Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 24 / What to expect Dec 09, 2024 thru Dec 13, 2024

In This Issue

Market-On-Close: All of last week’s market-moving news and macro context in under 5 minutes + futures-snapshots

Special Coverage: Bitcoin: Breakout or Bubble?

The Latest Investor Sentiment Readings

Institutional Support & Resistance Levels For Major Indices: Exactly where to look for a turn in markets this week in SPY, QQQ, IWM & DIA

Institutional Activity By Sector: Institutional flow by sector including the top names institutionally-backed names in those sectors

Top Institutional Orderflow In Individual Names: All of the largest sweeps and trade blocks on lit exchanges and dark pools

Investments In Focus: Bull vs Bear arguments for FDX, LULU, TGT, ALT, FIS, TSM, GFS

Top Institutionally-Backed Gainers & Losers: An explosive watchlist for day traders seeking high-volatility

Normalized Performance By Thematics YTD (Sector, Industry, Factor, Energy, Metals, Currencies, and more): which corners of the markets are beating benchmarks, which ones are overlooked and which ones are over-crowded

Key Econ Events and Earnings On-Deck For This Week

Market-On-Close

As the year concludes and the holiday season envelops us, investors find much to celebrate. The financial markets have climbed to unprecedented heights, with record-breaking stock performances and favorable bond yields reflecting a buoyant economic landscape. Underpinning this strength is a U.S. economy that continues to grow at or above trend, defying predictions of recession.

This resilience has been a hallmark of 2024, supported by a robust labor market, strong consumer spending, and sector-specific expansions. However, looming challenges—from policy shifts to global uncertainties—pose significant hurdles. Let’s take a brief look into the economic and market dynamics of the past year, highlighting key drivers of growth, areas of concern, and potential paths forward for 2025.

Consumer Spending: The Bedrock of Growth

The U.S. economy, with consumer spending accounting for approximately 70% of GDP, has proven its resilience despite challenges such as elevated inflation and higher interest rates. A significant dichotomy has emerged within consumer behavior, with middle- and upper-income groups maintaining robust spending due to wealth effects from higher stock market valuations and stable real estate prices.

Real wage gains across households have further supported consumer confidence. Wage growth has consistently outpaced inflation, a trend expected to persist into 2025 as inflation moderates to the 2%-3% range. These dynamics have particularly bolstered service-oriented sectors, including leisure, hospitality, and dining, which have seen strong demand. The consumer's resilience remains a cornerstone of economic stability, providing a vital buffer against external shocks.

The Labor Market: A Pillar of Strength

Employment trends in 2024 showcased a labor market adjusting to post-pandemic normalization. November's addition of 227,000 new jobs surpassed expectations, underscoring a rebound from October's weather-impacted figures. The average monthly job creation of 180,000, while below 2023 levels, remains above historical norms.

The unemployment rate, ticking slightly higher to 4.2%, reflects a balancing act rather than underlying weakness. Broader labor market metrics, including wage growth and job openings, point to sustained strength. Employment in manufacturing, healthcare, and leisure sectors has been particularly robust, with manufacturing showing signs of recovery from earlier contractions.

As interest rates trend downward and corporate earnings improve, the labor market is positioned for potential reacceleration in late 2025. Pro-growth policies could further drive hiring, contributing to economic momentum.

Sectoral Dynamics: Services Lead, Manufacturing Stabilizes

The services sector, constituting 70% of U.S. GDP, has been the economy's mainstay in 2024. Financial services, transportation, and leisure industries have exhibited steady growth, supported by resilient consumer demand. The ISM services index consistently signaled expansion, reflecting the sector's vitality.

Manufacturing, on the other hand, faced headwinds for much of the year, grappling with supply chain disruptions and global uncertainties. However, recent ISM data indicates a potential turnaround, with new orders for both services and manufacturing showing expansion. If sustained, this trend could herald broader industrial stabilization, complementing the strength of the services sector.

Navigating the Challenges: New “Walls of Worry”

Despite the rosy backdrop, 2025 presents its own set of challenges. Policy uncertainties, particularly under a new White House administration, could impact trade, tariffs, and immigration. Escalations in trade tensions could weigh on consumer confidence and inflation, introducing volatility into otherwise stable markets. However, the likelihood of extreme policy measures appears low, with potential disruptions expected to be contained.

Federal Reserve policy represents another critical variable. While rate cuts are anticipated, robust economic growth or re-emergent inflation could lead to a more cautious approach from the Fed, potentially tempering market enthusiasm. Nonetheless, the prevailing trajectory suggests lower rates, supportive of consumer spending and corporate investments.

Market Strategies: Turning Volatility into Opportunity

Increased uncertainty should not dissuade investors but instead serve as an opportunity to reassess portfolios. Pullbacks in markets can provide strategic entry points, particularly given the underlying strength of the economy. Diversification remains a key theme, with a balanced allocation across large- and mid-cap stocks and a mix of growth and value sectors.

The bond market also offers opportunities. While short-duration bonds and cash-like instruments have provided stability, a gradual shift toward intermediate maturity bonds could lock-in attractive yields amidst a declining rate environment. Strategic allocation between equities and bonds can help investors navigate the complexities of 2025.

Conclusion: Poised for a Soft Landing

The U.S. economy's performance in 2024 has been nothing short of remarkable. With resilient consumer spending, a robust labor market, and sectoral strength, it stands poised to achieve the elusive "soft landing"—a modest slowdown without tipping into recession. While challenges loom, from policy shifts to market volatility, the fundamental backdrop remains favorable.

As we transition into 2025, the focus should be on maintaining diversification, capitalizing on market opportunities, and navigating uncertainties with strategic foresight. With the U.S. economy on firm footing and no downturn in sight, the coming year offers a landscape ripe for growth and investment. Investors, armed with insights and a long-term perspective, can look forward to navigating this promising yet complex terrain.

