning on tech to carry the water. It wasn’t a week for grand global macro calls; it was a week for noticing that the U.S. remains the cleanest dirty shirt when the policy path is this price-sensitive.

Commodities and crypto added their own color. Crude rallied out of the weekend on OPEC+ optics that were less bearish than feared and a stew of geopolitical headlines, then cooled as the week wore on. Nat gas faded a few percent, giving back last week’s bounce. Precious metals digested recent gains; gold sat near records, tracking the drift lower in real yields earlier in the week and shrugging off Friday’s reflation wobble. Grains were choppy around the WASDE update—corn and soy sold the print, then ground back to the highs as the market re-balanced supply talk with export dynamics; wheat found a friendlier bid. Crypto, meanwhile, played its own game. Bitcoin held the breakout zone and finished the week up around five percent, but most of the fireworks lived in the alt-complex; ether rallied, Solana ripped, and the speculative corners lit up with the usual meme-coin theatrics. If you wanted evidence that liquidity is looser than the headlines suggest, you didn’t have to look past those charts.

The macro conversation, though, keeps coming back to the same two dials: labor and inflation. On the labor side, the signal is clear enough now that even the optimists have stopped hand-waving. The prior week’s nonfarm payroll miss was amplified by this week’s benchmark revisions; the slower-than-thought job creation arc is now written into the data. Weekly claims spiking to 263,000—some of it seasonal, some of it Texas-skewed—got everyone’s attention because it pushed beyond the “noisy but fine” corridor. Continuing claims held around 1.94 million, which tempers the alarm but doesn’t erase it. Participation has drifted lower over the last year, and demographics plus immigration policy changes aren’t going to flip overnight. The wonky takeaway is that fewer net jobs are needed to keep the unemployment rate from accelerating; the practical takeaway is that the Fed can point to slackening demand for labor as a reason to move without waiting for core inflation to magically land at two percent.

On the inflation side, the stew is messy but edible. Headline CPI ticked up month-over-month on energy and some goods categories that are sensitive to tariff pass-through, but core stayed right where markets expected. The wholesale side cooled more than forecasts on both the headline PPI and the stripped series, with the volatile trade services component swinging negative month-on-month. The mix keeps hope alive that goods inflation can stay contained even as services remain sticky. Shelter remains the swing factor that keeps core from rolling over faster. The Fed has been telling us for months that this is how the path would look in the back half of the year—higher near-term prints from tariffs and energy, with housing-related disinflation lagging. That is exactly what we got. If you build that into a policy reaction function, you end up with a central bank that cuts slowly while watching the labor side like a hawk.

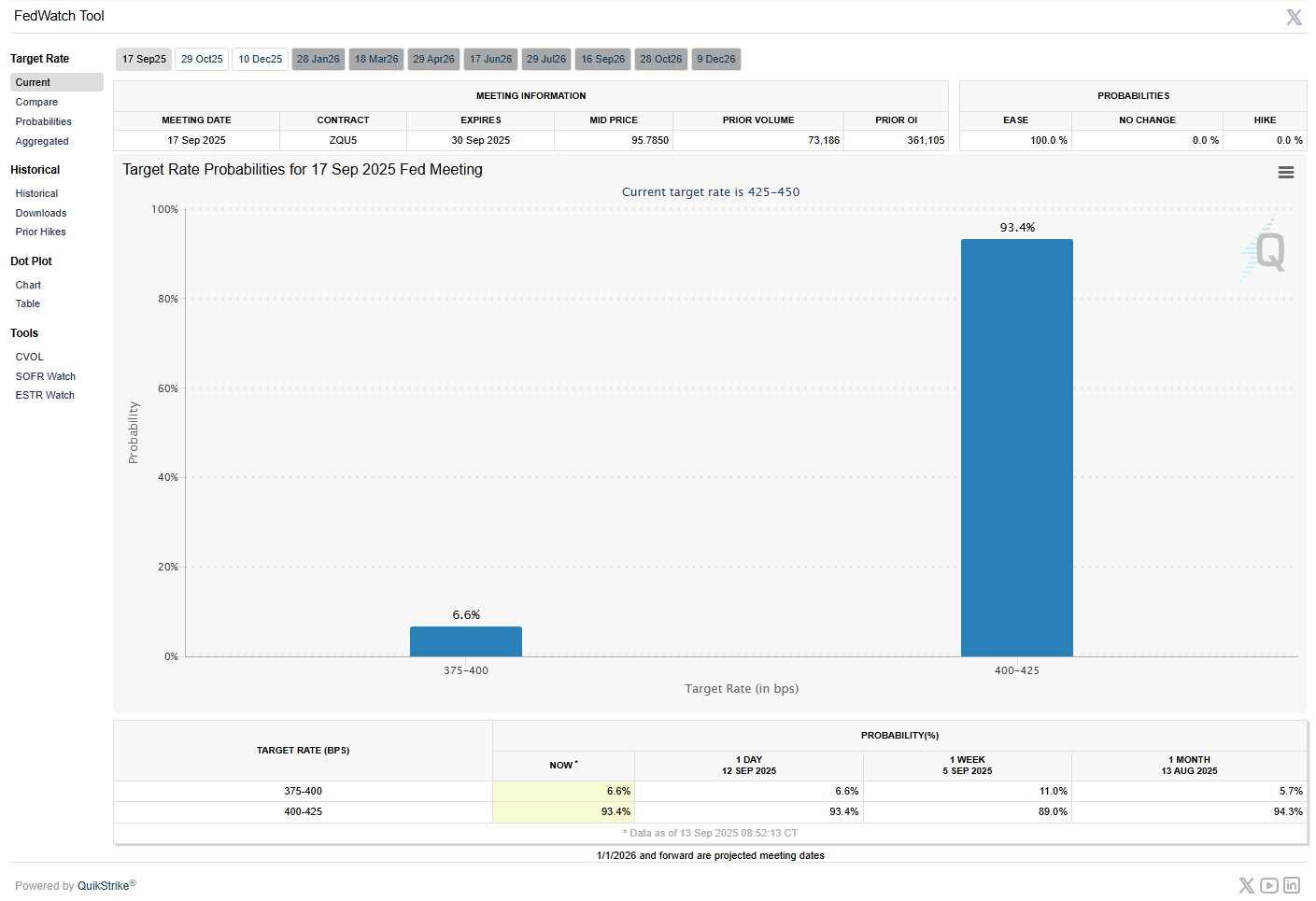

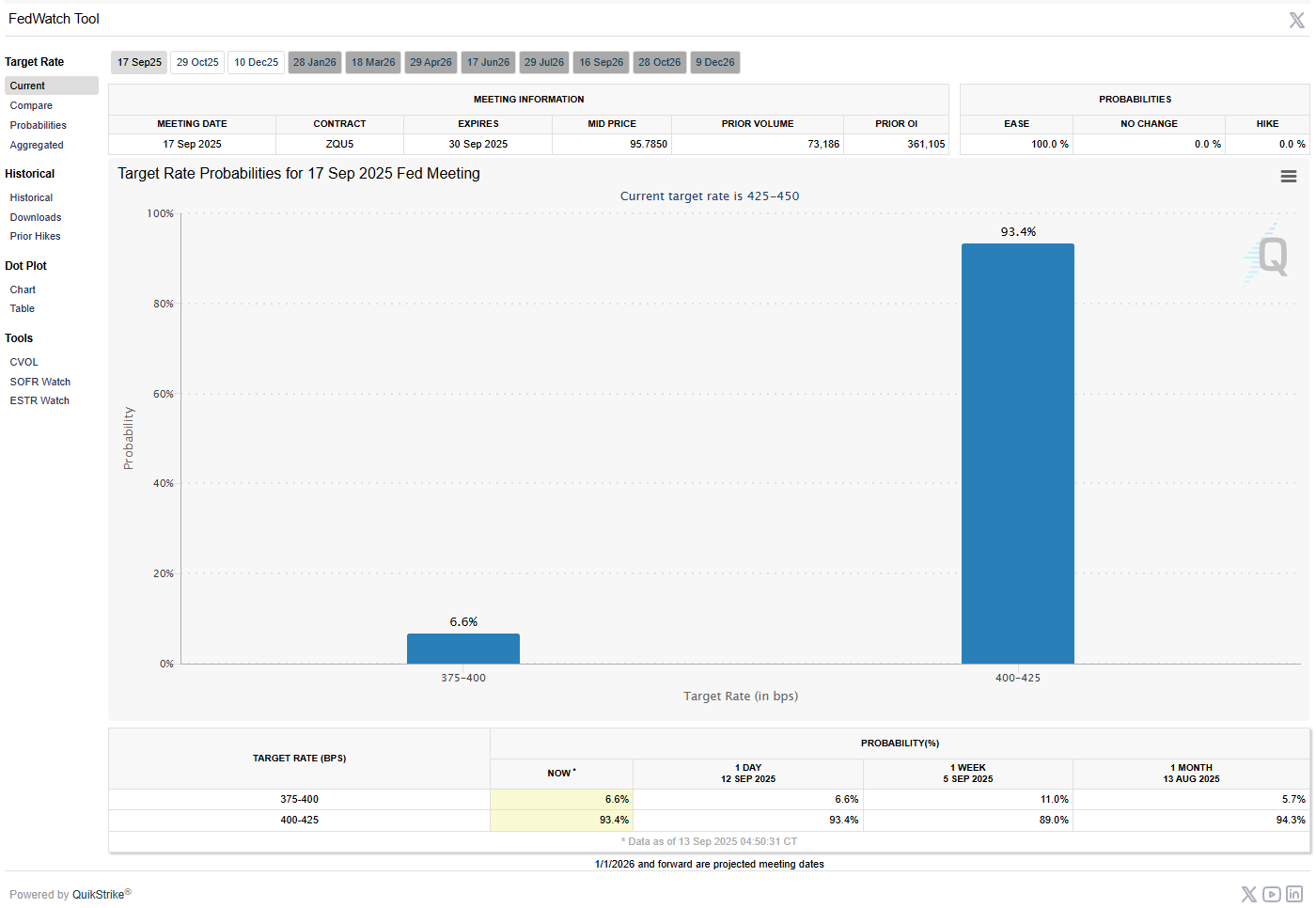

There was plenty of policy theater too. Debate about central bank independence got louder after the latest tussles over personnel—attempts to sideline a sitting governor on one hand and a nominee signaling he’d merely take leave from a White House role on the other. Markets care less about the personalities than the principle: if policy is going to be dragged into front-page politics during an easing cycle, you should at least expect more headline volatility around meetings. For next week, that boils down to a fairly tight set of expectations. A quarter-point cut is baked in. A half-point would require real choreography with friendly outlets beforehand, and we didn’t see it. The updated economic projections will do the heavy lifting—if the dots slide faster toward the market’s view, risk can live with a smaller initial cut because the glidepath matters more than the first step.

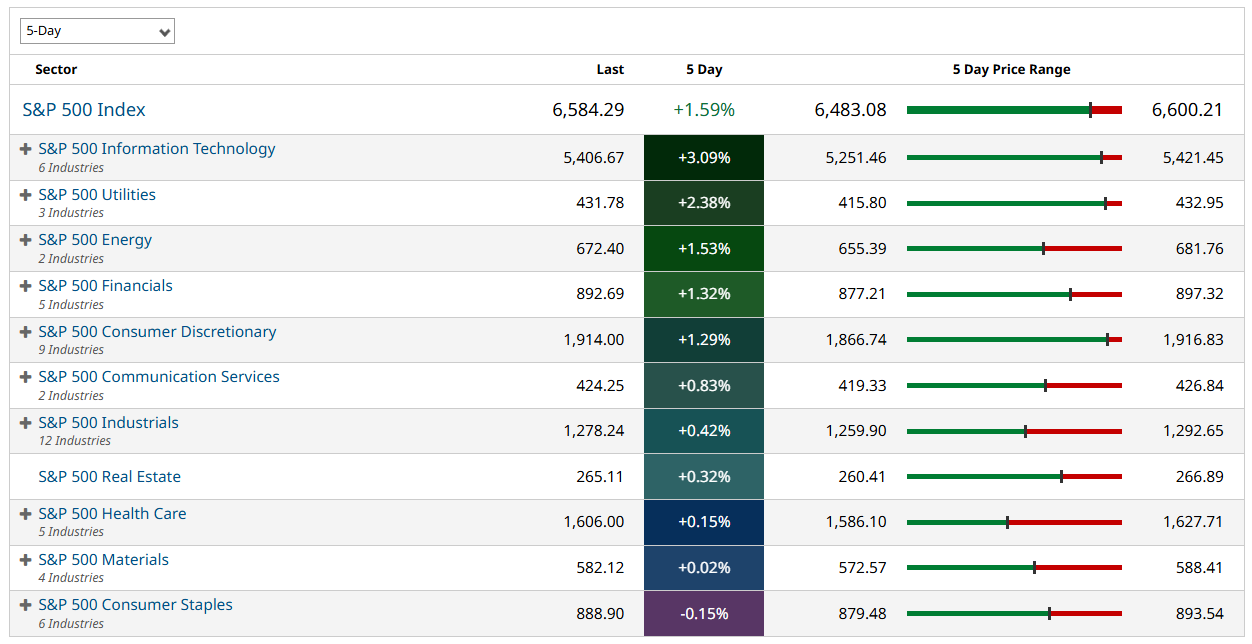

Sector-wise, the scorecard told a coherent story. Technology led, and not just the poster children. The appetite for the plumbing—chips, memory, the boxes and services that enable compute at scale—remained robust. Utilities outperformed again as investors keep telling a story about AI-driven grid demand, though the capex math and rate cases will eventually demand proof. Financials had a good run earlier in the week on a steepening curve theme and constructive commentary at conferences about consumer health; they bled a bit Friday when the 10-year ticked. Healthcare underperformed as political and regulatory crosscurrents kept a lid on enthusiasm. Staples sagged, especially beverages, a combination of recent guidance cuts, downgrades, and investor preference for higher-beta into an easing setup.

Earnings and corporate updates added texture. Department-store and specialty retail names put up some eye-catching gains on beats and improved guidance, though the tariff shadow still sits over import-heavy categories—management teams are talking openly about trying to offset the next leg of duties with vendor negotiations and mix/pricing. On the tech side, not every beat was rewarded—Salesforce’s print and raise looked fine on paper but failed to feed the valuation the street currently wants from software. Hardware-adjacent reports were better received. And in the background, a constellation of AI-linked partnership updates, capacity announcements, and order-book anecdotes kept the animal spirits fed. It’s hard to overstate how much “proof of demand” for compute and memory is doing for investor psychology right now.

Outside the U.S., the map was mostly green, with Asia in front thanks to tech exposure. Japan continued its run as investors leaned into a friendlier policy and fiscal mix and a leadership handoff that markets want to like. China stayed mixed—local demand indicators remain soft, and authorities keep one foot on the brake pedals of speculative froth—but the big platform companies in Hong Kong supplied plenty of beta on the AI tide. Europe advanced but lagged Asia. The ECB stayed in wait-and-see mode with open-minded chatter about further cuts if inflation cooperates, while country-specific politics (notably in France) kept sovereign spreads and growth jitters from fully fading. The Bank of England decision next week, alongside the Fed and the Bank of Japan, will round out a three-pack of policy signals that should set the tone into quarter-end.

One area that deserves a quick nod is credit. Investment-grade primary came heavy, was well-received, and traded up. That’s what you would expect with the 10-year hugging the low end of its year’s range and the policy narrative supportive. High yield followed through, as it tends to do when the market believes the growth slowdown will be managed and not abrupt. If you’re watching for cracks, you watch the lowest-quality tails and the new-issue concessions; neither flashed red this week. You also watch the collateralized and private sleeves for any sign that financing windows are narrowing. They aren’t, not this week.

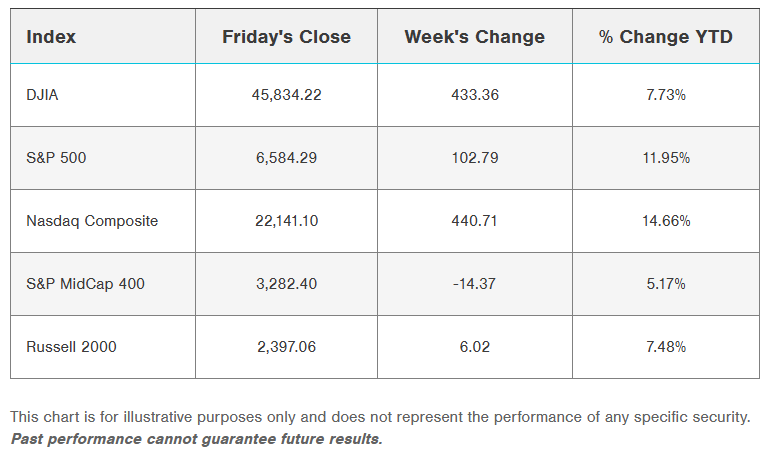

To put numbers to the story, take the dashboard snapshot: the S&P 500 near 6,584 at the Friday bell, essentially unchanged on the day; the Dow around 45,834, down about 274 points; Russell 2000 weaker into the close; the NYSE FANG+ index up roughly forty-odd points. Brent crude near $66.90, gold around $3,681, bitcoin hovering just north of $116k. That’s not a panic tape; it’s a market that tested the ceiling, peeked at a soft confidence read and a nudge higher in long-run inflation expectations, then exhaled into the weekend.

Looking ahead, the calendar is light on quantity and heavy on consequence. The Fed decision and dot plot are the main event. The press conference may matter even more than the statement if Chair Powell leans into the labor-side narrative and frames the cut as pre-emptive insurance rather than a response to a break. Retail sales and weekly claims will offer quick checks on household demand and labor stress. Across the water, the Bank of England and Bank of Japan will try to thread their own needles. On the corporate side, FedEx is one of those prints the macro crowd still respects as a read-through on goods flow and global demand. Then there’s quarterly expiration and the S&P rebalance at week’s end—plenty of mechanical flow to amplify whatever direction the market chooses.

