Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 58 / What to expect Aug 25, 2025 thru Aug 29, 2025

NOTE: This weekly periodical is too large for Substack to deliver in its entirety via email - you will only see a portion of this great content if you read from your email client. Click the header/title at the top to read the full article!

In This Issue

Weekly Market-On-Close Report: All the macro moves, market drivers, and must-know narratives—covered in less than five minutes.

Weekly Benchmark Breakdown: Our weekly intelligence report on major indices cuts through the index-level noise to uncover participation, momentum, and structural integrity and tell you whether markets are rising on solid ground or skating on thin breadth. This is where bull markets prove themselves—or quietly start to unravel.

The Latest Investor Sentiment Readings: Track the emotional pulse of the market with our curated dashboard of sentiment indicators. From fear-fueled flight to euphoric overreach, this week's readings reveal whether investors are cautiously creeping in—or stampeding toward the exits.

Institutional Support & Resistance Levels For Major Indices: Exactly where to look for support and resistance this coming week in SPY, QQQ, IWM & DIA

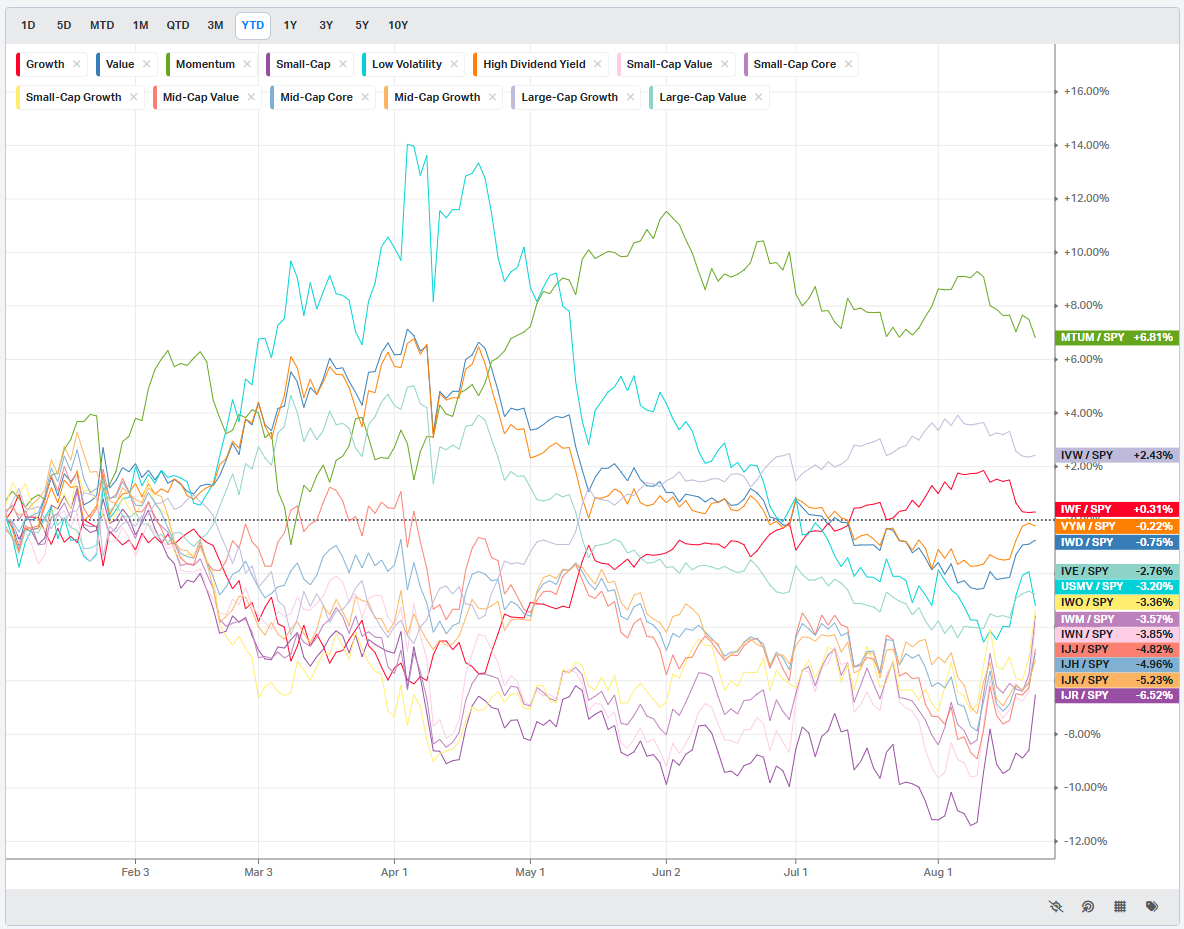

Normalized Performance By Thematics YTD: Which corners of the markets are beating benchmarks, which are overlooked and which ones are over-crowded!

Key Econ Events & Earnings On-Deck For This Coming Week

Market Intelligence Report: Track the real money. This section breaks down where institutions are placing their bets—and pulling their chips. You'll get a sector-by-sector view of flows, highlighting the most active names attracting large-scale buying or selling. We go beyond the headlines and into the tape, surfacing the week’s most notable block trades and sweep orders, both on lit exchanges and hidden dark pools. Whether you're following momentum or fading crowded trades, this is your map to where size is moving and why it matters.

Weekly Market-On-Close Report

The Week Powell Blinked

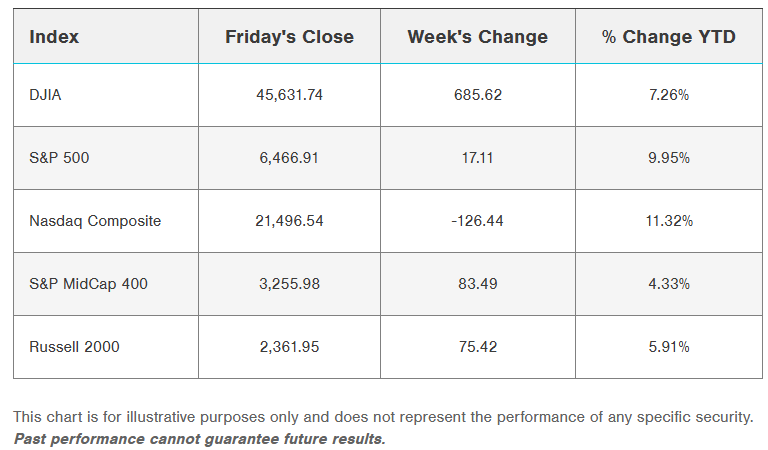

It was the kind of Friday close that forces investors to sit up straight. The Dow Jones Industrial Average surged nearly 1.9%, punching out a fresh all-time high. The S&P 500 tacked on 1.5% and clawed back into positive territory for the week. Even the Nasdaq 100, under pressure much of the summer from profit-taking in mega-cap tech, snapped higher by a similar margin. The trigger was clear: Fed Chair Jerome Powell used his Jackson Hole pulpit to hint that the next policy move could be down, not up. Bonds ripped, the dollar sagged, equities cheered. For the first time in months, the market had the sense that the central bank was blinking.

Powell Cracks the Door

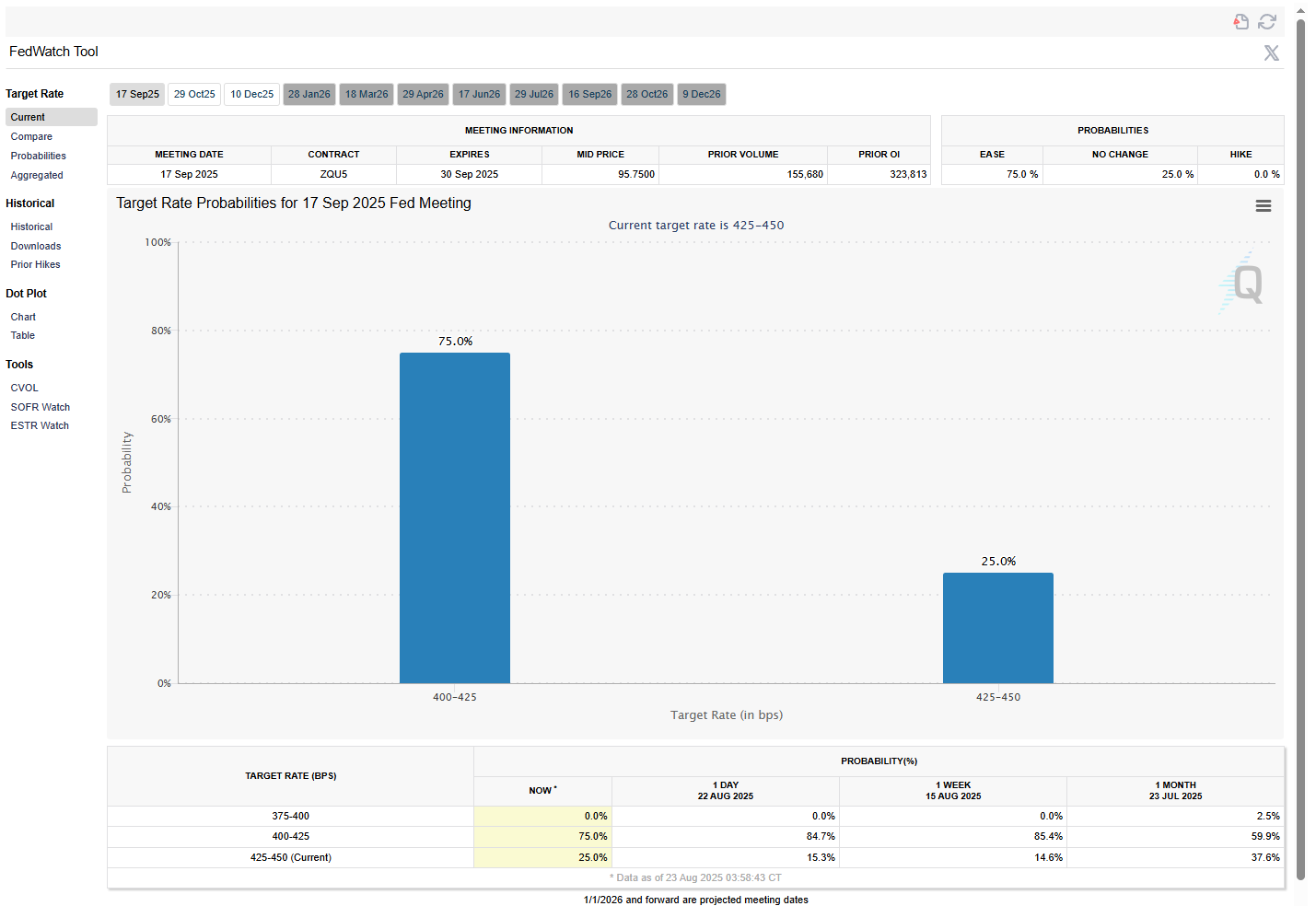

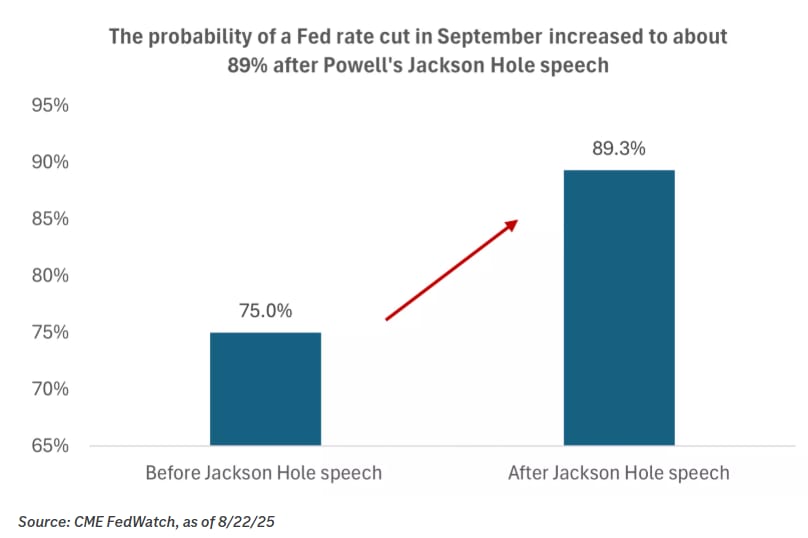

Powell did not bury the lede. He opened by noting that the “balance of risks appears to be shifting,” citing a labor market that is softening faster than expected. Payroll revisions and rising continuing claims have unnerved policymakers. Inflation, meanwhile, remains sticky but no longer one-dimensional. Tariffs are lifting headline measures, but Powell described the impact as “likely short-lived.” With the policy rate already deep in restrictive territory, the door for a cut in September swung wide enough for markets to run through.

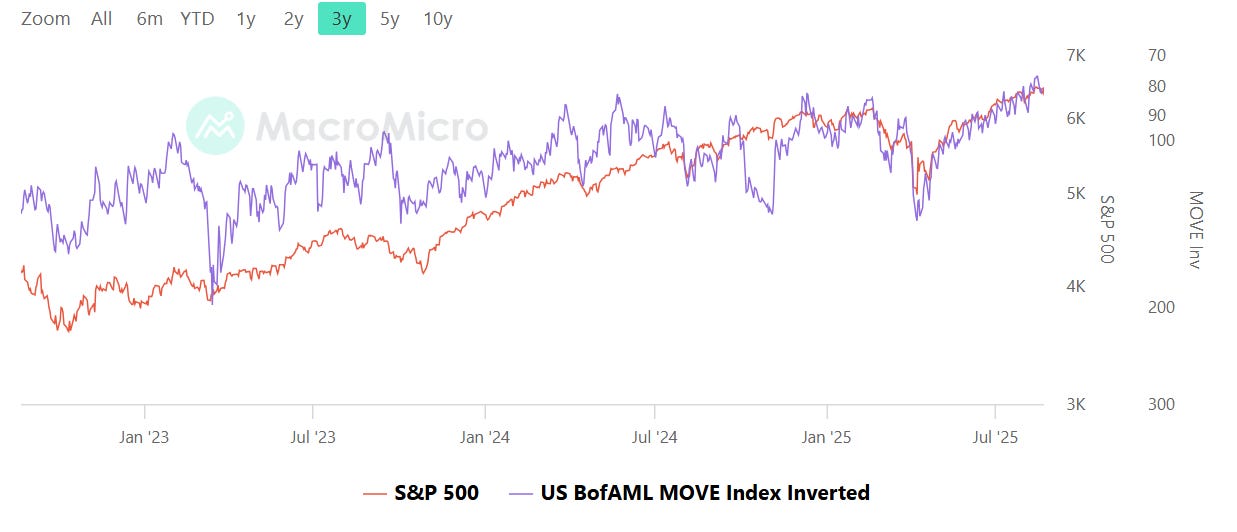

Fed funds futures immediately repriced. The odds of a 25bp cut at the September meeting shot back above 80%, with another cut in December now seen as better than a coin flip. Treasury yields tumbled—2s by nearly 10bp, 10s by 7bp—erasing weeks of creep higher. The MOVE index of Treasury volatility fell to its lowest since late 2021. In market terms, Powell put a floor under risk assets.

Hawkish Echoes

Not all were convinced. Boston Fed President Susan Collins was quick to push back, reminding that the economy still has “solid fundamentals” and that inflation risks have not been vanquished. She called policy “modestly restrictive” and “appropriate.” Markets brushed her aside—after Powell spoke, her comments were little more than background noise. But it was a reminder that the Fed is not unified, and that the September meeting will still hinge on upcoming data: PCE, CPI, jobs.

Tariffs and Geopolitics: The Other Backdrop

While Powell stole the spotlight, tariffs and geopolitics hummed in the background. President Trump’s administration widened tariffs on steel and aluminum products to more than 400 consumer goods, ranging from motorcycles to tableware. Semiconductor levies of up to 300% were floated, with exemptions dangled for firms willing to onshore production. Tariff truce extensions with China offered temporary calm, but India was slapped with doubled duties over Russian oil imports. Pharmaceutical imports could be next. Bloomberg Economics estimates average U.S. tariffs will rise to 15.2% once the announced measures are live, up from just 2.3% last year.

Meanwhile, the White House hosted Ukraine’s President Zelensky alongside European leaders, following Trump’s recent meeting with Putin. The choreography aimed at creating a framework for eventual peace talks. Markets barely flinched—the S&P traded in its narrowest intraday range of the year on Monday—but the geopolitical weight is obvious.

Rotation in the Tape

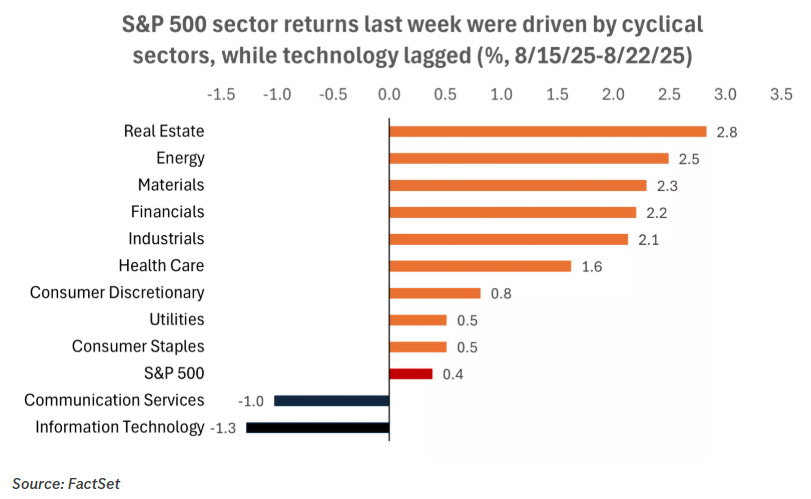

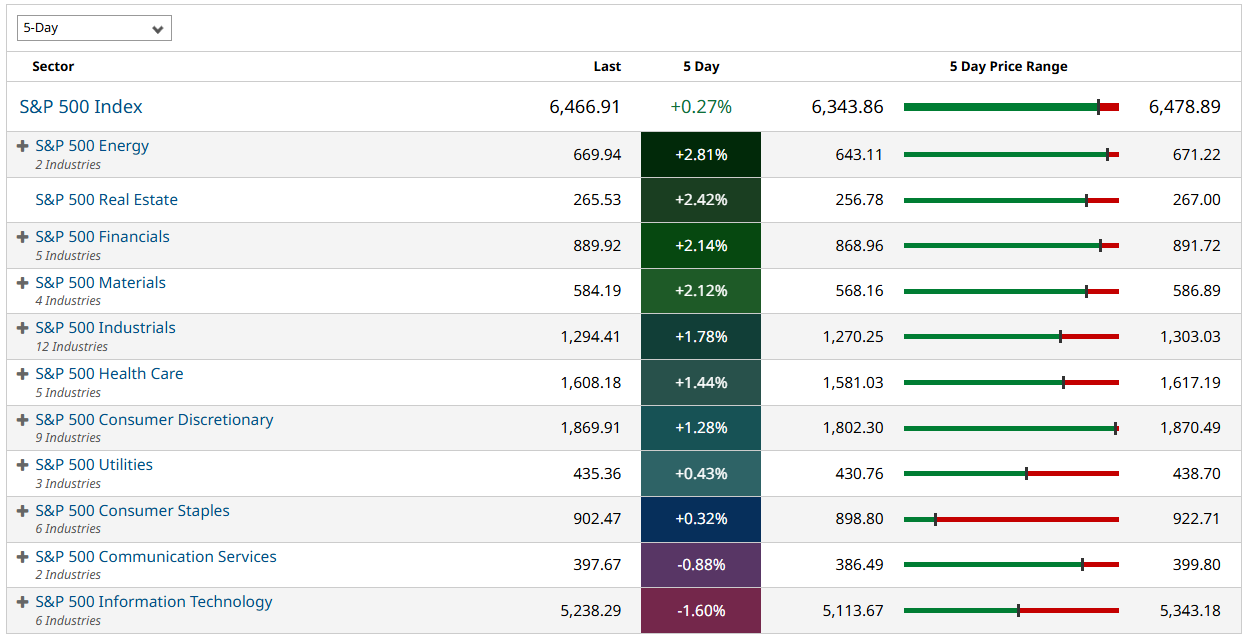

Last week saw a sharp rotation out of mega-cap tech and into value and cyclicals. That theme returned midweek before Powell reset the deck. Growth and AI names stumbled, while freight, homebuilders, and retailers caught a bid.

