Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 53 / What to expect July 14, 2025 thru July 18, 2025

NOTE: This weekly periodical is too large for Substack to deliver in its entirety via email - you will only see a portion of this great content if you read from your email client. Click the header/title at the top to read the full article!

In This Issue

[Free For Everyone]

Weekly Market-On-Close Report: All the macro moves, market drivers, and must-know narratives—covered in less than five minutes.

Weekly Benchmark Breakdown: Our weekly intelligence report on major indices cuts through the index-level noise to uncover participation, momentum, and structural integrity and tell you whether markets are rising on solid ground or skating on thin breadth. This is where bull markets prove themselves—or quietly start to unravel.

The Latest Investor Sentiment Readings: Track the emotional pulse of the market with our curated dashboard of sentiment indicators. From fear-fueled flight to euphoric overreach, this week's readings reveal whether investors are cautiously creeping in—or stampeding toward the exits.

Institutional Support & Resistance Levels For Major Indices: Exactly where to look for support and resistance this coming week in SPY, QQQ, IWM & DIA

Normalized Performance By Thematics YTD: Which corners of the markets are beating benchmarks, which are overlooked and which ones are over-crowded!

Key Econ Events & Earnings On-Deck For This Coming Week

[Only For Subs]

This Week’s Institutional Activity In Equities: Track the real money. This section breaks down where institutions are placing their bets—and pulling their chips. You'll get a sector-by-sector view of equity flows, highlighting the most active names attracting large-scale buying or selling. We go beyond the headlines and into the tape, surfacing the week’s most notable block trades and sweep orders, both on lit exchanges and hidden dark pools. Whether you're following momentum or fading crowded trades, this is your map to where size is moving and why it matters.

Institutional Activity By Day (rolling 6-months)

Institutional Activity By Sector By Week (rolling 6-months)

This Week’s Institutional Activity In ETFs: Follow the flows that shape the market. This section uncovers where institutions are deploying capital across the ETF landscape, broken down by sector and fund. We highlight the largest block trades and aggressive sweeps—both visible on lit exchanges and hidden in dark pools—to reveal how the smart money is positioning. Whether they’re rotating risk, hedging exposure, or scaling into themes, this is your lens into the ETF vehicles driving institutional intent.

Statistical Analysis and Insights From This Week’s Top Prints: we run the numbers on the most significant institutional trades of the week—those outsized prints that stand apart from the noise. Through statistical analysis and pattern recognition, we decode what these moves may signal about future price action. Whether it's the start of accumulation, a stealthy unwind, or a shift in market regime, this is where data meets intent. These are the trades that matter—and the stories they may be telling.

Weekly Market-On-Close Report

Markets Navigate Trade Tensions as Policy Uncertainty Persists

Executive Summary

Financial markets concluded a tumultuous week with mixed results as investors grappled with escalating trade tensions and policy uncertainty. The S&P 500 declined 0.27%, while the Dow Jones Industrial Average fell 0.66%, and the Nasdaq 100 dropped 0.17%. Despite these modest losses, markets demonstrated remarkable resilience in the face of renewed tariff threats and geopolitical developments.

The week's narrative was dominated by President Trump's announcement of expanded tariff measures affecting over 20 countries, with rates ranging from 15% to 50%. These developments, coupled with the recent passage of the One Big Beautiful Bill Act, created a complex policy environment that continues to influence market dynamics and Federal Reserve decision-making.

Equity Markets: Resilience Amid Uncertainty

Major Index Performance

U.S. equity markets exhibited a pattern of initial volatility followed by relative stability. The S&P 500's decline of 0.27% masked significant intraday movement, with the index reaching new all-time highs of 6,290 during Thursday's session before retreating on Friday's renewed tariff announcements.

The technology-heavy Nasdaq Composite demonstrated superior relative performance, reflecting continued investor confidence in the sector's growth prospects. This resilience was particularly noteworthy given the broader market's sensitivity to trade-related headlines.

September E-mini S&P futures declined 0.33%, while September E-mini Nasdaq futures fell 0.21%, indicating cautious sentiment heading into the following week's trading sessions.

Sector Rotation Dynamics

Energy emerged as the week's standout performer, advancing nearly 3% as commodity prices responded to supply chain concerns and geopolitical tensions. The sector's strength was further bolstered by infrastructure spending provisions within the recently enacted tax legislation.

Information technology continued its outperformance trajectory, driven primarily by semiconductor companies. The artificial intelligence theme maintained its momentum, with related companies in utilities and industrials also benefiting from the sector's positive sentiment.

Industrial stocks demonstrated mixed performance, with aerospace and defense contractors rallying on increased government spending announcements, while transportation companies faced headwinds from trade uncertainty.

Financial services underperformed, declining nearly 2% as investors positioned defensively ahead of the upcoming earnings season. Payment processors faced particular pressure amid the growing prominence of cryptocurrency alternatives.

Consumer staples and communication services sectors lagged, with food companies experiencing pressure following disappointing earnings results and advertising agencies struggling with revised guidance expectations.

Individual Stock Movements

The Magnificent Seven technology stocks displayed varied performance patterns. NVIDIA achieved a historic milestone by becoming the first company to surpass a $4 trillion market capitalization, advancing 0.5% following CEO Jensen Huang's meeting with President Trump. The company's achievement underscored the ongoing artificial intelligence revolution's market impact.

Other technology leaders showed mixed results, with Alphabet, Amazon, and Tesla posting gains exceeding 1%, while Apple and Meta Platforms recorded modest declines. This divergence reflects the nuanced investor approach to evaluating individual company prospects within the broader technology ecosystem.

Cryptocurrency-related equities experienced significant rallies as Bitcoin reached new record highs. MicroStrategy led Nasdaq 100 gainers with a 3% advance, demonstrating the growing correlation between digital asset prices and related equity investments.

Defense and aerospace companies surged following Defense Secretary Pete Hegseth's announcement of expanded drone production initiatives. Red Cat Holdings jumped over 25%, while Kratos Defense & Security Solutions and AeroVironment gained more than 11% and 10%, respectively.

The airline sector experienced volatility, initially rallying on Delta Air Lines' positive guidance before retreating as trade concerns resurfaced. American Airlines Group fell over 5%, United Airlines Holdings declined more than 4%, and Alaska Air Group dropped over 3%.

Earnings Season Expectations

Market participants are preparing for a challenging earnings environment as the second quarter reporting season approaches. Bloomberg Intelligence projects S&P 500 earnings growth of just 2.8% year-over-year, representing the smallest increase in two years.

The earnings outlook reflects broader economic uncertainties, with only six of eleven S&P 500 sectors expected to post earnings increases. This represents the fewest sectors showing growth since the first quarter of 2023, according to Yardeni Research analysis.

Trade Policy Developments

Tariff Expansion and Implementation

President Trump's trade policy announcements dominated market attention throughout the week. The administration revealed plans to implement tariffs on over 20 countries, with rates varying significantly based on bilateral trade relationships and strategic considerations.

Canadian tariffs are set to increase to 35% from the current 25% level, though goods complying with the U.S.-Mexico-Canada Agreement will remain exempt. This targeted approach reflects the administration's nuanced strategy toward different trading relationships.

Brazil faces particularly steep tariff increases to 50%, reportedly linked to the country's legal proceedings against former President Jair Bolsonaro. This development illustrates how political considerations continue to influence trade policy decisions.

Most other trading partners will face tariffs ranging from 15% to 20%, representing a significant increase from previous levels. The administration has indicated these rates will take effect on August 1st unless bilateral agreements are reached beforehand.

Commodity-Specific Measures

The administration announced a 50% tariff on copper imports, including semi-finished goods, triggering immediate price reactions in commodity markets. U.S. copper futures experienced sharp gains, while international benchmark prices showed more muted responses.

Pharmaceutical companies face potential tariffs as high as 200% on imports unless they relocate production facilities to the United States within one year. This represents one of the most aggressive sectoral tariff proposals announced to date.

Negotiation Dynamics

Vietnam successfully negotiated a trade agreement imposing a 20% levy on imported goods, significantly below the initially proposed 46% rate. This development suggests flexibility within the administration's approach and the potential for diplomatic solutions.

The United Kingdom previously secured a trade agreement establishing 10% duties on exports to the United States. These precedents indicate that announced tariff rates serve as starting points for negotiations rather than final implementations.

The One Big Beautiful Bill Act: Fiscal Policy Implications

Tax Provisions and Extensions

The One Big Beautiful Bill Act, signed into law on July 4th, extends key provisions of the 2017 Tax Cuts and Jobs Act while introducing additional tax relief measures. The legislation provides deductions for tips, overtime pay, and Social Security benefits, subject to specific limitations.

The state and local tax deduction cap increases to $40,000, phasing out at income levels of $500,000 or higher. This provision addresses a significant concern for taxpayers in high-tax states while maintaining progressive limitations.

The reinstatement of 100% bonus depreciation for qualified property, stepping up from the 40% level in 2025, should provide meaningful benefits for corporations and small businesses. This provision, combined with deregulation initiatives, is expected to support economic growth acceleration in 2026 and 2027.

Fiscal Impact and Offset Measures

The Congressional Budget Office projects the tax cuts will reduce federal revenues by $4.5 trillion over the next decade. Spending reductions, including work requirements for Medicaid and nutrition assistance programs, plus the termination of renewable energy credit programs, total approximately $1.2 trillion.

The net fiscal impact represents a $3.3 trillion increase in government deficits over the next decade. This substantial fiscal expansion occurs against a backdrop of already elevated debt levels and ongoing concerns about long-term sustainability.

Economic Growth Implications

Much of the fiscal impact stems from extending current tax rates rather than introducing new reductions, potentially limiting incremental economic benefits. The tax relief primarily benefits higher-income households, who demonstrate lower propensities to spend additional income.

However, the bonus depreciation reinstatement and deregulation initiatives should provide meaningful support for business investment and growth. These measures, combined with the extended timeline for implementation, suggest economic benefits may be more pronounced in the medium term.

Federal Reserve Policy Considerations

Interest Rate Outlook

Federal funds futures markets assign only a 7% probability to a 25 basis point rate cut at the July 29-30 Federal Open Market Committee meeting. This reflects the Fed's cautious approach amid ongoing policy uncertainty and inflation concerns.

The FOMC minutes from the mid-June meeting revealed significant disagreement among policymakers regarding the appropriate policy direction. While most members anticipate rate cuts during 2025, some expressed openness to reductions as early as the July meeting, while others see no cuts throughout the year.