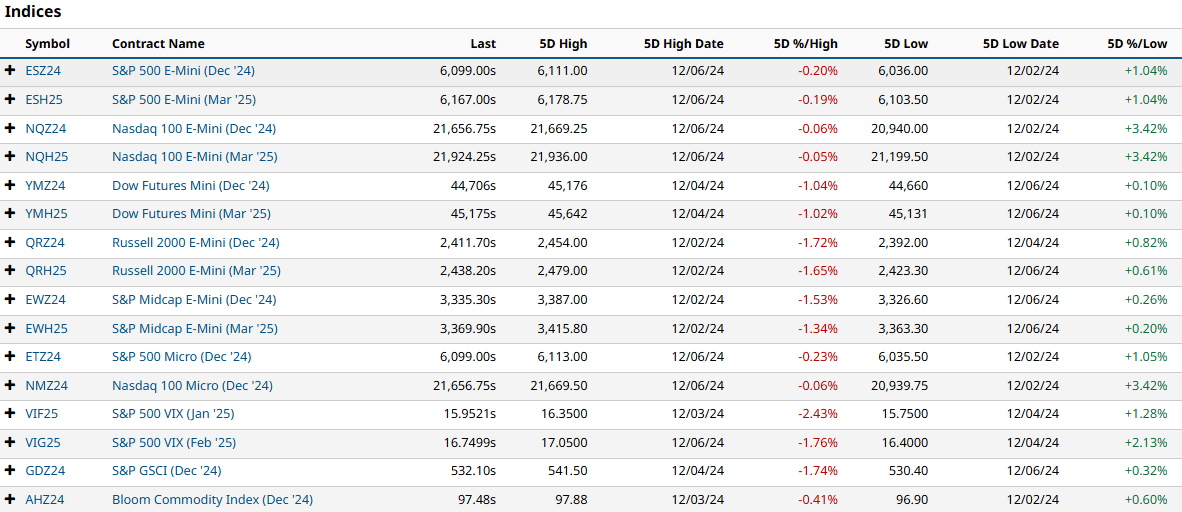

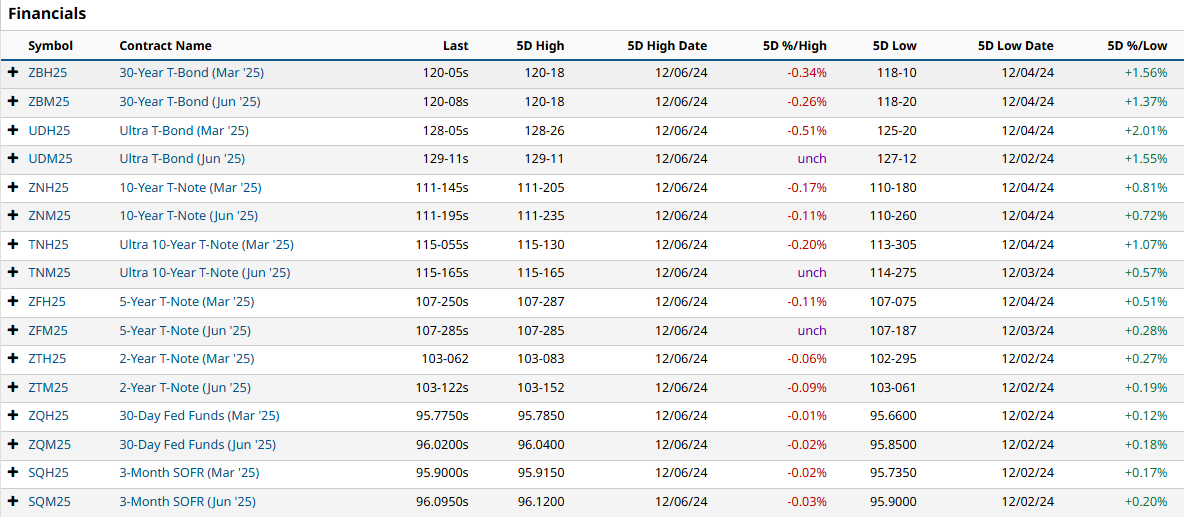

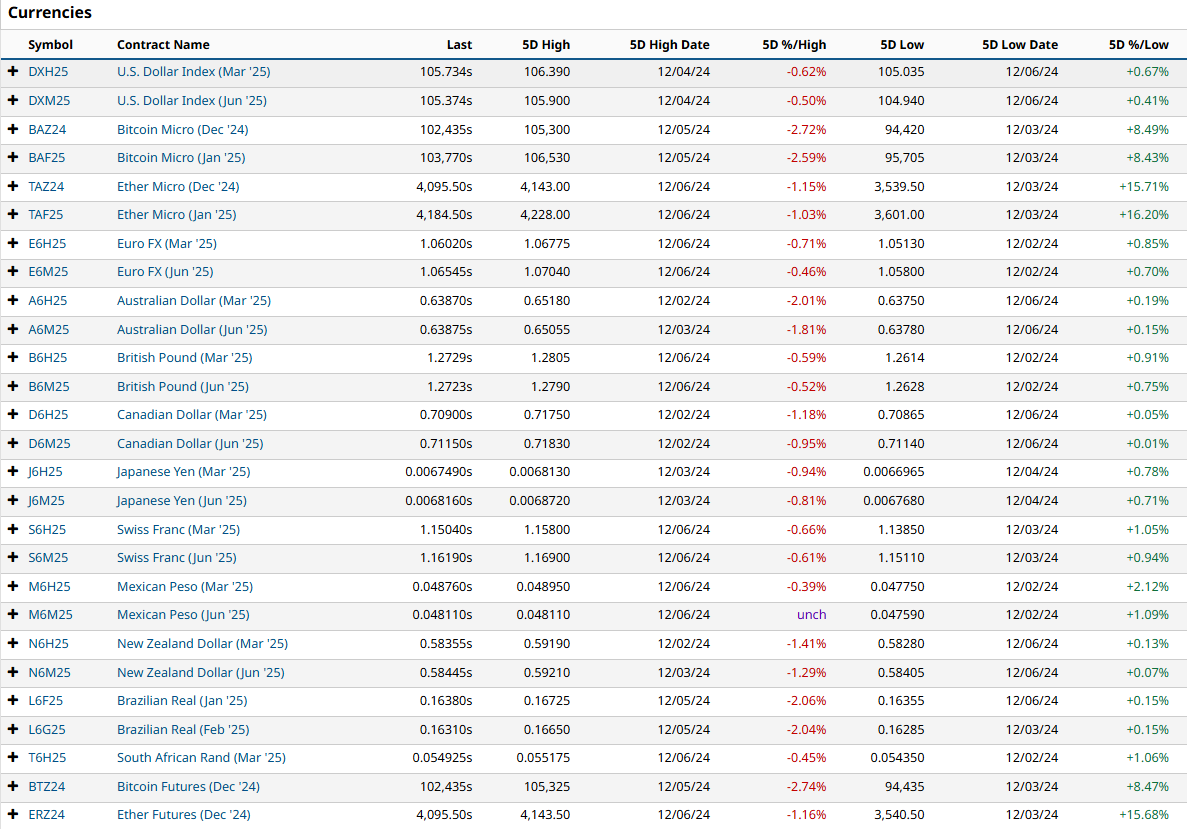

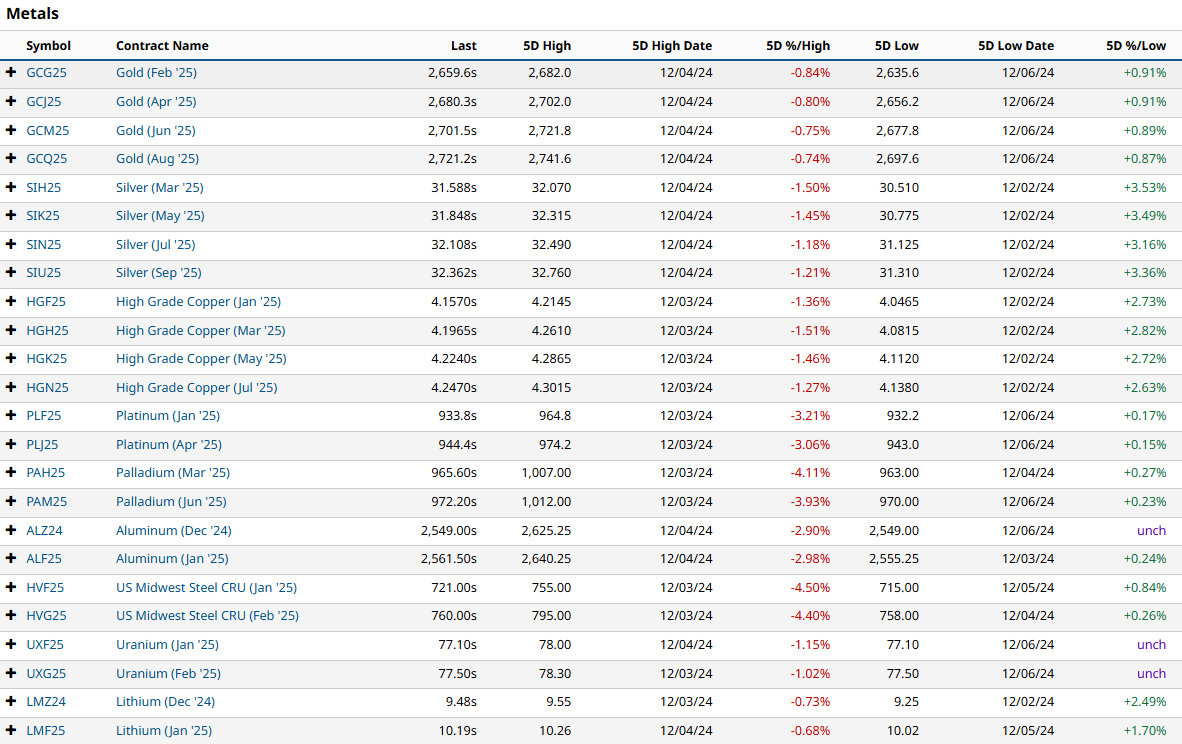

Futures Markets Snapshots

S&P 500: Sector Insights

Technology Sector:

Microsoft (MSFT): Shares rose by approximately 4.75%, closing at $443.57. The company continues to benefit from its strong position in cloud computing and AI services, maintaining investor confidence.

Apple (AAPL): The stock increased by about 2.32%, ending at $242.84. Apple's consistent product demand and services revenue contribute to its steady performance.

NVIDIA (NVDA): Shares surged by 10.77%, reaching $142.44. NVIDIA's dominance in AI hardware and software, along with its recent inclusion in the Dow Jones Industrial Average, has bolstered investor sentiment.

Broadcom (AVGO): The stock climbed by 10.77%, closing at $179.53. Broadcom's role in AI infrastructure and strong financial performance have attracted investor interest.

Consumer Discretionary:

Tesla (TSLA): Shares jumped by 12.77%, ending at $389.22. The rise follows the settlement of a lawsuit with JPMorgan Chase, removing legal uncertainties.

Amazon (AMZN): The stock increased by 9.21%, closing at $227.03. Amazon's announcement of a supercomputer using its Trainium chips for AI startup Anthropic positions it competitively in the AI chip market.

Communication Services:

Meta Platforms (META): Shares rose by 8.61%, reaching $623.77. Meta's advancements in AI and strategic investments have strengthened its market position.

Alphabet (GOOGL): The stock increased by 3.41%, closing at $174.71. Alphabet's continuous innovation in AI and digital advertising supports its growth.

Healthcare:

Eli Lilly (LLY): Shares rose by 3.94%, ending at $826.71. The company's strong product pipeline and positive clinical trial results have enhanced investor confidence.

UnitedHealth Group (UNH): The stock declined by 9.93%, closing at $549.62. The recent tragic death of CEO Brian Thompson has raised concerns about leadership stability.

Financials:

JPMorgan Chase (JPM): Shares fell by 0.94%, ending at $247.36. The settlement of the lawsuit with Tesla may have impacted investor sentiment.

Berkshire Hathaway (BRK.B): The stock decreased by 2.59%, closing at $470.50. Market fluctuations and portfolio performance may have influenced the decline.

Energy:

Exxon Mobil (XOM): Shares dropped by 3.72%, ending at $113.57. Fluctuating oil prices and market dynamics have affected the stock.

Chevron (CVX): The stock fell by 4.13%, closing at $155.24. Similar to Exxon Mobil, Chevron faces challenges from volatile energy markets.

Consumer Staples:

Walmart (WMT): Shares rose by 3.46%, reaching $95.70. Strong sales performance and strategic initiatives have contributed to the gain.

Procter & Gamble (PG): The stock declined by 3.04%, ending at $173.82. Market competition and cost pressures may have impacted the stock.

Industrials:

General Electric (GE): Shares fell by 3.61%, closing at $175.58. The company continues to navigate challenges in its industrial segments.

Boeing (BA): The stock decreased by 2.70%, ending at $153.93. Ongoing issues in production and regulatory scrutiny may have affected investor confidence.

Overall, the technology and consumer discretionary sectors have shown robust performance, driven by advancements in AI and strategic corporate developments. In contrast, the healthcare, financial, and energy sectors faced challenges due to leadership changes, legal matters, and market volatility.

ETF Insights

Major Index ETFs

SPY (+0.87%): The S&P 500 ETF had a modest gain, reflecting a generally positive week for large-cap stocks.

QQQ (+3.28%): Nasdaq's tech-heavy ETF significantly outperformed, driven by strong gains in technology and growth stocks.

DIA (-0.65%): The Dow ETF underperformed, indicating a relative lag in blue-chip industrials.

IWM (-1.22%): Small-cap stocks, represented by the Russell 2000 ETF, faced notable weakness, signaling a risk-off sentiment in smaller companies.

Growth vs. Value

IWF (+3.62%) and VUG (+3.45%): Growth ETFs outperformed significantly, supported by the rally in tech and consumer cyclical sectors.

IWD (-1.94%) and VTV (-1.96%): Value ETFs declined, highlighting weakness in financials, energy, and other traditionally value-oriented sectors.

Sector Highlights

Technology (XLK, +3.04%): Continued strength in tech, supported by outperformers like Microsoft, NVIDIA, and Apple.

Consumer Discretionary (XLY, +4.72%): Tesla and Amazon drove gains, with strong consumer sentiment in select areas.

Energy (XLE, -4.72%) and XOP (-6.64%): Energy ETFs plummeted due to weak oil prices and mixed demand outlooks.

Healthcare (XLV, -2.12%): Weakness in healthcare, led by declines in managed care and biotech.

Leverage and Inverse ETFs:

TQQQ (+9.83%): The leveraged Nasdaq ETF amplified the QQQ’s gains, benefiting from tech momentum.

SOXX (+5.35%): Semiconductor ETFs mirrored the strong tech performance, with NVIDIA and Broadcom leading.

SOXS (-6.92%): Inverse semiconductor ETFs fell sharply, reflecting the bullish momentum in semiconductors.

SQQQ (-9.18%): Bearish leveraged Nasdaq ETFs declined as growth stocks surged.

International Markets:

EFA (+1.41%) and IEFA (+1.30%): Developed market ETFs posted gains, driven by improving global sentiment.

EM (+1.36%): Emerging markets ETFs rose modestly, supported by stronger performance in Asia.

YINN (+4.43%): Leveraged China ETFs saw strong gains, likely reflecting optimism around policy easing or economic recovery.

Commodities:

GLD (-1.07%) and SLV (+1.18%): Gold saw modest losses, while silver gained, reflecting divergent moves in precious metals.

USO (-1.91%) and UNG (-7.35%): Oil and natural gas ETFs struggled, driven by oversupply concerns and weaker demand forecasts.

Fixed Income:

TLT (+0.45%): Long-term Treasury ETFs gained slightly, reflecting easing yields as investors sought safe-haven assets.

SHY (-0.26%): Short-term Treasuries showed slight losses, aligning with rate hike expectations.

TMF (+2.37%): Leveraged Treasury ETFs outperformed as bond markets stabilized.

Cryptocurrency:

BITO (+0.08%) and GBTC (+4.68%): Bitcoin-related ETFs showed resilience, reflecting continued interest in digital assets amid regulatory clarity.

Sector and Strategy Insights

Tech Leadership: Growth and tech-focused ETFs drove market performance, benefiting from optimism around AI, semiconductors, and cloud computing.

Energy Weakness: Declines in energy ETFs highlight ongoing challenges in the oil and gas sectors, including demand uncertainty and pricing pressures.