By Friday, Powell’s dovish tilt pulled everything higher, but the week’s story was still one of broadening participation. Equal-weight indices outperformed cap-weighted. The Russell 2000 surged nearly 4% on Friday alone, outperforming the S&P 500 by nearly 200bp on the week.

Healthcare, long a laggard this year, led all sectors. Materials and Financials followed, with banks and insurers rallying in tandem. Energy benefited from crude’s breakout above its 50-day moving average. On the downside, Information Technology lagged—semis like Nvidia, AMD, and Micron all slipped despite a late-Friday rescue. Communication Services also dragged, with Meta and Netflix losing ground.

Earnings: Retail Resilience, Tech Mixed

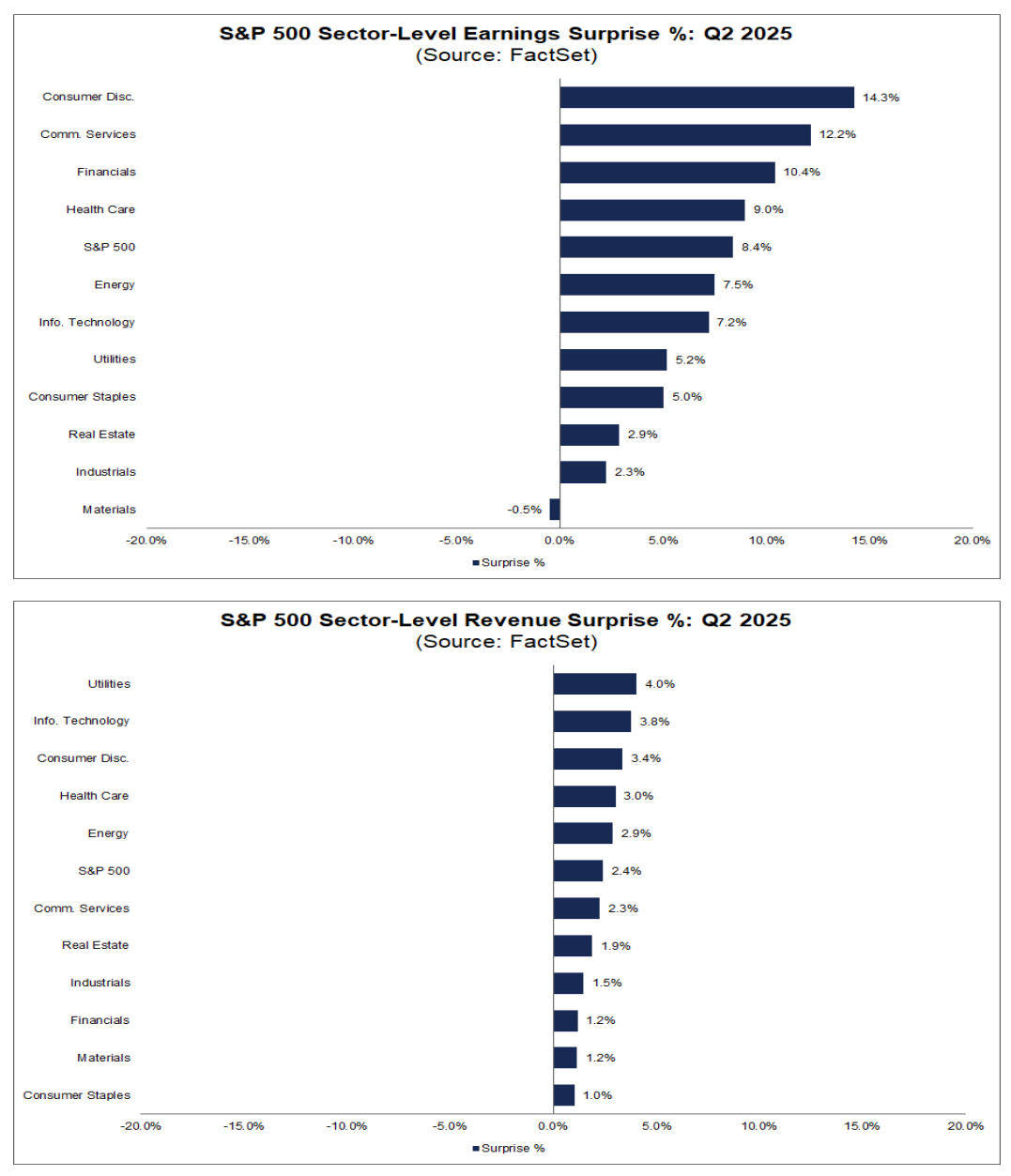

Earnings season is nearly complete, and the scorecard is better than anyone expected. S&P 500 profits are on track to grow over 9% year-over-year, the strongest showing in four years. Roughly 82% of companies beat estimates. Retailers in particular painted a picture of a consumer still spending—Walmart and Target exceeded forecasts, while Home Depot and Lowe’s showed homeowners are still putting cash into projects. Amazon, which reported last month, confirmed double-digit growth in its North American retail arm.

Tariffs, however, are creeping into corporate commentary. Walmart admitted that restocking inventory is coming at higher cost, a dynamic that will persist into the fall. Other retailers voiced similar concerns. The takeaway is that while retailers are absorbing some of the hit, consumers should expect higher prices on select goods over the next quarters.

On the tech side, results were mixed. Intel and ON Semiconductor rallied on earnings strength, with chipmakers broadly higher Friday. Zoom and Ubiquiti delivered blowout surprises. But Intuit fell more than 5% after offering a soft forecast, and Workday disappointed with an unexpected loss. Tesla surged 6% Friday, leading the “Magnificent Seven” rebound.

Macro Data: PMI Surprise, Jobless Claims Rise

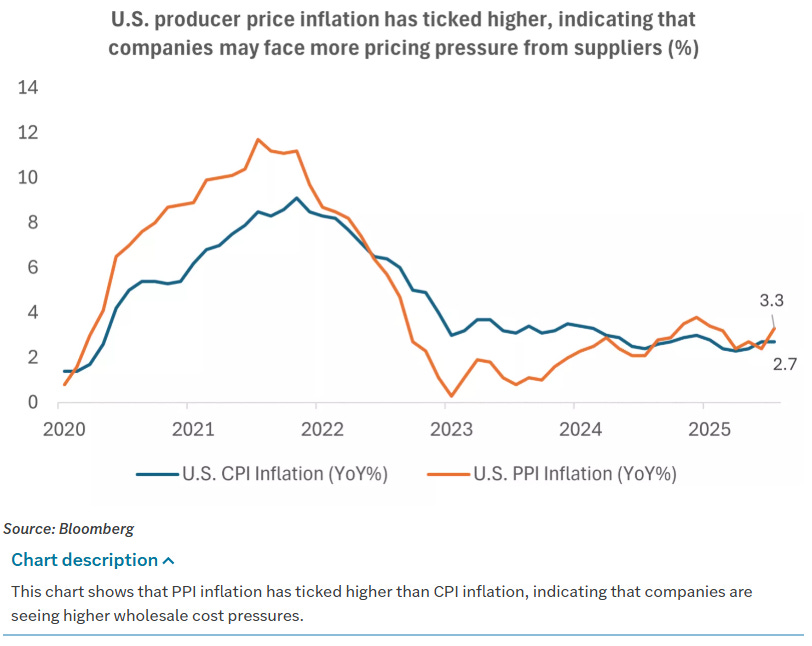

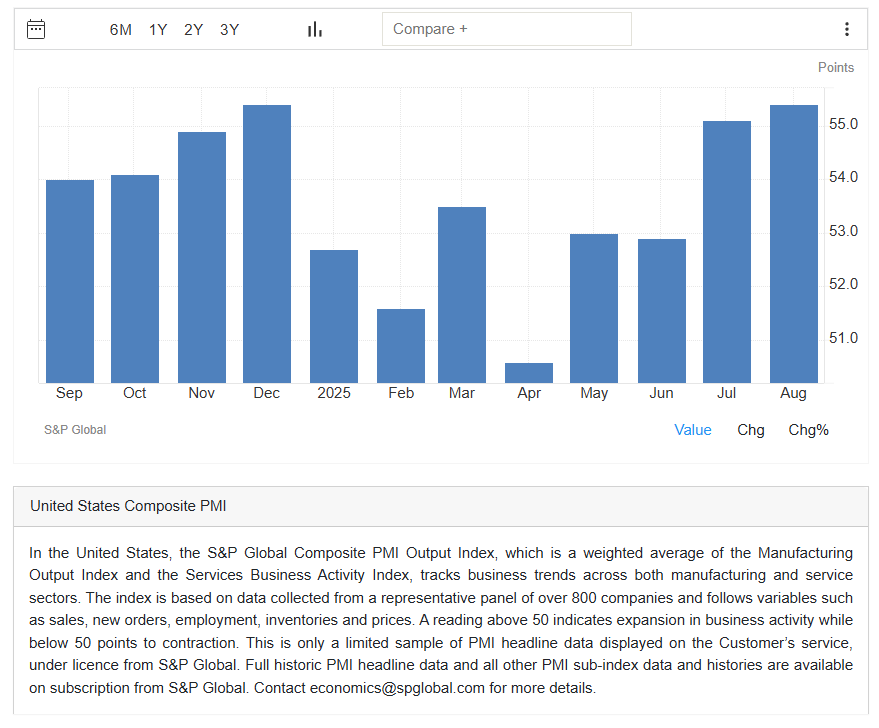

Macro data didn’t sit still either. Flash PMIs showed the U.S. composite at 55.4, the fastest pace this year. Manufacturing broke back into expansion at 53.3, a 39-month high, as firms scrambled to build inventories against tariff fears. Services ticked slightly lower but held strong. The bad news: input costs surged, with prices charged rising at the sharpest pace since 2022.

Jobless claims told a different story. Initial claims climbed to 235k, above consensus, and continuing claims hit their highest level in four years at 1.97 million. That divergence—firms reporting strong demand and hiring in surveys, while unemployment claims edge higher—was the context for Powell’s remarks. The Fed is weighing hot PMIs against cooling labor, restrictive rates against tariff-driven inflation.

Global Markets: Europe Strong, Asia Mixed

Global equity markets were generally higher. Europe’s Stoxx 50 rallied to a five-month high, with the UK’s FTSE 100 hitting a new all-time high. Germany lagged, with GDP revised lower even as manufacturing PMI improved. In Asia, Shanghai extended its overbought run, while Japan’s Nikkei slipped after a furious AI-led rally earlier in the summer. SoftBank announced a $2 billion Intel partnership and new AI manufacturing plans with Foxconn in Ohio.

Commodities and Crypto

Brent crude climbed 3%, breaking out of its recent range and finishing near $68. Natural gas slumped on warmer weather and robust production. Gold bounced off its 50-day moving average, closing the week higher alongside silver. Wheat fell, but most ags gained. Crypto staged a sharp rally on Friday, with Bitcoin back above 117k and Ethereum higher as well. The dovish Powell bid extended well beyond stocks.

Treasuries and FX

Treasuries were the cleanest read. The 2–5 year sector fell nearly 10bp Friday, the 10-year dropped 7bp, the 30-year shed 3bp. Yields are now back to where they were after the July “jobs revision-gate.” The MOVE index collapse underscored how much volatility has been wrung out. The dollar index fell 1% Friday, pushing negative on the week. The euro climbed above $1.17, with a key test at $1.18 overhead. The yen firmed below ¥147, a level it hasn’t sustainably broken since early July.

How I’m Synthesizing It (Without Overreaching)

The equity market wanted an excuse to breathe, and Powell gave it one. Breadth is improving, earnings have come in better than feared, and sectors beyond tech are finally showing signs of leadership. Yet the labor data remains fragile, tariffs are still rolling through the pipeline, and inflation isn’t entirely tamed. My synthesis: the Fed has created a window where equities can grind higher, but that window is only as durable as the next round of data.

What Would Change My Mind (Signals to Watch Next)

If incoming inflation data—PCE, CPI, PPI—shows tariffs sparking a persistent second wave of price pressure, or if jobless claims accelerate sharply higher, the balance tilts back. A labor market that suddenly cracks would flip the story too. Watch retail commentary: if Walmart and peers begin passing on costs in a broad way, that’s a red flag. And of course, keep an eye on Nvidia earnings; it’s not just about one stock, but the entire AI-driven growth trade that has carried markets this far.

Bottom Line (and a Positioning Sketch, Not Advice)

Powell blinked, and markets seized it. Bonds rallied, equities broadened, the dollar retreated. For positioning, it argues against hiding solely in mega-cap growth and toward balancing with cyclicals and value, while staying hedged for volatility. September is seasonally tough, but dips may offer entry points rather than exits. The Fed has shifted from being the market’s obstacle to potentially being its reluctant partner—and that subtle change could define the months ahead.

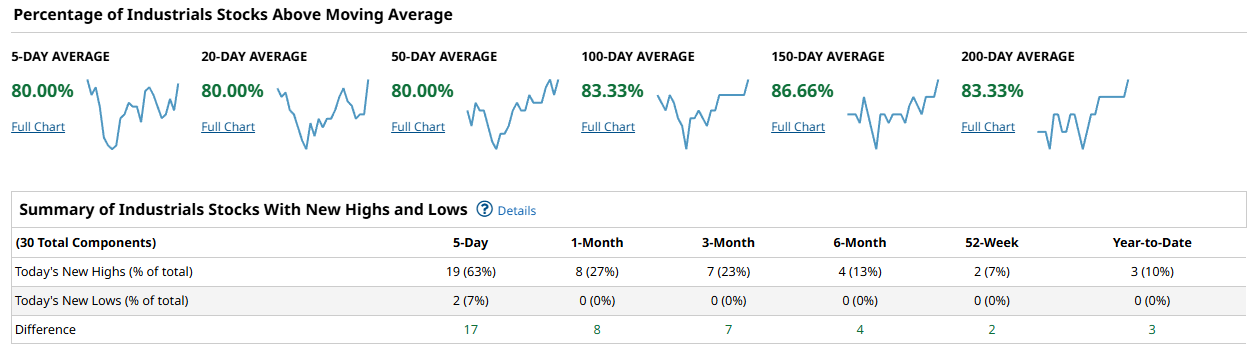

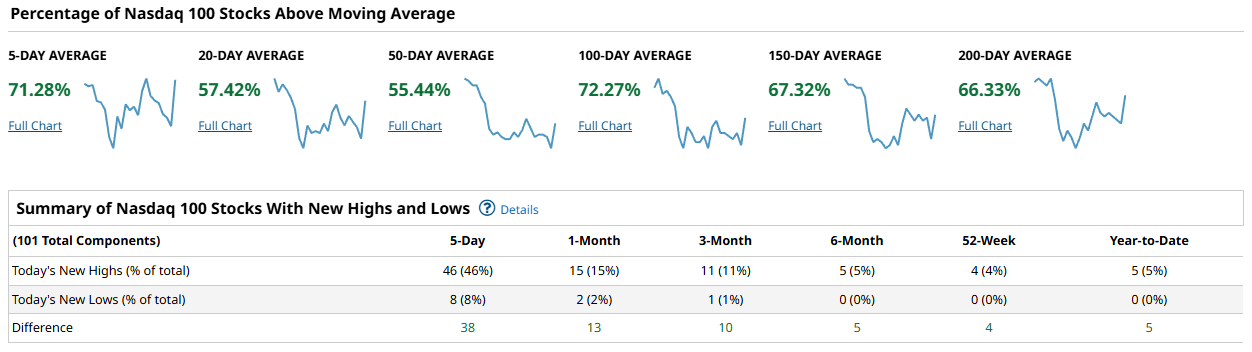

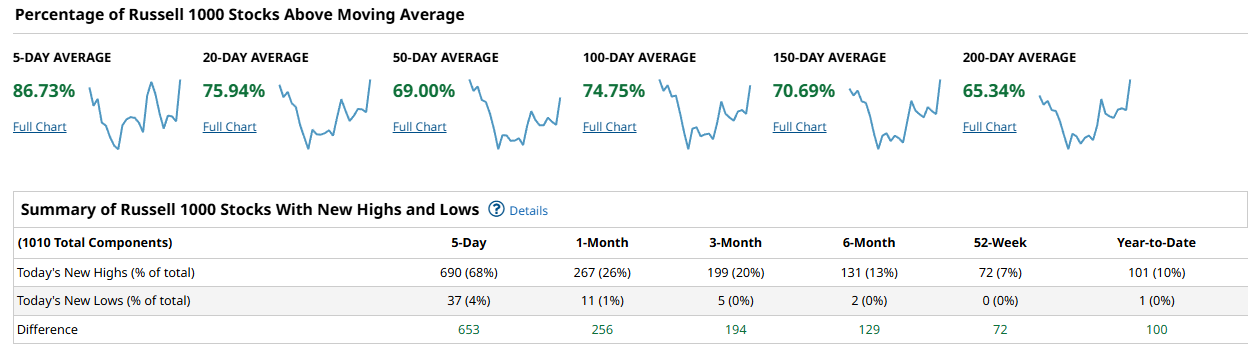

Weekly Benchmark Breakdown

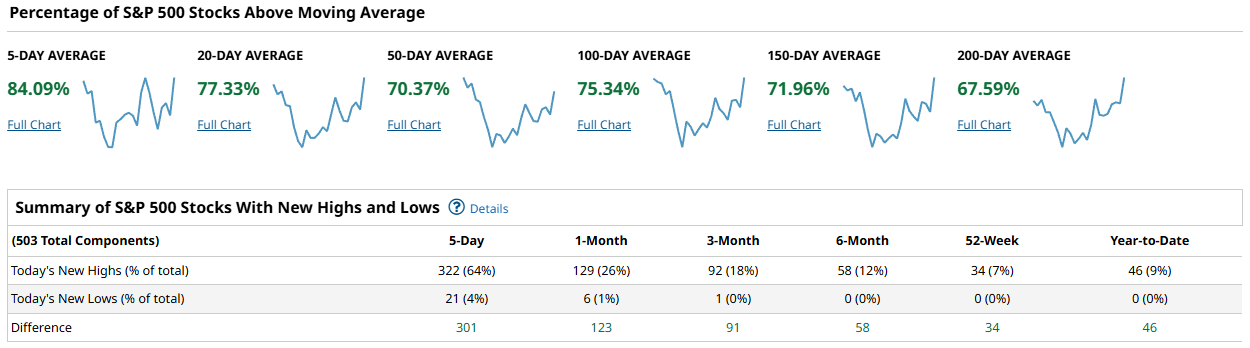

Breadth across the major benchmarks is telling a story of strength, but with some clear divergences under the hood. The S&P 500 is sitting on solid footing with more than two-thirds of its members above their 200-day moving average and an impressive 83% above their 5-day—a strong short-term surge layered on top of longer-term stability.