None of this erases the risks. September and October have a way of exposing positioning. The market is threading a fine line between “rate cuts because the labor market is fraying at the edges” and “rate cuts because inflation will glide to target while growth stabilizes.” The former merits a lower multiple; the latter buys time for earnings to catch up. This week’s data kept the latter alive. If you want a simple mental model for the next few sessions, use this: when 10-year yields press toward 4.0% and claims don’t accelerate, buyers show up; when yields pop and sentiment wobbles, we consolidate. If that pattern holds, the path of least resistance into quarter-end remains higher, but the slope is uneven and the runoff channels are well-worn.

The takeaway is straightforward. We’re at—or near—new highs because the path to easier policy is clearer and the AI-heavy parts of the market keep delivering catalysts. We wobbled into the weekend because long rates perked and a confidence gauge reminded everyone that households still feel pinched. The balance of evidence still argues for gentle easing, not emergency action; for growth that cools, not collapses; and for leadership that remains concentrated but is slowly leaking into the edges. That’s an investable mix, provided you treat each down-day as a test of sponsorship rather than a referendum on the entire advance.

Next week, the Fed writes the next few pages. The market has already penciled in most of the plot. If the committee’s dots move in the direction the strip has already mapped, Friday’s hesitation will look like what it was—position management ahead of a binary headline. If the dots resist and the guidance sounds tentative about labor, we’ll chop until the data forces the issue again. Either way, the burden of proof has shifted. For now, dips keep finding buyers, and strength still breeds rotation rather than euphoria. That’s how durable tapes usually behave.

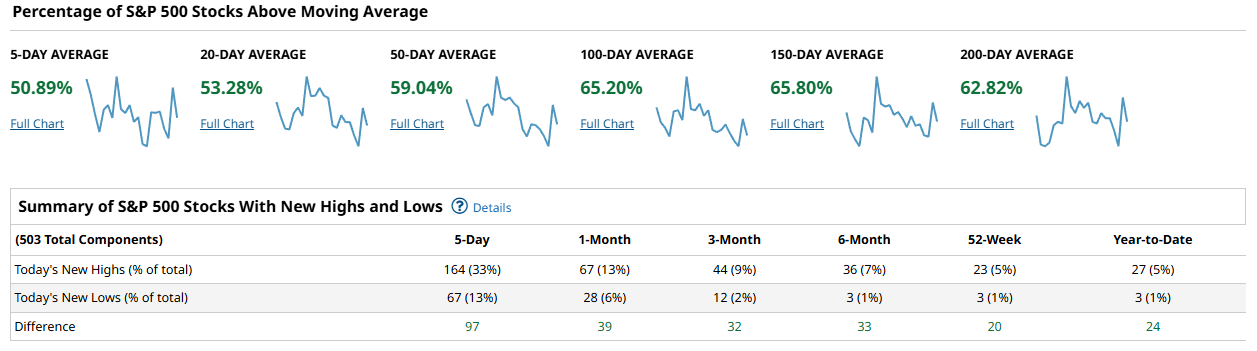

Weekly Benchmark Breakdown

S&P 500: under-the-hood tone is constructive. Roughly six in ten constituents sit above their 50-day and 200-day moving averages, and the 5-day new-high/new-low spread printed +97 (164 highs vs. 67 lows). Even out on the 6-month window, highs beat lows 36 to 3. That’s not euphoric, it’s “healthy trend with rotation,” which tends to travel well if indices chop sideways.

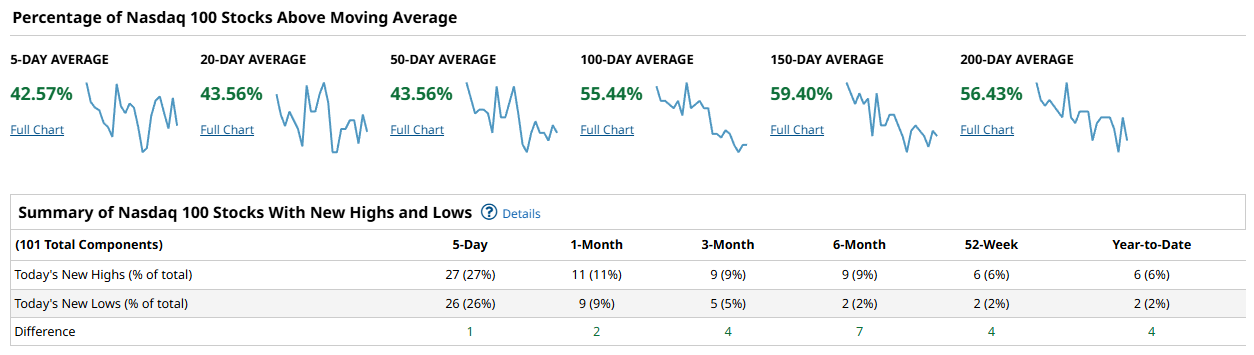

Nasdaq-100: still the laggard on participation. Only ~44% are above their 50-day and ~55% above the 100-day. New-high/new-low differentials are positive but thin (5-day +1; 1-month +2). Translation: leadership is patchy and rallies are being driven by a shorter list of names. Treat strength here as selective rather than blanket.

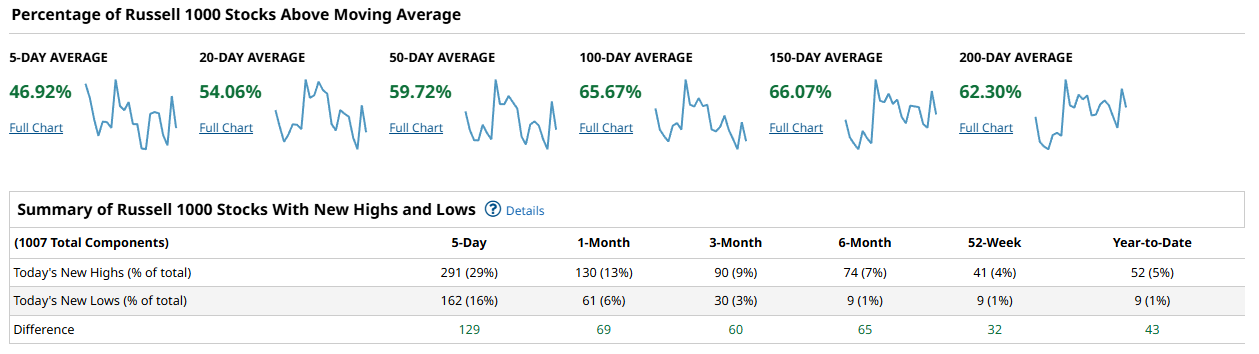

Russell 1000: broadening out nicely. Just under 60% are above the 50-day and ~62% above the 200-day, and the 5-day highs/lows spread is a hefty +129 (291 highs vs. 162 lows). The positive skew persists across 1- and 3-month lookbacks. That’s the kind of participation you want if you’re betting on rotation beyond the mega-caps.

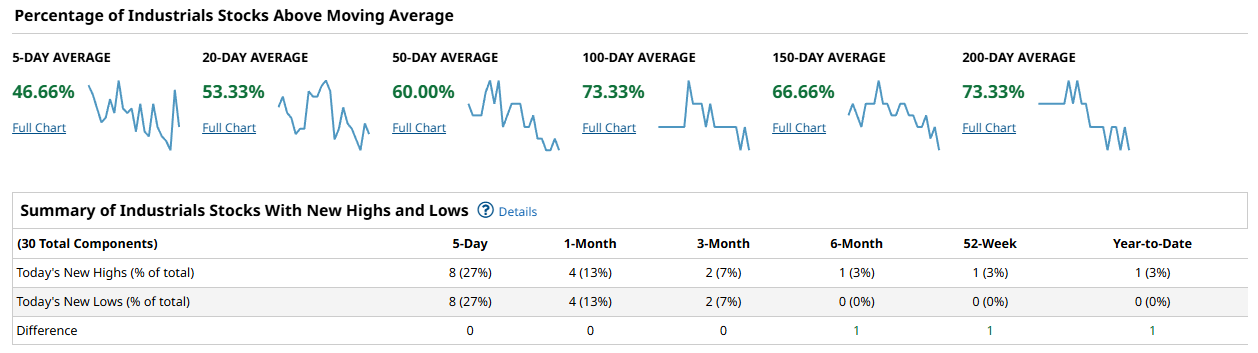

Dow 30: balanced to flat near-term. Short-term highs and lows were a stalemate (8 vs. 8), leaving the 5-day spread at zero. Longer windows still lean positive, with more members above the intermediate/long moving averages, but the message is “pause,” not “push.”

Netting it out: breadth tilts bullish across the broad market (SPX/R1K), is neutral in the Dow, and remains the soft spot in the NDX. That mix argues for fading weakness in quality large caps while keeping a bid under the broad tape and being more selective in the mega-cap growth complex.

US Investor Sentiment Report

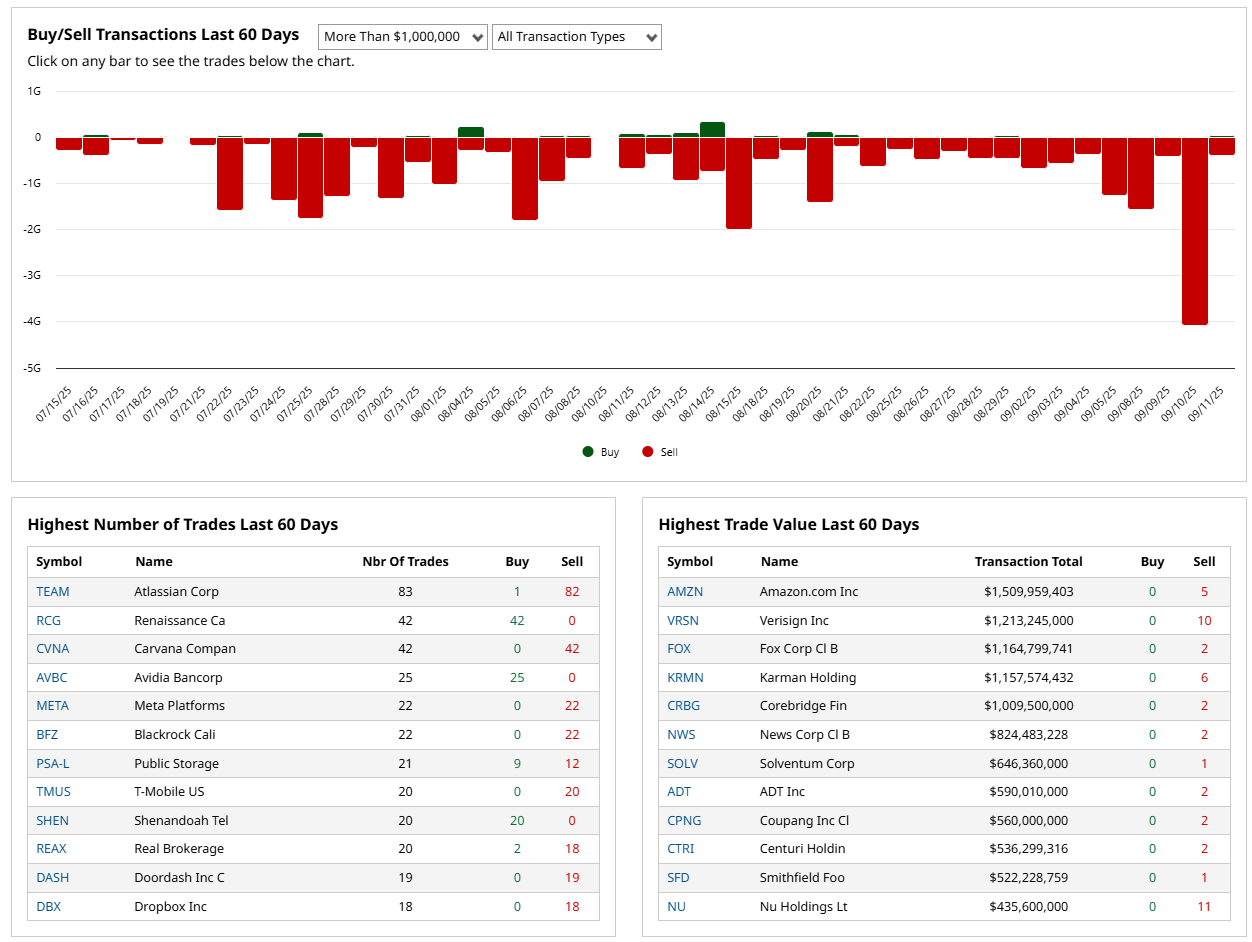

Insider Trading

Insider trading occurs when a company’s leaders or major shareholders trade stock based on non-public information. Tracking these trades can reveal insider expectations about the company’s future. For example, large purchases before an earnings report or drug trial results might indicate confidence in upcoming good news.

The insider tape is leaning risk-off. The 60-day bars are mostly red with only a couple of tiny green blips—classic distribution, not hedging. That’s insiders using liquidity to sell into strength rather than stepping up on dips.

Where it shows up: heavy, one-way clusters. Atlassian has 80-plus prints with virtually no buys, Carvana is all sells, and you see the same pattern in Meta and T-Mobile. On the big-dollar board, the marquee tickets—AMZN, VRSN, FOX, KRMN, CRBG, NWS, SOLV, ADT, CPNG—are almost entirely sales. Tech and Comm Services carry most of the weight, with Consumer and Financials not far behind.

Filter the noise: transfers, gifts, and plan “subscriptions” don’t tell you anything about risk appetite. Once you strip those out, genuine open-market buying is scarce. That absence matters.

Netting it out, insiders are treating rallies as exits while the index level stays elevated. That’s a caution flag for near-term risk and a reminder to be selective with growth and crowded mega-cap exposure.

%Bull-Bear Spread

The %Bull-Bear Spread measures the gap between bullish and bearish investor sentiment, often from surveys like AAII. It’s a contrarian indicator—extreme optimism may signal a coming pullback, while extreme pessimism can hint at a potential rally. Large positive or negative spreads often mark market turning points.

The AAII bull–bear spread slid to about -21% this week, a meaningful deterioration from last week and the third straight down tick. We’ve been swimming below zero for most of the year, so the tape is no stranger to pessimism, but this push back through -20% tells you retail sentiment has soured again. It isn’t a March-style capitulation (those prints pushed into the mid-to-high -30s), yet it’s bearish enough to matter.

In practice, I treat a sub-(-20%) spread as a contrarian tailwind only if price starts to cooperate. If the indices hold recent ranges, breadth stabilizes, and vol remains cool, this kind of sentiment can fuel a reflexive bid over the next few weeks. If, instead, the spread stays negative and widens while prices leak lower, it’s just confirmation that risk appetite is deteriorating and rallies should be sold. So I’m watching for higher lows in the majors, a pause in new lows, and continued compression in VIX/MOVE; the compression in vol won’t last forever but if we get that, I’ll lean into quality and liquidity with tight risk. If not, patience wins—negative sentiment without price confirmation is just background noise that usually forces many to chase.

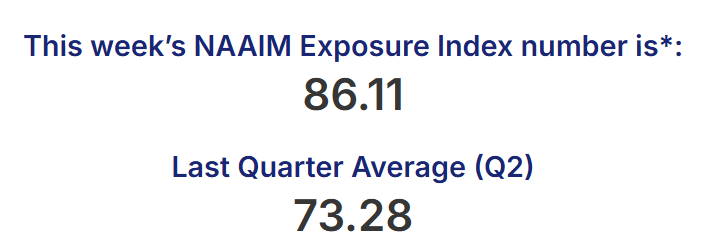

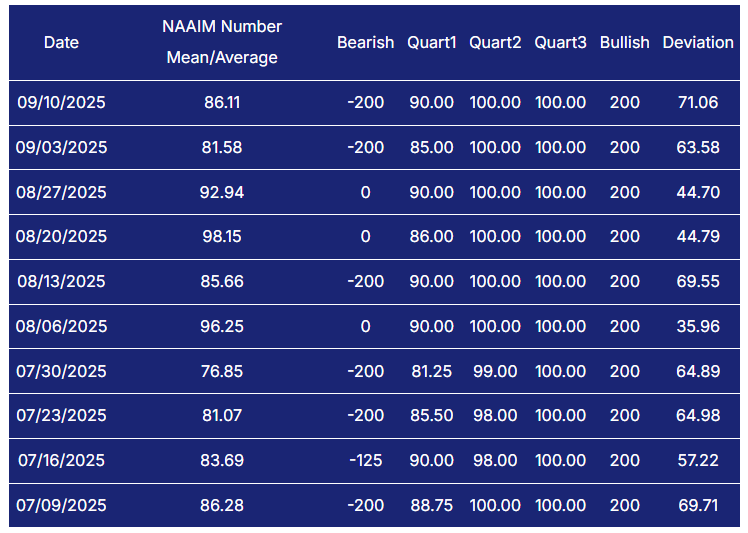

NAAIM Exposure Index

The NAAIM Exposure Index (National Association of Active Investment Managers Exposure Index) measures the average exposure to U.S. equity markets as reported by its member firms. These are typically active money managers who provide their equity exposure levels weekly. The index offers insight into how much these managers are investing in equities at any given time, ranging from being fully short (-100%) to leveraged long (up to +200%).

NAAIM ticked up again to 86 this week (from 82), which keeps active managers heavily net long. We’re still living in that 80–100 corridor that’s characterized most of the summer. Two things matter:

High exposure, high dispersion. The “deviation” jumped into the 70s, and the range spans -200 to +200. Translation: plenty of managers are pinned long, but positioning is barbelled—some fully risk-on, a minority outright short or tightly hedged. That mix usually dampens crash risk but also limits upside “fuel” because many pros are already in.

Contrast with retail. This stands in sharp contrast to the AAII bull–bear spread that just pushed deeper negative. Pros are buying dips; individuals are leaning defensive. That’s a classic wall-of-worry backdrop if price holds.

How I use it: above ~80 says the path of least resistance is still sideways to up provided breadth doesn’t crack. If NAAIM rolls over toward 60 or lower into weakness, that’s when pullbacks tend to extend. Until then, I’d expect managers to defend first support and rotate rather than de-risk in size—think “buy the wobble,” not “catch the falling knife.”