Divergent Fixed Income Performance: Long-term bonds saw some gains, possibly indicating investor hedging, while shorter durations were more muted.

Crypto Stability: Positive movement in cryptocurrency ETFs suggests improving sentiment, possibly tied to ETF approval optimism or macroeconomic factors.

This performance highlights a continued "risk-on" trade for growth and technology, while value sectors such as energy and financials remain under pressure.

[Special Coverage] Bitcoin: Breakout or Bubble?

Over the past decade, Bitcoin has evolved from an obscure digital experiment into a household name, inspiring fierce debate among economists, investors, and technologists. Lauded by some as the future of finance and dismissed by others as a speculative fad, Bitcoin sits at the intersection of innovation and speculation, begging a crucial question: is it a breakout technology poised to redefine global markets, or a bubble destined to burst, leaving chaos in its wake?

A Brief History of Bitcoin

Bitcoin’s genesis lies in the aftermath of the 2008 financial crisis, a period marked by widespread distrust of traditional financial institutions. Introduced in 2009 by the pseudonymous Satoshi Nakamoto, Bitcoin presented a radical alternative: a decentralized digital currency powered by blockchain technology. By enabling peer-to-peer transactions without intermediaries, Bitcoin aimed to provide financial sovereignty to individuals.

Initially dismissed as niche, Bitcoin began to garner attention as its value steadily climbed. Early adopters saw it as a hedge against inflation and currency devaluation, particularly in countries with unstable economies. By 2021, Bitcoin had reached an all-time high of nearly $69,000 per coin, cementing its status as a serious contender in the financial world. Yet, with dramatic price swings and periodic crashes, skepticism abounds.

The Case for a Breakout

Advocates of Bitcoin argue that it represents a paradigm shift in how we think about money. Unlike traditional currencies, Bitcoin operates on a decentralized network, making it resistant to government manipulation and censorship. This quality has proven especially attractive to individuals in authoritarian regimes or nations grappling with hyperinflation.

Moreover, Bitcoin’s supply cap of 21 million coins ensures scarcity, akin to gold. This “digital gold” narrative has driven its adoption as a store of value. Major institutions, including TSLA 0.75%↑ , MSTR 0.21%↑ , and SQ 0.00%↑ have added Bitcoin to their balance sheets, signaling growing mainstream acceptance.

Technological advancements also bolster Bitcoin’s case. The Lightning Network, a second-layer solution, aims to make Bitcoin transactions faster and more cost-effective, addressing criticisms of scalability. Additionally, developments in regulatory frameworks hint at a future where Bitcoin operates within a structured, less volatile environment.

For proponents, Bitcoin’s decentralized nature, scarcity, and technological evolution position it as a breakout asset capable of disrupting traditional financial systems. As younger, tech-savvy generations embrace digital assets, Bitcoin could well become the cornerstone of a new financial era.

The Case for a Bubble

Despite its promise, Bitcoin faces significant headwinds that suggest its valuation may be inflated. Skeptics point to its extreme volatility, which undermines its utility as a currency or store of value. Bitcoin’s price has often been driven by speculation rather than intrinsic value, leading to dramatic booms and busts.

Moreover, Bitcoin’s reliance on energy-intensive mining has sparked criticism from environmentalists. The process of validating transactions and securing the network consumes vast amounts of electricity, often sourced from fossil fuels. As governments and corporations prioritize sustainability, Bitcoin’s environmental impact could limit its growth.

Regulatory uncertainty poses another challenge. While some countries have embraced Bitcoin, others have imposed outright bans or severe restrictions. In 2021, China’s crackdown on cryptocurrency mining and trading sent shockwaves through the market. Future regulatory actions in major economies could stifle adoption and erode investor confidence.

Critics also question Bitcoin’s scalability. While the Lightning Network offers potential solutions, it remains in its infancy, and Bitcoin’s base layer struggles to handle high transaction volumes. Competing cryptocurrencies, such as Ethereum, offer more versatile platforms for decentralized applications, potentially diminishing Bitcoin’s dominance.

The Middle Ground: Bitcoin as an Asset Class

While the debate between breakout and bubble rages on, an emerging perspective positions Bitcoin as a new asset class. Neither destined to replace fiat currencies nor collapse entirely, Bitcoin could find its niche as a speculative investment akin to commodities or high-risk equities.

This view is supported by the growing infrastructure around Bitcoin. From regulated futures markets to Bitcoin exchange-traded funds (ETFs), financial instruments have emerged to facilitate institutional and retail participation. These developments suggest that Bitcoin is maturing, even if its path to mass adoption remains uncertain.

Bitcoin’s role as a portfolio diversifier is also gaining traction. Its lack of correlation with traditional assets makes it appealing to investors seeking to hedge against market downturns. While not without risks, Bitcoin’s inclusion in a diversified portfolio could offer asymmetric returns, balancing its volatility with its potential for outsized gains.

Lessons from History

Bitcoin’s trajectory bears striking similarities to past financial innovations. The dot-com bubble of the late 1990s, for example, saw astronomical valuations for internet companies, many of which ultimately failed. Yet, the underlying technology—the internet—revolutionized the world. Bitcoin could follow a similar pattern: a speculative phase marked by wild swings, followed by stabilization and integration into the broader economy.

Another historical parallel is the emergence of gold as a store of value. Gold’s journey from ornamental metal to financial cornerstone took centuries, shaped by cultural, economic, and technological factors. Bitcoin, still in its infancy, may require similar time and adaptability to cement its role.

The Path Forward

For Bitcoin to transcend its current volatility and skepticism, several developments are essential:

Regulatory Clarity: Clear, consistent regulations will provide the framework needed for broader adoption. Governments must strike a balance between fostering innovation and protecting consumers.

Technological Maturation: Scalability solutions like the Lightning Network must prove reliable, enabling Bitcoin to handle increased demand without compromising security.

Environmental Sustainability: Transitioning to renewable energy sources for mining operations could mitigate environmental concerns and enhance Bitcoin’s reputation.

Education and Awareness: Public understanding of Bitcoin’s utility and risks remains limited. Comprehensive education initiatives can empower individuals to make informed decisions.

Conclusion

Bitcoin embodies both the promise and peril of financial innovation. As a breakout technology, it challenges the status quo, offering a decentralized alternative to traditional finance. Yet, its volatility, environmental impact, and regulatory uncertainty underscore its speculative nature, raising legitimate concerns about its long-term viability.

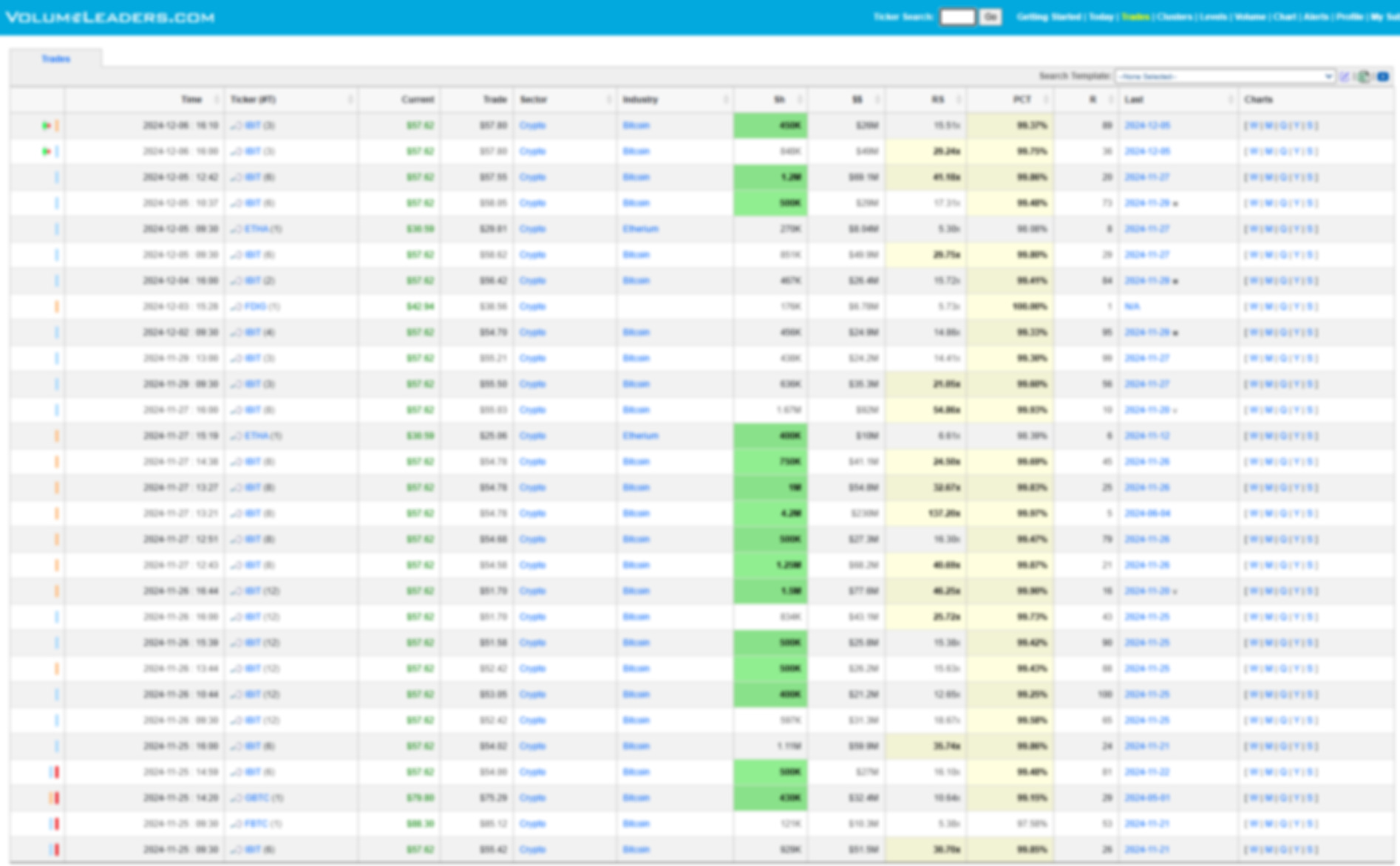

Whether Bitcoin proves to be a transformative breakthrough or a fleeting bubble will depend on how it navigates these challenges. In the meantime, it remains a fascinating experiment at the frontier of technology and finance, reflecting humanity’s enduring quest for progress and freedom. As the world watches and debates, one thing is certain: Bitcoin’s story is far from over. If you’re a VL subscriber, use the built-in search template to quickly see all of the institutional positioning in your favorite crypto tickers.

Whether you’re watching crypto-related tickers like COIN 0.55%↑ MSTR 0.21%↑ or RIOT 0.00%↑ or you’re seeking more direct exposure through ETFs like IBIT 0.53%↑ BITX 1.09%↑ and GBTC 0.00%↑ you’re going to want to login and see where institutions are positioned because there have been absolutely no shortages of prints since Thanksgiving:

US Investor Sentiment

Insider Trading

Insider trading occurs when a company’s leaders or major shareholders trade stock based on non-public information. Tracking these trades can reveal insider expectations about the company’s future. For example, large purchases before an earnings report or drug trial results might indicate confidence in upcoming good news.