Industrials are even healthier, with 80%+ of the group trading above key averages and fresh highs outpacing lows by wide margins, showing that cyclical leadership is still intact.

The Nasdaq 100, though, is flashing relative fragility: only about 55% of its components hold above their 50-day and 57% above the 20-day, a sign that mega-cap tech is masking some weakness beneath the surface.

By contrast, the Russell 1000 is roaring, with nearly 87% of its members above their 5-day and more than 65% holding above the 200-day, reflecting broad participation that extends well beyond the mega-caps.

In short: the broader market is firm and cyclical sectors are carrying weight, but the tech-heavy Nasdaq looks more vulnerable, making breadth the key tell to watch in the week ahead.

US Investor Sentiment Report

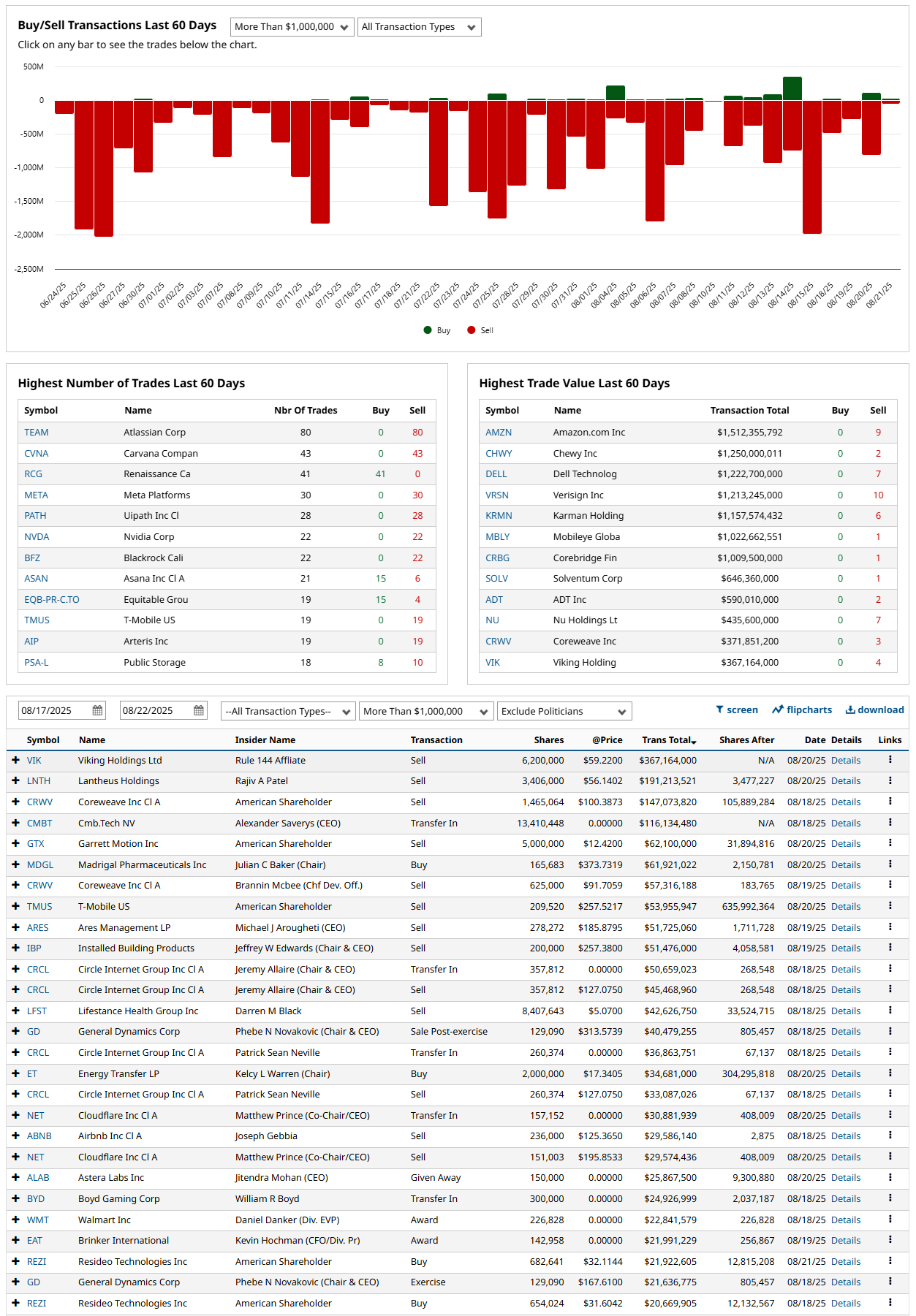

Insider Trading

Insider trading occurs when a company’s leaders or major shareholders trade stock based on non-public information. Tracking these trades can reveal insider expectations about the company’s future. For example, large purchases before an earnings report or drug trial results might indicate confidence in upcoming good news.

The insider tape over the past couple of months has been telling a very clear story. Almost every day has leaned heavily toward selling, with insiders unloading billions across big tech and consumer names, and only the occasional day showing net buying that was barely a blip compared to the red waves. The biggest headlines came from Amazon, Chewy, Dell, and Mobileye, where insiders collectively sold billions, suggesting that even the most dominant growth stories aren’t immune to profit-taking. Atlassian, Carvana, Meta, and Nvidia were also one-way streets—executives have been trimming positions without hesitation. That said, it wasn’t completely one-sided. Renaissance Capital was an outlier with steady insider accumulation, and we also saw notable buying in Coreweave and Viking Holdings, which stand out precisely because they buck the broader selling trend. On balance, insider sentiment still feels decidedly bearish, but those few pockets of buying may end up being the names to watch if the tide starts to shift.

%Bull-Bear Spread

The %Bull-Bear Spread measures the gap between bullish and bearish investor sentiment, often from surveys like AAII. It’s a contrarian indicator—extreme optimism may signal a coming pullback, while extreme pessimism can hint at a potential rally. Large positive or negative spreads often mark market turning points.

The AAII Bull-Bear spread has slid sharply back into negative territory, closing this past week at –13.96%. That marks a decisive swing from late July’s optimism, when sentiment briefly crept back into positive territory with a +7.3% print, and it caps off a three-week stretch of accelerating pessimism. The move is even more striking in context: back in March and April, the spread was deeply depressed at levels near –40%, but the rebound into summer had many thinking the worst was behind us. Instead, we’re now watching bulls retreat and bears regain the upper hand, with the spread retracing almost all of its mid-year recovery. Put simply, retail sentiment is leaning defensive again, which can often create the conditions for a contrarian bounce—but only if broader macro data and earnings stop giving investors fresh reasons to stay cautious.

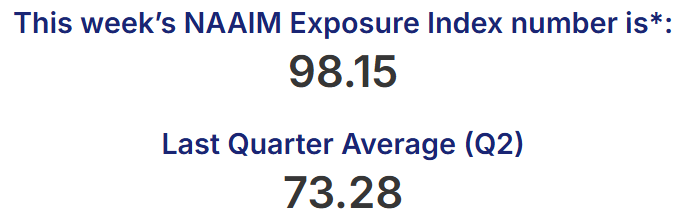

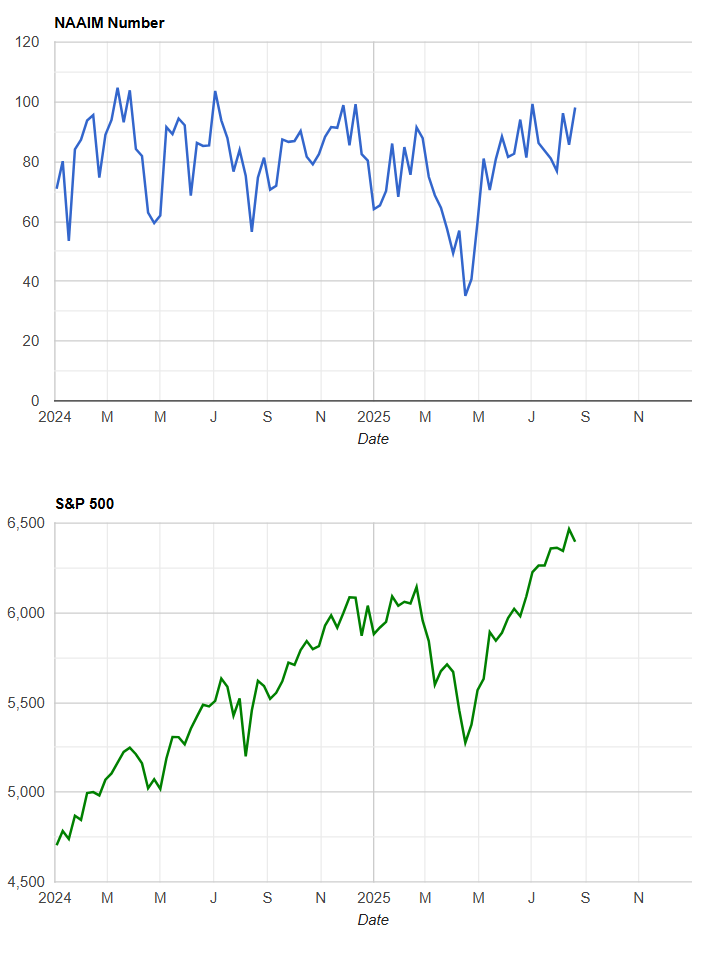

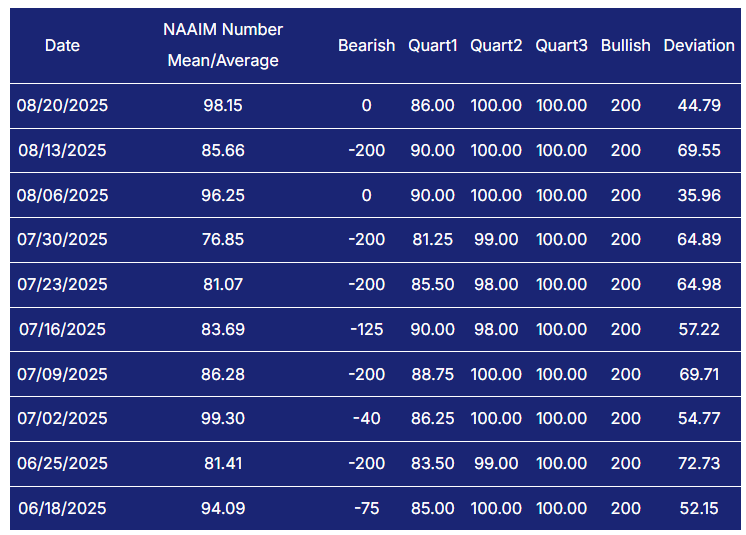

NAAIM Exposure Index

The NAAIM Exposure Index (National Association of Active Investment Managers Exposure Index) measures the average exposure to U.S. equity markets as reported by its member firms. These are typically active money managers who provide their equity exposure levels weekly. The index offers insight into how much these managers are investing in equities at any given time, ranging from being fully short (-100%) to leveraged long (up to +200%).

This week’s NAAIM Exposure Index came in at 98.15, pushing right back toward the top end of its historical range and showing that active managers remain heavily allocated to equities despite the choppiness in price action and sentiment. That’s a meaningful rebound from just two weeks ago, when readings slipped into the mid-80s, and it highlights how quickly professional positioning has snapped back. In other words, while the AAII Bull-Bear spread is flashing renewed caution at the retail level, the institutional crowd isn’t blinking—allocation is sitting near max long, with no bearish exposure showing up in the aggregate. It’s a telling divergence: Main Street is nervous, Wall Street is still leaning in.

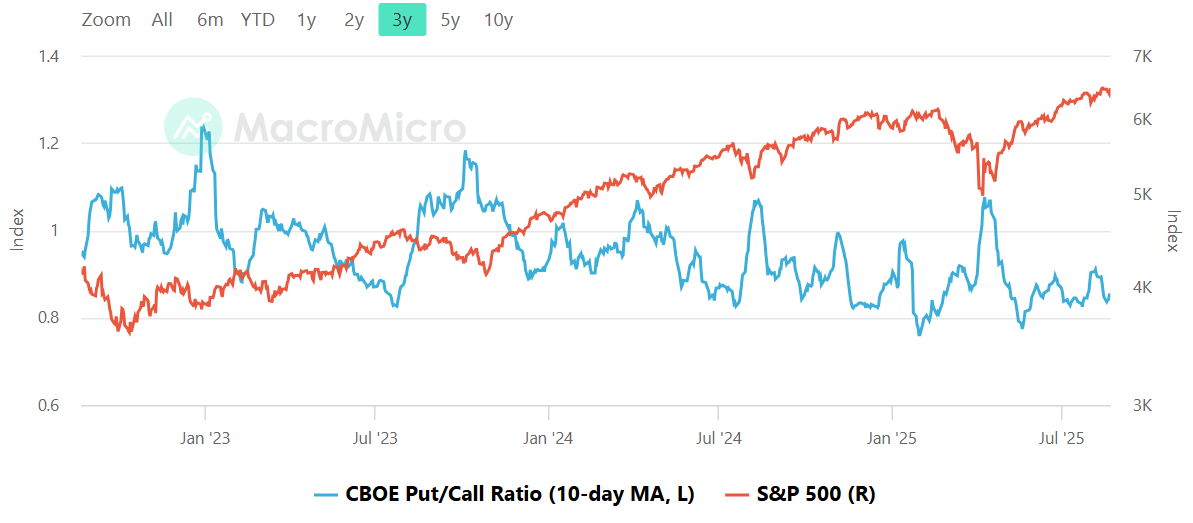

CBOE Total Put/Call Ratio

CBOE's total put/call ratio includes index options and equity options. It's a popular indicator for market sentiment. A high put/call ratio suggests that the market is overly bearish and stocks might rebound. A low put/call ratio suggests that market exuberance could result in a sharp fall.

Right now the CBOE total put/call ratio, smoothed on a 10-day basis, is sitting just under 1.0, which tells us that traders are leaning slightly more toward calls than puts but not in an extreme way. Historically, when this ratio spikes well above 1.0, it tends to coincide with fear-driven selloffs, while dips below 0.8 usually reflect complacency at market highs. What’s notable here is that the ratio has backed off from the fear levels we saw during the late-spring pullback and has settled back into its mid-range as the S&P has climbed to new highs. In other words, option sentiment is balanced—there’s no sign of panic hedging, but we’re also not at euphoric levels that often mark short-term tops.

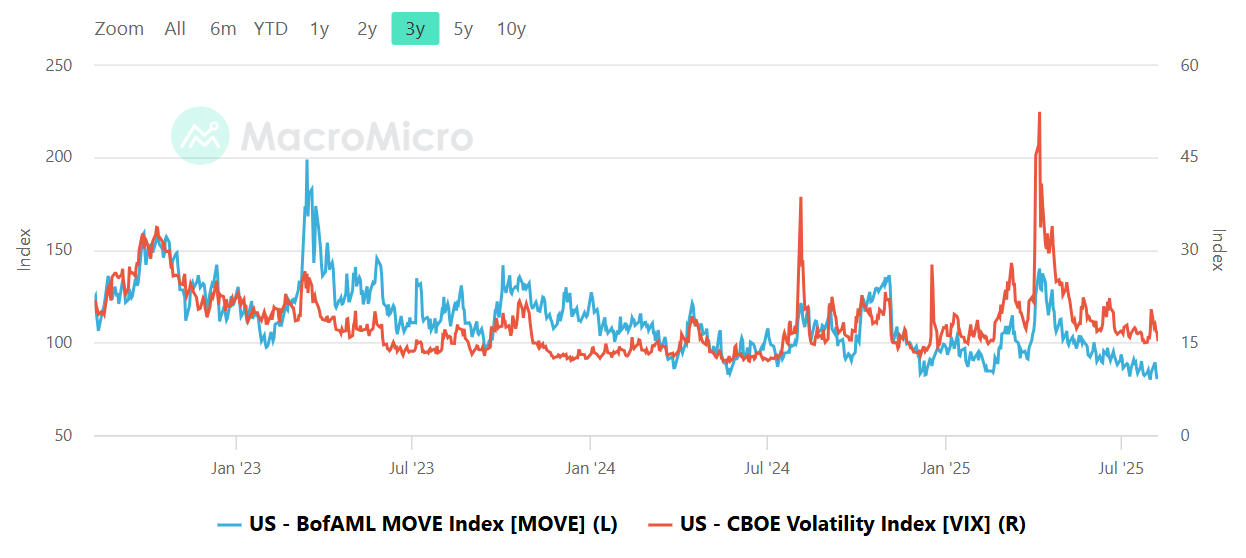

Equity vs Bond Volatility

The Merrill Lynch Option Volatility Estimate [MOVE] Index from BofAML and the CBOE Volatility Index [VIX] respectively represent market volatility of U.S. Treasury futures and the S&P 500 index. They typically move in tandem but when they diverge, an opportunity can emerge from one having to “catch-up” to the other.

Right now the divergence between equity and bond volatility is striking. The MOVE index, which tracks Treasury market volatility, has been grinding steadily lower and is now near its calmest levels in years—back toward the low-100s after peaking above 200 in early 2023. By contrast, the VIX hasn’t followed it down nearly as far; equity volatility has been sticky in the mid-teens, even after the summer rally. This split suggests that while the bond market is signaling confidence in stability around rates and macro policy, equity traders are still carrying some hedges against earnings risk, geopolitics, or just the sheer speed of the rally. Historically, when bond vol collapses while equity vol lingers, it can mean equities have a bit more room to grind higher as hedges bleed out—but it also means any surprise shock is more likely to show up in stocks first, since bond traders have stopped paying up for insurance.