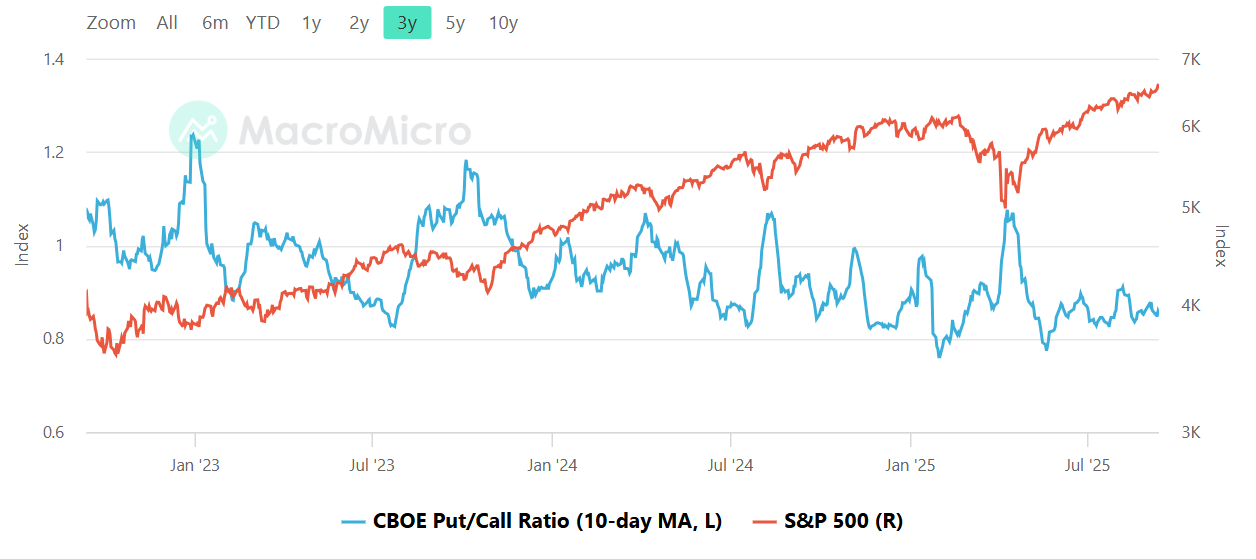

CBOE Total Put/Call Ratio

CBOE's total put/call ratio includes index options and equity options. It's a popular indicator for market sentiment. A high put/call ratio suggests that the market is overly bearish and stocks might rebound. A low put/call ratio suggests that market exuberance could result in a sharp fall.

The 10-day CBOE total put/call is sitting in the 0.85–0.90 neighborhood—firmly in the “comfortable” zone. That’s not euphoric, but it’s definitely not fearful. Historically, this series is a great contrarian tell:

Sub-0.90 tends to show complacency into strength; upside can continue, but risk/reward compresses because there isn’t much short-gamma or hedging fuel left to convert into a squeeze.

>1.00–1.10 spikes almost always show up near short-term lows and mark better entries for buying risk.

Right now we’re closer to the former. The pattern the past few months has been shallower highs and lows in the ratio as price grinds up—classic late-advance behavior. My takeaway: worth carrying some protection (puts or collars) into strength and saving the “buy the dip” mentality for a day when this 10-day lifts through 1.0 on a selloff. If we instead sink toward 0.80, that’s the kind of reading that has preceded minor tops—I’d tighten risk and avoid chasing breakouts until sentiment resets.

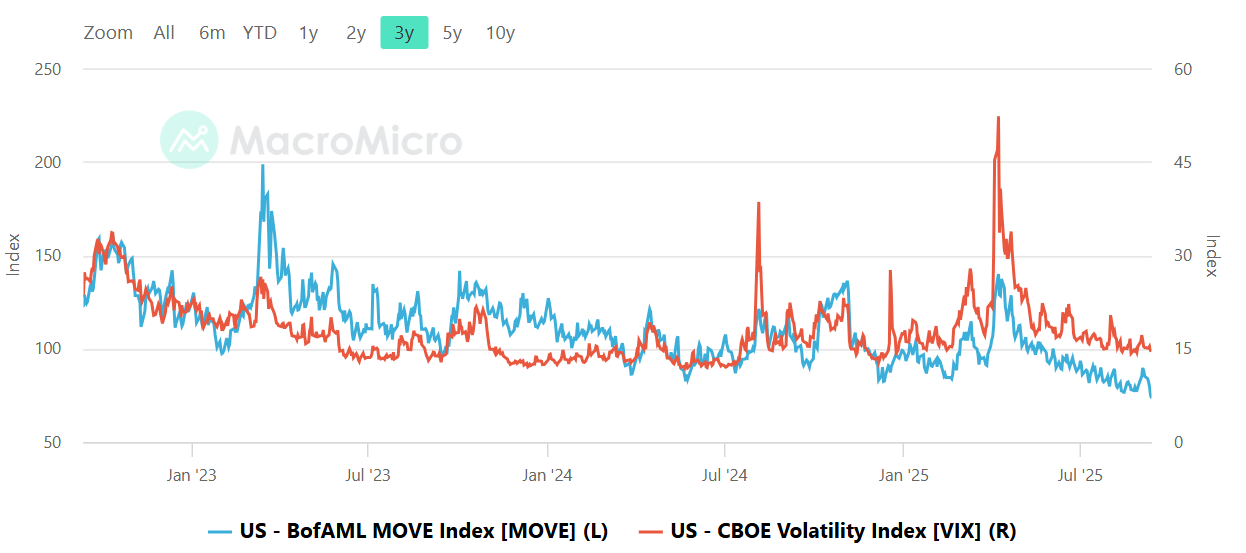

Equity vs Bond Volatility

The Merrill Lynch Option Volatility Estimate [MOVE] Index from BofAML and the CBOE Volatility Index [VIX] respectively represent market volatility of U.S. Treasury futures and the S&P 500 index. They typically move in tandem but when they diverge, an opportunity can emerge from one having to “catch-up” to the other.

Bond vol is melting and equity vol is dozing. The MOVE index has slid back toward the low-100s and is leaking lower, while VIX is parked in the mid-teens. That combo says the market is treating the recent macro wobble as noise, not regime change: rates traders aren’t stress-testing the curve anymore, and equity hedging demand is subdued.

Two implications:

Carry > Convexity (for now). Low/declining MOVE supports tighter financial conditions easing at the margin (friendlier for duration-sensitive groups and banks). With VIX ~13–16, mean-reversion and spread carry tend to work; breakouts need a catalyst to run.

Cheap insurance. Compressed vol into CPI/Fed/tariff headlines is exactly when you buy optionality, not after the spike. Short-dated index puts or light collars are inexpensive; they hedge the air-pocket risk that often appears when VIX drifts sub-15.

What would change the story? A MOVE pop back above ~120 usually leads equity vol higher with a lag; that’s your early warning. Conversely, if MOVE keeps dribbling lower and VIX can’t clear 17–18 on bad news, dips likely keep getting sponsored.

Bottom line: we’re in a low-vol carry regime with a macro calendar that can wake VIX quickly. Lean long with risk controls, harvest carry, and pre-position a little convexity while it’s still on sale.

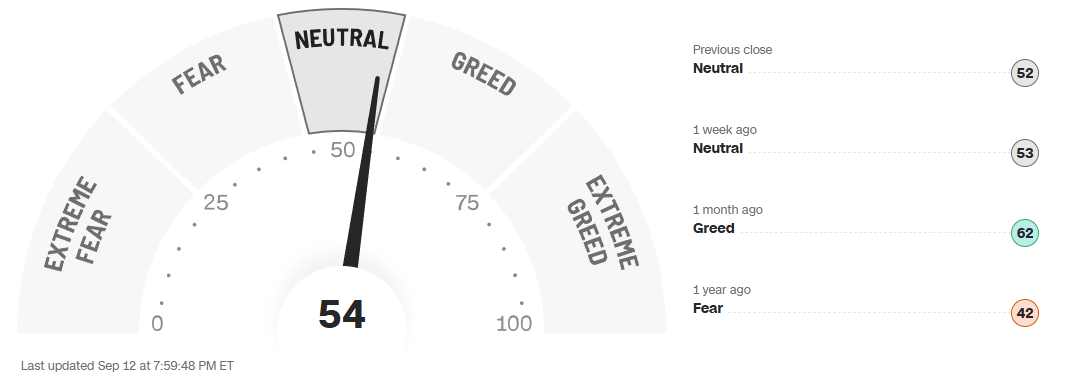

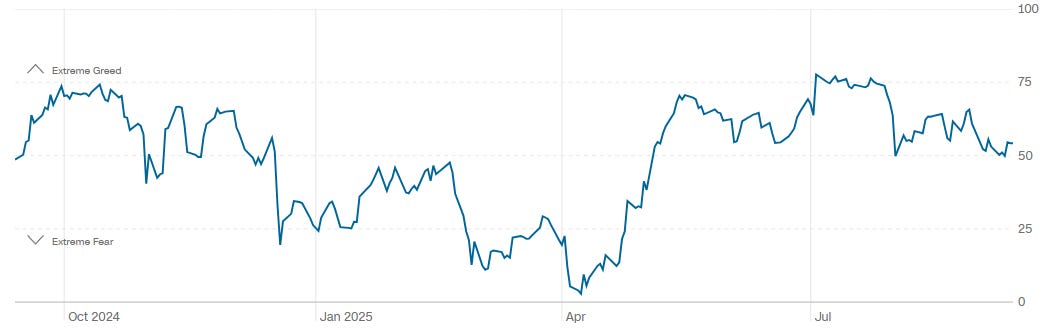

CNN Fear & Greed Constituent Data Points & Composite Index

The CNN Fear & Greed dial is parked around 54. That’s neutral with a slight bullish lean—up a hair from last week, down from last month’s “greed.” In practice, that means the crowd isn’t euphoric anymore, but it’s not scared either. Think two-way tape: breakouts don’t run as far without help, and dips tend to get bought—but selectively, not blindly.

We’re miles from the contrarian extremes on this one (no 80+ “fade it” signal, no sub-20 “back up the truck” either), so I treat this as context, not a trigger. In a neutral regime, the playbook is simple: trade levels, respect rotation, manage risk. Lean into improving breadth and new leadership on pullbacks; fade obvious overextensions into resistance. Patience > hero trades here.

Social Media Favs

Social sentiment offers a real-time view of investor mood, often revealing market shifts before traditional indicators. It can signal momentum changes, spot emerging trends, and gauge retail investor impact—especially in high-volatility names. Tracking sentiment around events or earnings provides actionable insights, and when layered with quantitative models, can enhance predictive accuracy and risk management. Sustained sentiment trends often mirror broader market cycles, making this data a valuable tool for both short-term trades and long-term positioning.

Institutional S/R Levels for Major Indices

When you’re a large institutional player, your primary goal is to find liquidity - places to do a ton of business with the least amount of slippage possible. VolumeLeaders.com automatically identifies and visually plots the exact spots where institutions are doing business and where they are likely to return for more. It’s one of the primary reasons “support” and “resistance” concepts work and truly one of the reasons “price has memory” - take a look at the dashed lines in the images below that the platform plots for you automatically; these are the areas institutions constantly revisit to do more business.

Levels from the VolumeLeaders.com platform can help you formulate trades theses about:

Where to add or take profit

Where to de-risk or hedge

What strikes to target for options

Where to expect support or resistance

And this is just a small sample; there are countless ways to leverage this information into trades that express your views on the market. The platform covers thousands of tickers on multiple timeframes to accommodate all types of traders.

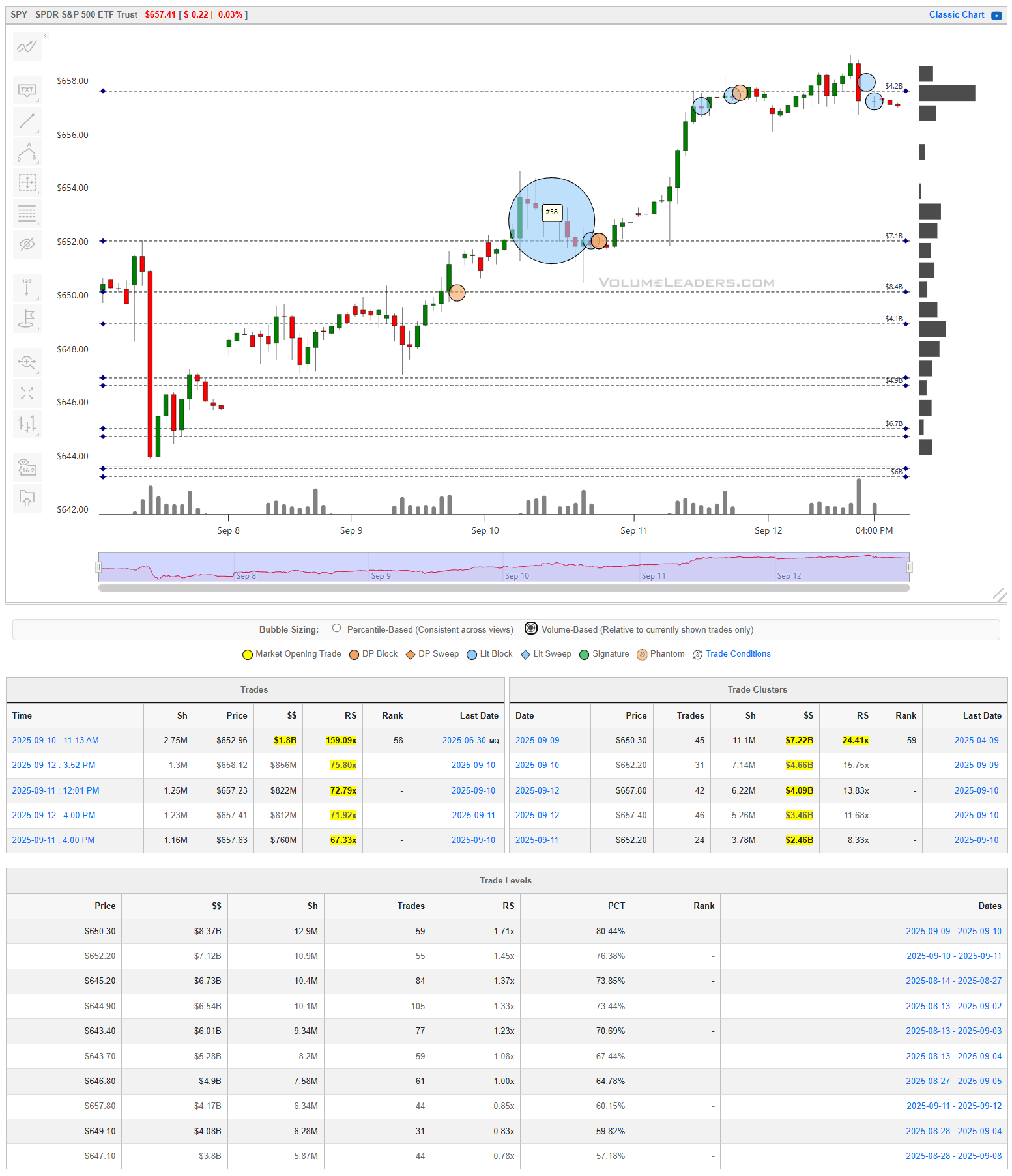

SPY

SPY’s tape is about as straightforward as it gets. We spent the front half of the week building higher lows into a chunky, high-volume shelf around 652. The brief balance there did its job while someone loaded-up #58: once buyers pushed through, the market spent time accepting higher into 657–660 before closing out the week at the what could be the first real supply band in this area.

If $657 holds on a dip then momentum likely stays intact. If it slips, the volume profile is thin down to $653 and invites a class breakout re-test before we spend a little time filling in the LVN. Lose that and we likely get to test the buyer’s conviction at #58. That’s the real line in the sand for this leg. A decisive break through there means inventory isn’t being defended hands control back to sellers and opens the door to a full give-back into $650-$647.

Tactically, I’d rather buy weakness that stabilizes above 655 than chase strength into 660. If we reject 659–660 and slide back under 657, I’d expect a rotation to 655 and possibly lower where responsive buyers should show. If, instead, we get time and volume above 660, I’ll treat it as acceptance and look for the quick extension toward 662–664.

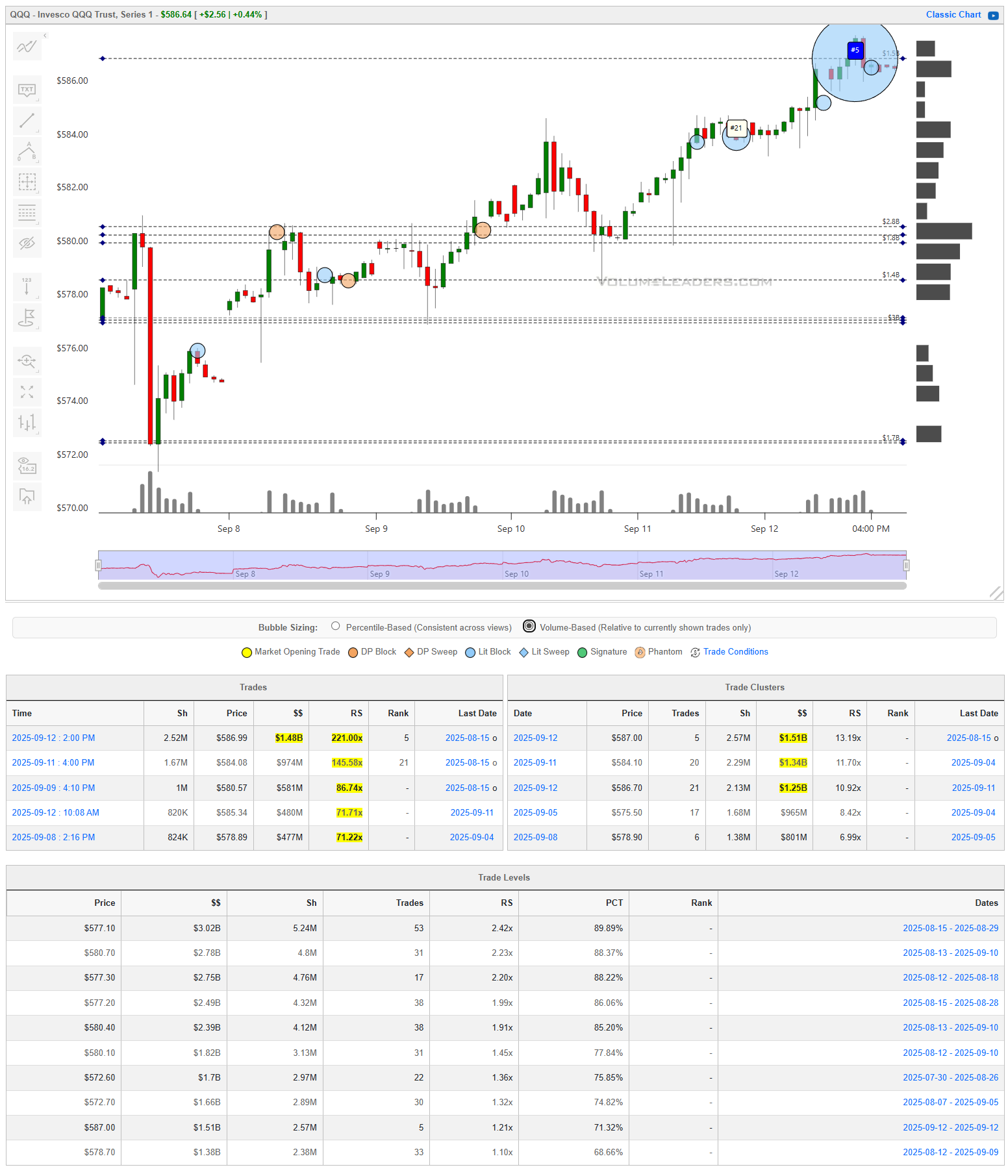

QQQ

QQQ spent most of the week stair-stepping out of a tight 577–580 range and finished by tagging the ceiling near 586–587 with a fat cluster of late-day prints. That tells me two things: there’s real two-way interest up here, and the next move is likely to be decided by whether we can accept above 587 or get pushed back into the prior balance.