%Bull-Bear Spread

The %Bull-Bear Spread chart is a sentiment indicator that shows the difference between the percentage of bullish and bearish investors, often derived from surveys or sentiment data, such as the AAII (American Association of Individual Investors) sentiment survey. This spread tells investors about the prevailing mood in the market and can provide insights into market extremes and potential turning points.

Bullish or Bearish Sentiment:

When the spread is positive, it means more investors are bullish than bearish, indicating optimism about the market’s direction.

A negative spread indicates more bearish sentiment, meaning more investors expect the market to decline.

Contrarian Indicator:

The %Bull-Bear Spread is often used as a contrarian indicator. For example, extremely high levels of bullish sentiment might suggest that the market is overly optimistic and could be due for a correction.

Similarly, when bearish sentiment is extremely high, it might indicate that the market is overly pessimistic, and a rally could be on the horizon.

Market Extremes and Reversals:

Historically, extreme values of the spread (both positive and negative) can signal turning points in the market. A very high positive spread can signal market exuberance, while a very low or negative spread may indicate fear or capitulation.

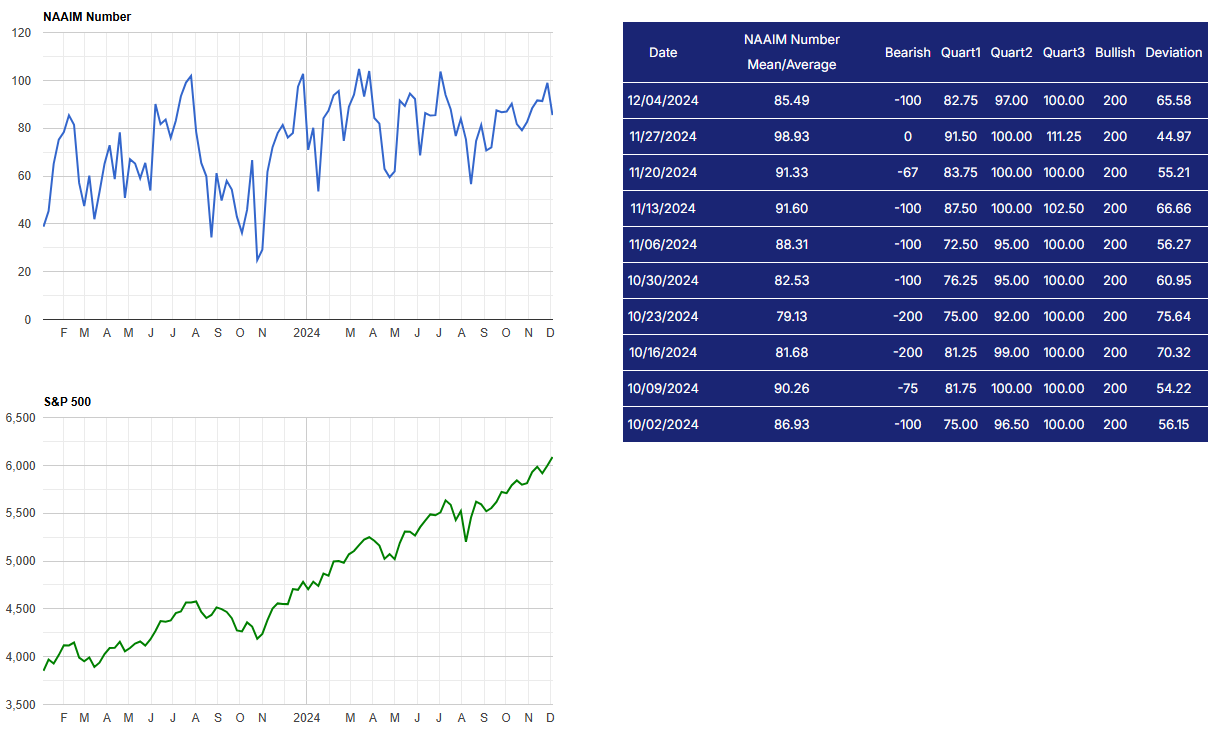

NAAIM Exposure Index

The NAAIM Exposure Index (National Association of Active Investment Managers Exposure Index) measures the average exposure to U.S. equity markets as reported by its member firms. These are typically active money managers who provide their equity exposure levels weekly. The index offers insight into how much these managers are investing in equities at any given time, ranging from being fully short (-100%) to leveraged long (up to +200%).

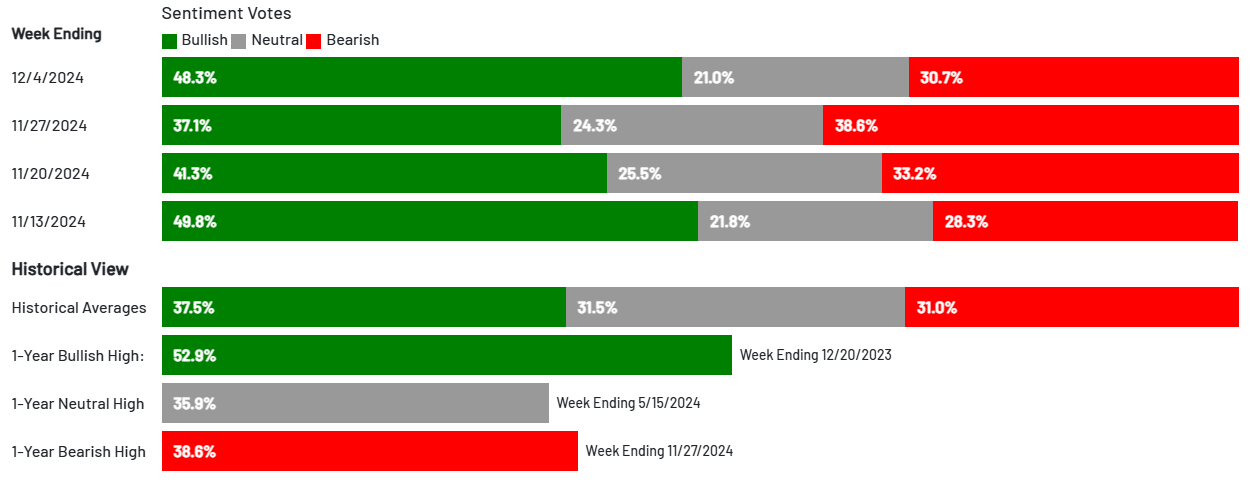

AAII Investor Sentiment Survey

The AAII Investor Sentiment Survey is a weekly survey conducted by the American Association of Individual Investors (AAII) to gauge the mood of individual investors regarding the direction of the stock market over the next six months. It provides insights into whether investors are feeling bullish (expecting the market to rise), bearish (expecting the market to fall), or neutral (expecting the market to stay about the same).

Key Points:

Bullish Sentiment: Reflects the percentage of investors who believe the stock market will rise in the next six months.

Bearish Sentiment: Represents those who expect a decline.

Neutral Sentiment: Reflects investors who anticipate little to no market movement.

The survey is widely followed as a contrarian indicator, meaning that extreme levels of bullishness or bearishness can sometimes signal market turning points. For example, when a large number of investors are overly optimistic (high bullish sentiment), it could suggest a market top, while excessive pessimism (high bearish sentiment) may indicate a market bottom is near.

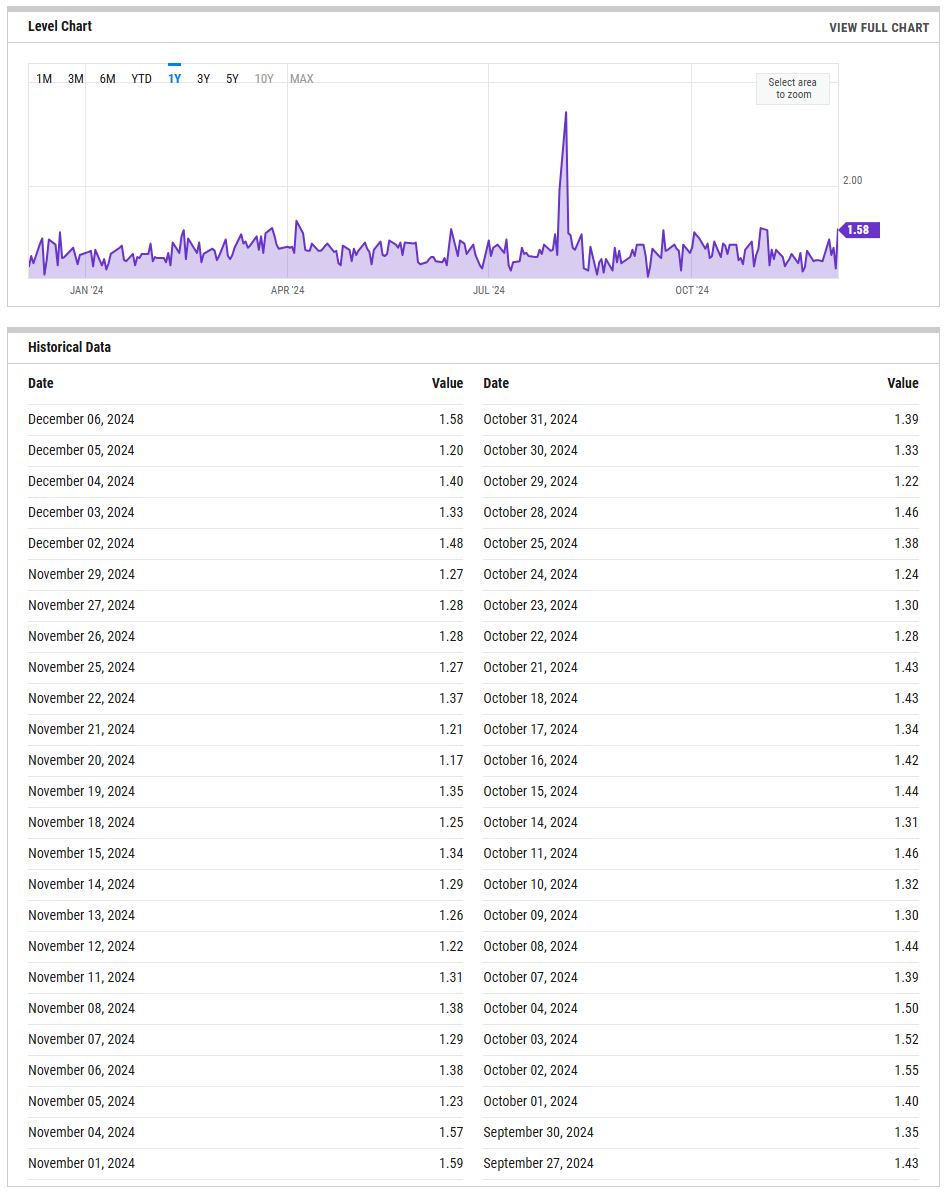

SPX Put/Call Ratio

The SPX Put/Call Ratio is an indicator that is used to gauge market sentiment. This is calculated as the ratio between trading S&P 500 put options and S&P call options. A high put/call ratio can indicate fear in the markets, while a low ratio indicates confidence. For example, in 2015, the Put-Call ratio was as high as 3.77 because of market fears stemming from various global economic issues like a GDP growth slowdown in China and a Greek debt default.