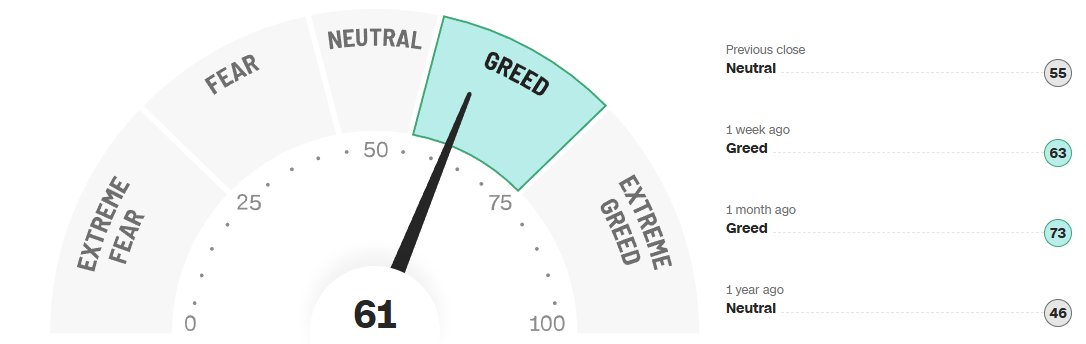

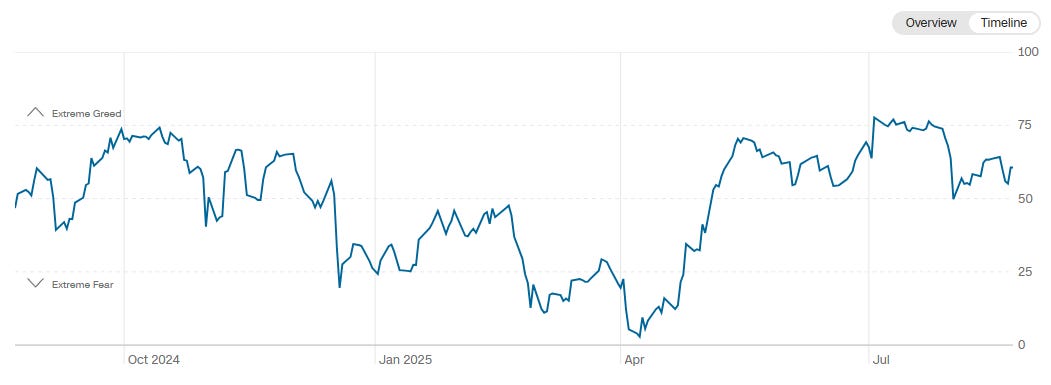

CNN Fear & Greed Constituent Data Points & Composite Index

The CNN Fear & Greed Index is sitting at 61, which puts it firmly in “Greed” territory—though it’s eased a bit from the higher readings we saw a month ago, when it touched into the low 70s. The recent dip from those levels lines up with the market’s late-summer wobble, but even so, sentiment remains far from fearful. Compared to a year ago, when the gauge was at 46 and leaning neutral, this shift shows just how much risk appetite has come back into play. Traders aren’t in full-on euphoria, but the bias is still toward optimism, with enough greed in the mix to keep markets buoyant while also raising the chance that positioning could get crowded if conditions turn.

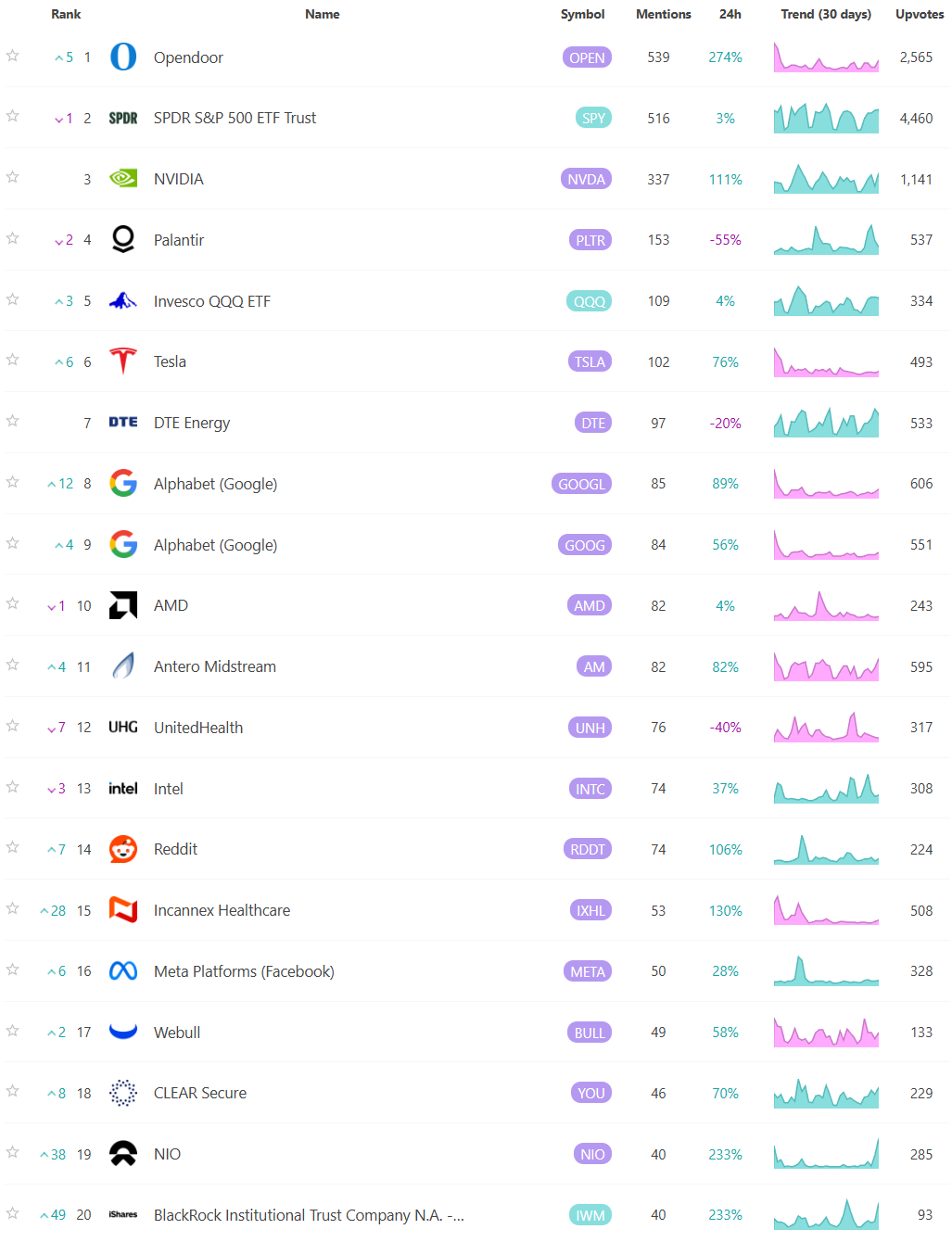

Social Media Favs

Social sentiment offers a real-time view of investor mood, often revealing market shifts before traditional indicators. It can signal momentum changes, spot emerging trends, and gauge retail investor impact—especially in high-volatility names. Tracking sentiment around events or earnings provides actionable insights, and when layered with quantitative models, can enhance predictive accuracy and risk management. Sustained sentiment trends often mirror broader market cycles, making this data a valuable tool for both short-term trades and long-term positioning.

Institutional S/R Levels for Major Indices

When you’re a large institutional player, your primary goal is to find liquidity - places to do a ton of business with the least amount of slippage possible. VolumeLeaders.com automatically identifies and visually plots the exact spots where institutions are doing business and where they are likely to return for more. It’s one of the primary reasons “support” and “resistance” concepts work and truly one of the reasons “price has memory” - take a look at the dashed lines in the images below that the platform plots for you automatically; these are the areas institutions constantly revisit to do more business.

Levels from the VolumeLeaders.com platform can help you formulate trades theses about:

Where to add or take profit

Where to de-risk or hedge

What strikes to target for options

Where to expect support or resistance

And this is just a small sample; there are countless ways to leverage this information into trades that express your views on the market. The platform covers thousands of tickers on multiple timeframes to accommodate all types of traders.

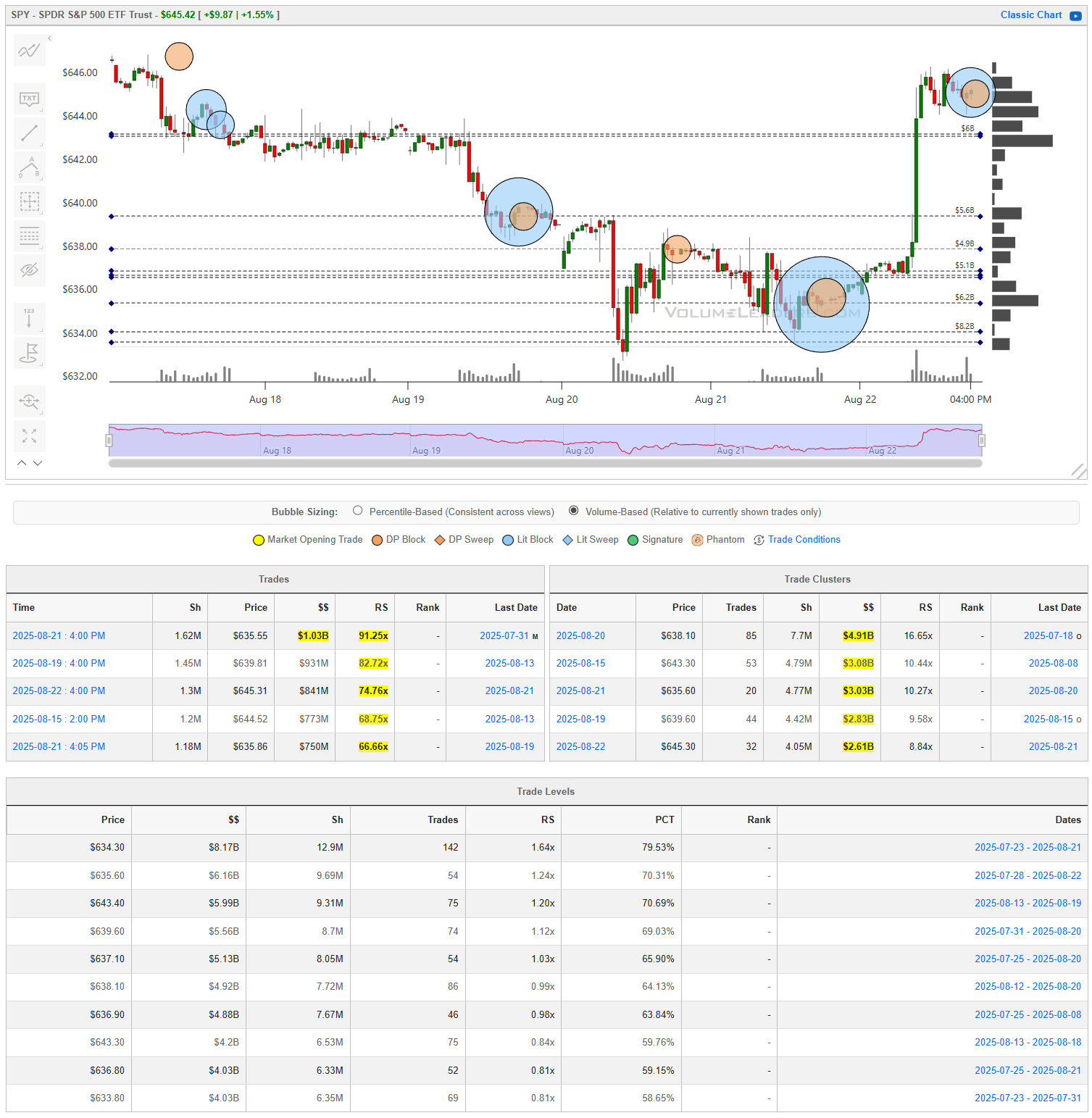

SPY

The SPY chart over the past week shows a textbook washout and rebound dynamic. The selloff into August 21 was met with a series of large institutional prints clustered around the $635–$640 zone, signaling accumulation as liquidity thinned. Those trades stood out not just in size—$1B+ blocks hitting—but also in relative size, with RS readings in the mid- to high-70s and even breaching 90% at the $635.65 pivot. By Friday, August 22, the payoff was obvious: SPY launched higher, ripping nearly 2% in a single session, with the heaviest buying pressure clustering at the $644–$645 shelf and carrying momentum into the close. The tape tells a clear story—institutions stepped in aggressively at the lows, and the market rewarded them with a sharp relief rally, turning what looked like capitulation into a springboard for upside. $640-$644 is looking pretty thin so some caution is warranted under $644 going into next week; holding $644 on a re-test confirms the upside impulsiveness and that this isn’t the spot to fight the tape.

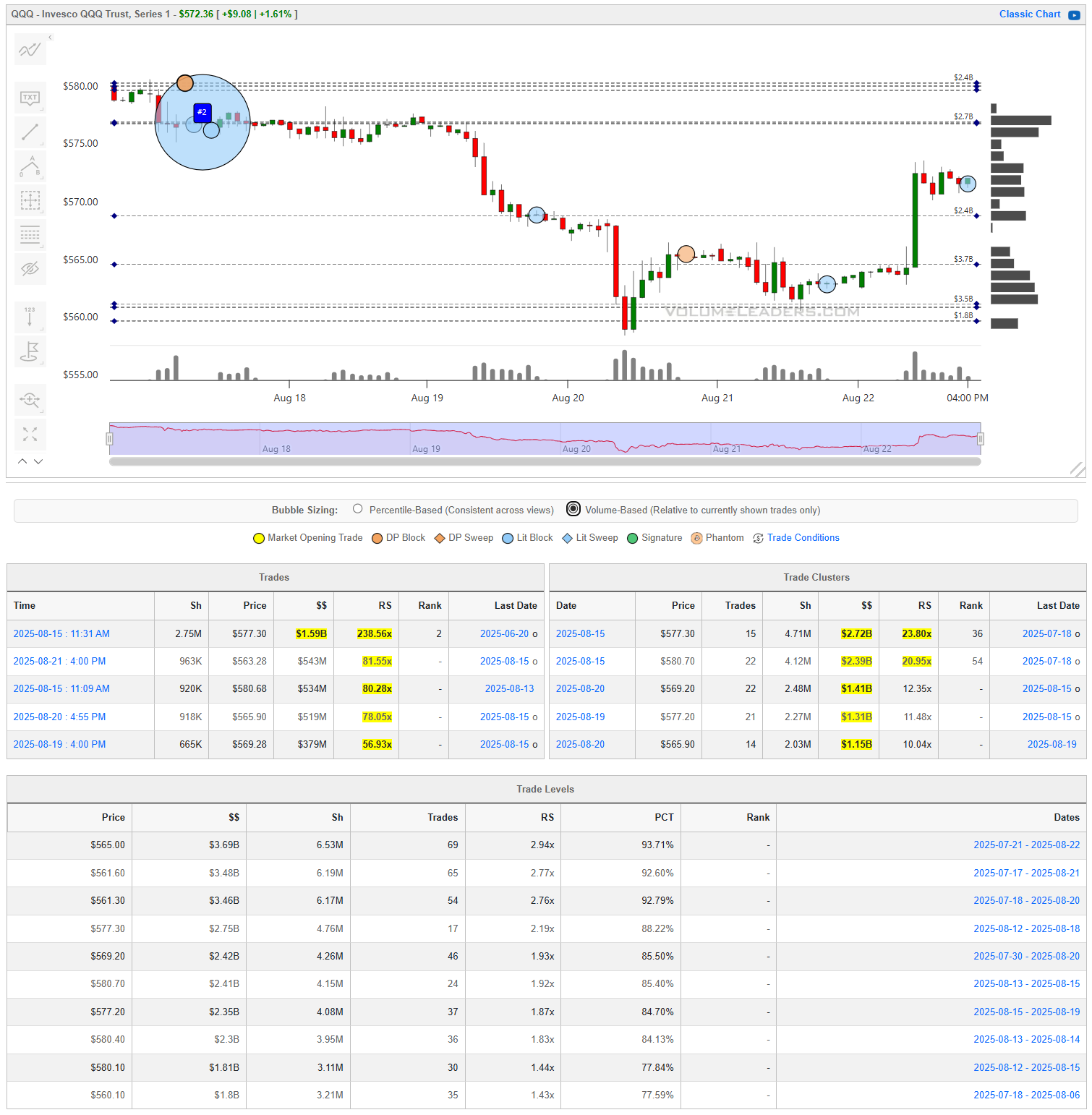

QQQ

The story begins with that monster August 15 print at $577.30 — nearly $1.6B notional and an RS of 238.5x. That’s not just outsized; it’s seismic. It dwarfs every other flow on the board and immediately set the tone for the week. What followed was a string of heavy trades in the low $560s to high $560s — $543M at $563.20, $534M at $566.80, $519M at $566.90. The clustering tells us that liquidity was being leaned on heavily as QQQ broke down, with institutions happy to size up their footprints while pressing price lower.

By August 20, the tape showed those same blocks concentrated in the $565–$570 band, totaling billions in flow. That became the fulcrum zone where institutions were most active, and by Friday’s rebound QQQ vaulted straight back into liquidity zone for the weekly close. Notably, the late-day prints on August 20 now look like small tactical longs for the pop that ensued.

The rebound to $572+ into the weekend leaves us with a clear takeaway: institutions showed their hand with notably more activity at the highs, presenting as supply. They were willing to get aggressive around $575. Small buyers were present in the $560-$565 range but they don’t appear to be a substantial threat to sellers above, especially with the week closing under that #2. Earlier commentary about tech breadth and relative underperformance this week further support the current sell-thesis in this ETF.