Inflation and Growth Concerns

The Federal Reserve faces challenging tradeoffs as tariff policies threaten to create stagflationary pressures. Higher import costs could elevate inflation while simultaneously dampening economic growth through reduced consumer purchasing power.

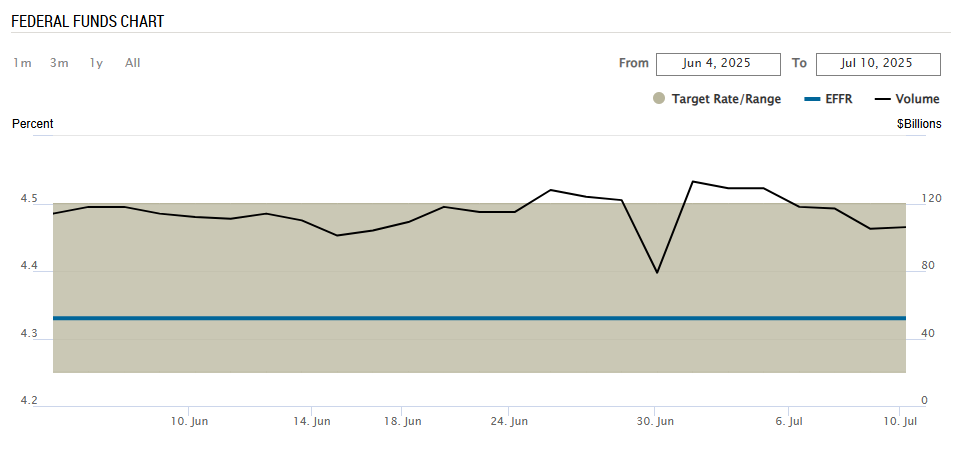

With the federal funds rate near 4.3% and personal consumption expenditure inflation at 2.3%, monetary policy maintains a restrictive stance. However, the central bank's ability to provide accommodation depends critically on inflation developments and labor market conditions.

Policy Communication and Market Expectations

Chicago Federal Reserve President Goolsbee emphasized the importance of concrete data regarding tariff impacts before making policy adjustments. This sentiment reflects the broader FOMC's preference for evidence-based decision-making amid significant policy uncertainty.

The central bank's communication strategy emphasizes patience and data dependence, suggesting rate cuts may resume in the fall once the economic impact of fiscal and trade policies becomes clearer. The resilient labor market provides the Fed with flexibility to maintain its cautious approach.

Fixed Income Markets

Treasury Market Dynamics

The 10-year Treasury yield rose 7 basis points to 4.419% as investors reassessed inflation risks and monetary policy expectations. September 10-year Treasury note futures declined 15 ticks, reflecting concerns about the inflationary impact of expanded tariff policies.

The Treasury curve experienced bear steepening, with 10-30 year yields rising approximately 10 basis points while 2-year yields remained relatively stable. This movement reflects investor concerns about long-term inflation expectations and fiscal sustainability.

European Government Bonds

European government bond yields moved higher in sympathy with U.S. Treasury movements. The 10-year German bund yield reached a 3.25-month high of 2.734% before ending the session up 2.0 basis points at 2.725%.

The 10-year UK gilt yield advanced 2.6 basis points to 4.622%, reflecting similar concerns about global inflation trends and monetary policy coordination challenges.

Corporate Credit Markets

U.S. investment-grade corporate bonds underperformed Treasuries, generating negative returns for the week. New issuance volumes exceeded expectations but were generally oversubscribed, indicating continued investor appetite for corporate credit.

High-yield bond markets tracked equity performance amid mixed sentiment. Light issuance followed several new deals priced at the week's beginning, suggesting measured corporate financing activity.

Bank loan markets remained active with opportunistic refinancing transactions dominating the primary calendar. This activity reflects companies' efforts to optimize capital structures ahead of potential rate changes.

International Markets

European Equity Performance

The Euro Stoxx 50 declined 1.01%, underperforming U.S. markets as European investors reacted negatively to trade policy developments. The region's export-dependent economy faces particular sensitivity to protectionist measures.

UK manufacturing production fell 1.0% month-over-month in May, significantly weaker than the expected 0.1% decline and representing the largest decrease in 10 months. This data point reinforces concerns about European economic momentum.

Asian Market Dynamics

China's Shanghai Composite reached a 9-month high despite minimal daily gains of 0.01%. This resilience occurred despite continued deflationary pressures, with producer price index falling 3.6% year-over-year, the largest decline in two years.

Japan's Nikkei Stock 225 fell to a 1-week low, declining 0.19% as investors evaluated the potential impact of U.S. tariff policies on the export-dependent economy.

Currency and Commodity Implications

The dollar's performance against major currencies reflects the complex interplay between U.S. economic strength and trade policy uncertainty. International investors must navigate both cyclical economic factors and structural policy changes.

Commodity markets experienced significant volatility, with copper futures leading gains on supply disruption concerns. The 50% tariff on copper imports created immediate price dislocations and supply chain adjustment pressures.

Cryptocurrency Market Surge

Bitcoin's Record Performance

Bitcoin surged above $118,000 during the week, representing an 8% gain from the previous week's closing price. This breakthrough marked the first significant breakout from the trading range established in May when the cryptocurrency reached its previous all-time high below $112,000.

The rally was supported by a steady stream of announcements from companies bridging traditional finance and decentralized finance sectors. The House of Representatives' designation of the week beginning July 14th as "Crypto Week" provided additional momentum.

Regulatory and Policy Developments

The House Committee on Ways and Means scheduled an oversight subcommittee hearing for July 16th titled "Making America the Crypto Capital of the World." This initiative suggests potential movement toward more favorable regulatory frameworks for digital assets.

The cryptocurrency market's total capitalization increased by approximately $60 billion to just under $3.7 trillion, according to CoinMarketCap data. This expansion reflects growing institutional and retail investor interest in digital assets.

Broader Market Implications

The cryptocurrency rally's correlation with equity markets, particularly technology stocks, demonstrates the increasing integration of digital assets into traditional investment portfolios. This trend has important implications for portfolio diversification and risk management strategies.

Cryptocurrency-related equities experienced significant outperformance, with companies like MicroStrategy leading major index gainers. This performance illustrates the growing investment theme connecting digital assets with traditional equity markets.

Business Sentiment

The National Federation of Independent Business Optimism Index came in slightly below expectations and declined from the previous month. Increased reports of excess inventories were the largest contributor to the decline.

Business sentiment surveys reflect the complex environment facing companies, with tax policy benefits offset by trade policy uncertainties. This mixed sentiment is likely to influence investment and hiring decisions.

Investment Strategy Implications

Asset Allocation Considerations

The current environment suggests maintaining diversified allocations while positioning for potential volatility. U.S. large-cap and mid-cap stocks remain attractive given domestic policy tailwinds and economic resilience.

International equity allocations should reflect the complex tradeoffs between valuation opportunities and policy uncertainties. Recent international outperformance may moderate as policy clarity emerges.

Fixed Income Positioning

Within fixed income allocations, extending duration in the seven to ten-year range may provide opportunities to lock in yields ahead of potential Federal Reserve easing. Credit spreads remain historically tight, suggesting caution in high-yield allocations.

International bond exposure faces challenges from lower yields and currency considerations. Investment-grade corporate bonds offer reasonable risk-adjusted returns despite recent underperformance.

Sector and Thematic Opportunities

Technology sector leadership appears sustainable given structural growth trends and policy support. Energy sector strength reflects both cyclical and policy-driven factors that may persist.

Defensive sectors may provide stability amid policy uncertainty, while infrastructure and defense themes benefit from increased government spending priorities.

Risk Management Considerations

Policy Uncertainty

The ongoing evolution of trade and fiscal policies creates significant uncertainty for market participants. Investors must balance the potential benefits of policy changes against implementation risks and unintended consequences.

The Federal Reserve's cautious approach to monetary policy reflects similar uncertainty about the economic impact of policy changes. This environment requires flexible positioning and active risk management.

Geopolitical Factors

Trade policy developments extend beyond purely economic considerations to encompass geopolitical relationships. The administration's approach to different countries reflects strategic priorities that may influence long-term investment themes.

Market participants must consider both immediate economic impacts and longer-term geopolitical implications when making investment decisions.

Market Volatility

Despite recent market resilience, the potential for increased volatility remains elevated given policy uncertainty and earnings season challenges. The MOVE index's recent decline to December lows may not persist given ongoing policy developments.

Options markets and volatility indicators suggest investor complacency may be premature given the range of potential outcomes from current policy debates.

Conclusion

Financial markets demonstrated remarkable resilience during a week dominated by trade policy developments and fiscal legislation. The modest declines in major equity indices masked significant underlying crosscurrents and sector rotation patterns.

The passage of the One Big Beautiful Bill Act provides meaningful fiscal stimulus while raising questions about long-term sustainability. The expansion of tariff policies creates both opportunities and challenges for different sectors and regions.

Federal Reserve policy remains data-dependent, with the central bank likely to maintain its cautious approach until the economic impact of policy changes becomes clearer. The resilient labor market provides flexibility for this patient approach.

Looking ahead, markets will likely continue to navigate the complex intersection of domestic policy changes, international trade relationships, and global economic conditions. The upcoming earnings season will provide important insights into how companies are managing this challenging environment.

Investors should maintain diversified portfolios while positioning for potential volatility and sector rotation opportunities. The current environment rewards active risk management and flexible positioning rather than static allocation strategies.

The cryptocurrency market's surge illustrates how policy changes can create new investment themes and opportunities. Similarly, the defense sector's strength demonstrates how government spending priorities can drive sector performance.

Ultimately, the week's developments reinforce the importance of understanding policy implications for investment decisions. Markets will continue to evolve as the administration's policy agenda unfolds and economic data provides clarity on the impact of these significant changes.

Weekly Benchmark Breakdown

S&P 500 Index

S&P 500 Index – A Pause in Progress

The S&P 500 ($SPX) closed the week at 6,259.75, down -0.33%, retreating slightly from its record high of 6,290.22. While price remains elevated near all-time highs, a closer inspection reveals a moderation in participation and a short-term cooling beneath the surface.