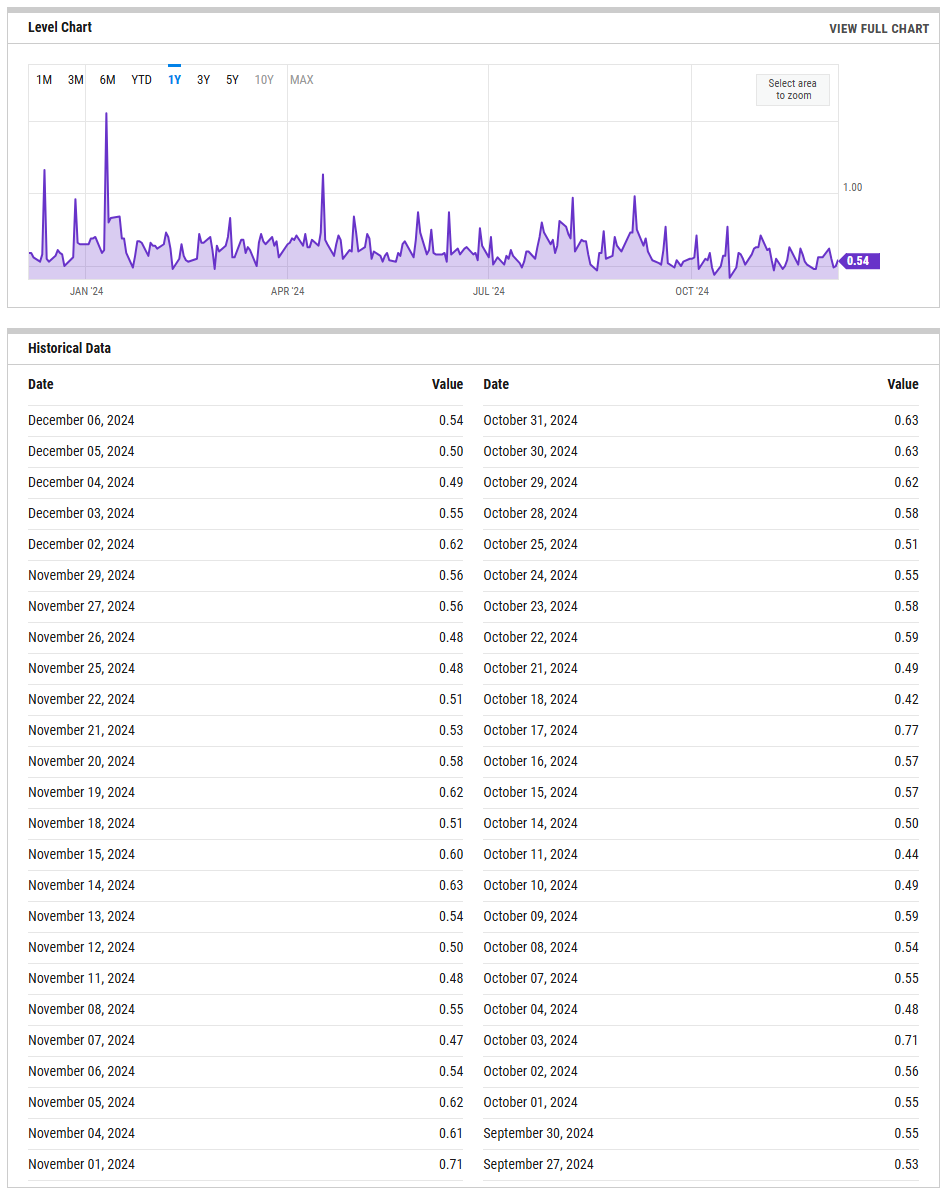

CBOE Equity Put/Call Ratio

The CBOE (Chicago Board Options Exchange) equity put/call ratio is a sentiment indicator used by traders and analysts to gauge market sentiment and potential shifts in investor behavior. It is calculated by dividing the volume of put options by the volume of call options on equities. Here’s what it reveals and how it is generally interpreted:

High Put/Call Ratio: When the put/call ratio is high (above 1.0), it suggests that there is more demand for put options than call options. This typically reflects a more bearish sentiment, as investors may be hedging against potential declines or expecting the market to fall.

Low Put/Call Ratio: Conversely, a low put/call ratio (below 0.7) indicates a higher volume of call options compared to puts, reflecting bullish sentiment. Investors may be expecting upward momentum and are positioning themselves to profit from price gains

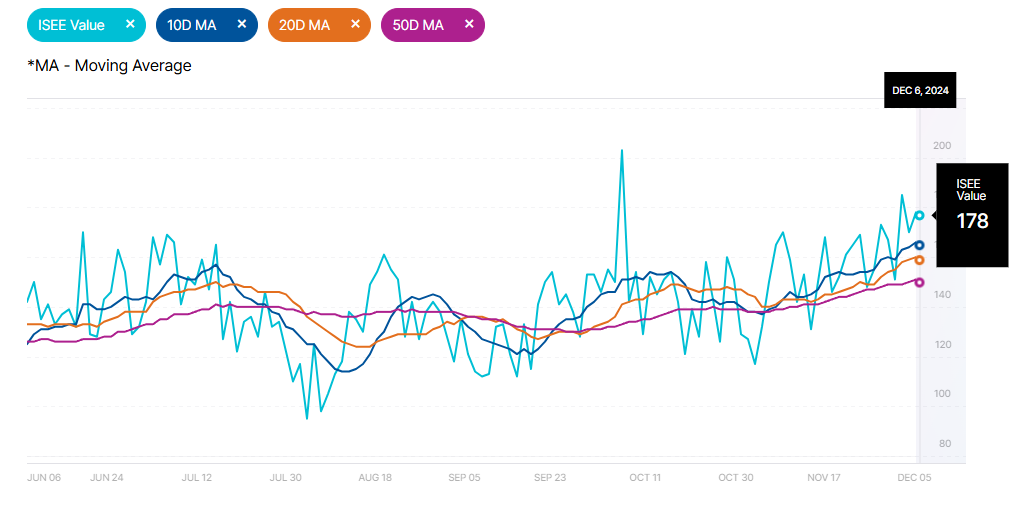

ISEE Sentiment Index

The ISEE (International Securities Exchange Sentiment) Index is a measure of investor sentiment derived from options trading. Unlike traditional put/call ratios, the ISEE Index focuses only on opening long customer transactions and is adjusted to remove market-maker and firm trades, providing a purer sentiment reading.

The ISEE Index typically ranges from 0 to 200, with readings above 100 indicating more call options being bought relative to put options, suggesting bullish sentiment. Conversely, readings below 100 suggest bearish sentiment, with more puts being purchased relative to calls.