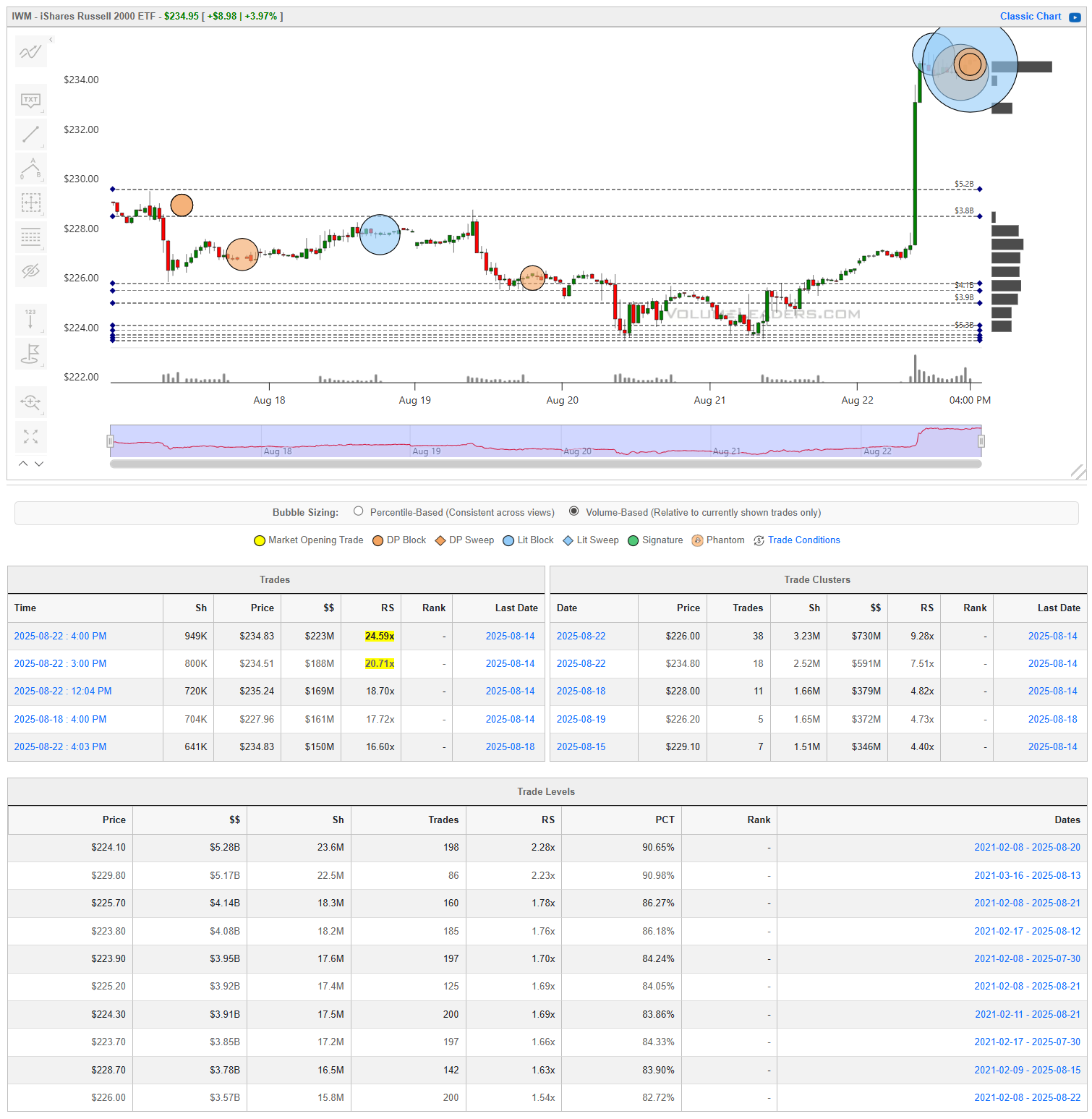

IWM

The Russell has been the laggard all summer, but this past week it finally staged a sharp reversal that deserves a closer look. The breakdown through $228 earlier in the week was accompanied by steady institutional activity, but not the kind that suggested aggressive conviction. Flows on August 18 clustered around $227–$228, with $160M–$180M trades going off. That looked more like liquidity provision than directional firepower, and price continued leaking lower Thursday into some quiet levels creating a liquidity pool at the lows.

What changed was Friday’s surge where the tape ignited. By the close, IWM had ripped nearly 4% higher and pinned against $235–$236, with the heaviest notional of the week ($730M) stacked right into the ramp. That sequence reframes the week entirely: instead of another failed rally, small caps just absorbed size at the lows and then rocketed higher on a wave of committed buying.

The key takeaway is that the $234–$236 zone is no longer just another stop on the chart; it’s now a battle-tested pocket where institutions finally leaned in. The Russell has been missing from the leadership rotation, but with this kind of footprint, the tape suggests small caps may be ready to join the party.

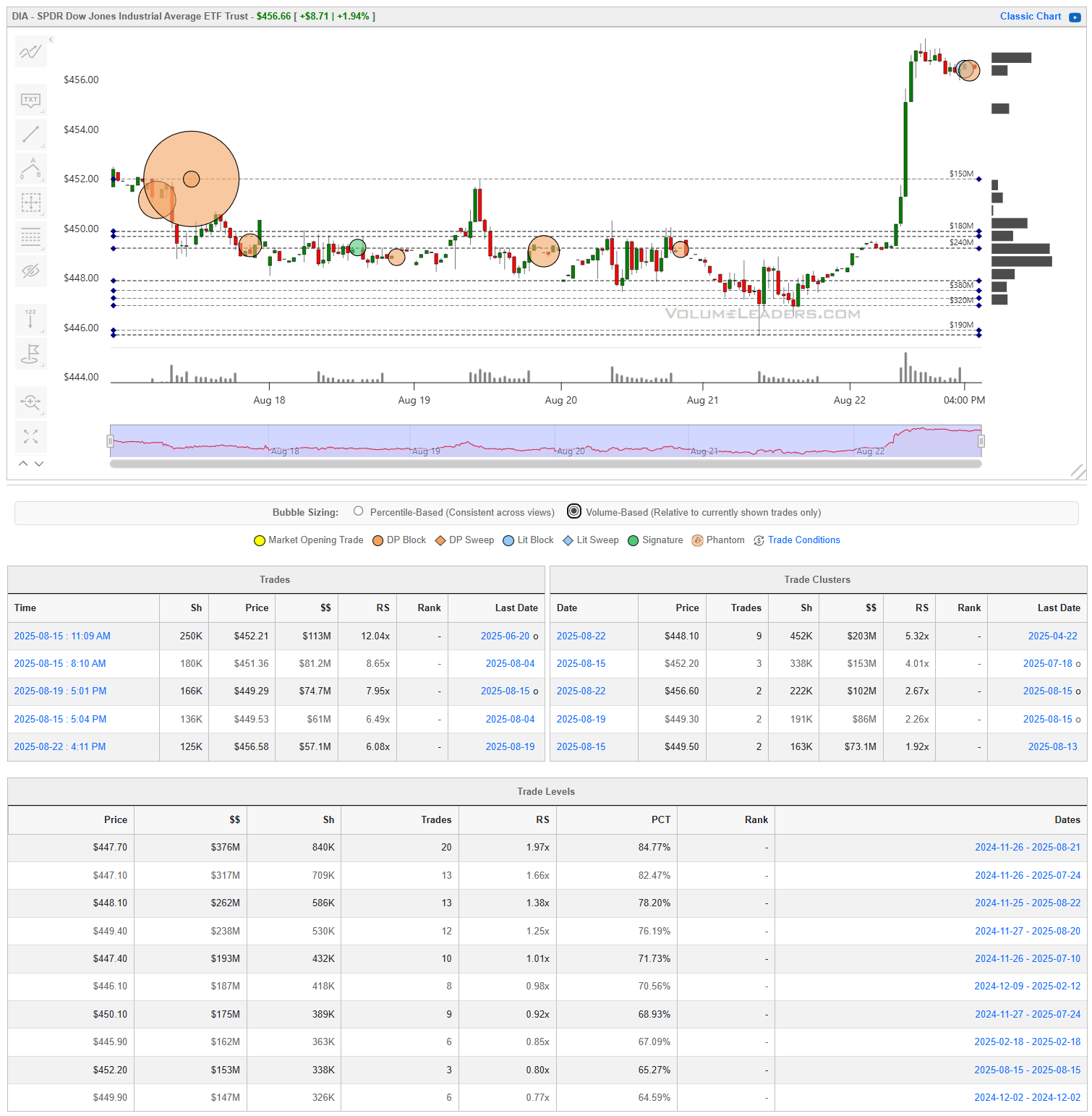

DIA

The Dow was the quiet one most of the week, trading in a tight $448–$452 range while other indices showed more decisive moves. But the tape wasn’t dead. On August 15, a $113M block hit at $452.21, the largest single Dow trade of the week, and that print effectively marked the ceiling for the next several sessions. Institutions were active inside that band — $74M at $449.39 and $61M at $449.30 on the 19th — but nothing that looked like real commitment.

That changed on Friday. The index gapped higher, chewed through the earlier block zone, and sprinted toward $456. The push carried size with it: $203M at $448.10 was the key anchor, with follow-through clusters building into the afternoon. By the close, the Dow had ripped nearly 2% and settled well above the prior congestion, flipping the week’s lethargy into a statement of strength.

The important shift here is context. For most of the week, the Dow looked like it was being capped by supply at $452. Friday’s action redefined that zone — the same level that had been a lid now looks more like a shelf of support, with institutions showing they’re willing to absorb risk beneath.