Breadth & Participation

Short-term momentum has clearly waned:

50.39% of stocks are above their 5-day average — down sharply from 79.52% last week

67.92% above the 20-day, also lower than last week’s 80.31%

Intermediate and longer-term metrics, however, remain firm:

50-day: 67.33%

100-day: 67.52%

150-day: 64.34%

200-day: 59.56%

Despite this week’s slight dip, the S&P is still supported by a structurally sound base. Participation remains broad on intermediate horizons, but short-term momentum has clearly reset.

New Highs vs. New Lows

This was the most notable deterioration in the data:

5-day net new highs: -87, with 61 highs vs. 148 lows

Longer timeframes also saw contraction:

1-month: -12

3-month: +16

6-month: +12

52-week: +6

This is the first time in several weeks we’ve seen new lows exceed new highs, even while price hovers near highs. This may indicate internal rotation, profit-taking, or reduced appetite for chasing breakouts.

Technical Context

The index remains elevated, consolidating just below a new high. The dip in short-term breadth and the shift in new highs/lows suggest a digestion phase rather than breakdown. Historically, this kind of internal reset within an uptrend often sets the stage for rotation or a refreshed move higher.

Verdict

This week’s pullback was minor in price, but more meaningful in internals. Short-term momentum has cooled and new lows are outpacing new highs, which is worth watching closely. That said, intermediate and long-term breadth remains robust, and price has not broken trend.

This is not a breakdown — it’s a pause. If internal participation stabilizes or rotates, the index remains positioned to continue higher. But for now, caution near the highs is warranted.

Dow Jones Index

The Dow Jones Industrial Average closed the week at 44,371.51, down -0.63%, slipping further from its recent 52-week high of 45,073.63. While the index still holds its uptrend on longer timeframes, this week revealed softening momentum and lackluster breadth beneath the surface.

Breadth & Participation

Short-term breadth is deteriorating:

50.00% of components are above the 5-day average

66.66% above the 20-day — unchanged from last week

50-day: also 66.66% — stable but unimpressive

Longer-term breadth is firmer:

100-day: 70.00%

150-day: 63.33%

200-day: 70.00%

The Dow is holding together structurally, but lacks momentum. The consistent 66–70% participation range shows a market that’s not breaking down but not breaking out either. It’s consolidating under the surface — directionless but intact.

New Highs vs. New Lows

This is where the Dow showed notable weakness:

5-day net new highs: -4, with 4 highs vs. 8 lows

Longer-term net highs remain flat to mildly positive:

1-month: +1

3-month: +3

6-month: +1

52-week: +1

This is the only major index this week with more new lows than highs on a 5-day basis. While the sample size is small (30 components), it’s a signal of rotation out of industrials and defensives — or simply a pause as other areas of the market lead.

Technical Context

The Dow remains in an uptrend, but it’s showing the least excitement. Price is well off the highs and internals aren’t providing a tailwind. It’s behaving like a late-cycle, defensive index — quietly consolidating while more growth-oriented segments drive the action.

Verdict

The Dow continues to lag. While long-term structure is healthy, short-term breadth has softened and new highs have dried up, reflecting sector rotation and a lack of leadership. There’s no breakdown here — but also no leadership. It’s the quiet laggard in an otherwise firm tape.

The Dow remains a rotational buffer rather than a driver. It’s not flashing warning signs, but it’s certainly not leading the charge.

NASDAQ 100 Index

The Nasdaq 100 ended the week at 22,780.60, down -0.21%, and roughly 1% below its recent all-time high. While price action remains orderly, the internals reveal growing fragility in short-term participation and a sharp deterioration in leadership breadth.

Breadth & Participation

Near-term breadth saw a sharp pullback:

5-day average: 43.56% (down from 79.2% last week)

20-day: 64.35%

50-day: 69.30%

Longer-term metrics remain strong:

100-day: 74.25%

150-day: 67.32%

200-day: 69.30%

The Nasdaq’s deeper breadth profile remains intact, but the steep drop in short-term participation signals rotation and caution. Many names have started to consolidate or decline despite index-level strength, indicating weakness beneath the surface.

New Highs vs. New Lows

Another red flag emerges in the highs vs. lows data:

5-day net new highs: -17, with just 20 highs vs. 37 lows

Longer-term differentials still lean bullish:

1-month: +4

3-month: +10

6-month: +7

52-week: +3

Despite the index remaining near highs, leadership breadth has narrowed sharply. In short, more stocks are slipping than breaking out.

Technical Context

The Nasdaq remains in a primary uptrend, but the rally is now being led by fewer names. This isn’t necessarily bearish in the short term — in fact, this kind of narrow leadership can last longer than expected — but it does weaken the foundation of the trend.

Verdict

Short-term fragility is building in the Nasdaq 100. The sudden drop in short-term breadth and negative net new highs are warnings that the rally is losing internal momentum even as price holds near highs. Leadership is narrowing — a classic sign of maturity in a move.

The Nasdaq is not breaking down — but it is thinning out. If this persists, broader weakness may follow. Keep an eye on whether internals stabilize or deteriorate further next week.

Russel 1000

The Russell 1000 closed the week at 342.67, down -0.40%, just shy of its all-time high of 344.63. However, while price has barely budged, internal metrics tell a radically different story — and it’s not bullish.

Breadth & Participation

Short-term participation has cratered:

5-day average: 48.61% (down sharply from 81.22% last week)

20-day: 68.37%

50-day: 70.35%

100-day: 70.45%

150-day: 63.43%

200-day: 58.89%

While intermediate and long-term moving average participation remains healthy, the near-term collapse in breadth signals a material change in tone. Sellers were active across a wide swath of names, despite the index holding close to highs.

New Highs vs. New Lows

This week’s breakdown in leadership is unmistakable:

5-day net new highs: -176, with 292 new lows vs. just 116 new highs.

Compare this to last week’s staggering +481 — this is a 657-point week-over-week reversal.

Longer-term differentials softened but remain net positive:

1-month: -16

3-month: +33

6-month: +24

52-week: +17

This is the most extreme deterioration in leadership breadth of any major index this week — and potentially the most important signal. The Russell 1000 represents the broad large-cap universe, and if it’s flashing warning signs, investors should take notice.

Technical Context

Structurally, the index remains within an uptrend, but that trend is being driven by a shrinking pool of names. This is a classic top-heavy dynamic, where the largest-weighted components mask deterioration in the broader universe.

Verdict

The Russell 1000 is undergoing a stealth correction under the hood. While the index price barely dipped, breadth collapsed and new lows surged — an unmistakable sign of distribution. This kind of divergence is a major yellow flag for the sustainability of the trend.

A market that is still near highs but hemorrhaging participation is one where rotation is breaking down, not rotating. The Russell 1000 breadth breakdown deserves full attention.

Major Indices Insights & Summary

After weeks of rising prices and broadening participation, this week delivered a stark shift beneath the surface. Despite relatively modest pullbacks in index prices, the breadth deterioration was severe across the board — particularly in the S&P 500 and Russell 1000. Momentum is stalling, and internal weakness suggests a short-term top may be forming.

S&P 500 – Structure Weakens, Momentum Cools

The S&P 500 ($SPX) closed at 6,259.75, pulling back -0.33% from last week’s close near all-time highs. While price action remains orderly, breadth deteriorated sharply:

5-day breadth dropped from 65.8% → 50.39%

Net new highs plunged to -87 (from +178 last week)

Longer-term participation still constructive: 67% of stocks remain above the 50- and 100-day moving averages

This isn’t a technical breakdown — yet. But leadership thinned materially, and sellers gained control in the lower half of the index. The sharp rise in new 5-day lows suggests distribution, not rotation.

Nasdaq 100 – Mega-Caps Mask the Fade

The Nasdaq 100 ($IUXX) declined modestly (-0.21%), closing at 22,780.60, but internals tell a more cautious story:

Only 43.56% of components are above their 5-day average (down from 79.2%)

Net new highs collapsed from +35 to -17

Longer-term moving average participation remains strong (69% above 200-day)

A handful of mega-cap names are keeping the index afloat. Beneath that, there is clear deterioration. The risk here is a sharp flush if the top 5–10 names stall or reverse.

Dow Jones – Flatlining Internals

The Dow Jones Industrial Average ($DOWI) dropped -0.63% on the week, closing at 44,371.51. Participation readings were oddly stagnant:

5-day average breadth sits exactly at 50%

Net new highs: -4

Long-term breadth still solid, with 70% of components above their 200-day average

The Dow has lost momentum. It’s not breaking down, but it isn’t providing leadership either. A flat signal in a fading tape isn’t encouraging — especially when its defensive sectors should be outperforming.

Russell 1000 – Massive Breakdown in Participation

Last week’s star performer became this week’s cautionary tale. The Russell 1000 ($IWB) fell just -0.40%, closing at 342.67, but:

5-day breadth plummeted from 81.2% → 48.61%

Net new highs cratered to -176, the worst of all indices

Longer-term averages remain strong, but the short-term collapse is too sharp to ignore

This was a stealth correction — price barely moved, but the internal damage was significant. A massive wave of selling hit broad large-cap names. If this persists, we risk a mechanical rotation failure.

Key Takeaways

Breadth deterioration across all four indices signals a coordinated pause or rollover in the uptrend

Net new highs collapsed, especially in the S&P and Russell 1000, which went from surging to negative territory in a single week

Longer-term structure remains intact, but the short-term action suggests the next directional move may be lower unless internals improve

Leadership is narrowing, with mega-caps doing most of the heavy lifting in the Nasdaq and S&P

VL Indices Market Score: 62 / 100 ( ↓21 WoW )

1. Breadth Breakdown ( -15 pts )

Sharp drops in 5-day and 20-day breadth across all indices:

S&P 500: 5-day breadth fell from 65.8% → 50.3%

Nasdaq 100: 79.2% → 43.6%

Russell 1000: 81.2% → 48.6%

Dow: 76.6% → 50.0%

This represents a major contraction in near-term momentum. The coordinated nature of the drop warrants a 15-point penalty.

2. Leadership Weakness ( -10 pts )

Net new highs vs. lows flipped negative across the board:

S&P 500: -87

Nasdaq 100: -17

Russell 1000: -176

Dow: -4

After multiple weeks of improvement, this reversal is a clear deterioration in leadership and bullish conviction.

3. Longer-Term Support Holds ( +5 pts )

Despite the short-term deterioration, longer-term metrics remain constructive:

Most indices still have >60% of stocks above the 100- and 200-day moving averages

Structural support has not yet broken

This provides a floor — for now.