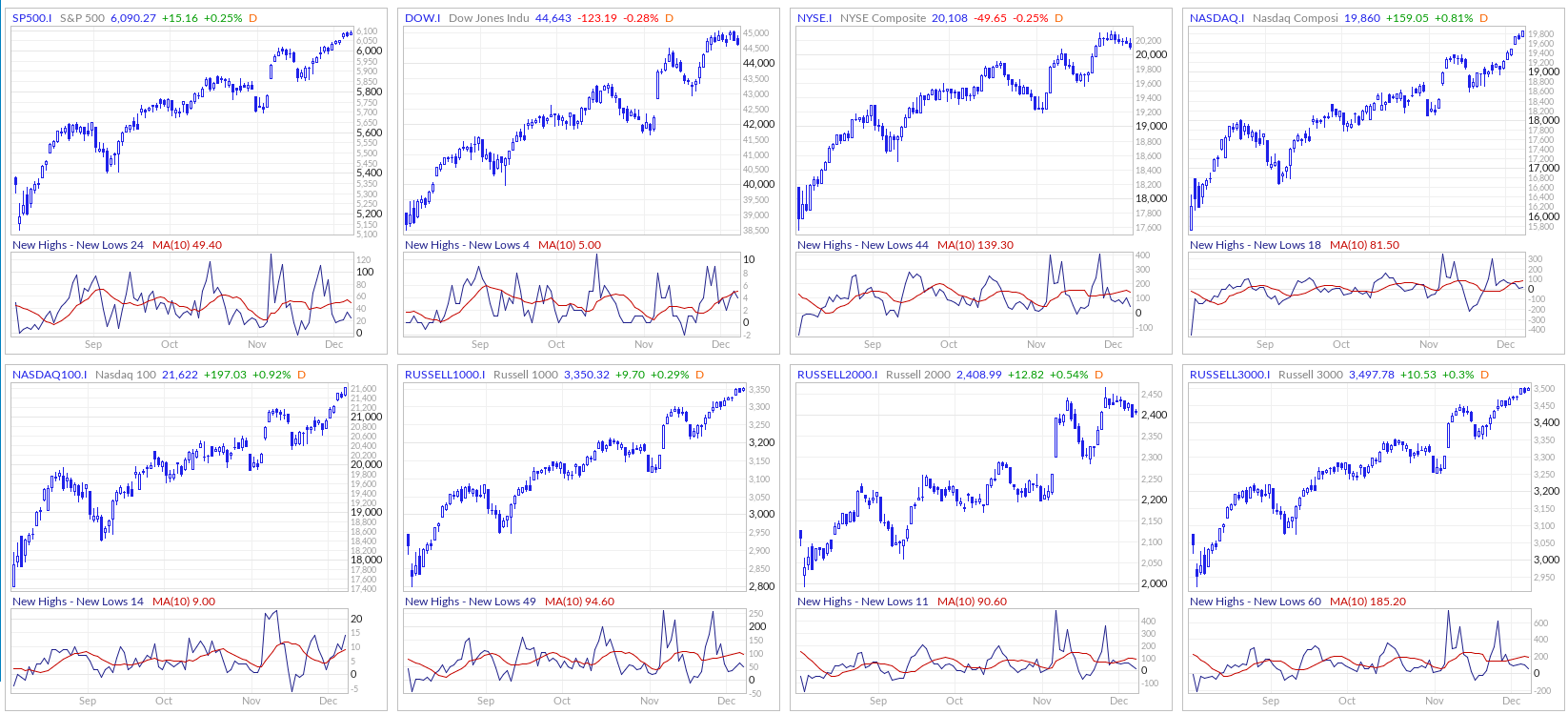

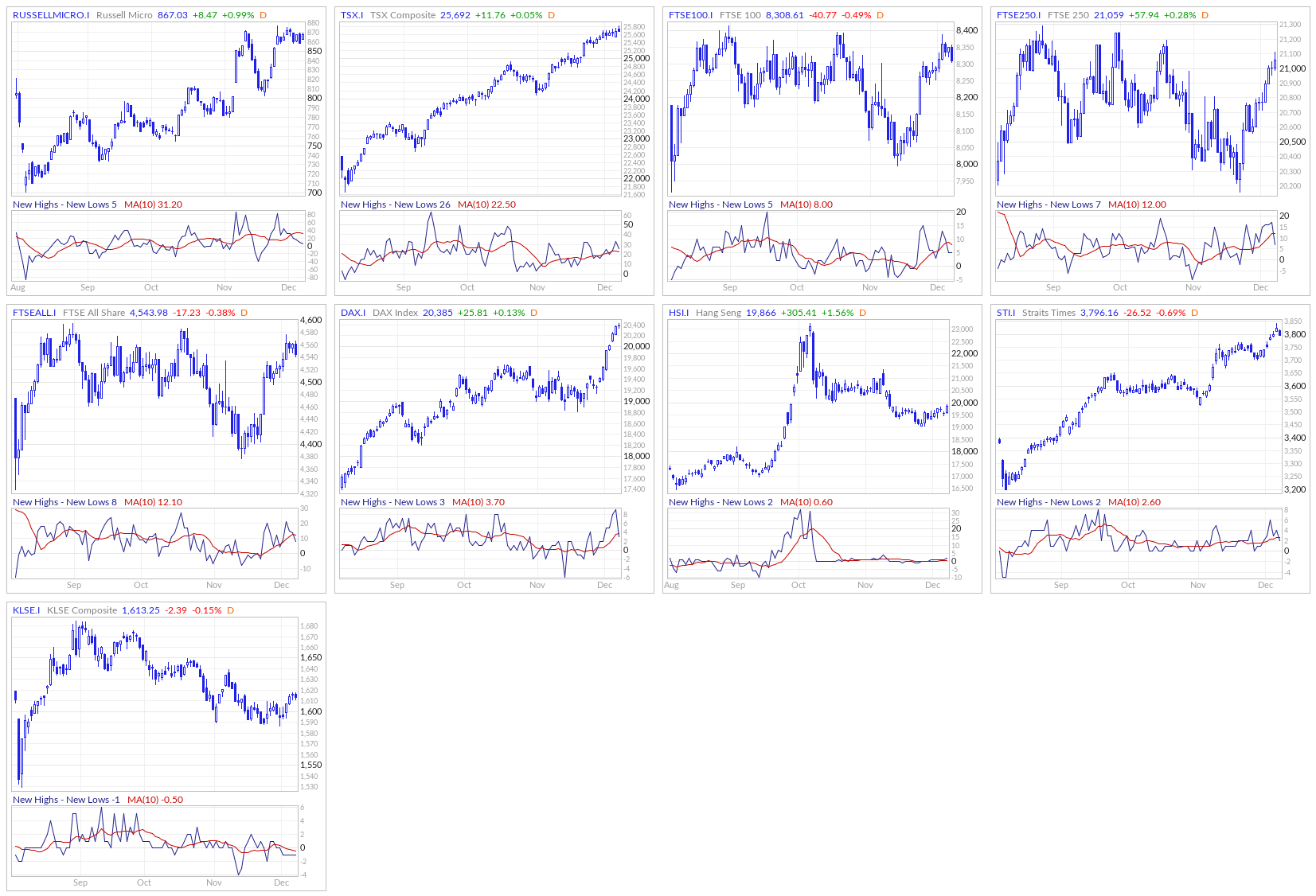

New Highs - New Lows

The New Highs - New Lows indicator (NH-NL) displays the daily difference between the number of stocks reaching new 52-week highs and the number of stocks reaching new 52-week lows. The NH-NL indicator generally reaches its extreme lows slightly before a major market bottom. As the market then turns up from the major bottom, the indicator jumps up rapidly. During this period, many new stocks are making new highs because it's easy to make a new high when prices have been depressed for a long time. The NH-NL indicator oscillates around zero. If the indicator is positive, the bulls are in control. If it is negative, the bears are in control. As the cycle matures, a divergence often occurs as fewer and fewer stocks are making new highs (the indicator falls), yet the market indices continue to reach new highs. This is a classic bearish divergence that indicates that the current upward trend is weak and may reverse.

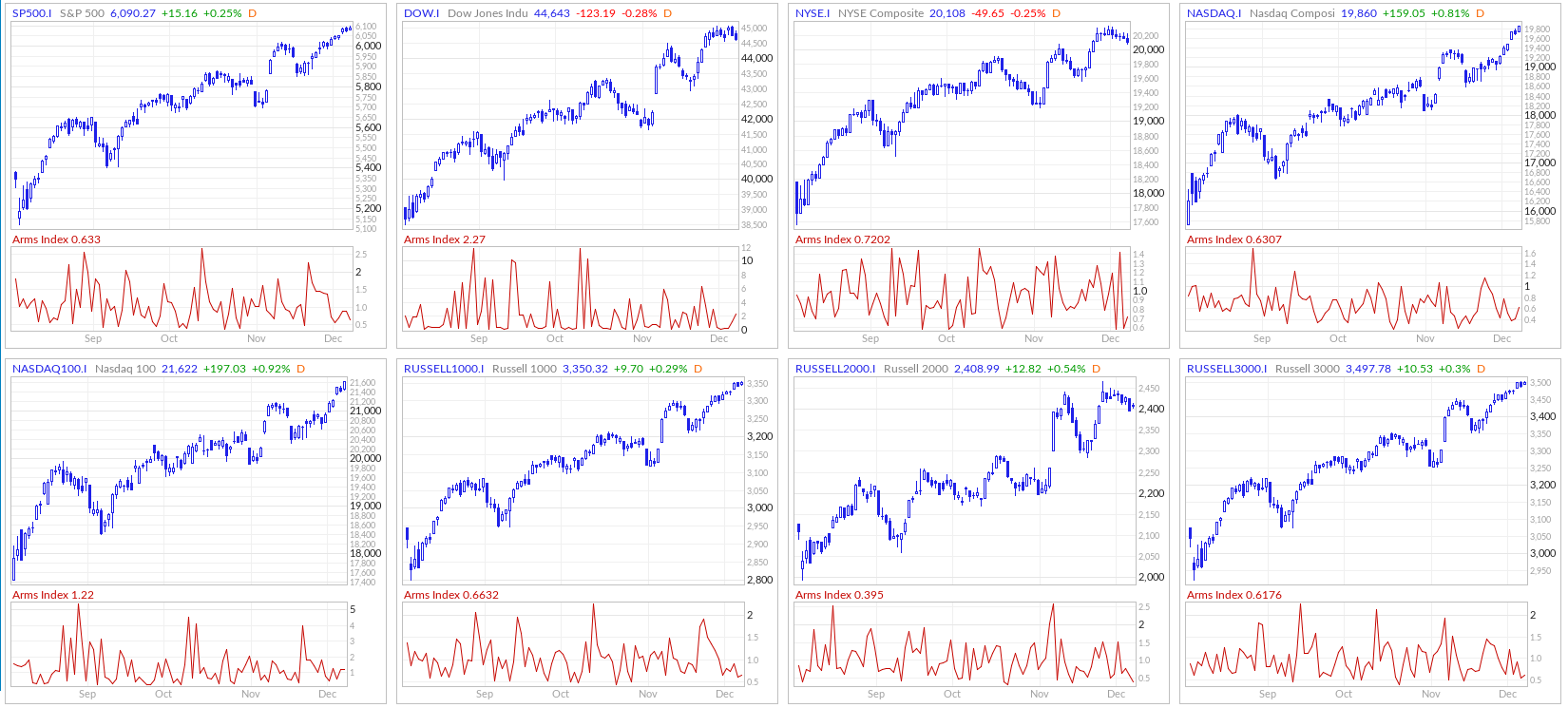

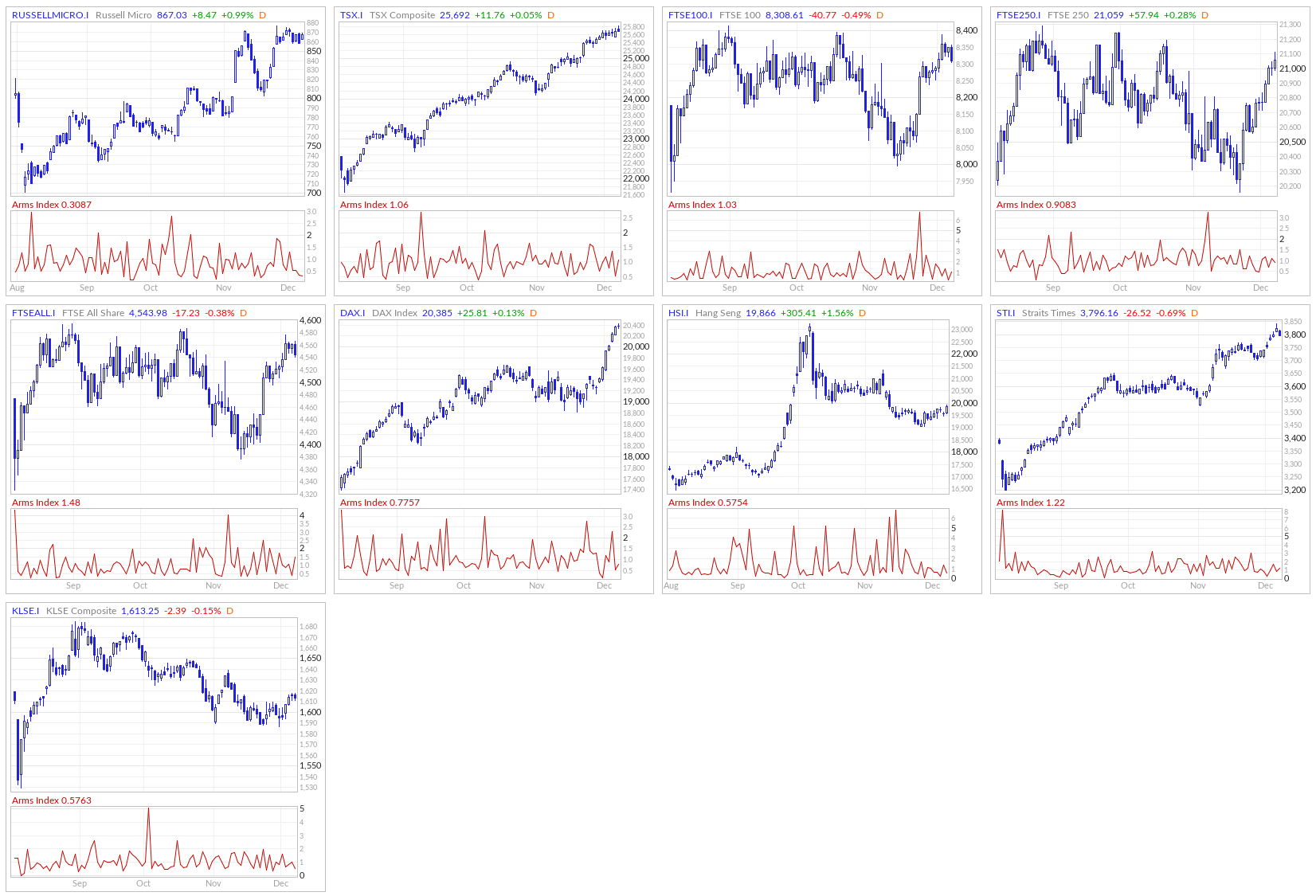

ARMS Index

The Arms Index, also known as the TRIN (Short-Term TRading INdex), was developed by Richard Arms in the 1960s. It is calculated by dividing the ratio of advancing stocks to declining stocks by the ratio of advancing volume to declining volume. Interpreting the Arms Index involves looking at its value in relation to certain thresholds. A value below "1" is considered bullish, indicating that advancing stocks and volume dominate the market. Conversely, a value above "1" is considered bearish, suggesting that declining stocks and volume are more prevalent. Extremely low values (below 0.5) or high values (above 2) are often seen as potential reversal signals.