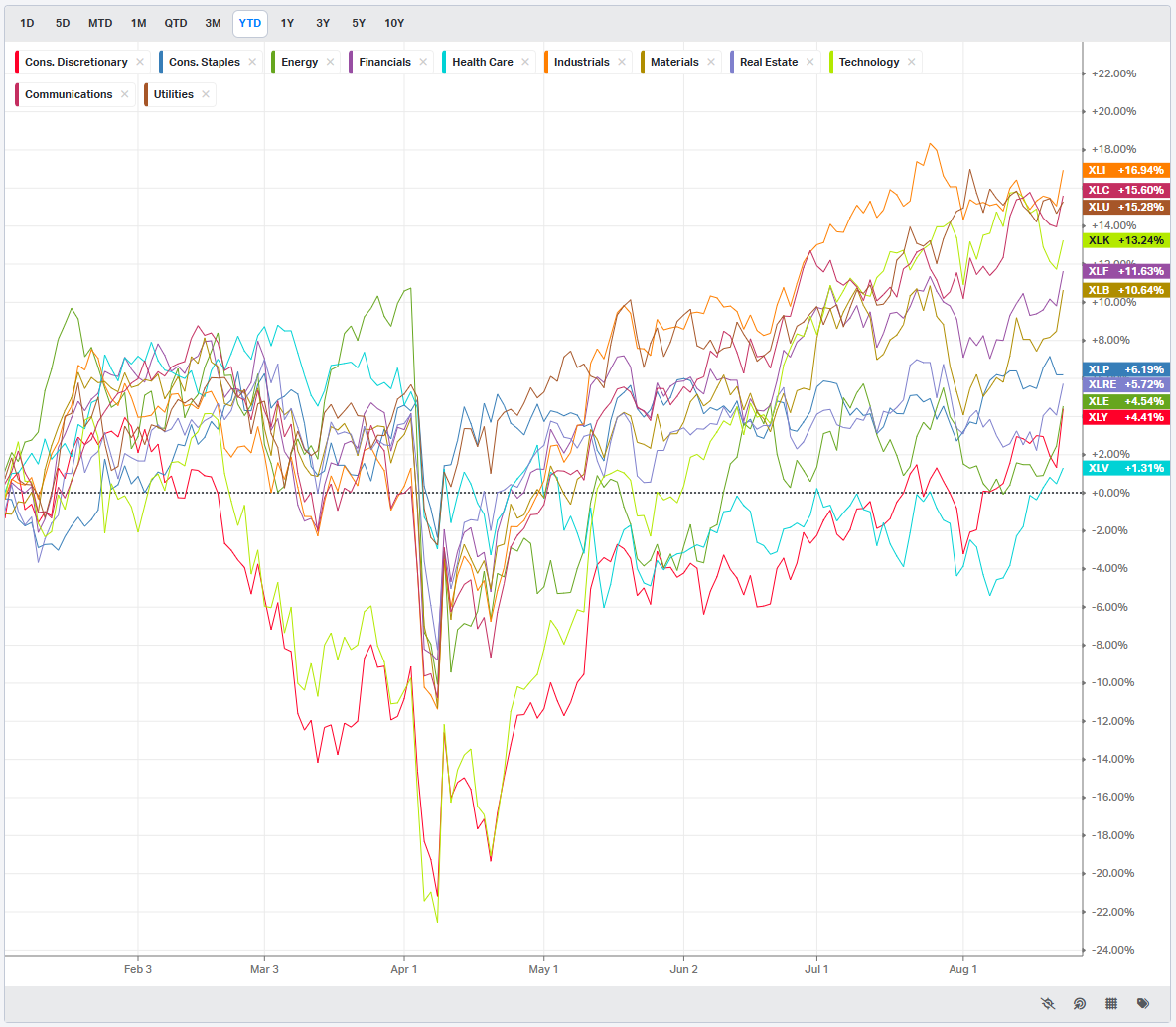

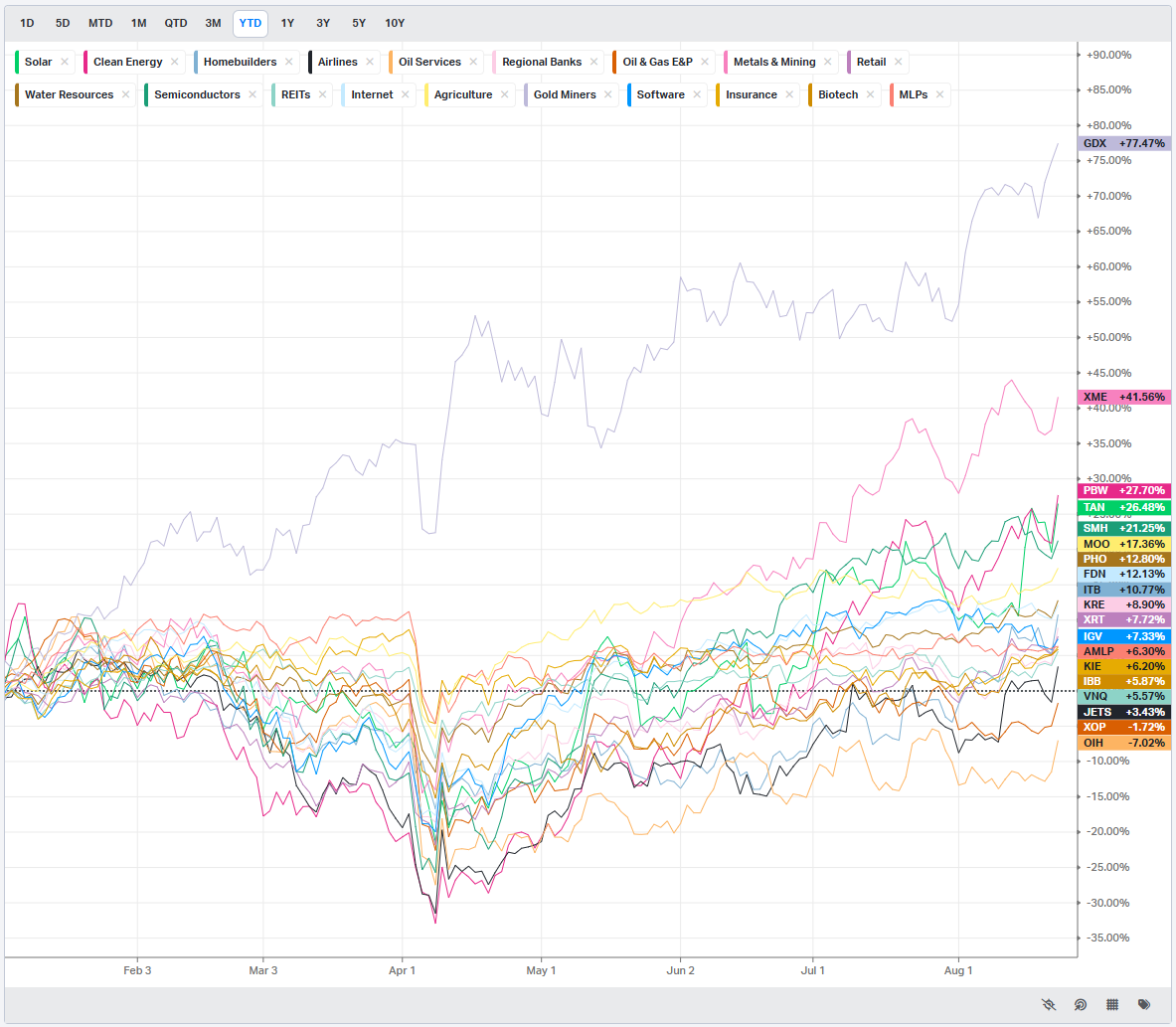

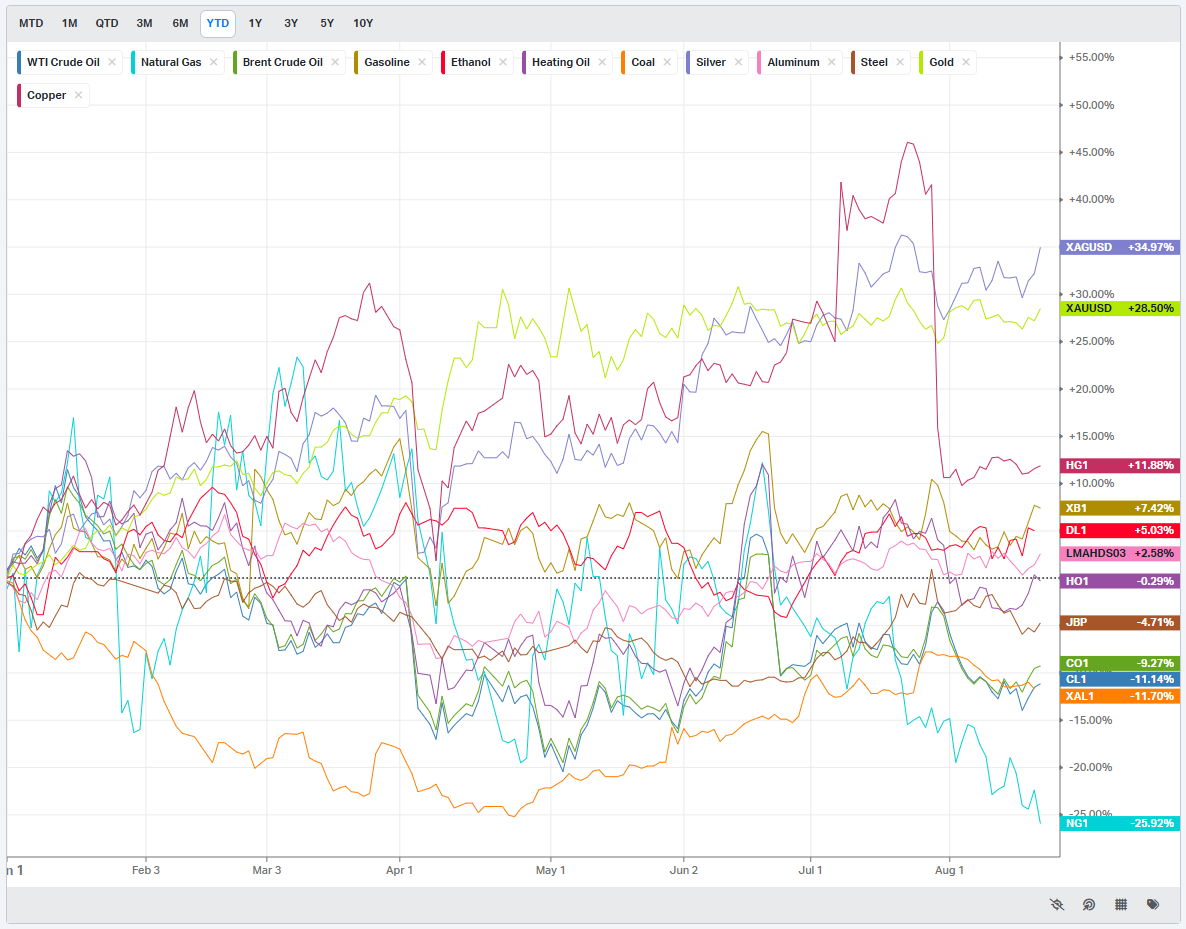

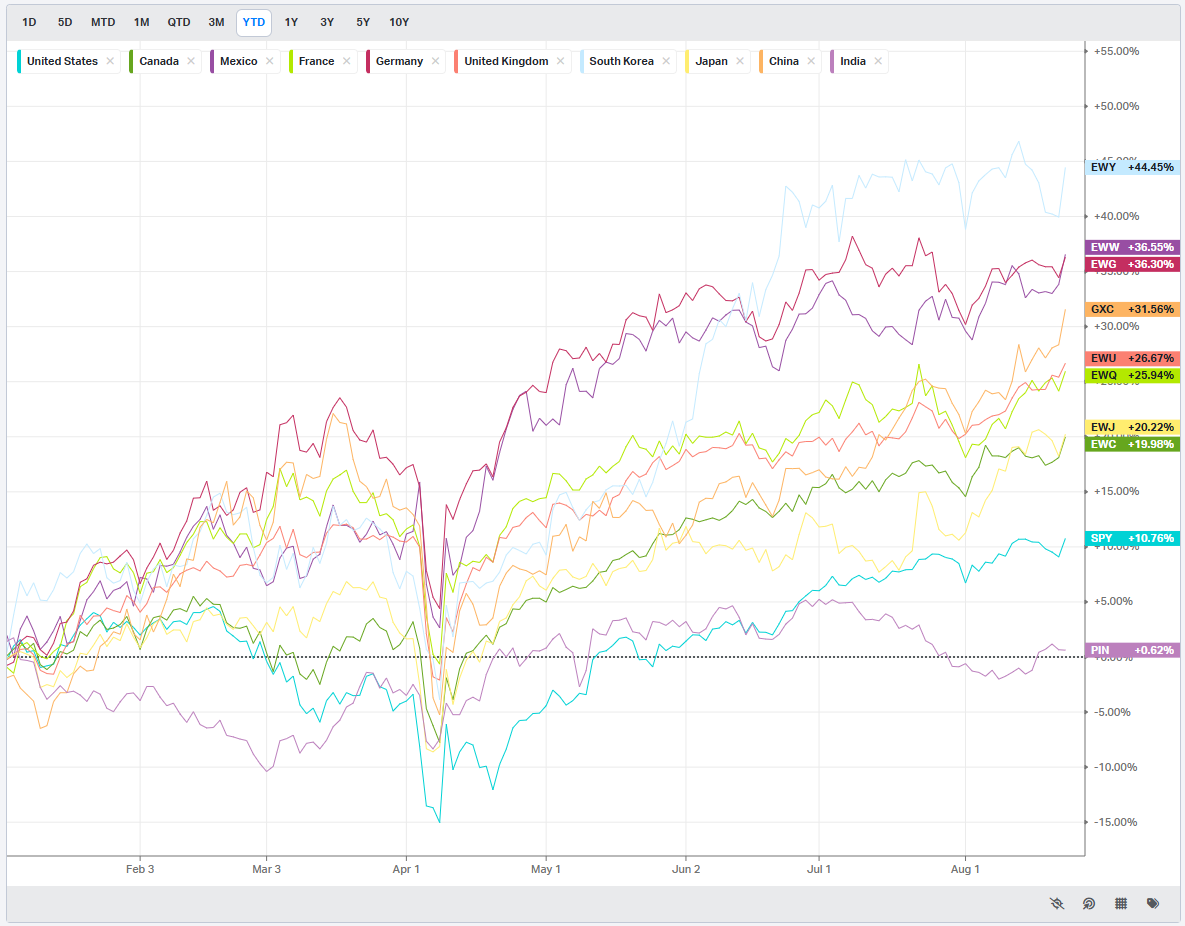

Summary Of Thematic Performance YTD

VolumeLeaders.com offers a robust set of pre-built thematic filters, allowing you to instantly explore specific market segments. These performance snapshots are provided purely for context and inspiration—think about zeroing in on the leaders and laggards within the strongest and weakest sectors, for example.

S&P By Sector

S&P By Industry

Commodities: Energy & Metals

Country ETFs

Currencies/Major FX Crosses

Factors: Style vs Size-vs-Value

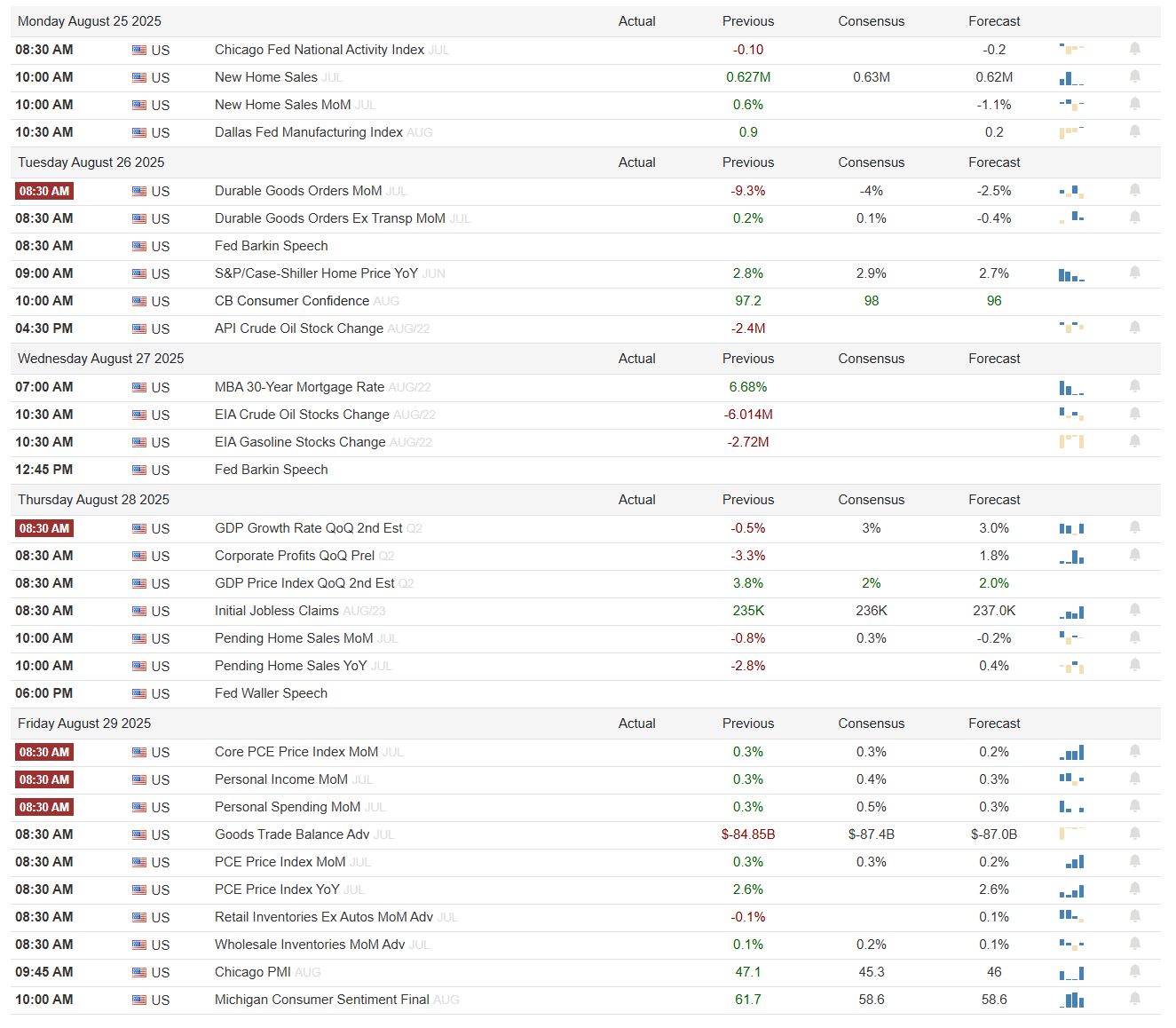

Events On Deck This Week

Here are key events happening this week that have the potential to cause outsized moves in the market or heightened short-term volatility.

Econ Events By Day of Week

It’s a macro-heavy week with housing (Mon/Tue), confidence (Tue), and Fed speakers early — but the real meat is Thursday GDP revisions + Jobless Claims, followed by Friday’s Core PCE and Personal Spending. Those two days are the main volatility windows.

Anticipated Earnings By Day of Week

Looking ahead to next week, the earnings calendar is stacked and it’s not just a matter of who’s reporting, but the sequencing of those reports that matters for flows and sentiment.

We start light with Pinduoduo (PDD) Monday morning and HEICO (HEI) after the close—interesting but unlikely to drive the broader tape. The real action begins midweek.

Tuesday night brings Okta (OKTA) and MongoDB (MDB), both high-beta SaaS names. In this environment where software multiples are being constantly repriced, they can set the tone for cloud sentiment into Wednesday.

Wednesday is the monster session. Before the bell we get Abercrombie (ANF), Williams-Sonoma (WSM), Royal Bank of Canada (RY), and Smucker’s (SJM)—a mix of discretionary, housing-adjacent, staples, and financials. That gives us a cross-section of consumer health and credit trends right as markets are debating the soft-landing narrative. But it’s the after-close slate that will dictate the week: NVIDIA (NVDA), CrowdStrike (CRWD), Snowflake (SNOW), HPQ, Veeva (VEEV), Pure Storage (PSTG), NetApp (NTAP), Trip.com (TCOM), Bill.com (BILL), and Five Below (FIVE). That’s AI, cybersecurity, cloud, legacy tech, travel, payments, and specialty retail all in one breath. If markets are looking for leadership confirmation, this is where they’ll find it—or not. NVDA’s print is the gravitational force here; everything else orbits around it.

Thursday morning keeps the retail pulse front-and-center with Best Buy (BBY), Dollar General (DG), Dick’s Sporting Goods (DKS), Burlington (BURL), Li Auto (LI), and TD Bank (TD). It’s a clean look at discretionary vs. defensive spending and auto vs. traditional retail. Then Thursday night adds another wall of market-moving tech: Dell (DELL), Marvell (MRVL), Affirm (AFRM), Ulta (ULTA), Autodesk (ADSK), Gap (GPS), Ambarella (AMBA), and a handful of smaller but still thematically important names like Iris Energy (IREN) and Elastic (ESTC).

By Friday, there’s nothing of note—which means positioning going into the weekend will largely be dictated by the Thursday close reaction.

This isn’t just another earnings week—it’s one of those inflection weeks where leadership is tested. NVDA in particular carries systemic weight: if the AI trade still has legs, the whole growth complex breathes easier. But layer in BBY, DG, DKS, and ULTA, and you’ve got a check on the real economy and consumer wallets. Financials via RY and TD bookend it with credit/housing exposure.

The setup, then, is a bifurcated test: tech vs. the consumer. If both fire, the rally extends. If only one side shows strength, leadership narrows. If both falter, breadth collapses fast.

Market Intelligence Report

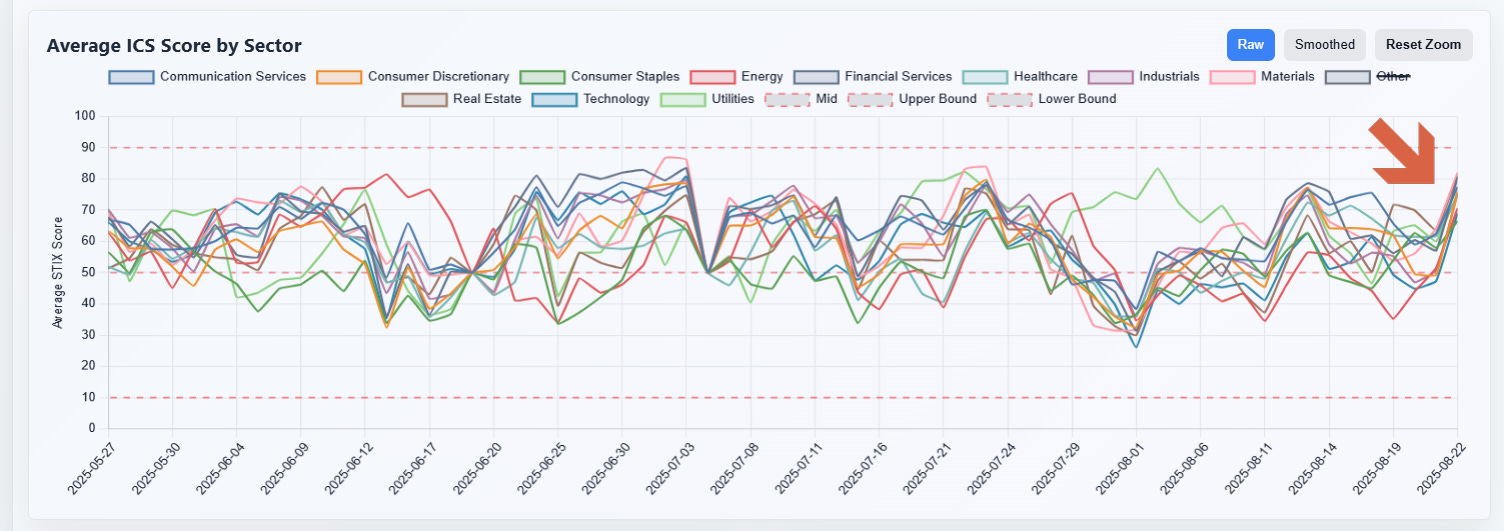

Let’s stitch the week together from the top down. The big picture first: breadth and sponsorship both snapped higher at the same time. On the breadth side, all four major benchmarks pushed a clear majority of constituents back above their intermediate trend gauges (the S&P 500’s 5‑day read sat north of 80%, with the 100–200‑day cohorts in the 70s), and the Russell 1000 showed the same “many stocks up together” signature. On the sponsorship side, your Institutional Conviction Scores (ICS) accelerated sharply across every sector and, unusually, in lockstep—most groups vaulted from the mid‑50s to the high‑60s/70s in a matter of days.

That sort of synchronized institutional thrust usually needs a policy nudge, and Powell’s Jackson Hole remarks provided a clean catalyst: he said policy is now “100 bps closer to neutral,” that the balance of risks has shifted, and that the Committee can “proceed carefully” with adjustments rather than stay on a preset path. Markets read that as permission to lean risk‑on rather than brace for renewed tightening. There is much ado on Fintwit about this chart:

It shows SPX mean reverting to the 100 MA 25 out of 27 times after Jackson Hole since 1999 so bears have a little history to lean on here despite the messaging from Powell.

Where the dollars actually went

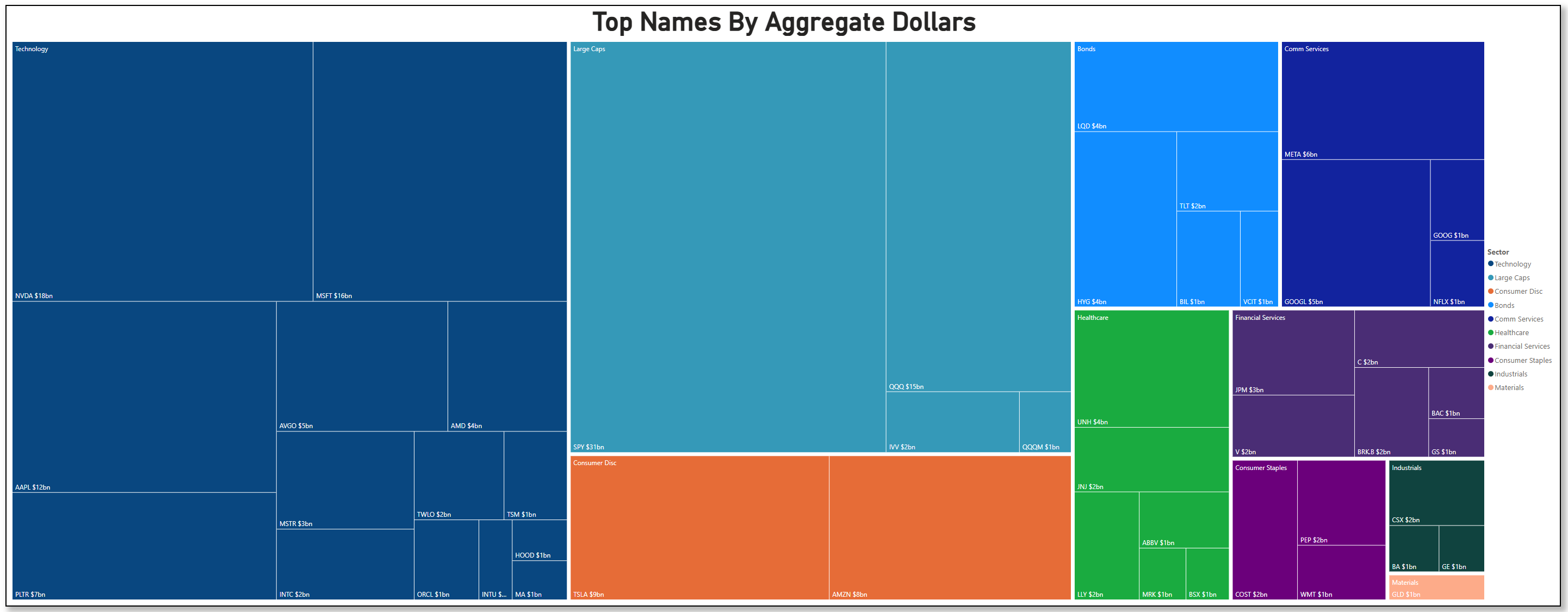

Over the last two trading weeks, the tape shows Technology and “index beta” (SPY/QQQ plus Large‑Cap baskets) doing most of the heavy lifting, with Communication Services and Consumer Discretionary forming the second tier. Defensives—Staples, Utilities—participated but trailed, and Financials/Healthcare caught a steady bid rather than a surge. Said differently: the money that moved chose growth, scale, and liquidity first, then broadened.