4. Rotation Breakdown ( -5 pts )

No sector or index picked up the slack. This wasn’t rotation — it was across-the-board fading.

The Russell 1000’s internals were particularly alarming given its broader reach.

5. Macro & Valuation ( -5 pts )

Large-cap tech continues to dominate flows, and with yields rising and macro data mixed, the market remains vulnerable to external shocks. Breadth fading in a narrow market is a classic setup for volatility spikes.

Conclusion: Broad-Based Weakness Creeping In

This was not a technical breakdown week — but the data clearly flashed caution. Breadth weakness, narrowing leadership, and the absence of defensive rotation make this week’s action notably different. While uptrends remain structurally intact, the internals no longer confirm the highs.

The burden of proof has shifted back to the bulls.

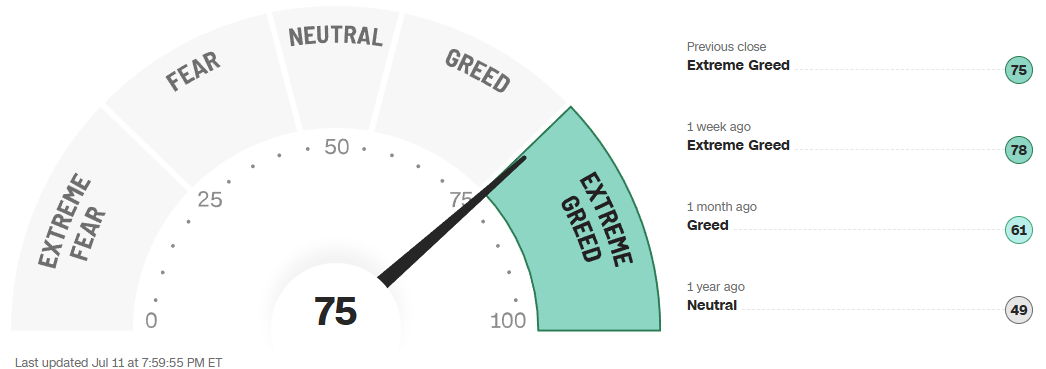

US Investor Sentiment Report

Insider Trading

Insider trading occurs when a company’s leaders or major shareholders trade stock based on non-public information. Tracking these trades can reveal insider expectations about the company’s future. For example, large purchases before an earnings report or drug trial results might indicate confidence in upcoming good news.

%Bull-Bear Spread

The %Bull-Bear Spread chart is a sentiment indicator that shows the difference between the percentage of bullish and bearish investors, often derived from surveys or sentiment data, such as the AAII (American Association of Individual Investors) sentiment survey. This spread tells investors about the prevailing mood in the market and can provide insights into market extremes and potential turning points.

Bullish or Bearish Sentiment:

When the spread is positive, it means more investors are bullish than bearish, indicating optimism about the market’s direction.

A negative spread indicates more bearish sentiment, meaning more investors expect the market to decline.

Contrarian Indicator:

The %Bull-Bear Spread is often used as a contrarian indicator. For example, extremely high levels of bullish sentiment might suggest that the market is overly optimistic and could be due for a correction.

Similarly, when bearish sentiment is extremely high, it might indicate that the market is overly pessimistic, and a rally could be on the horizon.

Market Extremes and Reversals:

Historically, extreme values of the spread (both positive and negative) can signal turning points in the market. A very high positive spread can signal market exuberance, while a very low or negative spread may indicate fear or capitulation.

NAAIM Exposure Index

The NAAIM Exposure Index (National Association of Active Investment Managers Exposure Index) measures the average exposure to U.S. equity markets as reported by its member firms. These are typically active money managers who provide their equity exposure levels weekly. The index offers insight into how much these managers are investing in equities at any given time, ranging from being fully short (-100%) to leveraged long (up to +200%).

CBOE Total Put/Call Ratio

CBOE's total put/call ratio includes index options and equity options. It's a popular indicator for market sentiment. A high put/call ratio suggests that the market is overly bearish and stocks might rebound. A low put/call ratio suggests that market exuberance could result in a sharp fall.

Equity vs Bond Volatility

The Merrill Lynch Option Volatility Estimate [MOVE] Index from BofAML and the CBOE Volatility Index [VIX] respectively represent market volatility of U.S. Treasury futures and the S&P 500 index. They typically move in tandem but when they diverge, an opportunity can emerge from one having to “catch-up” to the other.

CNN Fear & Greed Constituent Data Points & Composite Index

Social Media Favs

Analyzing social sentiment can provide valuable insights for investment strategies by offering a pulse on public perception, mood, and market sentiment that traditional financial indicators might not capture. Here’s how social sentiment analysis can enhance investment decisions:

Market Momentum: Positive or negative social sentiment can signal impending momentum shifts. When public opinion on a stock, sector, or asset class changes sharply, it can create buying or selling pressure, especially if that sentiment becomes widespread.

Early Detection of Trends: Social sentiment data can help investors spot trends before they show up in technical or fundamental data. For example, increased positive chatter around a particular company or sector might indicate growing interest or excitement, which could lead to price appreciation.

Gauge Retail Investor Impact: With the rise of retail investor platforms, collective sentiment on social media can lead to significant price movements (e.g., meme stocks). Understanding how retail investors view certain stocks can help in identifying high-volatility opportunities.

Event Reaction Monitoring: Social sentiment can provide real-time reactions to news events, product releases, or earnings reports. Investors can use this information to gauge market reaction quickly and adjust their strategies accordingly.

Complementing Quantitative Models: By adding a social sentiment layer to quantitative models, investors can enhance predictions. For example, a model that tracks historical price and volume data might perform even better when factoring in sentiment trends as a measure of market psychology.

Risk Management: Negative sentiment spikes can be a signal of potential downturns or increased volatility. By monitoring sentiment, investors might avoid or hedge against investments in companies experiencing a public relations crisis or facing negative perceptions.

Long-Term Sentiment Trends: Sustained sentiment trends, whether positive or negative, often mirror longer-term market cycles. Tracking sentiment trends over time can help identify shifts in investor psychology that could affect longer-term investments or sector rotations.

For these reasons, sentiment analysis, when combined with other tools, can provide a comprehensive view of both immediate market reactions and underlying investor attitudes, helping investors position themselves strategically across various time frames. Here are the most mentioned/discussed tickers on Reddit from some of the most active Subreddits for trading:

Institutional S/R Levels for Major Indices

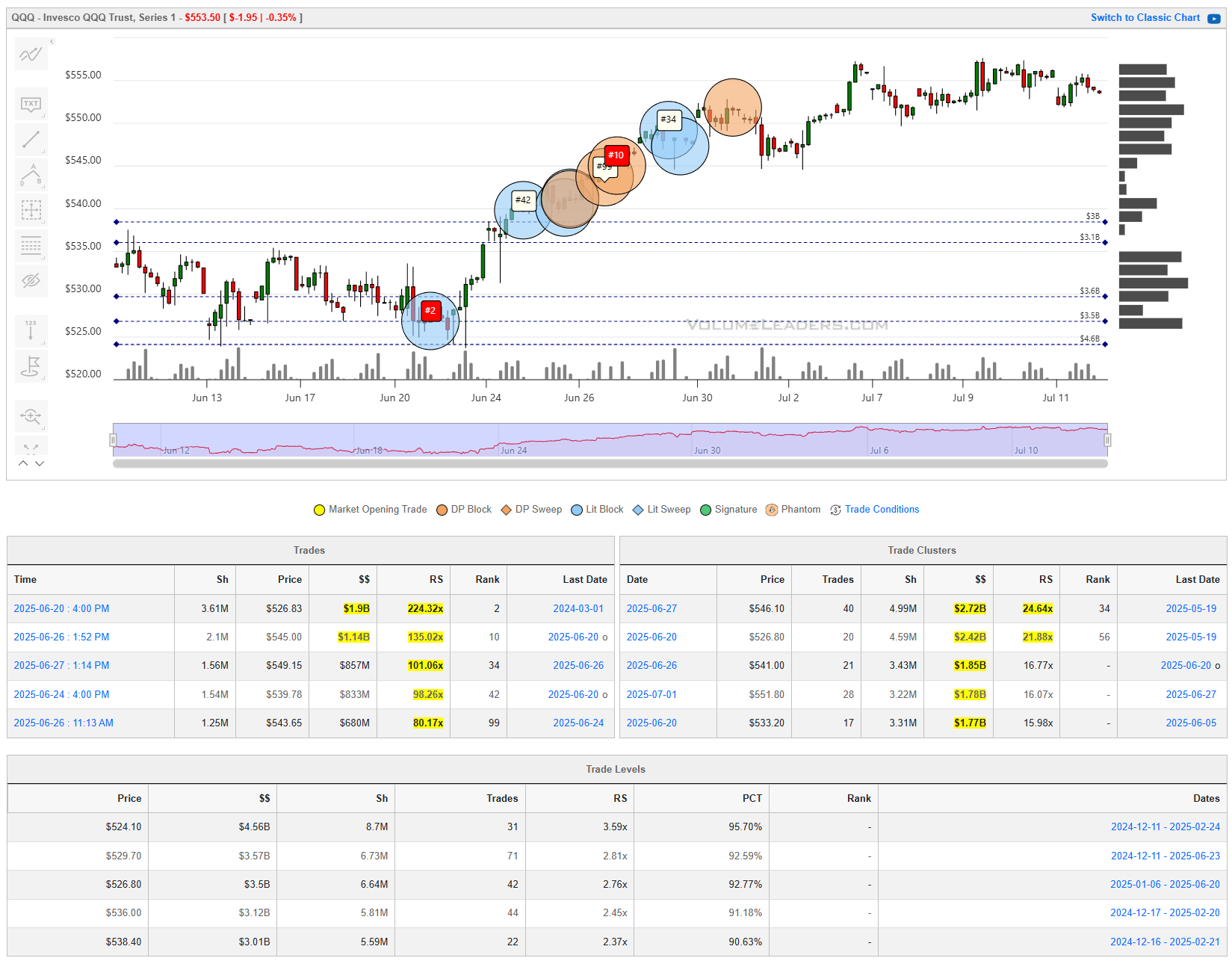

When you’re a large institutional player, your primary goal is to find liquidity - places to do a ton of business with the least amount of slippage possible. VolumeLeaders.com automatically identifies and visually plots the exact spots where institutions are doing business and where they are likely to return for more. It’s one of the primary reasons “support” and “resistance” concepts work and truly one of the reasons “price has memory” - take a look at the dashed lines in the images below that the platform plots for you automatically; these are the areas institutions constantly revisit to do more business.