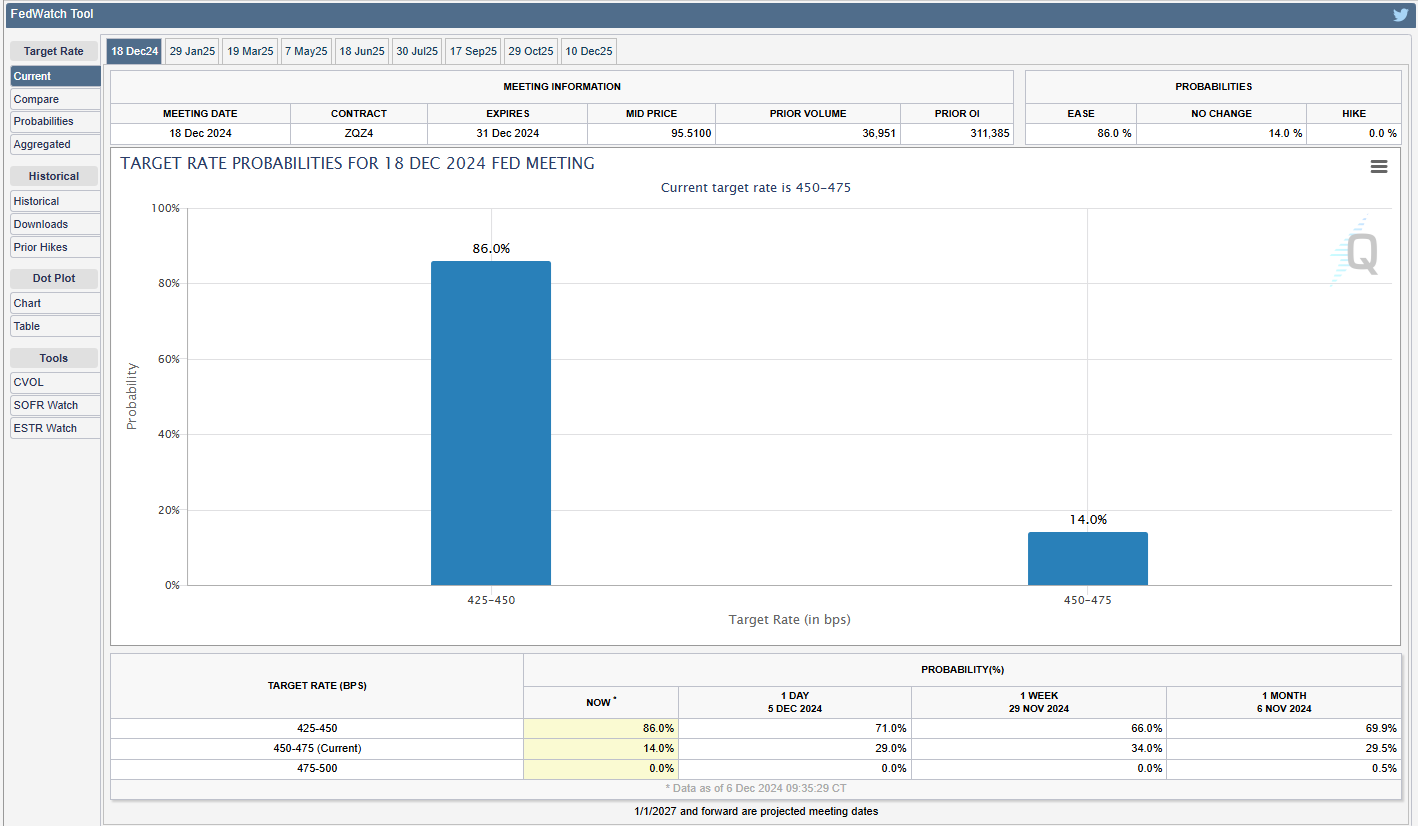

CME Fedwatch

What is the likelihood that the Fed will change the Federal target rate at upcoming FOMC meetings, according to interest rate traders? Use CME FedWatch to track the probabilities of changes to the Fed rate, as implied by 30-Day Fed Funds futures prices.