The structure underneath is clean. There’s a fresh shelf at 581 that was tested from above and accepted; buyers didn’t take their foot off until 584 which invited #21 before lifting again for the measured move, closing the week at the highs - not a ton bearish about that. So 584 becomes my first support on dips with 581 looking a lot more stable. Below that sits the heavier volume band at 577–581, which was the breakout platform—lose that and the door reopens to a full rotation toward 572.

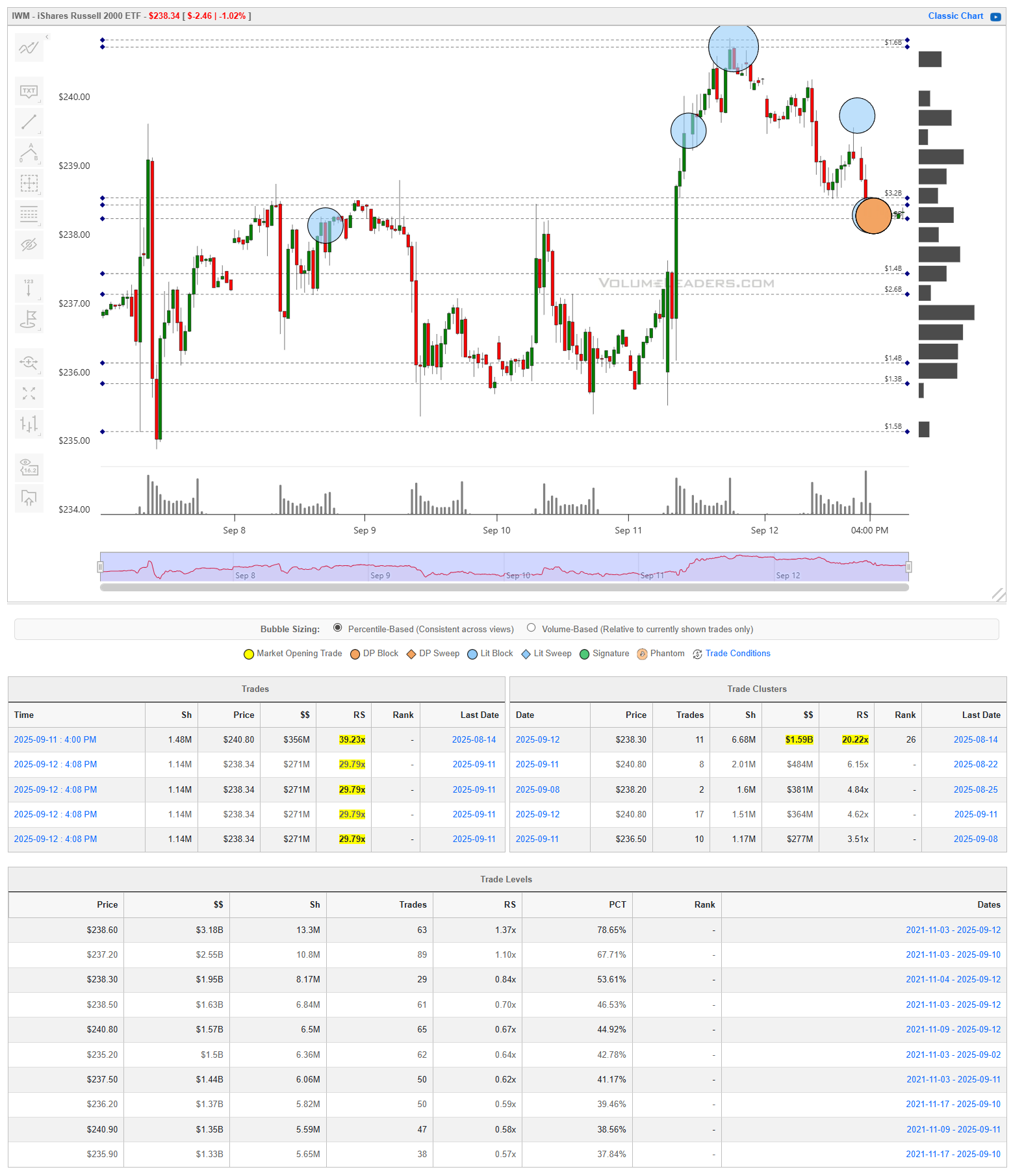

IWM

IWM had the big squeeze mid-week and then gave most of it back into Friday’s close. Sellers showed up right at the prior spike zone near 241 (multiple heavy prints at the highs), and the fade stopped right on a chunky volume shelf at 238.4–238.8. That shelf is now the battleground. Hold it, and we can rebuild a base for a push back through 240; if sellers reclaim that the path reopens to 237 then 236. IWM bulls really want to see the prior resistance zone flipped into support - the 1M share print at the bell on Friday might already have an idea about the next destination but we’re going to have to wait until Monday to see the reaction.

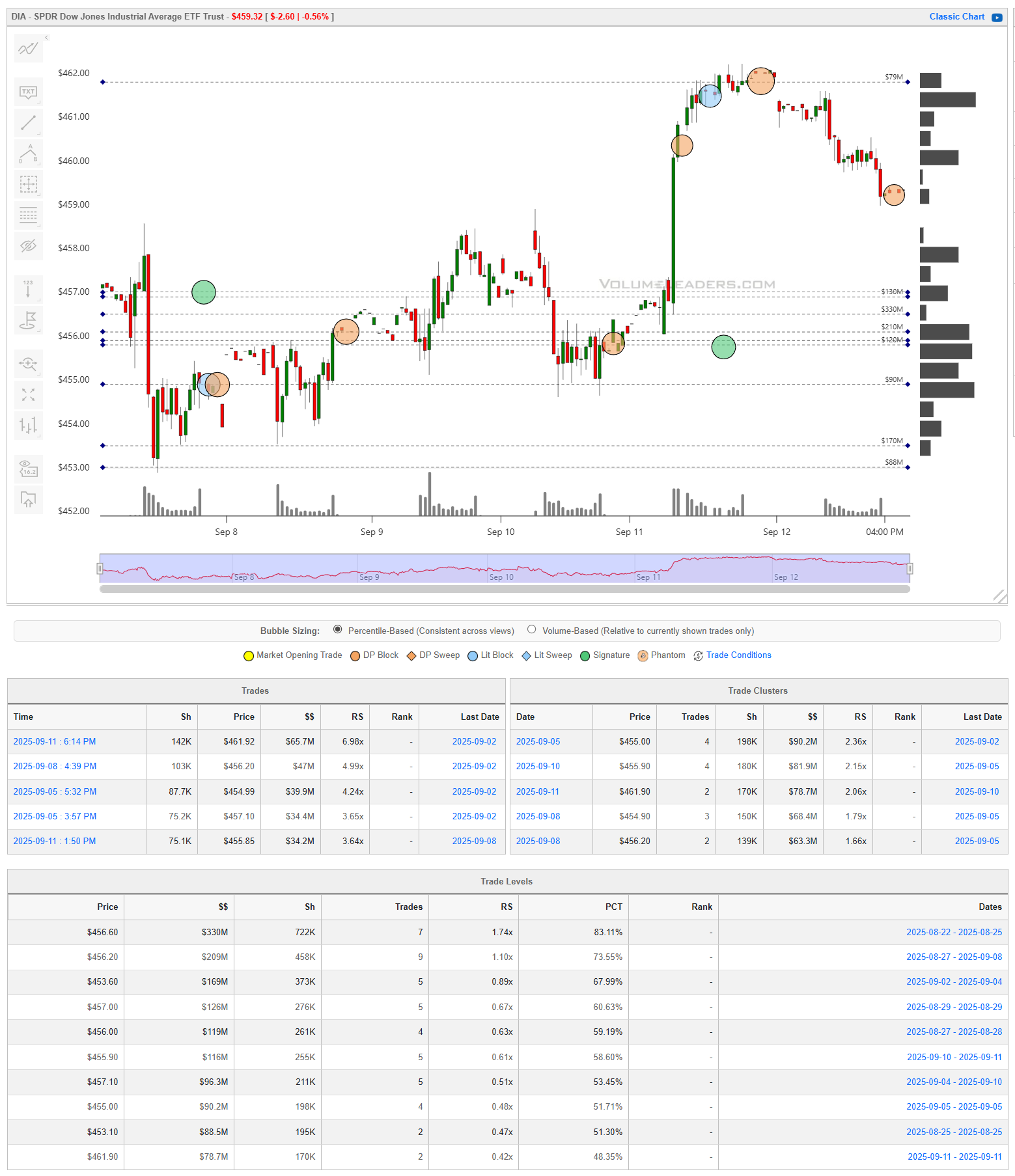

DIA

DIA did the classic “squeeze and fade.” We ripped straight through the 458s on 9/11, tagged the prior supply zone up near 461.5–462 (multiple large prints right at the spike), and then bled lower into Friday. The pullback seems to be working it’s way all the way back to 457 at this point. Hold above it and we can rebuild for another push into weekly highs. Lose 457 and you’re still not in terrible shape - you just end up back in the soup where a bunch of business is being done but control remains a coin toss. 455-457 will tell the tale early next week with roughly $5-rotations on either side to play for.

Tactically: I’m a buyer only on a controlled dip that stabilizes ≥456 with a tight stop under 455.8, looking to scale out 459ish and leave a trailer for 462. If we open soft and can’t reclaim 456 on a 30–60 minute basis, I’ll stand aside since we’ve seen no evidence of real sellers actively present. In short, 456 is the fulcrum; above it, repairs and a retest higher, below it, expect a walk back through the prior balance.