Drilling into this week’s tree map clarifies the leadership. In Tech, NVDA (~$18B), MSFT (~$16B), and AAPL (~$12B) were the largest single‑name dollar magnets, with AVGO, AMD, TSM and the software tail (ORCL, INTU, TWLO, PLTR, MSTR) rounding things out. In index beta, SPY (~$31B) and QQQ (~$15B) dominated, with IVV/QQQM adding incremental flow. Discretionary dollars were concentrated in TSLA (~$9B) and AMZN (~$8B); in Communication Services, META (~$6B) plus GOOGL/GOOG (~$5B each) led. Bond ETFs were not quiet either—LQD and HYG (~$4B each), with TLT/VCIT/BIL pulling smaller but notable prints.

Financials skewed to money‑center/liquidity names (JPM, C, V, BRK/B), Healthcare to mega‑cap quality (UNH, LLY, JNJ, ABBV, MRK), and Industrials saw targeted flow (CSX, GE, BA). That ordering—mega‑cap tech, platform consumer, and liquid beta—maps cleanly to the breadth thrust you’re seeing: institutions paid first for what they could scale quickly, then started to extend down the quality curve.

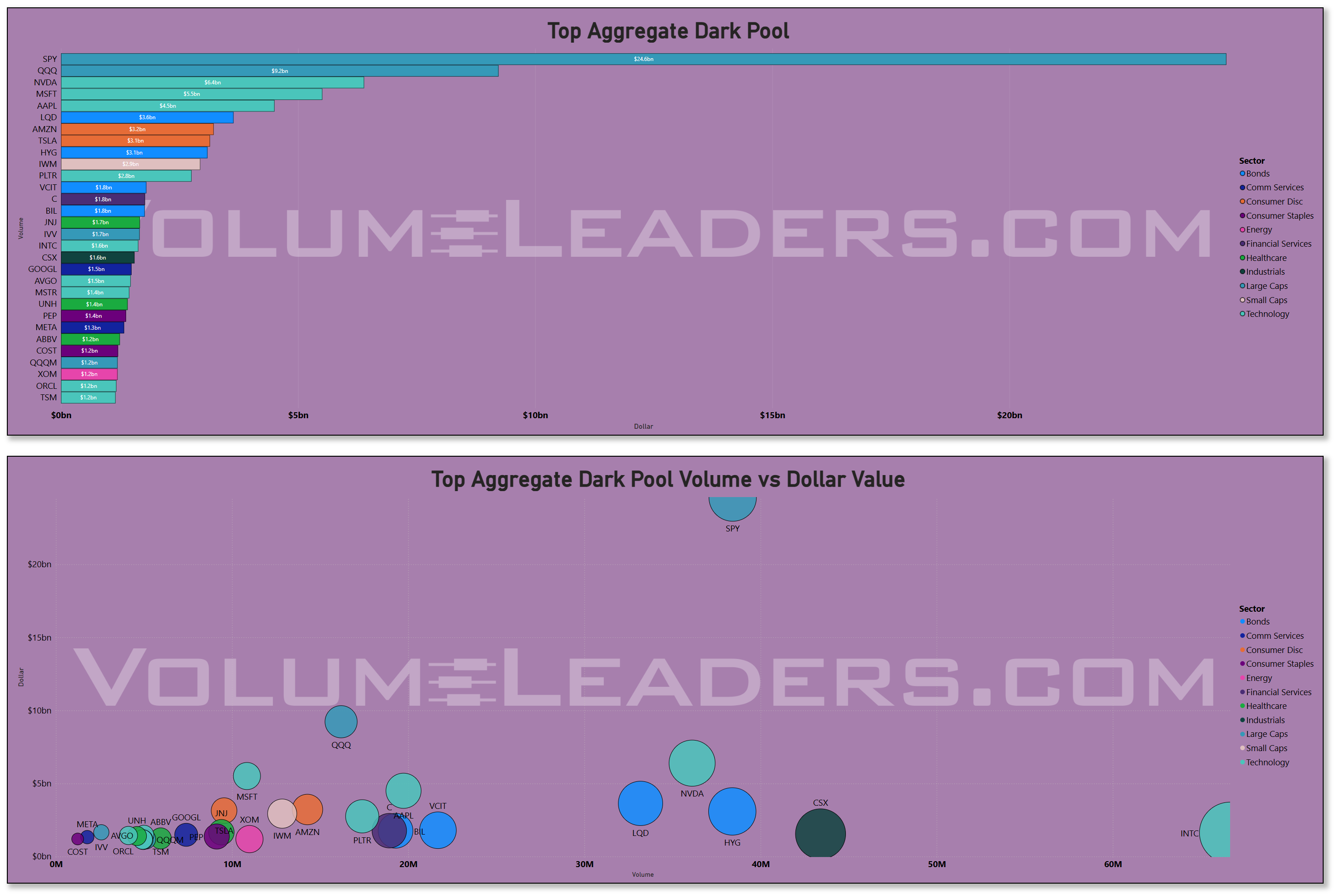

Dark Pools and Sweeps

The dark‑pool dashboard backs that story. SPY absolutely dwarfed everything in notional routed through ATS venues, with QQQ the clear No. 2 and the big Tech trio right behind. Two outliers are worth flagging.

INTC showed a very large bubble on the volume‑versus‑dollars scatter—outsized tape count relative to notional—almost certainly tied to news of the Government’s 10% stake in the chip maker, acquired as part of a deal where the government invested $8.9 billion in Intel, converting previously awarded CHIPS Act grants into equity.

CSX also printed a large bubble—meaningful dollars with heavy share count. Here we do have a clean catalyst: BNSF and CSX announced an intermodal service partnership that materially improves East–West connectivity via Memphis, a real, near‑term revenue and share‑take story in the rails. That announcement hit on August 22.

While the collaboration itself was intended to enhance service offerings, the market interpreted it as a sign that a potential merger between CSX and BNSF was less likely, leading to the decline in CSX's stock. This was further exacerbated by the fact that the announcement came on the heels of news about a proposed merger between Union Pacific and Norfolk Southern, which could significantly alter the competitive landscape within the railroad industry. Investors may have viewed CSX's partnership with BNSF as a defensive move in response to the potential UP-NS merger, rather than a step towards further industry consolidation that could have benefited CSX.

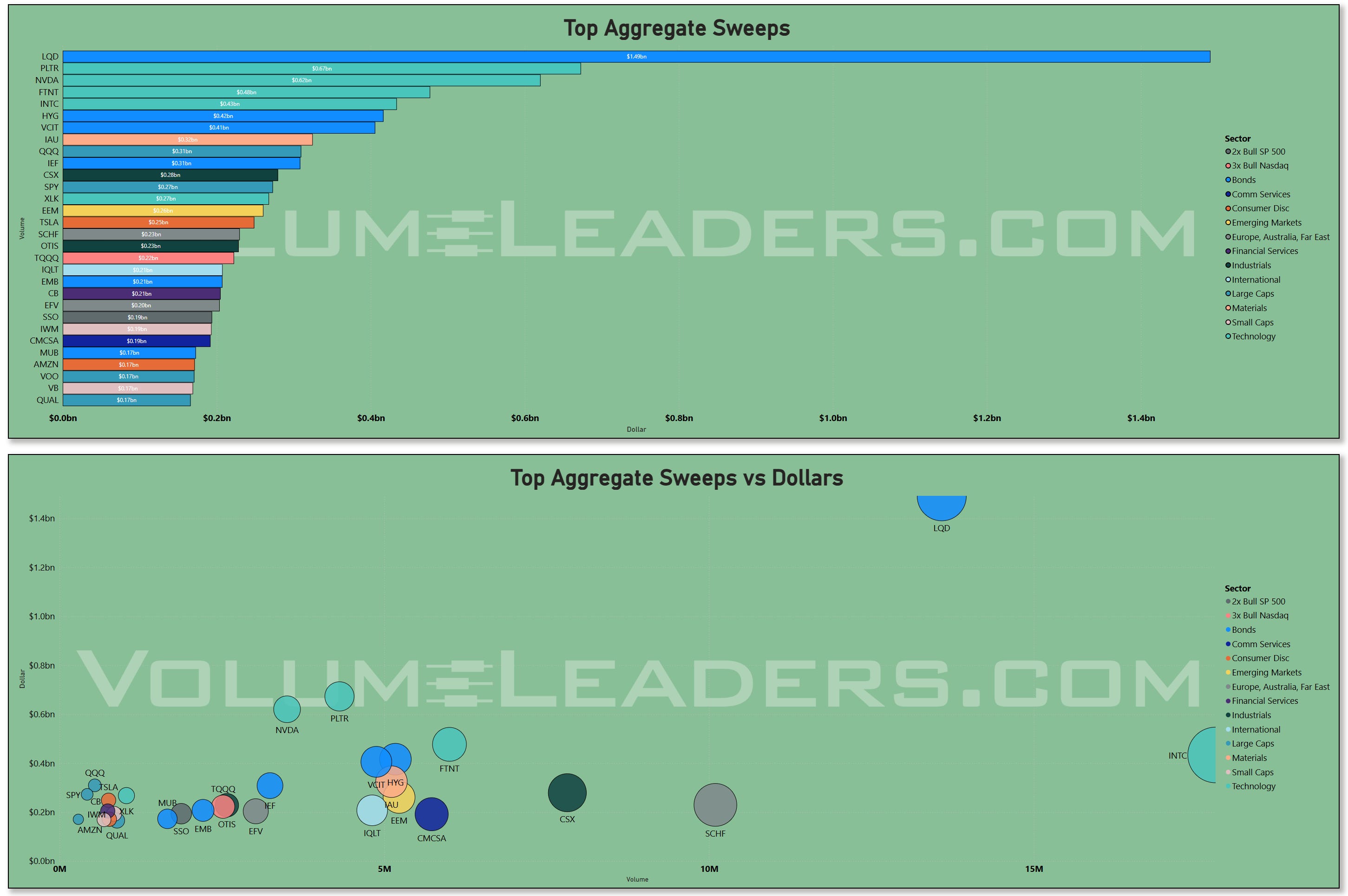

On “urgency” specifically, the sweep tape continues to feature LQD (it’s practically part of the plumbing now), but the names that pop as stories are PLTR, NVDA, and FTNT.

PLTR sits at the intersection of AI software procurement and rising federal/commercial pipelines; NVDA is still the capital‑expenditure fulcrum for AI infrastructure; and FTNT’s prints echo the cybersecurity budget cycle that tends to follow big AI and cloud rollouts. The cluster tells you the sub‑theme: “AI stack + secure deployment.” With Powell green‑lighting risk and fiscal/industrial policy still steering capex onshore, that complex remains the preferred hunting ground for urgency orders.

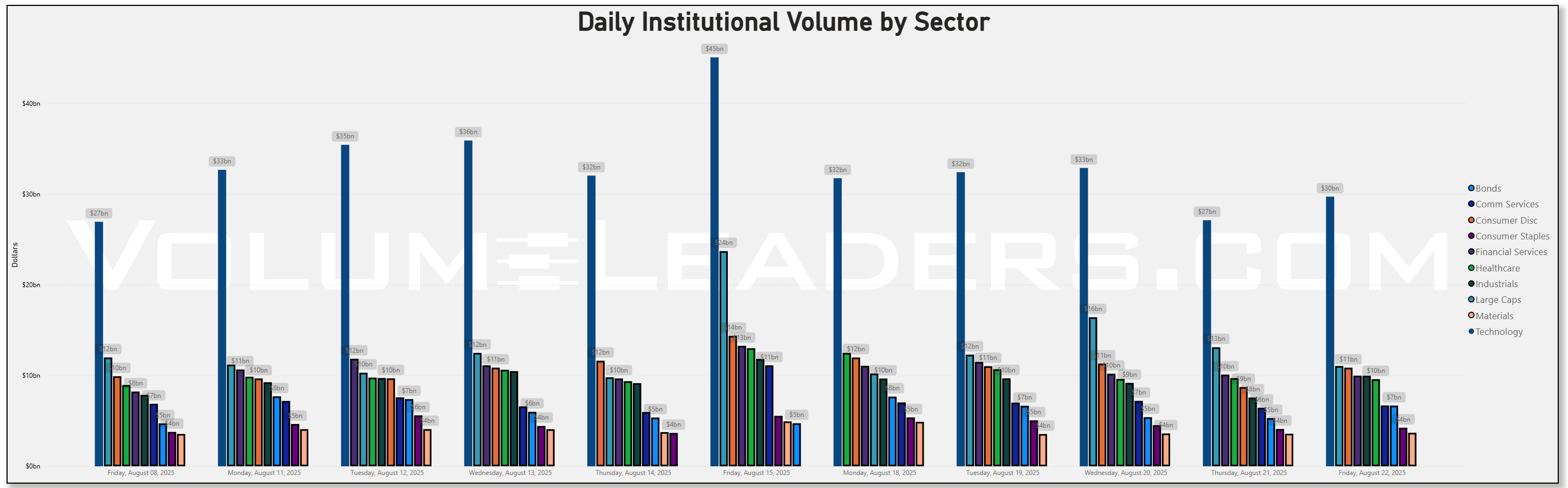

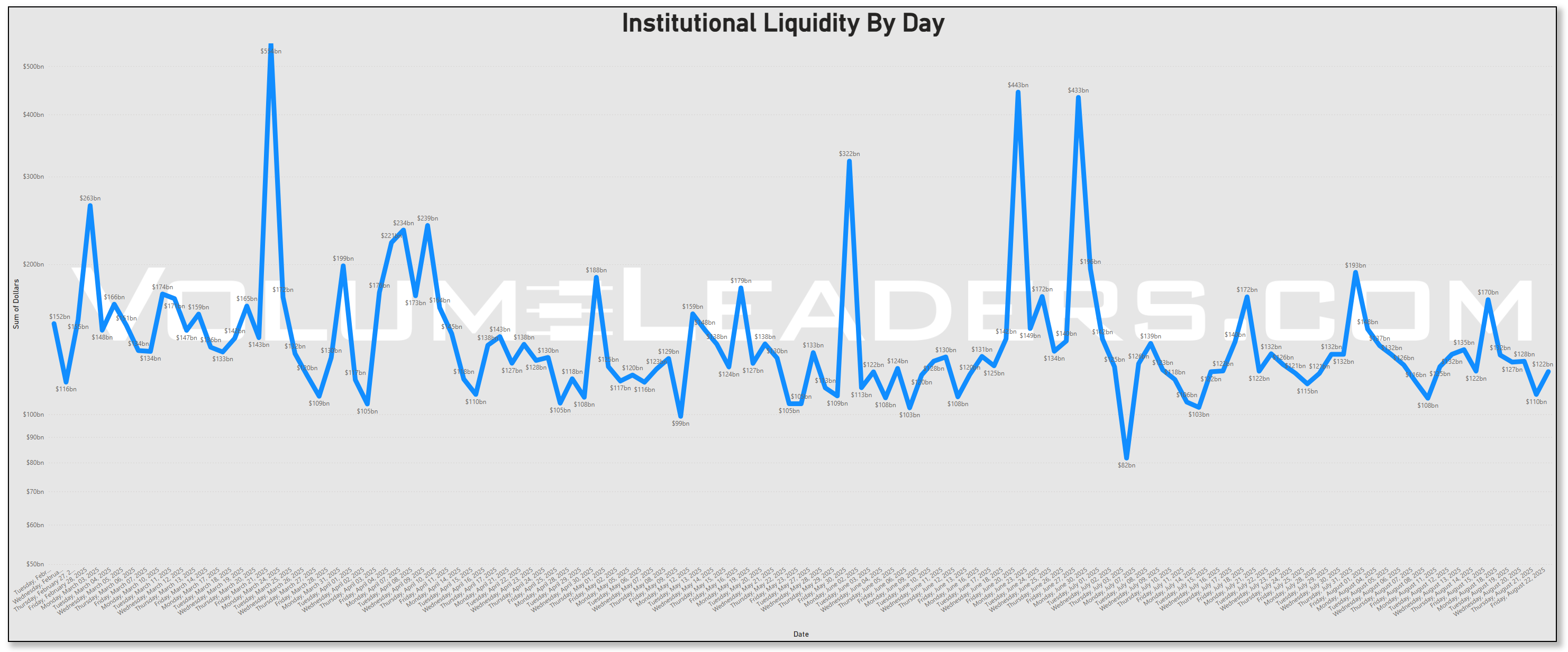

Liquidity regime and timing

The Institutional Liquidity by Day series shows what everyone on the desk felt: summer was thin, punctuated by a few large liquidity days, then the dollars started marching back up into late August. That re‑risking coincides with: (1) Jackson Hole’s “closer to neutral” messaging, (2) the seasonal end‑of‑summer rotation, and (3) a market that had already repaired breadth and momentum underneath. When breadth improves and sponsorship (ICS) rises and policy risk eases, the path of least resistance is higher until the tape runs into supply or macro data knocks it back.

This is shaping up to be a tough tape for bears to fight. Fundstrat’s Tom Lee is onboard with a 10% correction from here but it’s not clear what’s going to spook bulls from piling in here after Powell’s latest messaging.

How this changes positioning

Put the mosaic together and the institutional preference set looks like this:

First tier remains Mega‑Cap Tech + Index Beta. That’s where the biggest checks cleared, and where incremental money can still hide if volatility returns.

Second tier is AI‑adjacent software and security, plus scaled consumer platforms and select rails/industrials with tangible catalysts (the CSX/BNSF linkage fits; watch the other Class I rails for sympathy positioning).

Rates/credit are being used tactically: steady flow in LQD/HYG/VCIT provides ballast and optionality if the soft‑landing narrative wobbles.

That hierarchy aligns perfectly with the ICS surge: Tech, Comm Services, and Discretionary all ripped higher together, while Financials and Healthcare kept pace without leading. It’s exactly what we’d expect if investors are upgrading cyclicality but still hugging quality and liquidity.

What to watch next

Two things can reinforce or undercut this risk‑on turn. First, the macro tape: next week is stuffed with tier‑1 data—GDP revisions, PCE, PMI, and housing—plus another slate of large‑cap earnings. If those prints come in “goldilocks” (inflation cooler, activity resilient), the synchronized ICS breakout should continue and breadth can extend and run super hot. If we get a growth scare or a re‑acceleration in the PCE internals, the bond‑ETF bid probably intensifies and the equity tape rotates back toward the most liquid leaders.

Second, follow‑through in the dark pools and sweeps. If the heavy notional stays concentrated in SPY/QQQ/mega‑cap Tech while urgency orders keep clustering in PLTR/NVDA/FTNT‑type names, the AI‑plus‑platform theme remains the field’s base case. If we start seeing sustained urgency in cyclicals (industrial supply chain, transports ex‑rails, small‑cap value) alongside rising ICS there, that would mark a genuine phase‑two broadening.

Bottom line: policy tone shifted just enough to let positioning breathe, and institutions wasted no time scaling into the most liquid expressions of growth and AI. Breadth is healthy, sponsorship is rising, and liquidity is returning. Until the macro tape disagrees, the path of least resistance is to stay aligned with that preference stack—own the liquid leaders, keep a sleeve in the AI stack and its security layer, and use credit ETFs as the shock absorber while we test how far this breadth thrust can run.