Levels from the VolumeLeaders.com platform can help you formulate trades theses about:

Where to add or take profit

Where to de-risk or hedge

What strikes to target for options

Where to expect support or resistance

And this is just a small sample; there are countless ways to leverage this information into trades that express your views on the market. The platform covers thousands of tickers on multiple timeframes to accommodate all types of traders.

SPY

QQQ

IWM

DIA

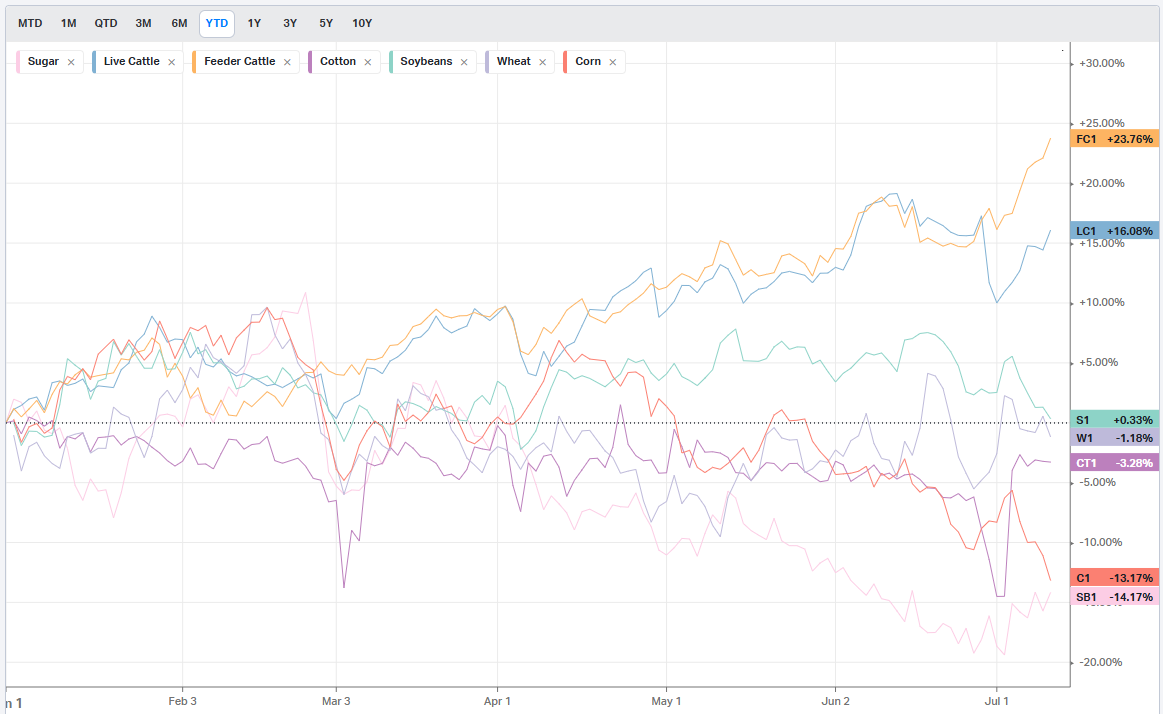

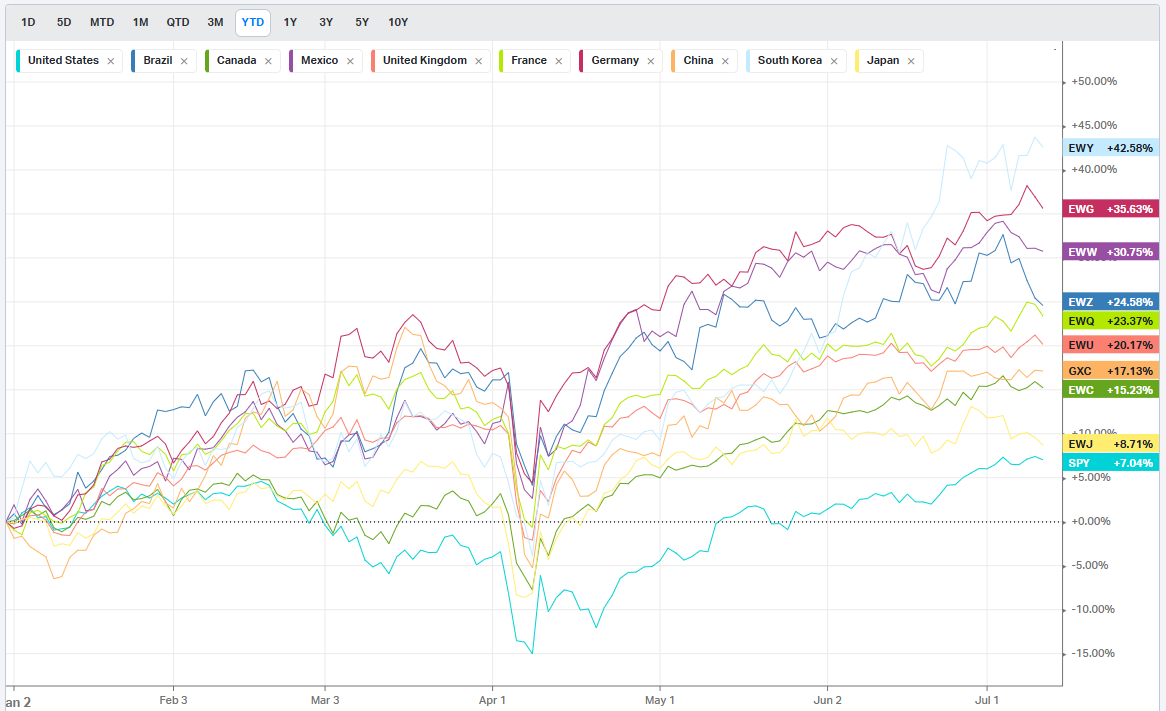

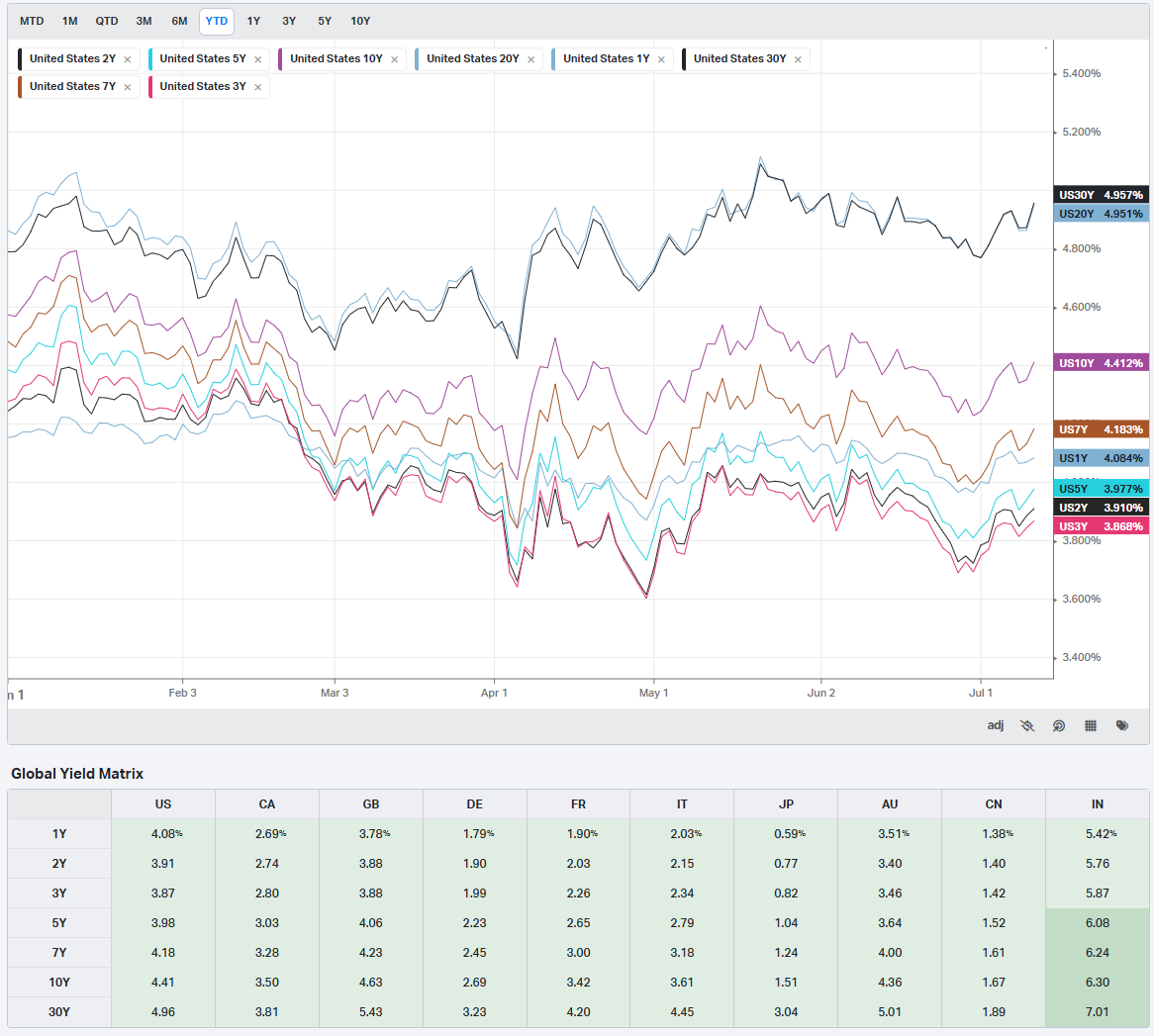

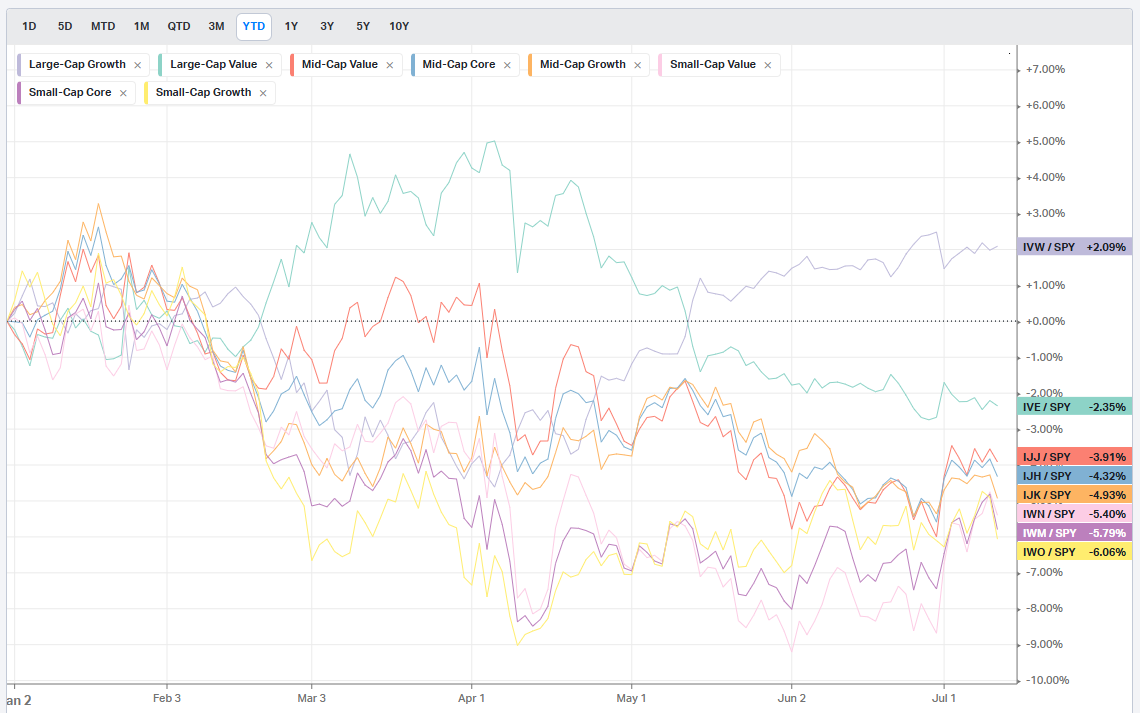

Summary Of Thematic Performance YTD

VolumeLeaders.com offers a robust set of pre-built thematic filters, allowing you to instantly explore specific market segments. These performance snapshots are provided purely for context and inspiration—think about zeroing in on the leaders and laggards within the strongest and weakest sectors, for example.

S&P By Sector

S&P By Industry

Commodities: Energy

Commodities: Metals

Commodities: Agriculture

Country ETFs

Currencies

Global Yields

Factors: Style

Factors: Size vs Value

Factors: Qualitative

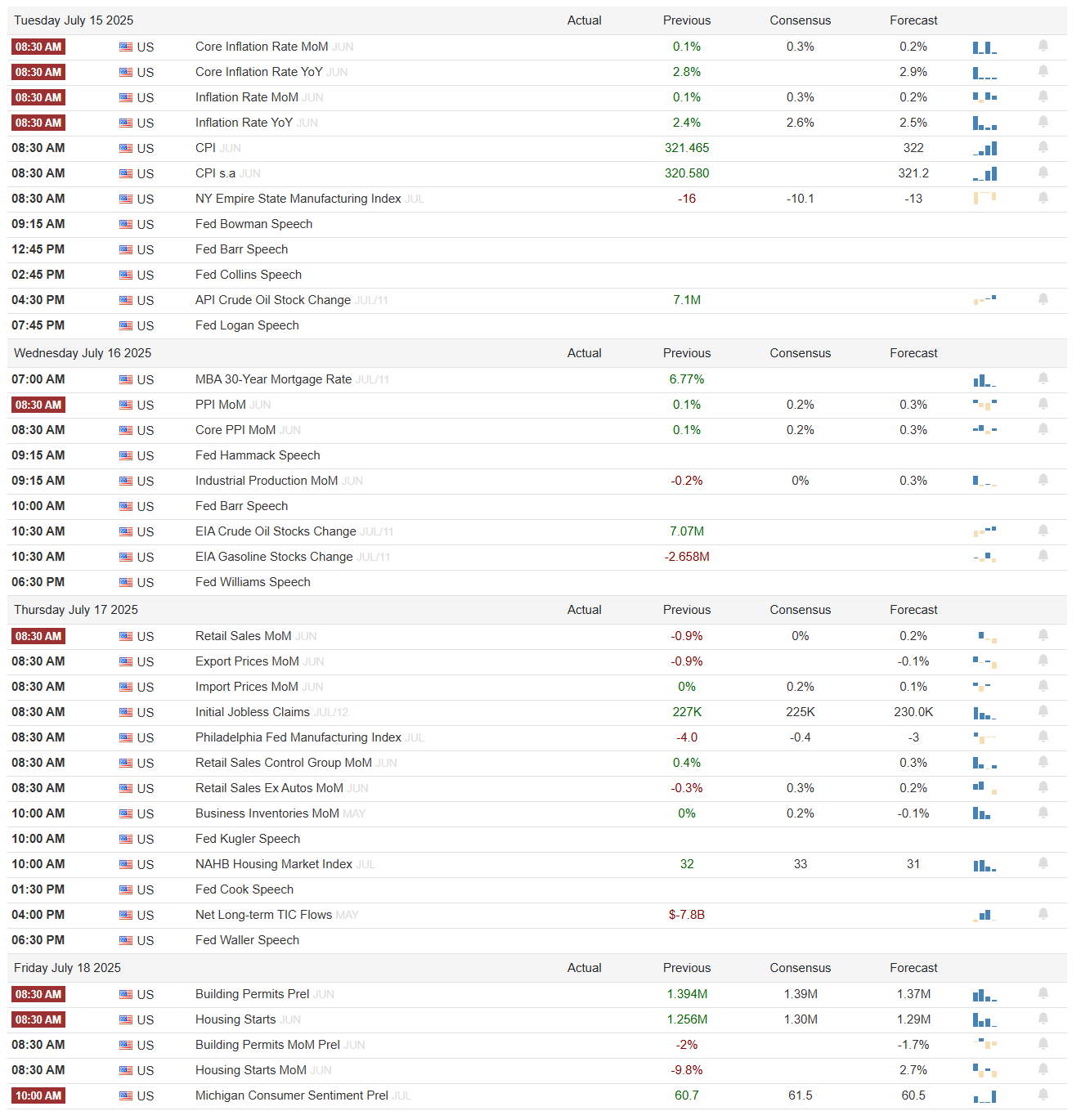

Events On Deck This Week

Here are key events happening this week that have the potential to cause outsized moves in the market or heightened short-term volatility.

Econ Events By Day of Week

Anticipated Earnings By Day of Week

Special Report

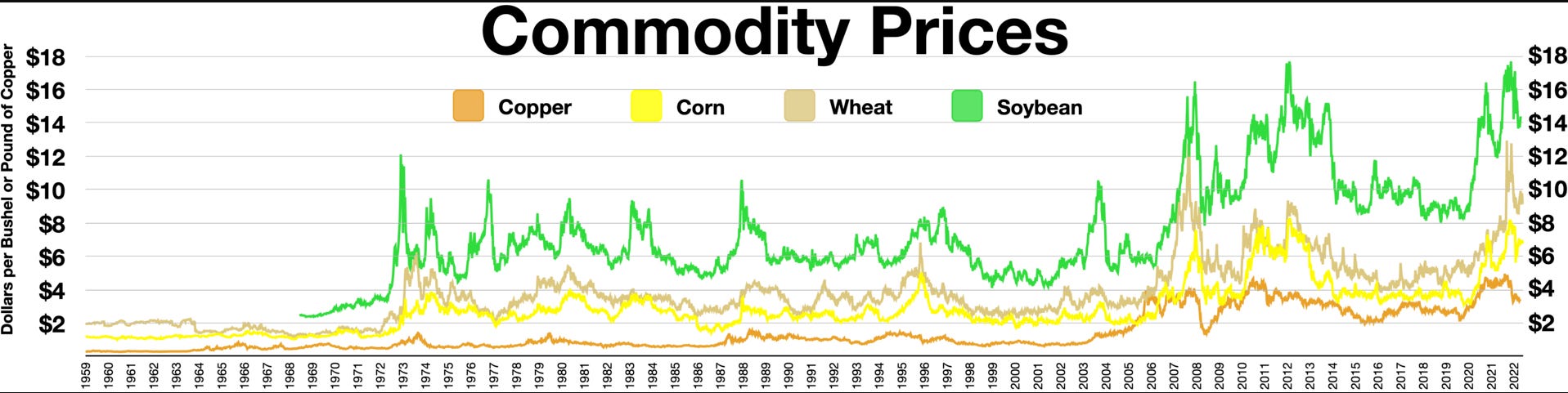

Copper: The Pulse of Progress

Copper, long known as a foundational metal of the industrial age, is once again at the center of global economic discussion. Often nicknamed "Dr. Copper" for its uncanny ability to forecast economic health, the reddish-brown metal is signaling deep shifts in both macroeconomic policy and structural demand. From the rollout of electric vehicles and grid modernization to geopolitical tariff battles and U.S. industrial capacity constraints, copper is more than just a raw material—it is a directional indicator of growth, bottlenecks, and capital flows.

In 2024 and into 2025, copper prices have been notably volatile. After a modest correction in late 2023 amid concerns about global growth, prices surged sharply in Q2 2025, driven by a combination of speculative positioning, fears of underinvestment in new production, and, most recently, the announcement of a new round of tariffs on Chinese copper products under the policy direction of former President Donald Trump. These tariffs, aimed ostensibly at reviving U.S. copper processing and shielding strategic supply chains, have had the opposite near-term effect: they constrained availability, created bottlenecks, and drove prices sharply higher as importers scrambled to secure alternative sources.

This report will walk through the contemporary state of copper markets, dive into the long arc of historical price analogs and economic cycles, and explore the structural factors shaping copper’s future—from mining and recycling, to smelting and trade policy. Along the way, we’ll also examine the importance of copper in the broader economic and market landscape, particularly how traders can use it as a signal for macro conditions, liquidity regimes, and sector rotation.

The central argument of this piece is simple: copper is no longer just a cyclical metal, but a strategic one. As the energy transition accelerates, geopolitical fractures deepen, and capital becomes more selective, copper’s role as both input and indicator grows more important.

Whether you're trading futures, evaluating ETFs, or building thematic equity baskets, understanding the state and trajectory of copper is indispensable.