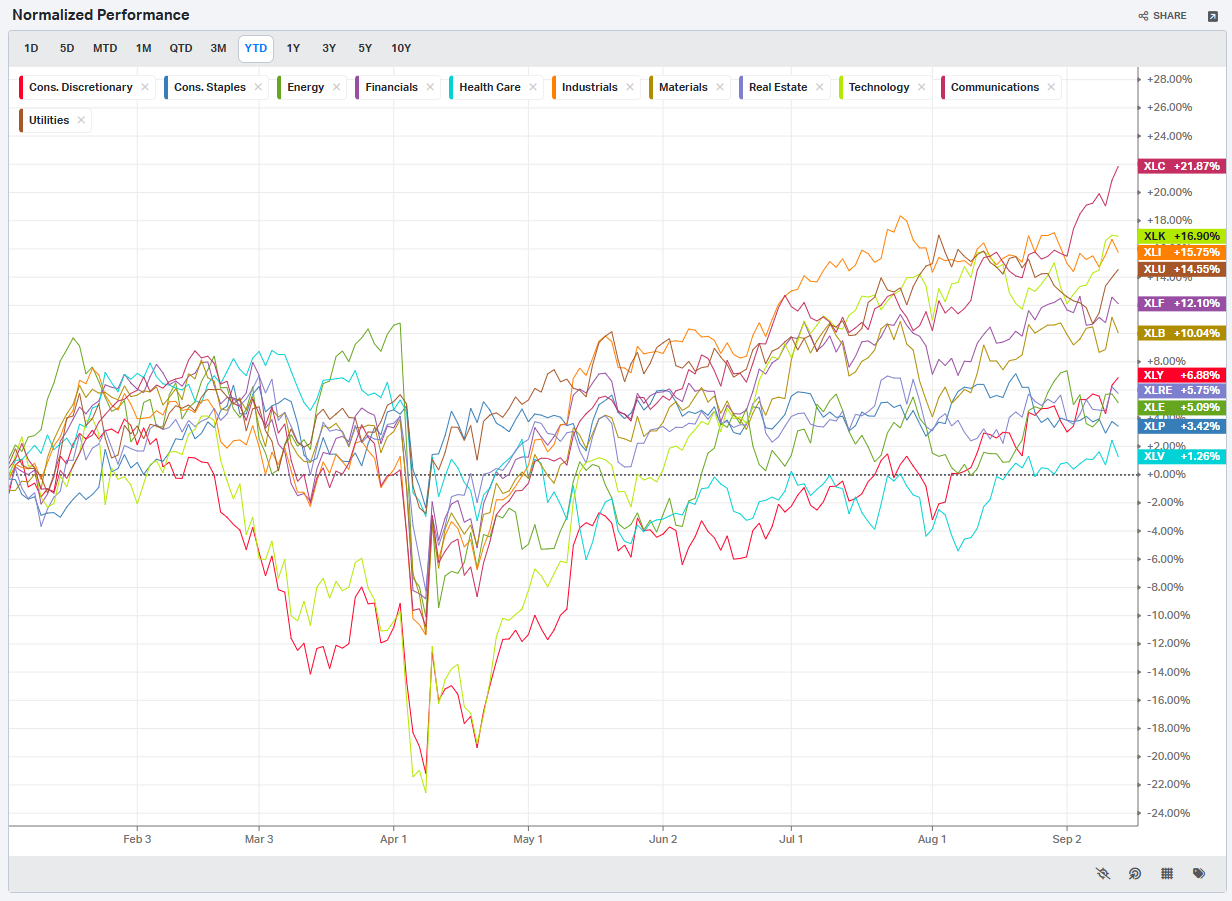

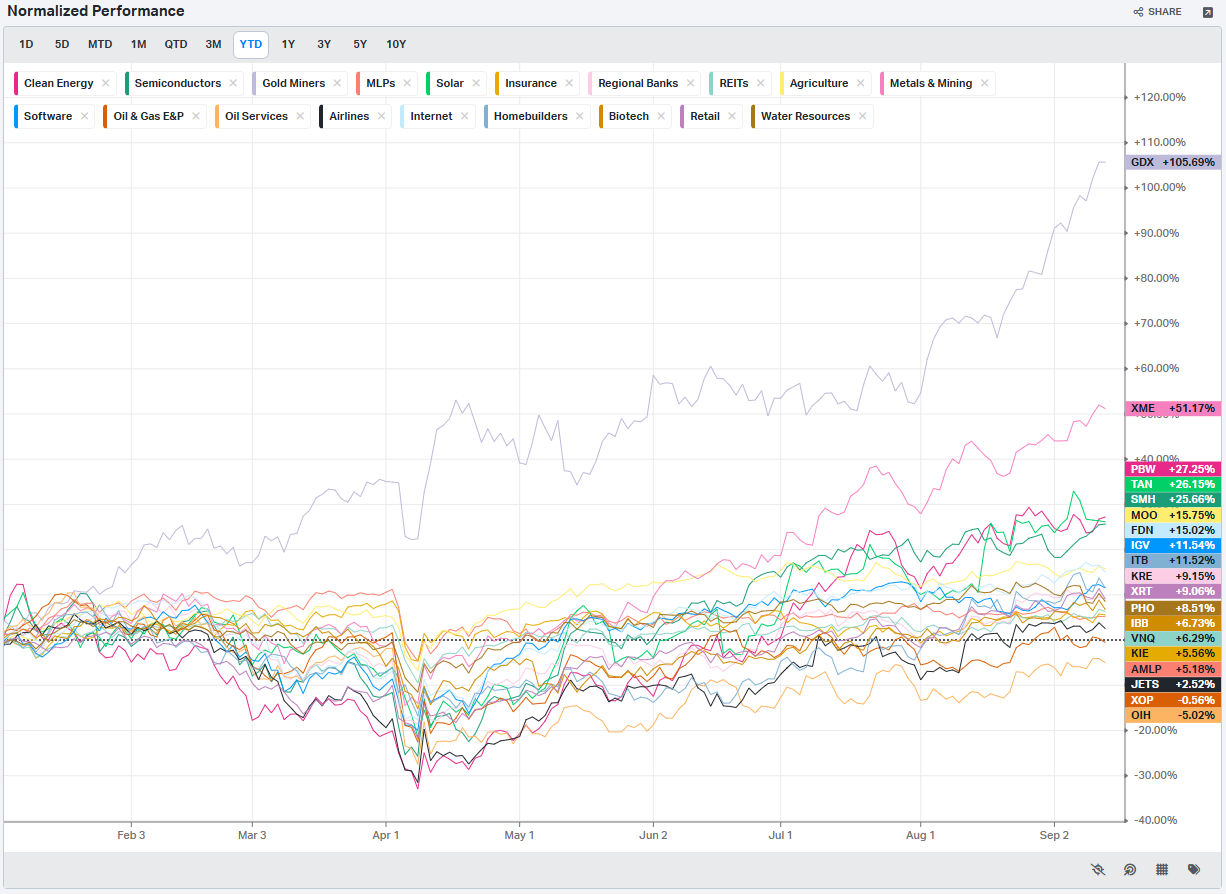

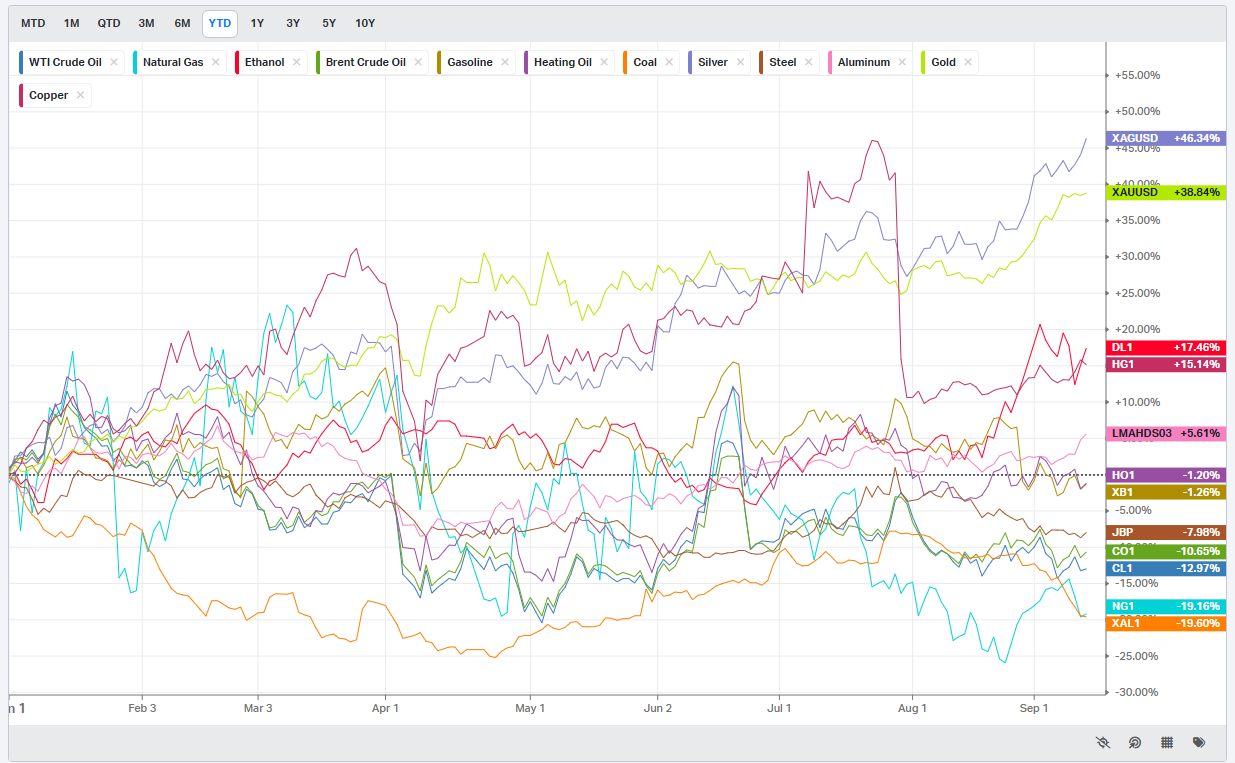

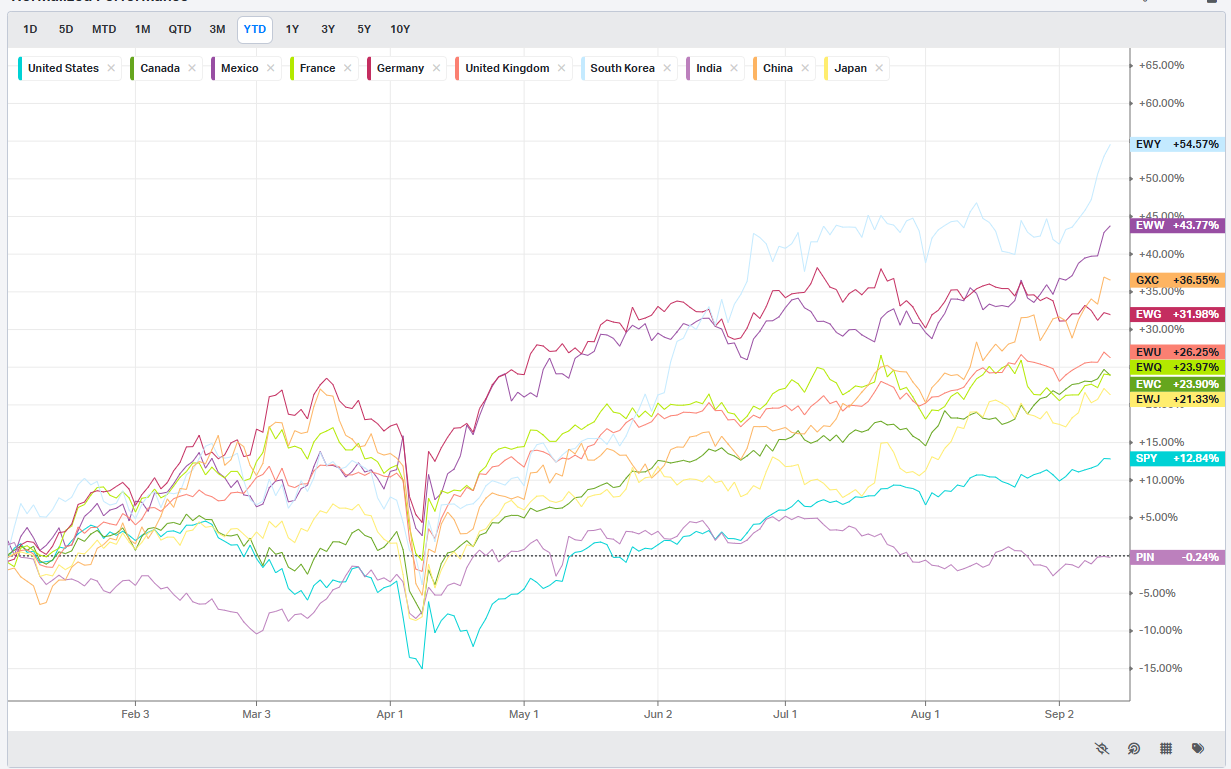

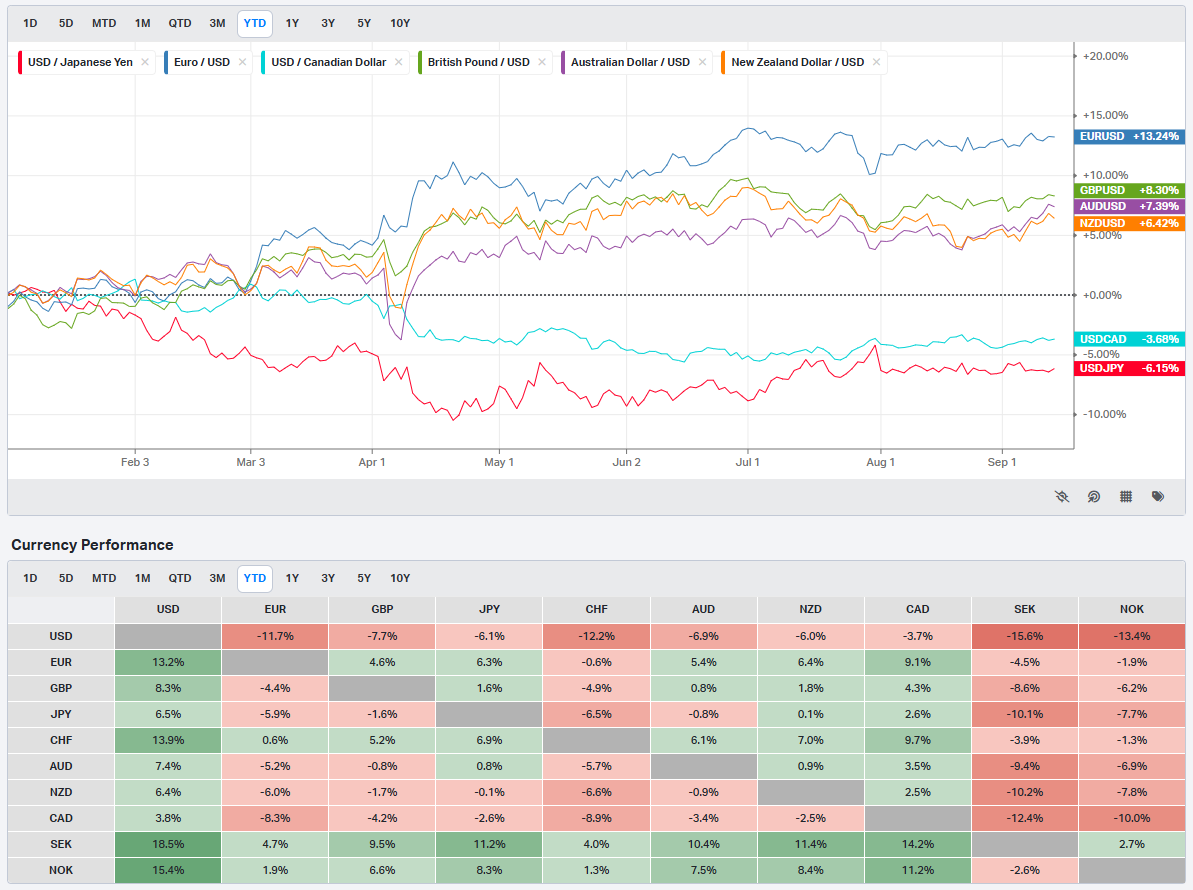

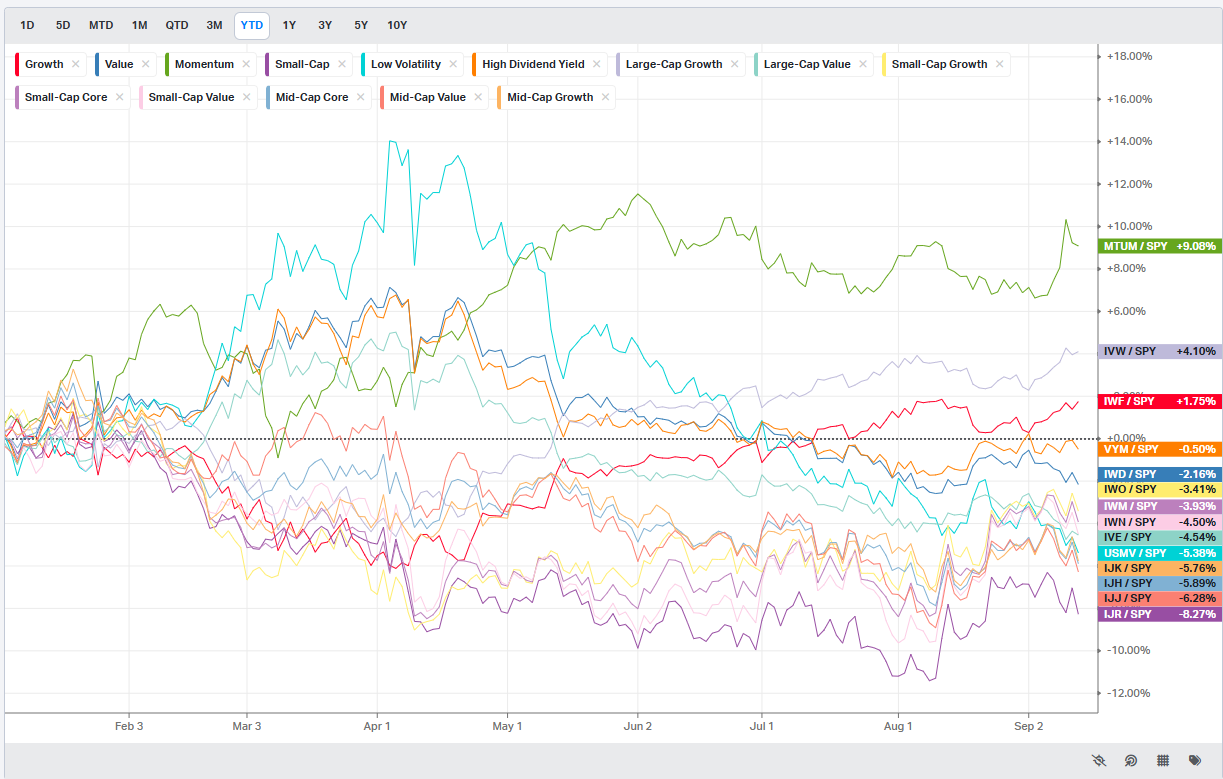

Summary Of Thematic Performance YTD

VolumeLeaders.com offers a robust set of pre-built thematic filters, allowing you to instantly explore specific market segments. These performance snapshots are provided purely for context and inspiration—think about zeroing in on the leaders and laggards within the strongest and weakest sectors, for example.

S&P By Sector

S&P By Industry

Commodities: Energy & Metals

Country ETFs

Currencies/Major FX Crosses

Factors: Style vs Size-vs-Value

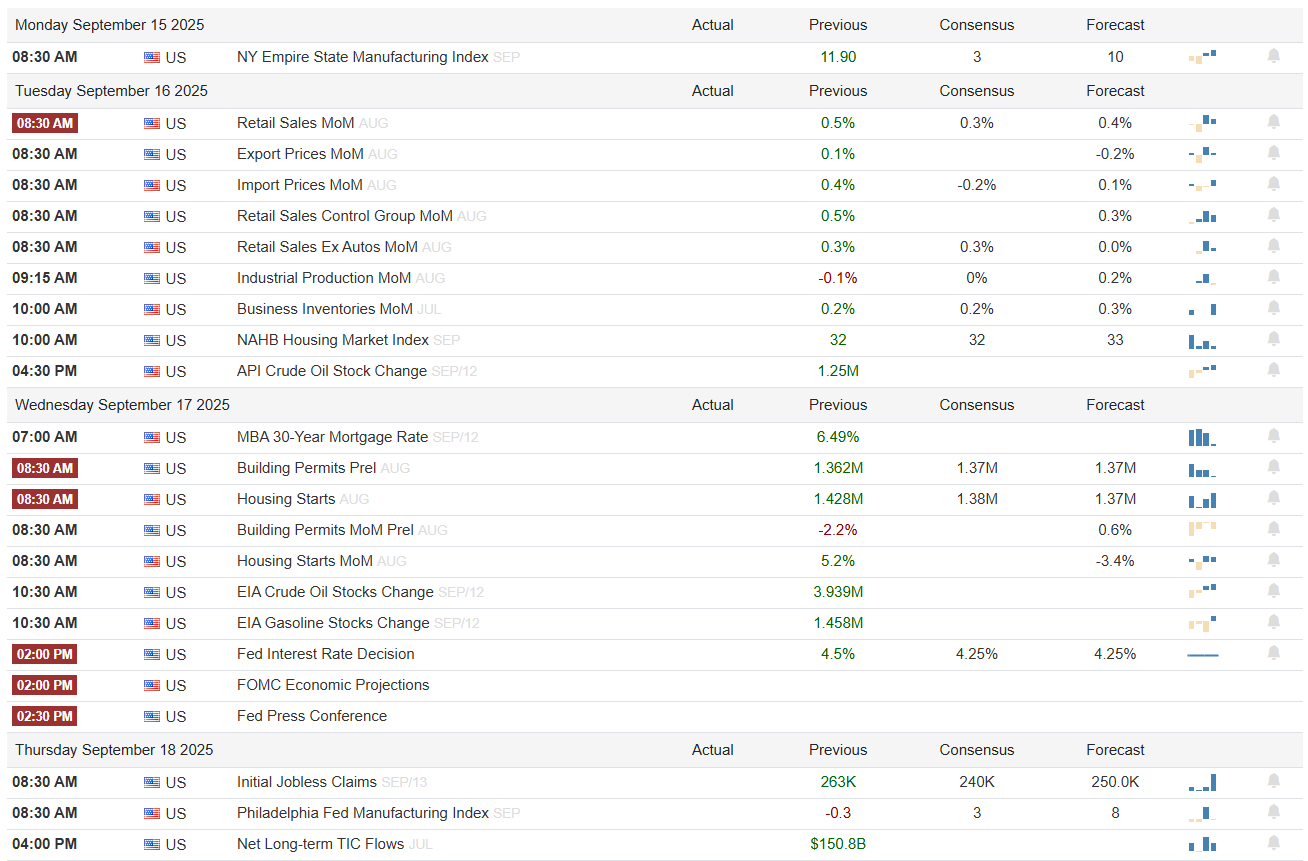

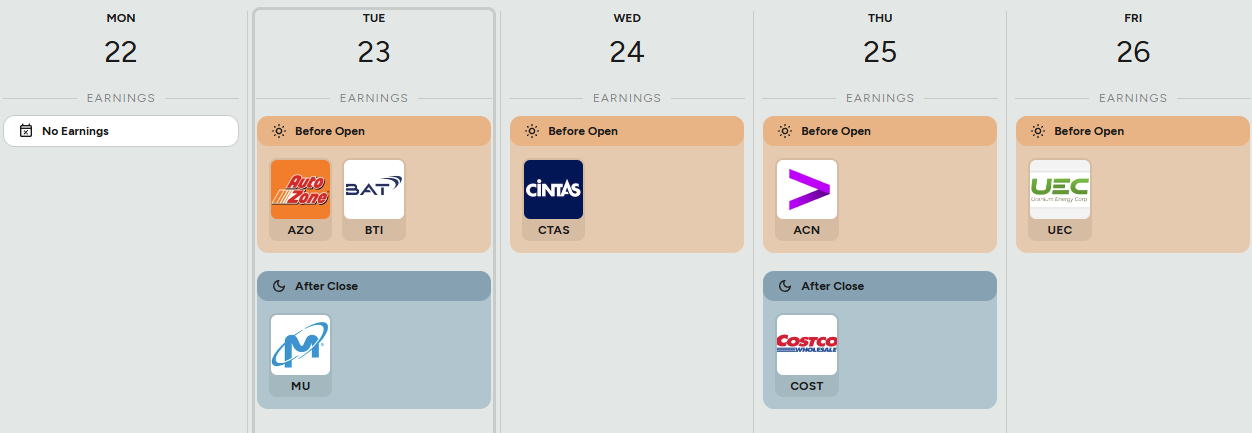

Events On Deck This Week

Here are key events happening this week that have the potential to cause outsized moves in the market or heightened short-term volatility.