Individual Names with Institutional Interest

VolumeLeaders tracks several proprietary signals designed to spotlight names drawing significant institutional interest. Below, we’ve surfaced the latest results and analyzed them in aggregate to highlight emergent themes. If any of the sectors, narratives, or positioning trends resonate, the names mentioned here offer a strong starting point for deeper research and watchlist consideration in sessions ahead.

VL Trade Rank Velocity™ (TRV)

TRV is a proprietary metric that measures the recent acceleration or deceleration in institutional trading activity for a given stock by comparing its average trade rank over the past few days to its average in recent weeks. A sharp improvement in TRV typically reflects a notable shift in positioning, often accompanied by sustained trade activity, suggesting institutions are actively engaging with the name and that intensity of activity is rising. This often precludes meaningful price or narrative shifts. This isn’t a buy-list or sell-list; it’s meant to draw your eyes to names where institutions are putting money to work.

Emergent Themes from the TRV Watchlist

Sometimes the most revealing insights aren’t found in headline indexes or mega-cap earnings calls but buried in the velocity of institutional positioning — where dollars accelerate into names that rarely make CNBC’s ticker crawl. This week’s TRV leaderboard makes that point crystal clear. What emerged wasn’t just a continuation of the AI trade, but something broader, more eclectic, and perhaps more telling about how professionals are thinking about the next leg of the cycle.

Technology still leads, but the flavor is different.

It’s no surprise to see tech claim the top slot again, but the roster is less about the household names and more about what lies beneath the surface. TLS, FIG, and SKYT aren’t the banner carriers of Silicon Valley hype, yet they’re attracting sharp inflows. IT services, software-application players, and niche semis are drawing consistent institutional sponsorship. The message is subtle but important: institutions are broadening their tech footprint beyond Nvidia and Microsoft, scattering exposure across the stack rather than betting only on the generals. That diversification suggests two things — one, there’s genuine conviction in the sector’s staying power, and two, some recognition that concentration risk in the “magnificent” few has grown uncomfortable.

Crypto is not going away quietly.

BMNR, BLSH, EZBC — acronyms unfamiliar to many casual traders, but they’ve carved their way onto the TRV list alongside leveraged crypto proxies like MSTZ. Institutional engagement with crypto-adjacent equities has been sticky even as Bitcoin itself consolidates. Whether it’s tactical hedging against policy risk, or speculative capital anticipating another volatility burst, the takeaway is that institutions are no longer treating crypto as a sideshow. They’re weaving it into the broader alternatives toolkit, even if exposure is fragmented.

Industrials and materials are moving back into fashion.

One of the week’s more interesting signals came from the marine shippers (NMM), metals and miners (EQX, SSRM, OR), and construction/engineering plays (STRL). None of these names are momentum darlings, yet they’re catching real flow. That lines up neatly with the tariff drumbeat out of Washington — steel, aluminum, semiconductors, even furniture components suddenly in the trade crosshairs. When the policy winds shift like this, institutions don’t wait for confirmation in GDP prints; they front-run the supply chain impact. The accumulation in these sectors looks like exactly that: early rotation into the logistical and industrial arteries that will feel tariffs first.

Healthcare is quietly being accumulated.

Biotech and healthcare services are showing up again and again in the middle ranks — PROK, HUMA, XERS, CELC, AXGN, CRGX. These aren’t the mega-cap pharmaceuticals that dominate sector ETFs, but rather the under-the-radar innovators and mid-caps. That clustering suggests an accumulation trend in the space. Whether institutions are gaming potential election-year policy shifts, hunting for idiosyncratic alpha, or simply rotating into a sector that’s been lagging all year, the signal is too consistent to ignore. Healthcare may be one of the few places where institutions see asymmetry: limited downside after a long period of underperformance, with optionality tied to catalysts.

Energy flows are scattered, but uranium stands out.

Institutional energy exposure isn’t clean — there’s no one-sided bet on crude. Instead, the flows are fragmented: uranium miners like URNJ, midstream names like HESM, traditional drillers like SOC, and equipment providers like VTOL all make appearances. The uranium bid is notable — it reflects the sticky narrative of nuclear as a cornerstone of long-term energy security, particularly with tariffs and geopolitics reshaping the commodity complex. This is less about speculative leverage to oil and more about diversified energy bets that span the spectrum from fossil to alternative.

Financials are selective, not wholesale.

Perhaps the most striking absence is a broad wave into financials. Instead, the list is dotted with specific names in insurance (HIPO, BOW), specialty finance (PJT), and niche brokers. That tells us institutions aren’t buying the whole sector — they’re cherry-picking where they think balance sheets or business models can withstand, or even benefit from, the shifting policy and rate environment. In other words, financials are not a sector call right now; they’re a stock-picker’s playground.

What to make of it all?

The TRV picture this week reinforces the theme of broadening leadership. Technology remains the strongest current, but it’s spreading into smaller, less obvious streams. Crypto is hanging around longer than skeptics expected, while industrials and materials are catching policy-driven bids. Healthcare is quietly building a base of support, and energy is fragmenting into multiple thematic sub-trades. Financials, meanwhile, are about precision strikes, not blanket allocations.

If you zoom out, the signal here is that institutions aren’t running a monolithic playbook. They’re probing, diversifying, and positioning for a market where policy, tariffs, and Fed risk are just as important as earnings beats. The concentration in mega-cap tech is loosening at the edges, and that alone makes the TRV board worth watching closely.

VL Institutional Outliers™ (IO)

Institutional Outliers is a proprietary metric designed to spotlight trades that significantly exceed a stock’s recent institutional activity—specifically in terms of dollar volume. By comparing current trade size against each security's recent normalized history, the metric flags outlier events that may indicate sudden institutional interest but may be missed because the activity doesn’t raise any flags/alerts when comparing the activity against the ticker’s entire history. For example, it’s conceivable that a ticker today receives the largest trade it has had in the last 6 months but the trade is unranked and would therefore be missed by current alerts built off Trade Ranks. Use “Realized Vol” to identify tickers with large price displacement and to size your risk appropriately.

Emergent Themes from the Institutional Outliers Watchlist

Every week, there are tickers that break from the pack — not because they’re trending on social media or flashing across retail dashboards, but because the size, urgency, or persistence of institutional flow around them simply refuses to be ignored. This week’s IO Watchlist reads like a cross-section of where conviction is being tested, rewarded, and sometimes punished.

At the very top of the list, Gildan Activewear (GIL) turned heads with unusual size. The scale of flow here would be easy to dismiss as an outlier in consumer discretionary, but the reality is that textiles and apparel are deeply exposed to the tariff story. If institutional players are leaning into this space, it may be more about front-running the pricing power embedded in staple clothing than betting on a consumer boom.

Technology, as usual, is everywhere — but it’s not just the usual mega-cap suspects. Twilio (TWLO) led on abnormal sigma prints, and what makes it stand out isn’t just the size, but the direction. Software names like TWLO are being repriced not as speculative growth but as infrastructure plays in a world where enterprise IT spending has proven more resilient than feared. Similarly, Qualys (QUAL) and Bill.com (BILL) posted strong IO readings, reinforcing that software tied to payments, security, and back-office functions continues to draw sticky attention.

Energy names showed up prominently too. Viper Energy (VNOM) and Sitio Royalties (STR) both printed significant sigma scores, confirming that while crude prices have been rangebound, institutional positioning is still quietly building in the royalty and exploration pockets of the space. That dovetails with the uptick in PMI manufacturing input costs tied to tariffs: the energy complex is indirectly being repriced as cost inflation seeps through.

Healthcare remains a minefield — but one institutions are willing to step into. Novavax (NVAX), Cytokinetics (CYTK), and Edwards Lifesciences (EW) were among the biotech and medtech names drawing unusual flow. These are not broad-based sector allocations, but targeted shots — a reminder that even in a defensive sector, conviction shows up in concentrated bursts. The IO data suggests investors are bracing for binary outcomes around trials and regulatory catalysts.

On the financials side, banks like KBE, HBNC, and TCBI popped up, echoing the broader theme we’ve been flagging for weeks: institutions are leaning into regional banks, even if the tape still looks heavy. The presence of diversified insurers (MFC) and specialty finance names suggests this isn’t a one-off — it’s a sector-wide recalibration of risk premia.

And then there are the oddballs that demand a second look. CSX, the rail operator, showed up with size — the tape punished the stock on merger chatter. Meanwhile, crypto proxies like HODL, ETHU, and BMNR made the list, underscoring that digital asset–linked equities are increasingly treated as liquid leverage on macro sentiment rather than fringe speculation.

Finally, it’s worth noting the utilities and REITs that crept into the Watchlist (XIFR, VRE, RHP). These sectors rarely print on institutional outlier screens unless positioning is shifting beneath the surface. Given Powell’s Jackson Hole pivot, the logic isn’t hard to trace: duration-sensitive names are back in play as rate cut odds get priced higher.

Bottom Line

This week’s institutional outliers suggest that money isn’t just chasing momentum — it’s building positions in areas that align with a softening Fed and a still-resilient consumer. That’s constructive, but it also raises the stakes: if Powell backtracks or tariffs bite harder than expected, the same sectors could unwind quickly. For now, though, the IO Watchlist looks like the scaffolding of a broader rally, not just another rotation within tech.

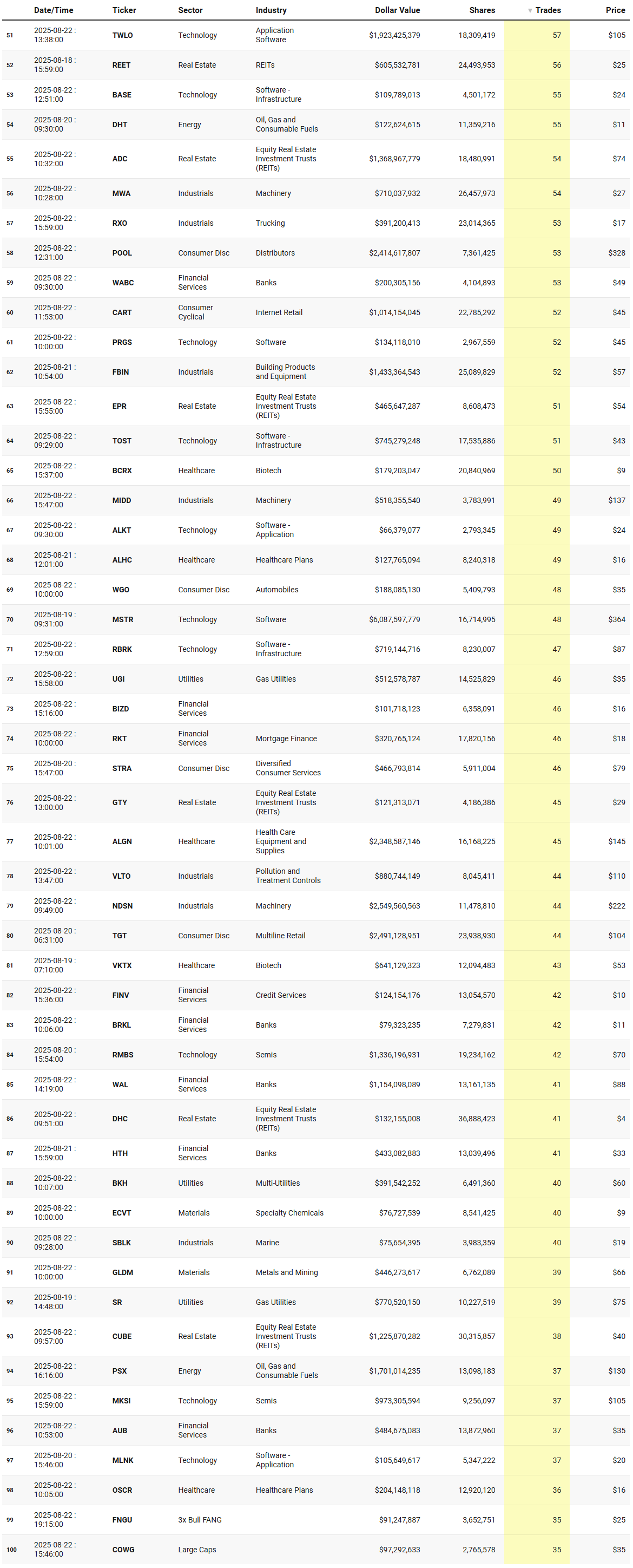

VL Consensus Prices™

These are the most frequently traded #1-Ranked Levels in VL this week. Trades occurring at the highest volume price in a ticker’s history are significant because they represent institutional engagement at a key price memory level—where the market once found consensus. These areas act as liquidity hubs, enabling large players to transact efficiently, and often signal a reassessment of fair value. This activity may precede major moves, mark equilibrium zones, or reflect broader portfolio shifts, making these price levels important to watch even without yet knowing how price will resolve. (Note: many Bond products trade in such a tight range that they dominate the top positions and are therefore omitted to provide better clarity around other flows. The data is still available in the VL platform however.)

Emergent Themes from the Consensus Prices Runs Watchlist

The consensus levels offer a revealing cross-section of where institutions appear to be anchoring conviction. What stood out this week is the sheer clustering around semiconductors and technology adjacencies — AAPL, NVDA, AMZN, QCOM, MRVL, SOXL — all appearing near the upper tiers. This is not just noise: it lines up with the IO watchlist, TRV strength, and the Fed-driven macro backdrop. Even after a bruising rotational week, institutional consensus continues to treat the semi/AI complex as the spine of equity markets.

Interestingly, consumer discretionary names (NKE, AMZN, TGT) also show up prominently. That aligns with retail earnings resilience we saw last week and suggests institutions are willing to lean into consumer-led strength, even as tariffs introduce cost pressure. It looks more like a barbell approach: megacap retail/brands on one side, high-beta tech on the other.

Financials and banks (KEY, WABC, WAL) hold a middle-tier presence. That’s notable given how sensitive financials are to Powell’s dovish tone. The fact they show up in consensus levels indicates institutions are at least willing to defend positions here — less enthusiasm than tech, but not abandonment either.

We also see energy and industrials sprinkled throughout (CVX, CSX, LI, NXE). While not dominant, their consistent representation suggests rotational demand hasn’t disappeared; it’s simply running second-tier to the technology/consumer axis.

Finally, utilities and REITs (AES, SCHH, RYN, STAG, EPR) maintain visibility — not as leaders, but as ballast. Their inclusion in consensus levels shows institutions aren’t operating under a one-trade mindset; they’re keeping defense on the board, a recognition that Powell’s “shifting balance of risks” could cut both ways.

Synthesis:

The emergent theme is one of concentrated conviction in semis and AI, paired with selective consumer discretionary bets, while keeping financials and defensives in play as hedges. In other words, institutions are not scattering their chips; they are stacking them around a few durable narratives while still maintaining optionality in sectors that benefit if the Fed really does pivot dovish.

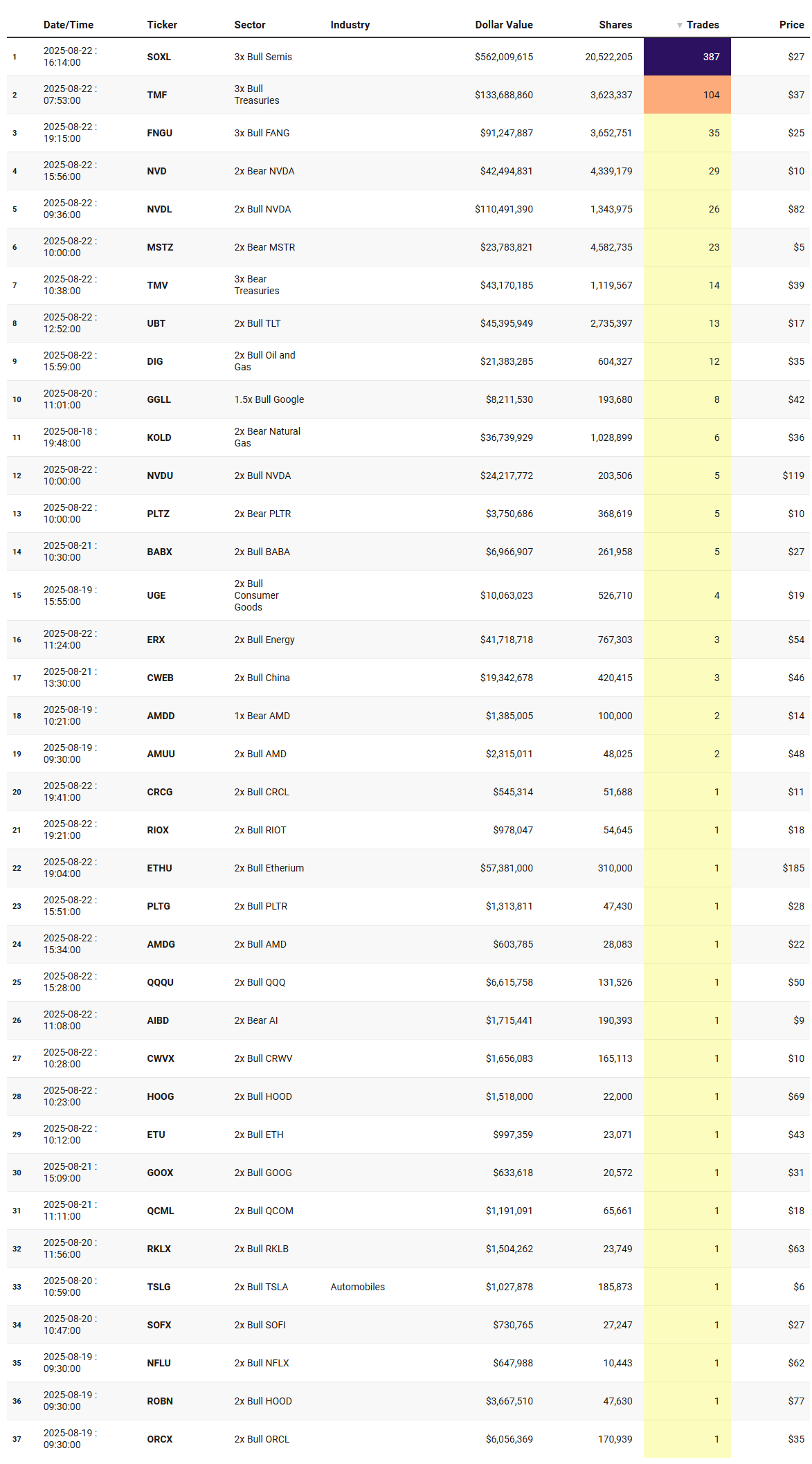

BONUS: Consensus Prices Watchlist for leveraged names from this week:

Thank you for being part of our community and for dedicating your time to this edition. Your insights and engagement drive everything we do, and we’re honored to share this space with such committed, thoughtful readers. Here’s to a week filled with clear opportunities and strong performance. Wishing you many bags 💰💰💰

—VolumeLeaders