Recent Price Activity and Market Drivers:

After trading in a $3.50 to $4.00/lb range for much of 2023, copper broke above $4.25 in early 2025.

The announcement of tariffs in April 2025 created a supply shock and led to a speculative rally; prices briefly touched $4.85/lb in June.

Chinese demand remains somewhat muted, but India and Southeast Asia are picking up the slack.

Supply chains have yet to meaningfully adjust to U.S. tariff policies, which many in the industry believe could be politically reversible after the 2026 midterms.

Copper Today – A Market in Motion

Copper is at a crossroads. The global economy, still adjusting to the post-pandemic reality, is undergoing a structural transformation. Decarbonization initiatives, generational shifts in industrial policy, and new fault lines in global trade have redefined the role of strategic commodities—and copper sits at the center.

In 2025, copper prices are reflecting more than traditional supply and demand. Market behavior suggests a metal that is increasingly financialized, used by institutional capital as both a macro hedge and a thematic expression of long-term global trends. Copper futures volumes have risen dramatically, driven in part by speculative flows anticipating supply constraints and electrification demand outpacing capacity.

Key Short-Term Catalysts:

Tariffs on Chinese Copper Imports: In April 2025, a renewed round of tariffs targeting Chinese copper products caused an immediate supply squeeze. U.S. consumers, already dependent on imports for semi-processed forms, saw a spike in prices as they scrambled for alternative sources.

Speculative Positioning: Managed money positioning reached multi-year highs in May, as hedge funds and commodity traders sought exposure to copper's bullish narrative. This speculative layer has contributed to outsized price moves, creating both opportunity and risk for short-term traders.

Global Demand Disparity: China, traditionally the largest consumer of copper, continues to underperform expectations amid a weak property market and industrial overcapacity. However, demand from India, Southeast Asia, and parts of Latin America is rising steadily, reshaping the demand curve.

Underlying Structural Tensions:

Investment Gaps in Production: Despite the price rally, few major mining projects have broken ground. The capital intensity, regulatory hurdles, and long timelines for mine development—often exceeding 7–10 years—have kept new supply constrained.

Energy Transition Acceleration: The metal-intensive nature of decarbonization technologies—especially wind, solar, and electric vehicles—means demand forecasts continue to rise. Utilities and infrastructure projects are increasingly sensitive to copper input costs.

Processing Bottlenecks: The U.S. maintains only two operational copper smelters, with limited capacity. In the face of new tariffs, this lack of domestic throughput is becoming a national strategic liability.

Market Signals to Watch:

Backwardation in copper futures curves may indicate acute short-term tightness.

ETF inflows into copper-related funds like CPER and COPX can act as sentiment gauges.

LME warehouse levels remain a proxy for global surplus or shortage; recent drawdowns suggest constrained supply.

Copper’s recent performance is not simply about today’s supply and demand—it reflects mounting anxiety about tomorrow’s readiness.

Historical Context and Analogues

Copper has always been a sensitive barometer of economic cycles. In periods of industrial expansion and infrastructure investment, copper prices tend to rise in anticipation of stronger demand. Conversely, recessions and monetary tightening cycles often usher in steep corrections. As traders look to assess today’s landscape, a closer look at historical analogues reveals recurring patterns and cautionary tales.

The last two major copper bull markets—the China-driven commodity supercycle of the 2000s and the post-COVID recovery rally—offer particularly relevant comparisons.

The Supercycle Peak (2002–2011): Driven by China’s explosive urbanization and infrastructure buildout, copper prices rose from below $0.75/lb in 2002 to a peak of over $4.60/lb in 2011. Massive stimulus packages and fixed asset investment in roads, bridges, power grids, and housing drove sustained demand. Traders who identified the early signs of this regime shift captured enormous gains, both in copper futures and mining equities.

However, the rally eventually gave way to overcapacity, speculation, and a China-led slowdown. Prices declined steadily for nearly five years, illustrating the perils of extrapolating linear growth from one-off investment booms.

Post-COVID Recovery (2020–2022): Following the economic disruption of COVID-19, copper prices surged once again—this time propelled by synchronized global stimulus, a rebound in industrial activity, and a renewed push for energy transition. The narrative shifted toward "green demand"—EVs, solar farms, and grid expansion—all of which require significant copper input.

By mid-2022, however, inflation concerns and central bank tightening punctured the rally. Prices corrected sharply from over $4.80/lb to under $3.50/lb in less than a year. The episode reinforced copper’s vulnerability to liquidity conditions, even amid favorable long-term fundamentals.

Analog Signals for 2025 and Beyond:

Today’s price behavior mirrors the early stages of past supercycles: supply is tight, demand is shifting, and policy is uncertain.

However, speculative froth is building more quickly than in past cycles, aided by financialization and ETF accessibility.

Traders should be alert to the difference between structural narratives (e.g. decarbonization) and cyclical reality (e.g. global manufacturing weakness).

The historical record is clear: copper leads, but it can also mislead. Price trends must be evaluated in tandem with inventory data, credit cycles, and fiscal policy. As we continue, we’ll explore the metal’s underlying role in industry and why the world simply can’t function without it.

Copper’s Industrial Importance

Copper is fundamental to the modern world. Its conductivity, malleability, and durability make it irreplaceable across sectors as diverse as construction, electronics, energy, and transportation. But its true industrial importance lies in the fact that copper is not just a component—it’s infrastructure.

In electrical applications, copper is king. It transmits power more efficiently than any other affordable metal, and is the default choice for wiring, motors, transformers, and power transmission lines. The average home contains more than 400 pounds of copper; electric vehicles use more than twice the copper of internal combustion cars; and utility-scale solar or wind farms depend on copper-heavy substations and interconnects.

Its industrial footprint is massive:

Power generation and transmission

Construction (plumbing, wiring, HVAC)

Electronics and semiconductors

Automotive (especially EVs)

Telecom infrastructure (5G, broadband)

Copper is also widely recycled, with nearly one-third of global copper demand met via secondary supply. But even recycling has limitations. The infrastructure required to melt and repurpose scrap is energy-intensive, and the scrap stream itself can’t grow faster than the products being retired. Meanwhile, substitution options—such as aluminum—often require tradeoffs in efficiency, weight, or cost.

Resources for embedding:

Supply Chain, Mining, and Recycling

The copper supply chain begins at the mine face. From there, copper ore undergoes crushing, grinding, flotation, and finally smelting and refining before reaching the form required for industrial applications.

The world’s largest copper producers include Chile, Peru, the Democratic Republic of Congo, and China. Chile alone accounts for nearly a quarter of global mined copper, but its output has stagnated due to water shortages, labor strikes, and regulatory challenges. Peru has experienced similar disruptions due to political unrest.

In the U.S., production is modest. Arizona leads domestic output, but many deposits remain undeveloped due to permitting challenges and ESG opposition. While some new exploration projects are underway, large-scale production can take 7–10 years to bring online, even with accelerated timelines.

Compounding the challenge is refining capacity. The U.S. currently has only two operational copper smelters—one in Utah and one in Arizona. Most concentrate is exported, then re-imported as semi-finished or refined copper. With new tariffs in place, this dependency has become a chokepoint.

Recycling is a growing contributor. Copper is one of the few materials that can be recycled indefinitely without loss of performance. But scrap flows are limited by product life cycles, and rising demand means primary supply will remain essential for decades.

U.S. Industrial Bottlenecks and Processing Constraints

The U.S. finds itself strategically vulnerable when it comes to copper processing. With just two aging smelters and a regulatory environment hostile to new industrial development, the country imports more than half of its refined copper needs. Tariffs may be designed to stimulate domestic industry, but in practice they often shift cost burdens without unlocking capacity.

President Trump’s April 2025 tariffs on Chinese copper semi-finished goods and refined cathodes were designed to penalize Chinese overcapacity and support American processors. But because the U.S. lacks the infrastructure to absorb redirected flows, the effect was a bottleneck—not a boom.

Industry experts estimate it could take a decade or more to build a new smelting facility in the U.S., at a cost exceeding $3 billion. With environmental permitting timelines uncertain and long-term policy unclear, few firms are willing to take the risk.

Thus, U.S. copper consumers—utilities, automakers, industrial firms—face a conundrum: rising prices, tight supply, and no domestic cushion. Traders must now factor in not just the market’s response to macro conditions, but the structural inability of U.S. industry to pivot quickly.

Copper as an Economic Bellwether

Copper’s moniker as "Dr. Copper" is well earned. It has long served as a real-time proxy for global growth expectations, particularly in manufacturing-heavy economies. Its broad industrial usage makes it responsive to economic inflection points, from stimulus booms to liquidity crunches.

Correlations are strong:

Copper prices often lead global PMI changes.

They mirror shifts in credit growth, especially in China.

They tend to fall ahead of recessions and rise in recovery phases.

Importantly, copper can act as both signal and noise. Traders should pair copper’s signals with confirming data—ISM prints, rates markets, dollar strength, and commodity curves. When copper and equities diverge, it often precedes turning points. As we look toward the future, copper's role in decoding macro conditions will remain critical.

How to Trade Copper

Copper offers multiple vehicles for traders:

Futures: COMEX (HG) contracts are the most liquid. Traders must manage roll schedules and margin requirements.

ETFs: CPER and JJC track futures prices. COPX holds copper miners.

Equities: Large-cap miners (FCX, SCCO), equipment providers (CAT), and renewable infrastructure names are indirect plays.

Options and Spreads: Options on HG futures allow for directional, volatility, and calendar strategies.

Copper tends to exhibit seasonality, with stronger demand in the first half of the year and lower activity in Q4. Liquidity is global, with substantial flow from Asia and London. LME and SHFE activity can precede U.S. moves.

The Outlook – Bullish, Bearish, or Balanced?

Short-term, the copper market is being driven by trade policy volatility and speculative buildup. Tariff-induced bottlenecks, LME inventory draws, and fund flows suggest elevated risk of further upside—but also rising crash risk if positioning reverses.

Mid-term, demand from renewables, EVs, and grid expansion continues to build. But progress will be non-linear. The global economy remains fragile, and inflation concerns could prompt tighter policy.

Long-term, the copper story is fundamentally bullish. Without breakthrough alternatives, copper will remain the backbone of electrification and modern infrastructure. But supply discipline, ESG pressures, and trade fragmentation will define the pace and volatility of this cycle.