We open with the NY Empire State survey Monday. It’s a decent, high-frequency read on factory orders and pricing, but the main event doesn’t really begin until Tuesday. That morning is the growth pulse check: Retail Sales (watch the “control group”—it feeds GDP nowcasts), Export/Import Prices (a clean read on traded-goods inflation amid tariff noise), Industrial Production, Business Inventories, and NAHB homebuilder sentiment. If sales cool while prices ease, the market will lean into the “soft landing + easier Fed” narrative and favor duration, megacap growth, and housing. A hotter control group and firmer import prices would do the opposite—press the front end and rotate toward cyclicals.

Wednesday is a two-part story. First, housing and energy in the morning—Mortgage Rates, Housing Starts/Permits, and the weekly EIA inventory set. With mortgage rates retreating, any pop in permits or starts would reinforce the budding housing-beta bid we saw this week. A larger-than-expected crude build would keep a lid on energy; a surprise draw and stronger gasoline stocks would give the complex a bounce. Then the main course: the FOMC rate decision, Summary of Economic Projections, and Powell’s presser. Markets are positioned for a 25 bp cut and a “measured” path. The risk isn’t the cut—it’s the dots and the tone. A shallower 2025–26 path or a hard “data-dependent” refrain keeps the curve steepening bid alive and supports banks and defensives; an aggressive glidepath lights a fire under long duration and high multiple growth. Watch the 2s/10s spread and the dollar’s first reaction—those two will set sector tone into quarter-end.

Thursday cleans up with Initial Claims and the Philly Fed survey—both timely barometers for labor and manufacturing momentum—plus TIC flows after the close, which matter for the Treasury supply/demand debate. Claims drifting lower alongside a firm Philly print would argue the slowdown is orderly; a claims pop and a weak diffusion index would have the market re-pricing growth risk again.

In earnings-land, Tuesday brings AutoZone and BAT before the bell, then Micron after the close. AutoZone is a clean consumer read with pricing/margin tells for discretionary; Micron is the week’s swing factor for semis and AI-adjacent capex—watch bit supply commentary, HBM mix, and capex outlook. Wednesday features Cintas before the open—an underrated read-through on small-biz hiring and wage pressure. Thursday has Accenture pre-market and Costco after the close. Accenture is a high-beta thermometer for enterprise IT spend and AI services bookings; Costco is gold-standard consumer staples + basket inflation surveillance. Friday’s quiet, with Uranium Energy pre-market for the commodity crowd.

Tactically, the first move on Tuesday’s sales and Wednesday’s dots likely gets faded; the second move tends to stick. I’m watching: (1) 10-year yield versus ~4.1%—break lower extends the duration/growth bid; hold and bounce helps value/cyclicals. (2) Housing Starts/Permits momentum for confirmation in homebuilders and building products. (3) Semis into Micron—if management tightens supply talk and keeps HBM capacity disciplined, the group re-rates; if pricing softens, expect a quick factor unwind. (4) Dollar reaction post-FOMC—down dollar is a tailwind for multinationals, materials, and EM; firm dollar crimps those and helps domestics.

Bottom line: it’s a policy and consumer-centric week. If retail sales cool and the Fed sketches a gentle path, dips in quality growth and housing look buyable. If sales run hot and the dots don’t budge, expect a quick duration shakeout and a rotation day into cyclicals and financials. Either way, keep position sizes honest into Wednesday 2:00–2:30pm ET—the real trend for the back half of September will be defined in that window.

Market Intelligence Report

MIR Part 1: The Backdrop

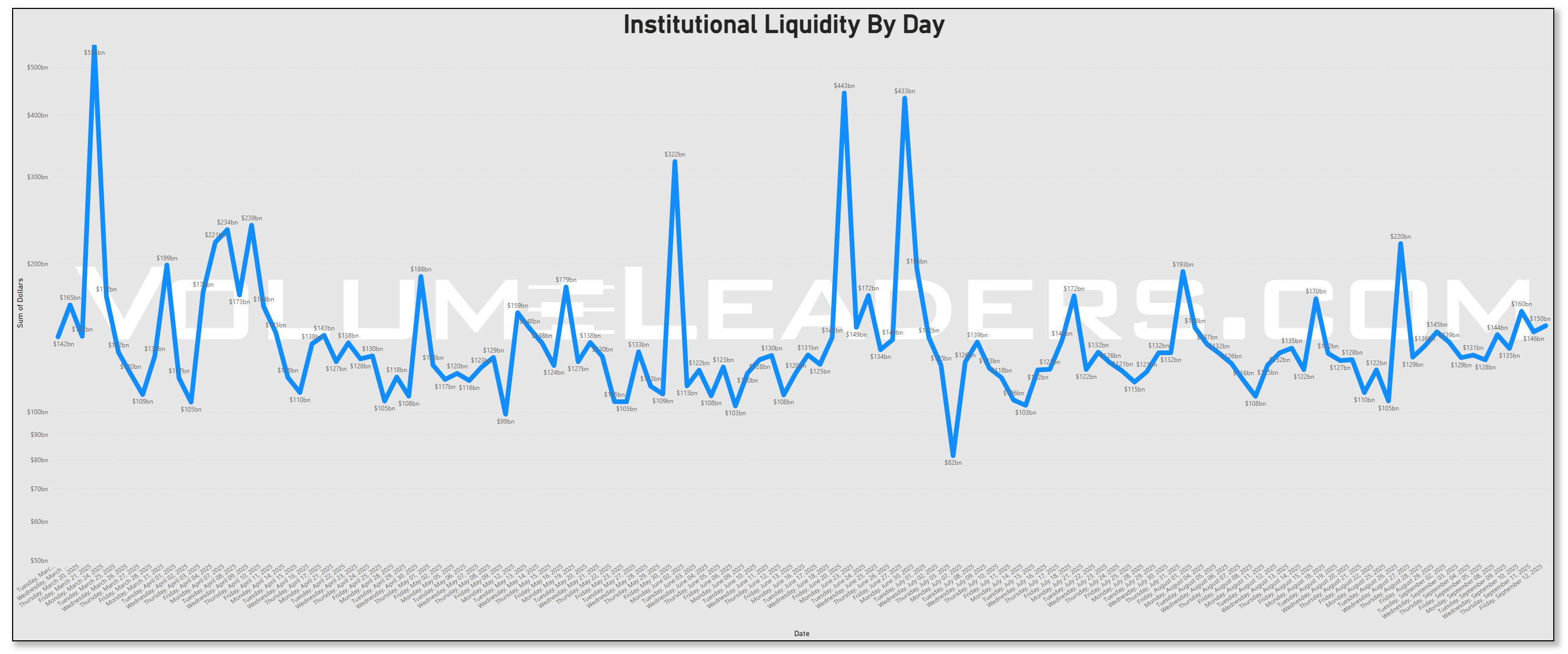

Liquidity first. “Institutional Liquidity by Day” series shows the summer lull is done. We’ve transitioned from choppy, under-$120b sessions into a steadier cadence of $130–$170b with a couple of outsized spikes. That’s classic post-Labor Day behavior: desks are back, risk meetings are happening again, and bigger tickets are printing. Said differently, positioning—not headlines—is starting to drive price again.

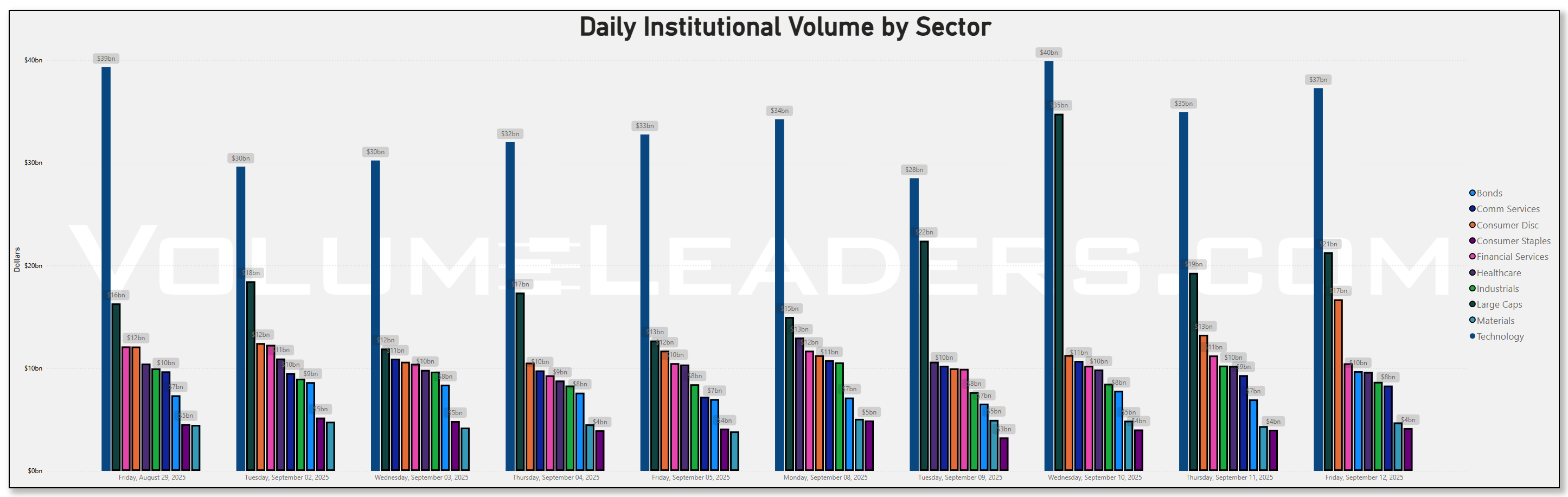

Now look at the daily sector dollars. The standout is Wednesday: Technology and the Large-Cap complex lit up just ahead of the two-day index ramp into week’s end. When Tech and broad beta get sponsored in the same session, that’s not retail chasing—it’s allocation. If you need a map for coming sessions, treat Wednesday’s intraday ranges as nearby pivots. If the market respects those ranges on pullbacks, that sponsorship is still live; if we slip back through them, it’s a tell that Wednesday was more one-off than regime or someone found a greater fool and was able to unload large chunks of inventory.

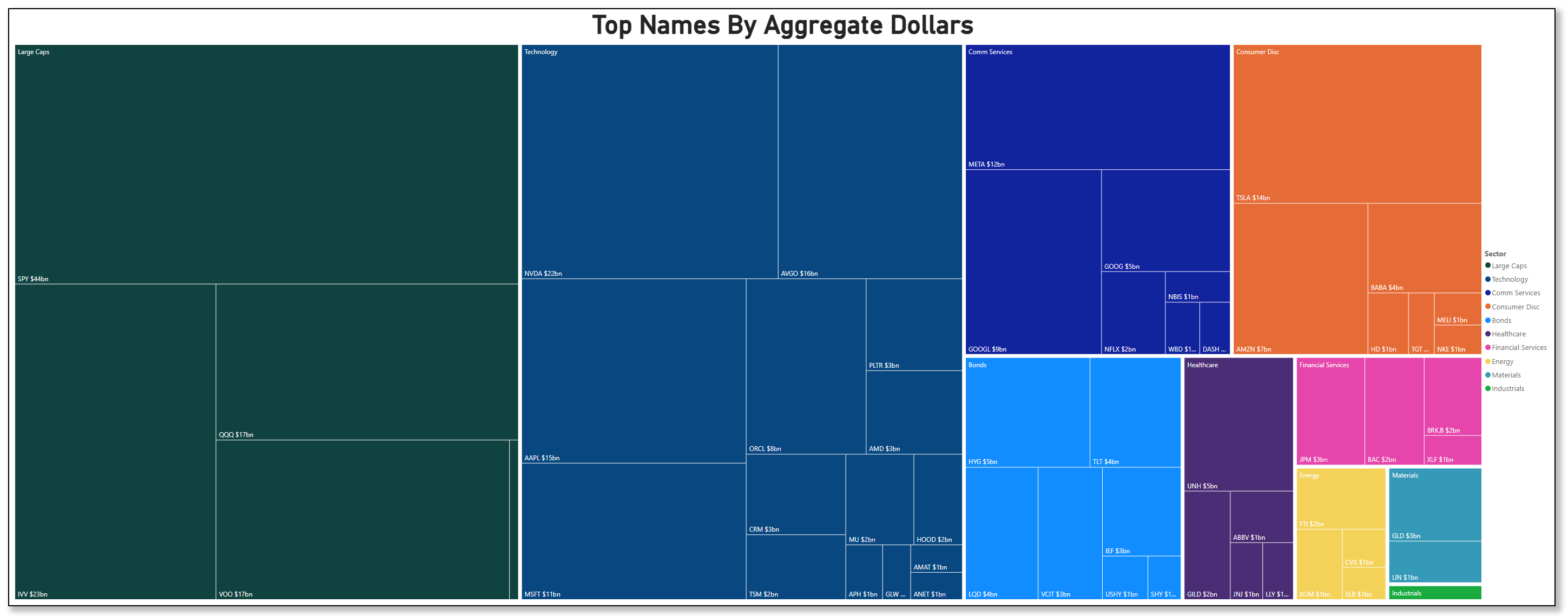

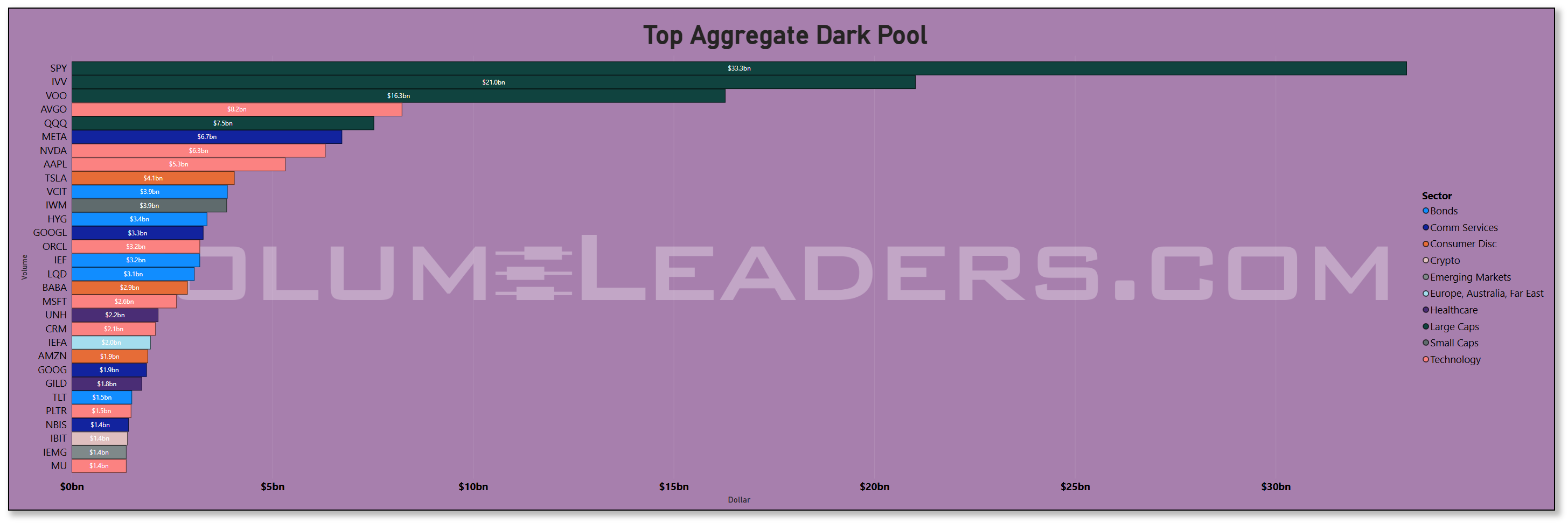

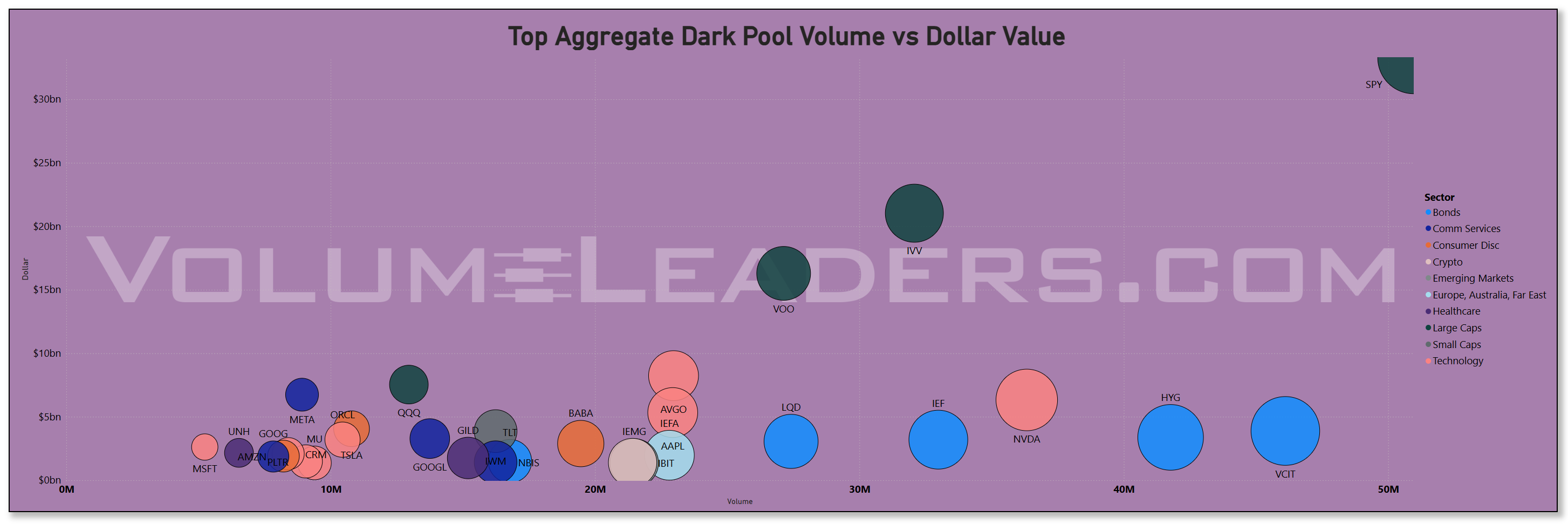

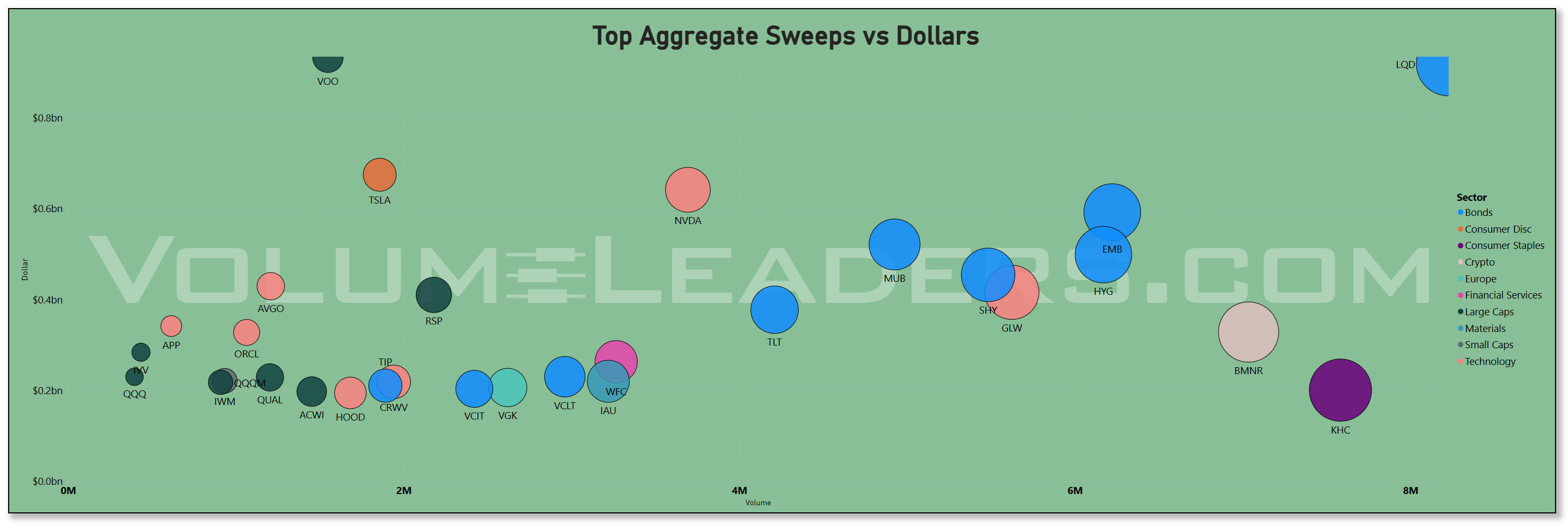

The “Top Names by Aggregate Dollars” treemap makes the sponsorship obvious: SPY/IVV/VOO on the index side, then NVDA/AVGO/AAPL/MSFT/META/GOOGL and TSLA on the single-name side. That’s the megacap spine of this tape. A few China ADRs popping onto the board (e.g., BABA) after sharp price runs—my sense is that the dramatic pops have caught some impatient buyers who are going to get their feet held to the fire a little so I wouldn’t rush-in here but I would start keeping one eye on them.

Cross-asset tells are important this week. Credit is everywhere on our boards. LQD, VCIT and HYG/USHY sit near the top of both aggregate flow and sweeps, with SHY showing up too. That’s a classic barbell: add intermediate-IG carry (LQD/VCIT), take some high-yield spread (HYG/USHY), and keep front-end bills (SHY) as a ballast. It lines up with the macro: softer labor data pushed the market to lean harder into near-term Fed easing, which naturally boosts appetite for duration and quality carry. The August jobs report added just 22k payrolls with unemployment up to 4.3%, reinforcing the “cooling, not collapsing” narrative and nudging the curve to steepen.

Futures pricing followed: after that print, traders firmed up September cut expectations and even entertained a larger first move before quickly converging on 25 bps with additional easing likely into year-end—exactly the kind of path that pulls asset allocators into IG credit and keeps beta on a short leash rather than a full sprint.

The dark-pool tape backs this up. SPY/IVV/VOO dominate (broad beta under the surface), but the interesting bit is how large the off-exchange prints were in the credit sleeves and a handful of megacaps. NVDA/AVGO/AAPL/META/GOOGL had meaningful hidden-hand activity—steady accumulation rather than frantic chasing—while VCIT/LQD/HYG also posted chunky dark-pool dollars. When the hidden tape agrees with the lit tape, I give the flow more weight.

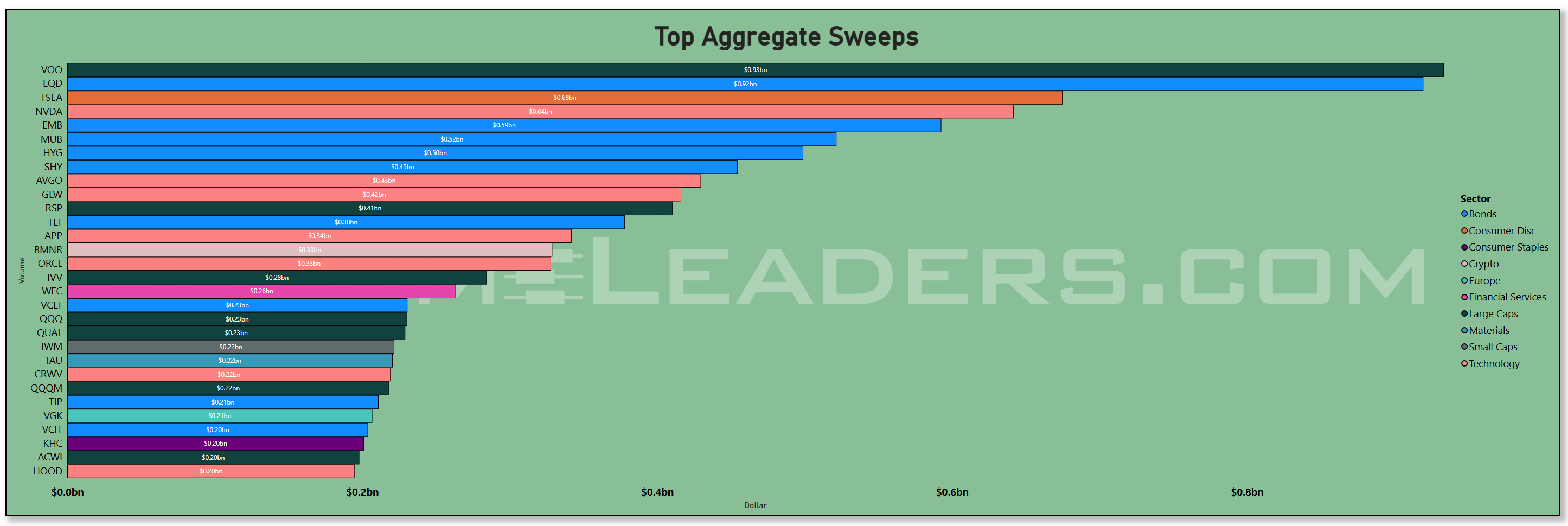

Sweeps add a tactical layer. VOO and LQD topping the sweep board says the fastest money was leaning into index beta and IG carry on a time-sensitive basis. TSLA and NVDA were next tier—those two remain the speculative pressure valves. SHY, EMB and MUB up there as well tell you institutions weren’t going “all gas, no brakes”: they kept ballast in the mix (front-end Treasuries, EM debt, and munis). That’s an “ease with a net” posture.

Stock-specific color lines up with news risk. AVGO strength had a fundamental catalyst—reports that OpenAI tapped Broadcom to design and produce a new AI chip, a direct challenge to the incumbent setup and a fresh leg to the custom-silicon story. The flows you’re seeing into AVGO make sense against that backdrop. TSLA’s sweep activity fits the headline cadence and options heat we’ve seen around compensation/governance and production milestones—this ticker has been quietly compressing and broke above recent highs on decent volume - perma-faders beware.

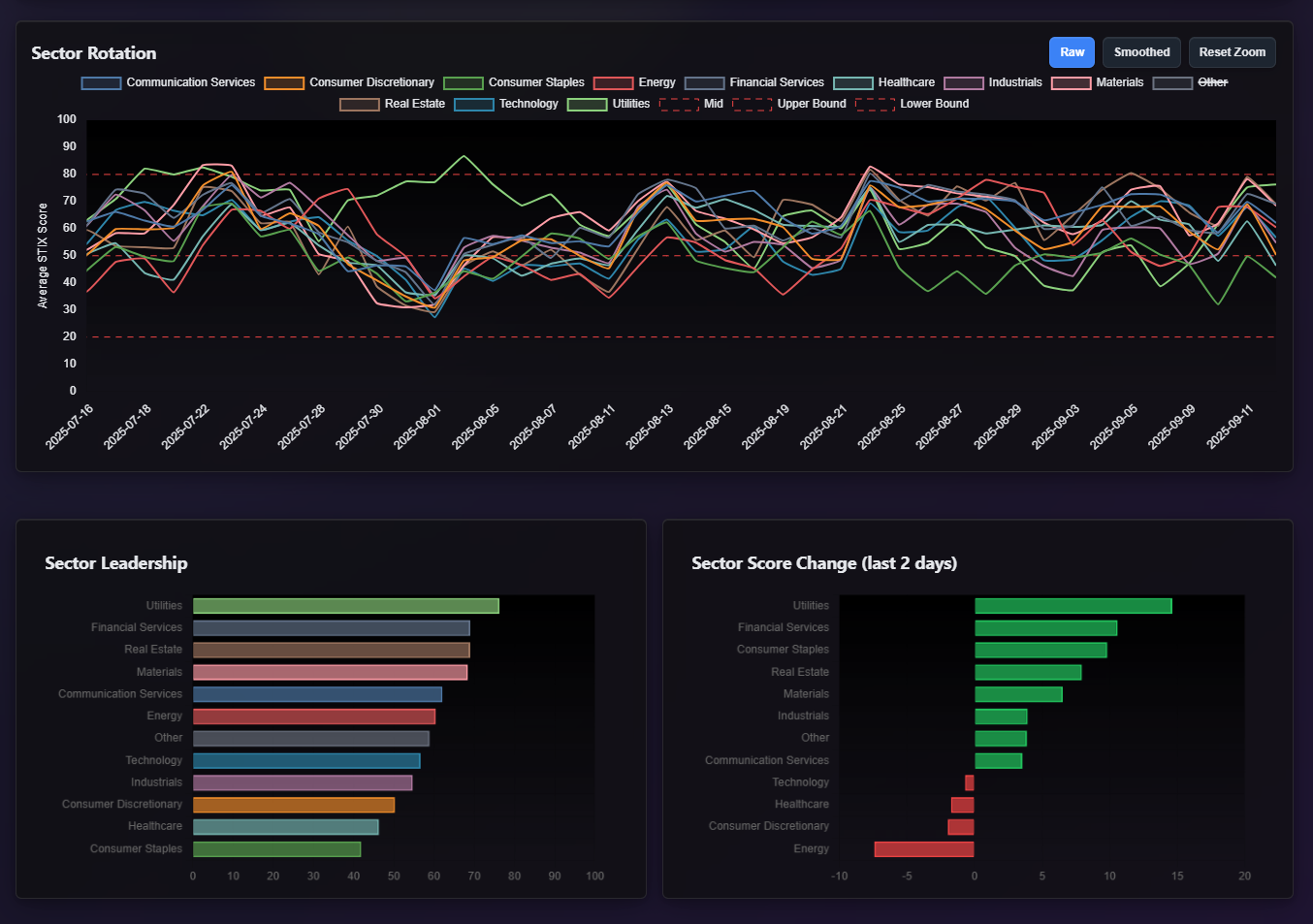

Sector rotation and leadership boards are the clincher. Utilities and Financials sit on top with Real Estate and Materials not far behind, while Technology is still strong but not the only game in town, and Energy is slipping on the two-day delta. That’s exactly what you get when (a) rates ease and the curve steepens (Utilities/REITs breathe; Banks’ NIM optics improve), and (b) crude gets hit on supply chatter—Saudi push for OPEC+ to bring forward additional output weighed on oil and the equities followed.

Macro overlay I’d keep in mind for the coming two to three weeks:

• Policy & growth: The labor print keeps the Fed on track to cut this month, with markets gaming additional easing into Q4. That’s supportive of credit flows seen in VL and of the “index first, then expand” equity posture we’ve been witnessing.

• Policy noise: Tariff policy is a wild card again after the appeals court said the President exceeded statutory authority on global tariffs under the emergency framework—tariffs remain in place during appeals and could land at the Supreme Court. If that ultimately bites, it’s a margin headwind that favors high-quality balance sheets (again, megacap/IG preferences demonstrated by the institutional tape making complete sense here).

• Seasonals: we’re smack in the heart of the worst month for stocks on long-term averages—the only month with a negative average S&P return since 1950, and the lowest “win rate” across the calendar. That matters most for your risk-management lens: fresh sponsorship can push against seasonals, but it rarely ignores them. Expect choppy uptrends and sharp mean-revert days rather than straight-line rallies.

Here are the broad strokes in a brief a working narrative with a little bias:

The big money came back and started with the “liquid core.” SPY/IVV/VOO on the index side and NVDA/AVGO/AAPL/MSFT/META/GOOGL on the single-name side carried both the lit and dark tape. That’s not a rotation away from Tech; it’s a reinforcement of the leadership spine while credit carry and front-end ballast get built alongside.

Credit is the tell. LQD/VCIT/HYG/USHY plus SHY showing up together says allocators are expressing a soft-landing-with-easing view. If the next inflation prints cooperate, that barbell (IG + some HY) probably gets more sponsorship, and Financials/REITs keep their relative bid. If inflation re-accelerates, the first place you’ll see stress is HYG/USHY and the long-duration growth complex—watch those ETFs in VL for early cracks.

Energy is the outlier. The two-day drop in the sector delta and the absence of heavy accumulation on the energy sleeves keep me cautious there while OPEC+ supply headlines ping-pong. Energy looked like a stronger trade two weeks ago when we looked at it then and I’m not ready to abandon the idea but until institutional positioning shows up, we’ve got to trim-up positions and wait.

Small caps are still a “prove it” trade. IWM is present on both the dark-pool and sweep lists, but it isn’t leading. Until Wednesday’s large-cap tech ranges are retested and hold—a lot of people are pinning high hopes on rate cuts carrying IWM into the end of the year, until you see breadth expand treat small caps as tactical, not foundational.

Watch the Wednesday footprints. The way Tech and Large Caps were bid that day—then validated by the next two sessions—makes those intraday ranges the obvious “line in the sand” in sessions soon to come. Above them, markets are turning their eye on seasonal expectation and dips are buyable into the end of month. Lose them convincingly, and I’d expect fast mean reversion back into recent ranges that had contained price for some time.

Bottom line: institutional dashboards are telling a coherent story. Funds are back, building positions the professional way—beta and credit first, megacap leaders second, ballast sprinkled in, and tactical single-name risk where catalysts allow (AVGO/NVDA/TSLA). Macro is cooperating just enough to keep that playbook in place: labor is cooling without breaking, the Fed is sliding toward cuts, and seasonals argue for respecting VL levels rather than getting greedy. If we keep seeing SPY/IVV/VOO and the IG sleeves (LQD/VCIT) printing big in both lit and dark, the path of least resistance into late September is a choppy stair-step higher led by the same megacap spine—until one of the macro pillars (inflation or policy) says otherwise.

MIR Part 2: Individual Names From The Institutional Tape

VolumeLeaders tracks several proprietary signals designed to spotlight names drawing significant institutional interest. Below, we’ve surfaced the latest results and analyzed them to highlight emergent themes. If any of the sectors, narratives, or positioning trends resonate, the names mentioned here offer a strong starting point for deeper research and watchlist consideration.

VL Institutional Outliers™ (IO)

Institutional Outliers is a proprietary metric designed to spotlight trades that significantly exceed a stock’s recent institutional activity—specifically in terms of dollar volume. By comparing current trade size against each security's recent normalized history, the metric flags outlier events that may indicate sudden institutional interest but may be missed because the activity doesn’t raise any flags/alerts when comparing the activity against the ticker’s entire history. For example, it’s conceivable that a ticker today receives the largest trade it has had in the last 6 months but the trade is unranked and would therefore be missed by current alerts built off Trade Ranks. Use “Realized Vol” to identify tickers with large price displacement and to size your risk appropriately.

First, the duration-and-quality bid is alive. IEF posts a 6.3σ dollar outlier and VCIT prints a 4.5σ—plus BSV, TFI, BRTR show up down the list. That’s classic “carry with a kicker”: take the coupon in intermediate IG, keep some Treasury convexity, and let the easing narrative do the heavy lifting. The fact that these are huge notional moves with microscopic realized vol says this is positioning, not a chase.

Second, AI/semis—and even the edge cases—were the flow magnets. AVGO scores a 4.7σ print, and you’ve got CAMT, CRUS, and a cluster of the “future compute” proxies—IONQ, RGTI, QBTS—lighting up. CHAT pops as well. That grouping is exactly the same “compute + model spend” lane we saw in the weekly dashboards. It reads like institutions re-upped the core AI book and sprinkled in optionality at the speculative fringe.

Third, the Tesla complex was a live wire. TSLA itself is an outlier, and both the levered wrappers lit up—TSLT on the long side, TSLZ getting leaned on the other way. When you see the underlying and both synthetics ping simultaneously, it’s typically gross-up plus hedging around a directional view. Given the week’s macro (lower yields, cut odds higher), bias tilts constructive.

Fourth, a media/entertainment sub-rotation: WBD is a 5.4σ buy amid the Paramount Skydance chatter and you’ve got SPHR, TKO, CABO all printing. That’s a pretty tight cohort, which usually means programmatic reweighting or an event path being priced (takeover, sports rights, bundles, ad recovery—pick your poison). It complements the broader Comm Services support we flagged earlier.

Fifth, crypto beta crept back onto the blotter. IBIT, BITF, BITQ, HIVE all show outlier dollars with decent up-days. That fits the “risk add, but with guardrails” pattern we’ve seen when front-end rate odds swing dovish—institutions won’t chase alt-coins, but they’ll buy the listed plumbing and the spot wrappers.