Watchpoints:

Will new mining projects be approved and financed?

Can the U.S. improve its smelting base?

Will China’s growth stabilize or slip further?

Takeaways for Traders and Investors

Copper is no longer a passive macro indicator. It’s an active, central node in a web of economic, environmental, and geopolitical forces. Traders and investors alike should:

Track copper futures curves and LME inventories weekly.

Monitor tariff developments and U.S. infrastructure policy.

Use copper as a cross-check on equity rallies or corrections.

Diversify exposure across copper futures, ETFs, and equities to reflect differing time horizons.

For active traders, copper provides volatility and edge. For long-term allocators, it offers exposure to a secular growth theme. For policymakers, it represents a test of industrial resilience. And for everyone else—it may just be the most important metal you’re not watching closely enough.

Market Intelligence Report

After a strange lull heading into the long holiday weekend—with July 3rd marking one of the lowest institutional dollar volume days of the year at just $81.9 billion—markets returned this week with noticeably restored participation, though not without signs of caution.

Dollar flow rebounded sharply to kick off the week, surging to $126.3B on Monday and holding a solid average of $122B over the five-day stretch. But while the aggregate may suggest a broad return of activity, the internals reveal something more nuanced: a market rotating, reallocating, and quietly repositioning around both macro uncertainty and micro conviction.

ETF Flows: Sector Sensitivity Returns

Institutional activity in ETFs was focused, even if not explosive. Large Cap and Bond exposures again dominated, with $12.9B and $6.9B respectively on Monday alone. Bond demand gradually cooled as the week wore on, dropping to $5.3B by Friday, but on a relative basis held up far better than large caps suggesting institutions aren’t rotating aggressively out of defensive posturing despite recent equity rallies.

This could reflect lingering concerns around interest rate sensitivity or a strategic desire to balance exposure ahead of potential macro catalysts like inflation data or earnings season kickoff. Small caps held their own in a show of some market optimism.

Equity Sector Flows: Conviction in Select Cyclicals

Equity sector flows told a story of strategic rotation. Technology remained in the lead, with $30B+ in flows early in the week and a still-healthy $27B on Friday. But the standout narrative came from the Consumer Discretionary and Industrials sectors.

Consumer Discretionary saw $11B on Monday and maintained strength through the week—likely driven in part by Tesla's recovery and ongoing positioning in travel, auto, and apparel plays that may benefit from a late-summer demand push.

Industrials saw renewed interest midweek, possibly reflecting positioning ahead of infrastructure earnings and positive outlooks from key transport/logistics names. There was also a sharp Wednesday uptick in Healthcare and Financials, with $12B and $10B respectively—perhaps tied to rate expectations following recent dovish commentary from Fed officials.

Dark Pools vs Sweeps: Different Stories, Same Leaders

In the dark pool view, mega cap tech and consumer names dominated the aggregate dollar bars. NVDA, GOOGL, TSLA, AAPL, and META all featured prominently, signaling continued high-touch interest in names with liquidity and options overlays. The scatter view added important nuance—showing GOOG and META receiving high-dollar trades despite lower volume footprints, indicating larger, more deliberate block-style buying.

In the sweeps-only universe, the message diverged: PLTR, NVDA, and TSLA led in dollars and volume, with sweeps concentrated in fast-moving names that have become retail and institutional battlegrounds alike. VISA and INTC also stood out, the former likely reacting to cross-border travel demand data and the latter seeing speculation ahead of Q2 chip supply updates.

What It All Suggests

The takeaway this week is one of measured re-engagement. There’s no panic-buying and no one-way flows, but institutional players are clearly tilting into selective growth, notably in Tech, Consumer Discretionary, and Industrials. Defensive allocations remain, especially in bonds and stable sectors like Healthcare, suggesting a hedge against volatility or unexpected macro shifts.

Add to this the ongoing anticipation around Q2 earnings season, Fed commentary, and geopolitical noise (including fresh trade restrictions and soft inflation figures), and it becomes clear: this is a market in strategic motion, not reckless pursuit.

For traders and allocators alike, the edges aren’t found in chasing heat—they’re found in observing who’s rotating, what sectors are quietly absorbing liquidity, and where the fast money and big money overlap or diverge. Let’s take a look at some individual names that are already on the move and under everyone’s radar.

Individual Names with Institutional Interest

Trade Rank Velocity (TRV)

TRV is a proprietary metrics that measures the recent acceleration or deceleration in institutional trading activity for a given stock by comparing its average trade rank over the past few days to its average in recent weeks. A sharp improvement in TRV typically reflects a notable shift in positioning, often accompanied by sustained trade activity, suggesting institutions are actively engaging with the name and that intensity of activity is rising. This often precludes meaningful price or narrative shifts. Traders should use VL’s charting tools to investigate the nature of the trades—price, size, and context—before making any decisions.

Emergent Themes from the TRV Watchlist

Micro/Mid-Cap Speculation & Special Situations

Names like FULC, AEVA, STRL, HNST, TMC, UUUU, MP, IDMO, SLDP, HCKT, IREN, ANGIE, AAPU and others suggest institutional interest in under-the-radar or distressed innovation plays, many of which trade thinly and fly below traditional screeners. These often surge ahead of earnings, regulatory catalysts, or M&A chatter.

Alternative Energy, Rare Earths, and Materials

There’s meaningful representation in: MP, UUUU, TMC, SVM, IREN, SLDP – Clean energy, lithium, uranium, and rare earth players. These are especially relevant given this week’s continued commentary around strategic resource security and EV supply chains, particularly with U.S.–China tensions and tariff-related news.

Crypto-Adjacent or Blockchain Exposure

BITW, BITQ, GLXY, ETHE, USXF, VTEI

Reflects a possible second-leg build in crypto allocations following recent ETF approvals and BTC’s defensive posture. Many of these saw flows despite Bitcoin’s flat week, which may hint at rotation or dip accumulation by institutional allocators.

AI & Emerging Tech

PATH, NVTS, ANGIE, AEVA, LFST, FRHC, APIE

These are names on the periphery of the AI/automation narrative, especially in robotics, chip supply chains, and digital services. While they’re not megacap names like NVDA or SMCI, they often move in sympathy or as "second-tier" beneficiaries.

Financial Services & Niche Lending

ENVA, BKSKY, OPFI, OPRT, FRHC, PLMR

A cluster of alt-lenders, fintechs, and regional players shows up here. This could indicate positioning around credit normalization, small business loan demand, or easing rate expectations.

Consumer Discretionary / Retail Repricing

BRO, MSGS, FWRG, TDUP, PNTG, FUN, GWW, NGVC

There's scattered presence of low-float consumer plays, retail operators, and entertainment companies. This may tie into theme park attendance rebounds, Q3 spending seasonality, or bets on consumer resilience post-CPI.

SPAC Legacy / Illiquids

Names like HIMS, OLO, KIND, HNST, TDUP, VCRB, WE fall into what could be described as post-SPAC or heavily repriced growth. Institutions may be sifting through this wreckage for value re-emergence or technical bottoming.

Institutional Outliers (IO)

Institutional Outliers is a proprietary metric designed to spotlight trades that significantly exceed a stock’s recent institutional activity—specifically in terms of dollar volume. By comparing current trade size against each security's recent normalized history, the metric flags outlier events that may indicate sudden institutional interest but may be missed because the activity doesn’t raise any flags/alerts when comparing the activity against the ticker’s entire history. For example, it’s conceivable that a ticker today receives the largest trade it has had in the last 6 months but the trade is unranked and would therefore be missed by current alerts built off Trade Ranks.

Emergent Themes from the Institutional Outliers Watchlist

Global Rotation: International Equities

Top of the list: BBCA (Canada), VWOB (Emerging Market Bonds), BBEU (Europe), and EFAV (Foreign Large Blend) all show extreme dollar flows. This suggests a significant institutional reallocation for international assets—a continuation of the rotation out of crowded U.S. megacaps and into overlooked global exposures or is it time for money to come home? Contextually, this aligns with a rising dollar retracement this week and speculation around diversification away from U.S. rate risk. These names are some of the sleepier ones on the list judging only by realized vol but continue to monitor for a shift in this huge investors thematic of 2025

Risk-On Crypto Tilt

GBTC, BITO, IBIT, and FBTC all appear in the top ranks. While none posted enormous volatility or price changes, their presence here implies bigger dollar bets, not just retail froth. Institutions may be positioning into ETF-wrapped crypto exposure as regulatory headwinds ease (following July 10's positive SEC guidance on staking clarity).

Biotech & Speculative Healthcare Surge

High sigma trades in SMLR, DVAX, RNA, HR, RARE, QGEN, NVS indicate targeted interest in small- and mid-cap biotech/healthcare names. Notably, UMAC, a SPAC recently rumored to be involved in a genomics deal, shows the highest realized vol (1.49), hinting at speculative positioning. This risk-on shift into clinical trial or acquisition candidates suggests confidence in FDA calendars or M&A activity. Size carefully when playing names with higher realized vol…

Consumer Discretionary

LI (EV), MOD, NIO, MBLY, MODG all register large flow outliers. This cluster suggests institutional interest in consumer cyclicals tied to autos and durable goods—perhaps driven by China’s July 9 rate cut and improving global consumer sentiment or perhaps someone had an inside line on Trump’s surprise weekend announcements with some of the US’ largest trading partners

Real Estate Rebound?

ADC, HR, and LXP all make the outlier list. While not the highest sigma prints, this group shows elevated flows in an otherwise quiet REIT sector, possibly reacting to falling treasury yields or macro soft-landing hopes.

Industrials, Materials, and Commodities

AAON, PAC, OR, GBX, MEOH, MODG, and AAAU all appear. These span across industrial equipment, precious metals, and chemicals, hinting at a thematic move into hard assets—perhaps a hedge against inflation stickiness or in response to infrastructure spending headlines (e.g. the new July 8 bipartisan bill passed in the Senate).

Summary

This week’s outlier basket reflects a interesting participation beyond the tech/AI darling trade. Institutions appear to be:

Rotating globally,

Positioning for risk, especially in crypto and speculative healthcare, and

Sifting through underweighted cyclical sectors like industrials and real estate for value.

Thank you for being part of our community and for dedicating your time to this edition. Your insights and engagement drive everything we do, and we’re honored to share this space with such committed, thoughtful readers. Here’s to a week filled with clear opportunities and strong performance. Wishing you many bags 💰💰💰

—Volumeleaders