Sixth, Energy saw de-grossing. CVE and NBR register outliers on down days, while nuclear (NUKZ) sneaks in on the bid. That’s perfectly in step with crude’s wobble and the supply headlines. If the house view is softer growth and more supply, you trim upstream beta and keep the nuclear theme on a leash.

Seventh, rate-sensitives caught a bid where you’d expect. SLG and PECO show up for REITs; HD and RH print in specialty retail/home improvement, and TMHC appears in homebuilders. Lower long rates plus a steeper curve is exactly the cocktail those tickers like. Again, note the calm realized vol—this is quiet accumulation, not a squeeze.

Eighth, financials were selective. The broad ETF VFH shows an outlier but flat price, FAS gets flow, and single-names skew toward insurers (HCI, CINF) and LatAm broker/capital-markets exposure (XP). That lines up with “steeper curve helps lenders,” but the dollars say buyers favored quality and fee income over pure NIM beta. Makes sense while credit is still a question mark.

Ninth, international tilts were incremental, not thematic. You’ve got INDY, KSA, EWU, EWW and XSOE all on the sheet—small but purposeful. That reads like benchmark hygiene and a nudge toward EM ex-SOE quality rather than a wholesale country bet.

Tenth, single-name health care was catalyst-driven (RNA, ARGX, BNTX, IMVT, CRNX, RMD) with no unified tape direction—consistent with trial headlines and idiosyncratic positioning, not a sector call.

Round it out with a travel/industrial split—ULCC got sold while Rolls-Royce ADR (RYCEY) was bought—which says “be picky” inside Industrials; and a consumer two-hander—MELI and HD/RH got attention while M and CHWY were faded, which is the same quality-over-value tilt we’ve seen all quarter.

Net, the outliers reinforce the institutional blueprint we drew: scale into duration and intermediate-IG carry, re-risk into mega-cap AI and adjacent compute, keep TSLA on a tight leash with wrappers, dial down Energy beta, keep accumulating rate-sensitives in REITs and housing, and sprinkle crypto and media for upside convexity. The dollar sizes, low realized vol, and the way cohorts move together all say “positioning” rather than “panic”—summer’s over and the big books are back to work.

VL Trade Rank Velocity™ (TRV)

TRV is a proprietary metric that measures the recent acceleration or deceleration in institutional trading activity for a given stock by comparing its average trade rank over the past few days to its average in recent weeks. A sharp improvement in TRV typically reflects a notable shift in positioning, often accompanied by sustained trade activity, suggesting institutions are actively engaging with the name and that intensity of activity is rising. This often precludes meaningful price or narrative shifts. This isn’t a buy-list or sell-list; it’s meant to draw your eyes to names where institutions are putting money to work.

The acceleration isn’t in the AI headliners as much as in the plumbing—IT services and software infrastructure are where interest is surging and sticking. CTLP and TSSI light up alongside a cluster of infra names—TIXT, PGY, CRWV, KLAR, GRRR, GBTG—plus application security (CYBR). That’s exactly how big books re-risk after a choppy stretch: they buy the integrators, the outsourcers, the deployment layer. It pairs neatly with the outlier dollars we saw in mega-cap compute; the TRV says the follow-through is happening down the stack.

Semis are re-accelerating, but it’s selective and surgical. SITM (timing), PLAB and NVMI (process control/metrology), AEHR and AMBA show up—precision picks tied to utilization and yield, not just “AI everything.” Add the levered wrappers (AVGX/NVDU, SMCX) and you’ve got a coherent picture: institutions are topping up core AI exposure, but they’re leaning harder into the high-beta suppliers that benefit if capex holds.

On the macro overlay, the carry bid is still very much alive. YYY (CEF income) and VCEB/BRTR/VCRM on the bond side post meaningful TRV, which matches the outlier flows we flagged in IEF/VCIT. That’s the same playbook: intermediate duration, IG tilt, harvested systematically while cuts get priced.

Crypto shows measured risk-on. BITQ and SOLT pop, with BLSH in the mix and a tactical hedge in SMST (bear MSTR). That’s not euphoria; it’s basis-friendly, listed-wrapper exposure you can throttle quickly if front-end rates or liquidity wobble.

The TSLA complex looks hedged rather than chased. TSLS (1x bear) and TSLY (covered call) both ramp, which says overwriting and downside protection around a core long—consistent with the outlier dollar flows we saw in TSLA and its levered twins. Institutions want the optionality, not the whipsaw.

Cyclicals are attracting rate-sensitive capital. Building products (GMS, AWI), specialty industrials and machinery (RRX, PSIX, SERV, CR, CDRE), construction/engineering (EME), and even VTOL/Joby in air services all carry elevated TRV. That keys off the steepening we’ve had and the softer labor tape—exactly the cocktail that feeds housing/applied industrials without forcing a pure early-cycle bet.

Energy is a barbelled story. Uranium prints across URNJ and LEU; services/midstream get bids (FTI, VTOL, CMBT) while refiners (PARR, WKC) and a smattering of upstream show up. Layer in the two-way in miners (GDXU and GDXD) plus EQX, and it reads like inflation hedges and real-asset optionality are active—but managed tight, not a one-way commodity chase.

Financials are selective and diversified. You’ve got the crypto miners in the “capital markets” bucket (IREN, WULF), high-quality banks (FCNCA, SSB, HBNC, CUBI), brokers/advisors (HLI, SNEX), and specialty credit/insurtech (SEZL, OPRT, HIPO, ARX). That’s a factor mix—steeper-curve beneficiaries, fee-income defensives, and niche growth—rather than a blunt ETF buy.

There’s also a modest ex-US tilt—IEFA, ISRA—and a factor broadening tells on the equity side: XMMO (mid-cap momentum), DFSV (small value), SUSA/QLTY (quality/ESG). That dovetails with the EM narrative and the cooling of mega-cap dominance.

Healthcare looks event-driven: a basket of biotech and diagnostics (ZVRA, RNA, CNTA, APGE, PROK, MEDP) with sustained activity more than big “improvement” spikes—exactly what you get when calendars and data drop matter more than macro.

Netting it out: TRV says the acceleration is flowing to the same places the outlier dollars identified—carry in credit, core-plus AI (with an emphasis on the services/metrology supply chain), hedged mega-cap exposure (TSLA overwrites), and rate-sensitive cyclicals. Crypto and real-asset hedges are on, but in controllable wrappers. If you were looking for a shift to pure defensives, it’s not here; this is positioning for a softer-growth, easier-policy tape with a bias to breadth and cash-flow quality, not capitulation.

VL Consensus Prices™

These are the most frequently traded #1-Ranked Levels in VL this week. Trades occurring at the highest volume price in a ticker’s history are significant because they represent institutional engagement at a key price memory level—where the market once found consensus. These areas act as liquidity hubs, enabling large players to transact efficiently, and often signal a reassessment of fair value. This activity may precede major moves, mark equilibrium zones, or reflect broader portfolio shifts, making these price levels important to watch even without yet knowing how price will resolve. (Note: many Bond products trade in such a tight range that they dominate the top positions and are therefore omitted to provide better clarity around other flows. The bonds data is still available in the VL platform.)

The heaviest footprints remain around the AI backbone. You’ve got repeated interactions at the most-traded prices in AAPL and across the semi stack—QCOM, MRVL, MCHP, ON, UMC, ASX, HIMX—with SOXL popping up as the levered expression that institutions sometimes use when they want beta-in-a-bucket without telegraphing single-name intent. When this many semiconductor and compute-adjacent names keep revisiting their primary volume nodes, it’s usually not “capitulation”; it’s inventory being re-marked while big accounts decide whether the next move is another leg up or a handoff into rotation. Add IONQ on the edge of the compute theme and it reads like they’re still nursing the AI complex—just doing it at reference levels, not in chase mode.

Right behind that, software/infrastructure keeps showing up where sponsorship typically sticks: ESTC, GTLB, BASE, AFRM, TWLO, RBRK (and even your “XYZ” bucket that behaves like application software). That’s classic “picks and shovels” flow—own the rails and tools while the megacaps digest. The cadence is consistent with the TRV strength we’ve been seeing in tools and infra over the last couple weeks: higher touch counts at the node, then bursts of acceleration as news/flows line up.

Communication services is acting like a cash-flow quality sleeve. CMCSA and PINS are frequent flyers at their consensus prices, and ASTS/TLK give you that satellites/telecom flavor we’ve seen crop up in the outliers and TRV as well. The pattern there is two-way but constructive: price keeps getting pulled back to the most-traded area, buyers show up, and the tape rotates rather than breaks.

Defensives are not hiding. KDP, KMB, TSN, and WBA all sit on or near their historical volume magnets. That’s the kind of tape you get when big money wants carry and predictability while the macro shifts—happy to add (or at least defend) size at well-worn levels and let the easing narrative eventually do the work. If you connect that with what we’ve seen in utilities and REITs (HE, BKH, SWX on the utes side; GLPI, NNN, EPR, CUBE, NHI, DX for REITs), it looks like a steady build of rate-sensitives into a lower-yields backdrop. Mortgage-adjacent tickers like UWMC and RKT living at their consensus zones fit the same thought process.

Energy’s showing a two-track bid. The integrateds and refiners (BP, CVE, CVI, PSX, DK, CLMT, MGY) keep meeting price where the most business has historically been done, while services (OII) and the nuclear/uranium proxies (SMR, DNN) pop up around their own nodes. That’s not “sell energy”; it’s a rotation within energy—reloading after pullbacks and shifting emphasis as crude, crack spreads, and policy headlines move around.

Financials are quietly busy at their magnets: SOFI, NU, XP, IBKR, OWL, and a handful of regionals (AUB, WAL, PPBI, BRKL). When regionals and capital-markets brokers cluster at consensus levels while the curve steepens, it’s usually balance-sheet calibration rather than an outright stance—think “add what benefits from a friendlier curve, trim what’s run too fast.” IBKR’s presence at its node alongside the S&P 500 inclusion chatter we flagged earlier is a nice confirmation that institutions are using volume areas to re-size rather than chase headlines.

Discretionary is barbelled. Travel/gaming (LVS), specialty retail (BBWI, FND), and autos (LI, HMC, LKQ) keep coming back to home base. That’s what you see when macro uncertainty is high but rates are slipping—sponsors are willing to press the parts of the consumer that remain resilient, but they want the liquidity of trading at known price shelves. If the labor data stays soft-but-not-broken and mortgages continue to ease, this cohort can catch a tailwind.

Sprinkle in the international and alt-beta tells: TLK (Indonesia), LI (China EV), ASX/UMC (Taiwan semis), XP/NU (Brazil fintech), and even crypto proxies like BITX. It lines up with the slight ex-US and digital-asset tilt we’ve been picking up elsewhere: position size stays disciplined, trades get done at the magnets, and they let the macro dictate follow-through.

Net-net, with bonds removed from the view, the equity consensus sheet still looks like classic institutional positioning into an easing-leaning regime: keep working the AI/compute value area (via semis and infra) while rotating into defensives and rate-sensitives, maintain a measured energy bid with an eye on alternatives for nice opportunities, and probe selectively in ex-US and crypto proxies. The common denominator isn’t “risk on” or “risk off”—it’s sponsorship negotiating at the most-traded prices. That’s where the next directional handoff tends to start, and right now those battlegrounds are getting a lot of traffic.

MIR Part 3: Framing-Up A Trade

Here’s how I’d frame it and actually put risk to work, pulling together what the institutional tape just told us.

First, the backdrop. Big money came back in size around the MSCI rebalance and then dialed down the throttle—liquidity is coming back and it reads like institutions rotating and re-benching inventory at their preferred price shelves while the macro tilts toward easing. The consensus-level map makes that obvious: semis and software rails keep meeting price at their most-traded nodes, defensives and rate-sensitives are being quietly built, and energy is being managed by sleeve rather than as a monolith. IO and TRV confirm who’s getting the incremental sponsorship right now and who’s just getting traded.

So, what do you actually buy? I’d start with the AI backbone, but with a technician’s discipline. Outliers flagged real money in AVGO, and TRV is lighting up the semi-cap/peripheral stack—SITM, PLAB, AMBA, NVMI—with repeated touches at their historical volume magnets across QCOM, MRVL, MCHP, ON, UMC, ASX, HIMX. That combination—heavy prints, accelerating rank velocity, and business getting done at the node—says “sponsored digestion,” not blow-off. My approach is simple: scale into that basket at the consensus shelves the tape keeps revisiting, risk a close below the shelf, and let the next leg higher pay for the carry. If you want the index wrapper, SMH works, but I prefer owning a couple idiosyncratic rails alongside a core like AVGO so I’m not just paying for the whole factor. I’d also acknowledge the split signal in TSLA: huge outlier flow in the common, but TRV interest in the bear and covered-call products tells you institutions are owning it hedged, not naked. That argues for diagonal calls or buy-writes rather than clean longs if you need exposure there at all.

Right behind semis, I’d lean into the software “picks and shovels” that keep showing up on TRV and at consensus prices—ESTC, GTLB, CYBR, PGY, TIXT, and the “XYZ/CRWV” style application rails. These names have the same fingerprint as the chips: business keeps returning to the most-traded price areas, and velocity is improving on good days without getting air-pocketed on bad ones. My playbook is to buy the first pullbacks into supportive volume nodes and use a tight line just below the shelf. If we’re right about policy easing into year-end, this is exactly the cohort that tends to lead once the megacaps stop doing all the heavy lifting.

I also want a sleeve that gets paid if the curve keeps steepening and yields continue to ease: REITs, utes, and a smattering of banks. You can see the quiet accumulation at consensus in GLPI, NNN, EPR, CUBE, NHI and mortgage-adjacent DX, with SLG showing up on the outlier tape. On the utilities side, HE, BKH, SWX have been defended at their magnets. For financials, I like nibbling the better-capitalized regionals that saw size (PPBI, BRKL) and the capital-markets names that are still being worked at their volume shelves (IBKR, XP, NU, OWL). None of this is going to make you a “hero”; it’s carry with a tailwind if rate cuts land without a hard-landing headline. I’ll pair that with some intermediate credit exposure expressed through equities that correlate to lower rates and better financing—again, the REIT/mREIT mix—rather than reaching for bond wrappers here, since the equity sleeve is where we’re getting the sponsorship tells.

Energy is a stock-picker’s game at the moment. The integrateds and refiners—BP, CVE, PSX, DK, CLMT, MGY—are being managed around their nodes, which says institutions want the exposure but aren’t paying up. Services and the “new energy” sleeves are where the relative appetite sits. TRV heat in FTI and continued attention in nuclear/uranium proxies (URNJ, UUUU, LEU) give you a clean way to stay involved without betting on one crude headline which has me on the edge of my seat by the time the weekend rolls in every week. My bias is to add uranium on dips into institutional level and keep the refiner/integrated sleeve smaller until crack spreads and OPEC rhetoric stop whipsawing the tape.

I still want ballast, and the staples are doing exactly what they should do in this phase. KDP, KMB, TSN, and even KO via sweeps are being sized at their consensus prices. That’s not “hiding”; that’s institutions paying for time. I’ll hold a small defensive bucket and finance a piece of it with covered calls because the tape keeps handing us reversion around those big nodes. It won’t win the week, but it will keep me in the game if we get the seasonal September chop.

Two more sleeves round out the book. First, an industrials/building tilt that benefits if lower yields trickle through to housing and project starts: GMS and AWI showed up on TRV, and EME just got the index upgrade tailwind. Add a bit of specialty machinery (RRX, CR, SERV) where velocity is improving and trade them against their shelves. Second, a tactical crypto-beta toe-hold. I’m not treating IBIT, BITQ, IREN, WULF and SOLT as “investments,” but the outlier and TRV attention is real. That gets a small, clearly defined trading sleeve with nearby stop-outs and no averaging down.

Internationally, I’m keeping it subtle: IEFA has a TRV bid, XP/NU continue to sit on their magnets with sponsorship, and there’s been a trickle into Israel/EM ex-China proxies. That’s a light tilt, not a core bet—more a way to capture the breadth we’re seeing creep back into global tapes without chasing anything that doesn’t have a healthy volume shelf beneath it.

Entries and risk are anchored in the same place across the board: do business at the consensus levels where the biggest prints keep happening. When the tape hands me those prices, I take a first slice; when price confirms by accelerating in my direction in the following sessions, I look for places to add some more; really trying to keep everything level to level in this current tape because vol is incredibly compressed. If we break and close below levels on expanding volume, I’m out all the way and will happily try again at the next lower node. I’m not pretending every dollar-flow is a buy; it’s positioning, and the price tells you when you’re wrong.

Hedges are boring by design. With AVGO/semis in the core, I’ll keep a small SMH put spread two to three weeks out and roll it rather than trying to thread needles around single-name prints. If the macro risk is the labor tape softening faster than the Fed can spoon-feed, a touch of duration long is fine tactically—but I’ll usually express the macro hedge with index puts rather than chasing bond ETFs in the equity book. For TSLA specifically, I’ll either be flat or run a buy-write—TRV’s interest in the bear and covered-call products tells you how the big money is playing it. And if I need dry powder, those cash-like vehicles that showed up on sweeps (think ultra-short, short IG) are perfectly acceptable parking spots between adds.

I want to stay a little honest to the calendar: we’re in the messy part of the year; if breadth holds up and the curve keeps steepening with yields biased lower, the barbell I just laid out should work. If either of those snaps, I’ll trade what’s left in front of me after the major VL levels do the talking.

Net-net, the best places to deploy capital right now remain the sponsored value areas: a core in AI infrastructure led by AVGO and the semi-cap/peripheral stack bought at their magnets, a rails sleeve in software/security that keeps showing velocity, a measured dose of rate-sensitives in REITs/utes and select banks, selective energy with an overweight to services and uranium, staples for ballast, an industrials/building kicker, and a small crypto-beta trading sleeve. Size it so you can sit through September’s noise, I get the sense that the back-half of this month is not going to be easy.

Thank you for being part of our community and for dedicating your time to this edition. Your insights and engagement drive everything we do, and we’re honored to share this space with such committed, thoughtful readers. Here’s to a week filled with clear opportunities and strong performance. Wishing you many bags 💰💰💰

—VolumeLeaders