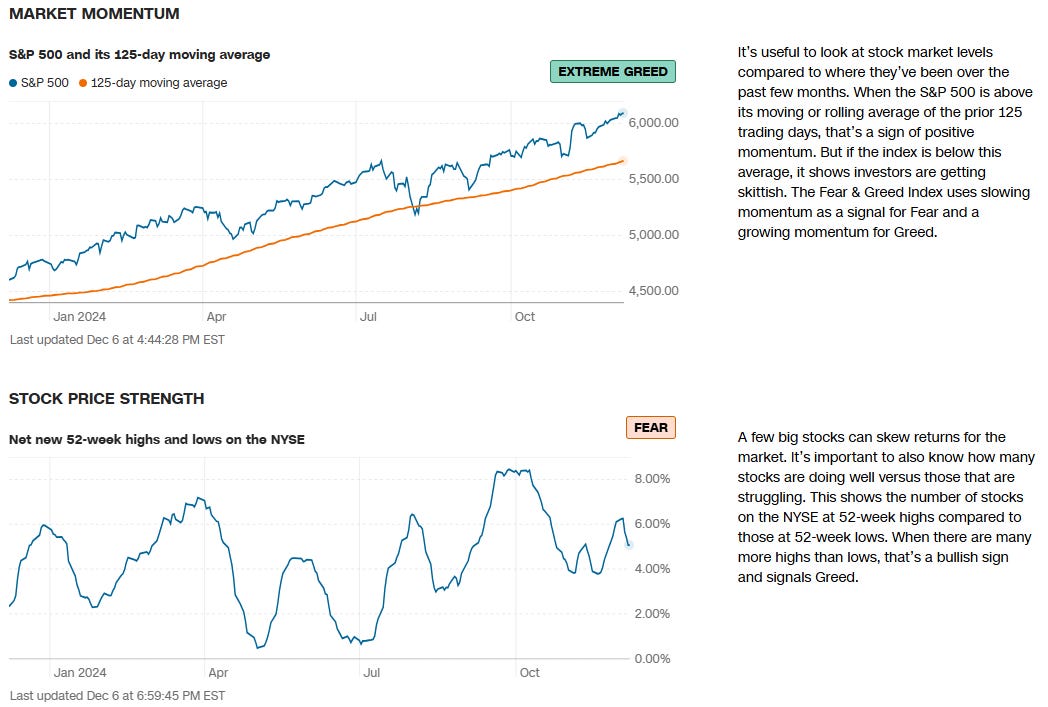

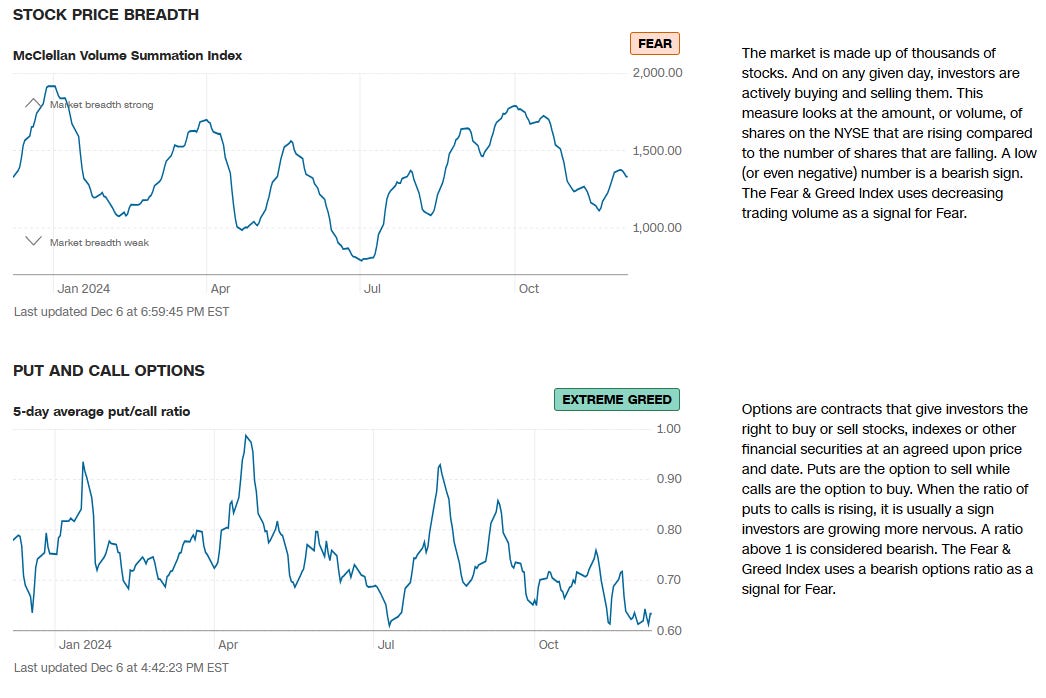

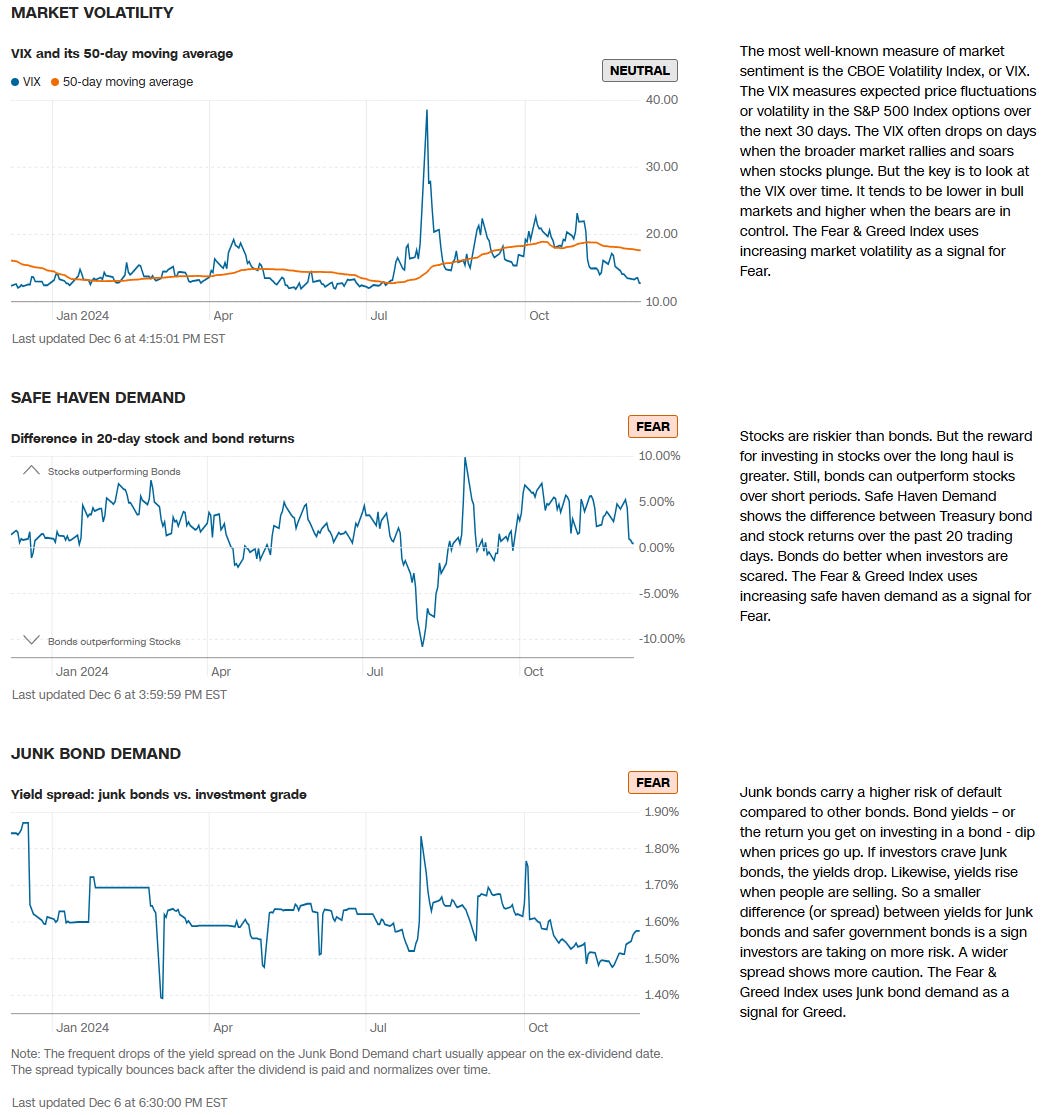

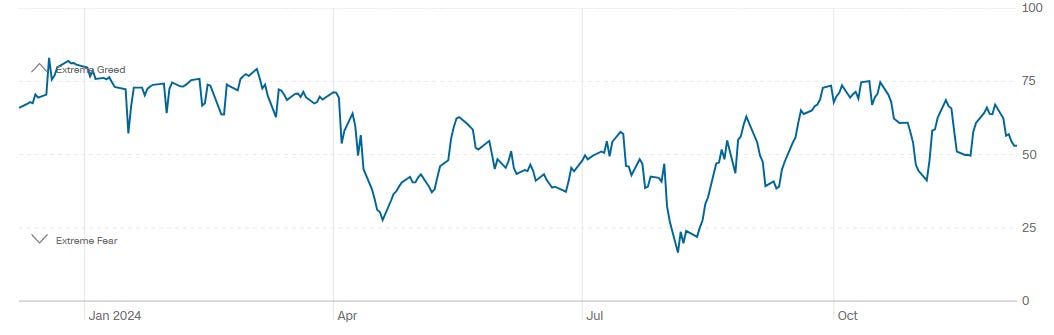

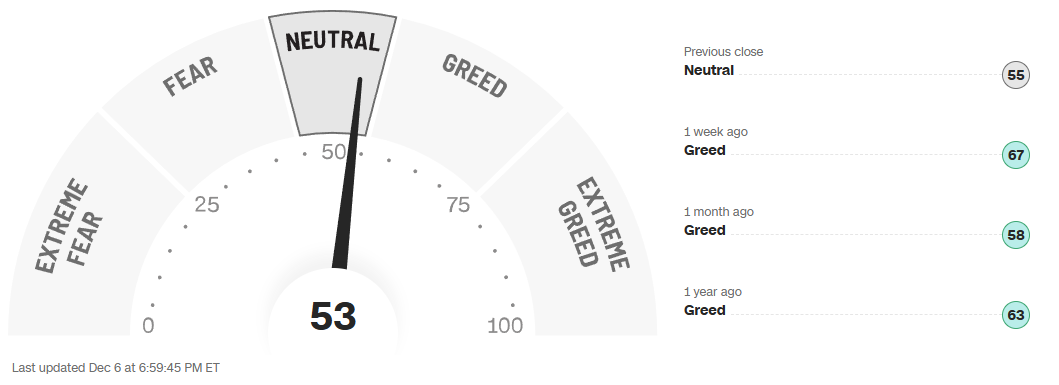

CNN Fear & Greed Constituent Data Points & Composite Index

Final Composite Fear & Greed Index Reading

Institutional S/R Levels for Major Indices

When you’re a large institutional player, your primary goal is to find liquidity - places to do a ton of business with the least amount of slippage possible. VolumeLeaders.com automatically identifies and visually plots the exact spots where institutions are doing business and where they are likely to return for more. It’s one of the primary reasons “support” and “resistance” concepts work and truly one of the reasons “price has memory”.

Levels from the VolumeLeaders.com platform can help you formulate trades theses about:

Where to add or take profit

Where to de-risk or hedge

What strikes to target for options

Where to expect support or resistance

And this is just a small sample; there are countless ways to leverage this information into trades that express your views on the market. The platform covers thousands of tickers on multiple timeframes to accommodate all types of traders. Observe for yourself how accurate the levels are by marking-up your charts with the information in the “Trade Levels” boxes and play-along in real-time this week.

SPY -0.01%↓

SPY has steadily broken through several major volume-based resistance levels, each previously highlighted by heavy institutional-sized trades in the $583–$593 range. After consolidating around these high-volume zones, the ETF advanced higher, confirming that buyers absorbed supply at key support levels. The price is now trading well above these large trade clusters, suggesting that the market has efficiently digested past selling pressure and continues to find willing buyers on dips.

With each successful test of former resistance—now likely turning into support—SPY’s uptrend structure remains intact. The series of higher lows and higher highs, combined with the ability to push above major liquidity pools, indicates positive momentum. Unless the price slips back below these volume-heavy regions, the technical picture favors continued strength in the near term.

QQQ 0.04%↑

QQQ has successfully reclaimed and advanced beyond several major volume-based supply zones, indicating strong buyer commitment. Initially, heavy institutional trades created resistance around $505–$512. After consolidating and absorbing that selling pressure, the ETF broke higher, showing that demand was robust enough to overcome these large-volume hurdles.

With prior overhead supply now likely converting into support, the path of least resistance appears to the upside. The shift from defending old resistance levels to building a series of higher lows and highs suggests bullish momentum is intact. As long as QQQ remains above these previously challenging price zones, the technical posture supports further gains

IWM 0.02%↑

IWM faced substantial resistance after its initial rebound from lower-volume support levels near $227–$230. Heavy institutional-sized trades around $238–$242 created an overhead supply zone that has thus far capped the upside. After an attempt to push higher, the ETF was unable to hold above these liquidity-rich areas and has since retreated, suggesting sellers remain active at those key price levels.

This rejection near previously established high-volume clusters indicates a market in equilibrium rather than a clear uptrend. Price action is now oscillating between its support and resistance zones, hinting at range-bound conditions until a decisive breakout occurs. If IWM can break and sustain above the $240–$242 band, it would signal that buyers have absorbed supply and are ready to push higher. Conversely, a failure to hold the lower support levels would tilt the balance in favor of sellers, potentially leading to a retest of the November lows.

DIA 0.00%↑

DIA staged an impressive recovery from its November lows, pushing through multiple price zones marked by large institutional trades. These previously high-volume areas between roughly $432–$439 acted first as resistance and then converted into stepping stones on the ETF’s climb higher. However, as DIA approached the upper boundary near $447–$448—another region with notable transaction density—it met increased selling pressure.

The inability to sustain momentum above these upper-volume clusters suggests that overhead supply remains an obstacle. With the ETF now slipping below a key previously conquered level, the immediate technical picture implies consolidation or a short-term pause in the uptrend. Should DIA hold above the lower volume-based support zones, it may merely be regrouping before another attempt higher. On the other hand, a decisive break below those established support areas would tilt the balance back toward the bears, warranting caution until buyers can reassert strength.

Institutional Order Flow

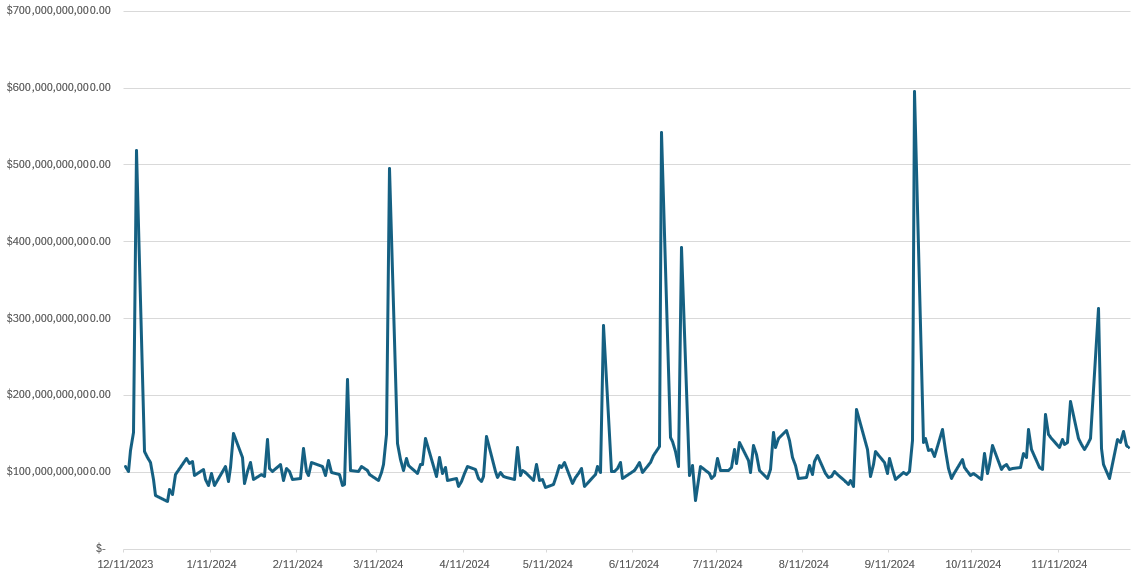

Rolling 1-Yr Dollars By Day

This chart shows institutional activity by dollars by day on a rolling 1-year basis. From a theoretical standpoint, examining a chart of daily institutional dollar activity over the course of a year can offer several insights and possible inferences, though all should be approached with caution since the data alone may not prove causality or confirm underlying reasons. Some potential takeaways include:

Event-Driven Behavior:

Sharp, singular spikes on certain days might correlate with major market-moving events. These could include central bank policy announcements, significant geopolitical news, sudden macroeconomic data releases (like employment reports or GDP data), earnings seasons for large-cap companies, or unexpected shocks (e.g., mergers, acquisitions, regulatory changes).Liquidity Dynamics:

Institutions often concentrate large trades on days with higher expected liquidity. For instance, heightened activity might coincide with index reconstitutions, option expiration dates, or the days leading up to or following a major index rebalance, when large amounts of capital shift hands simultaneously.Risk Management and Hedging Activity:

Institutions may significantly adjust their exposures on days that are critical from a risk management perspective. Large spikes can occur if hedge funds, pension funds, or asset managers are rolling over futures contracts, initiating or closing out large hedges, or reacting to volatility triggers.Market Sentiment Indicators:

While the data is purely transactional, the sheer volume of institutional involvement on certain days might indirectly hint at changing sentiment or strategic shifts.

In essence, a chart like this can lead you to hypothesize that institutional trading volumes are not constant or random but rather influenced by a mix of predictable calendar effects, major market events, liquidity considerations, risk management decisions, and strategic allocation shifts.

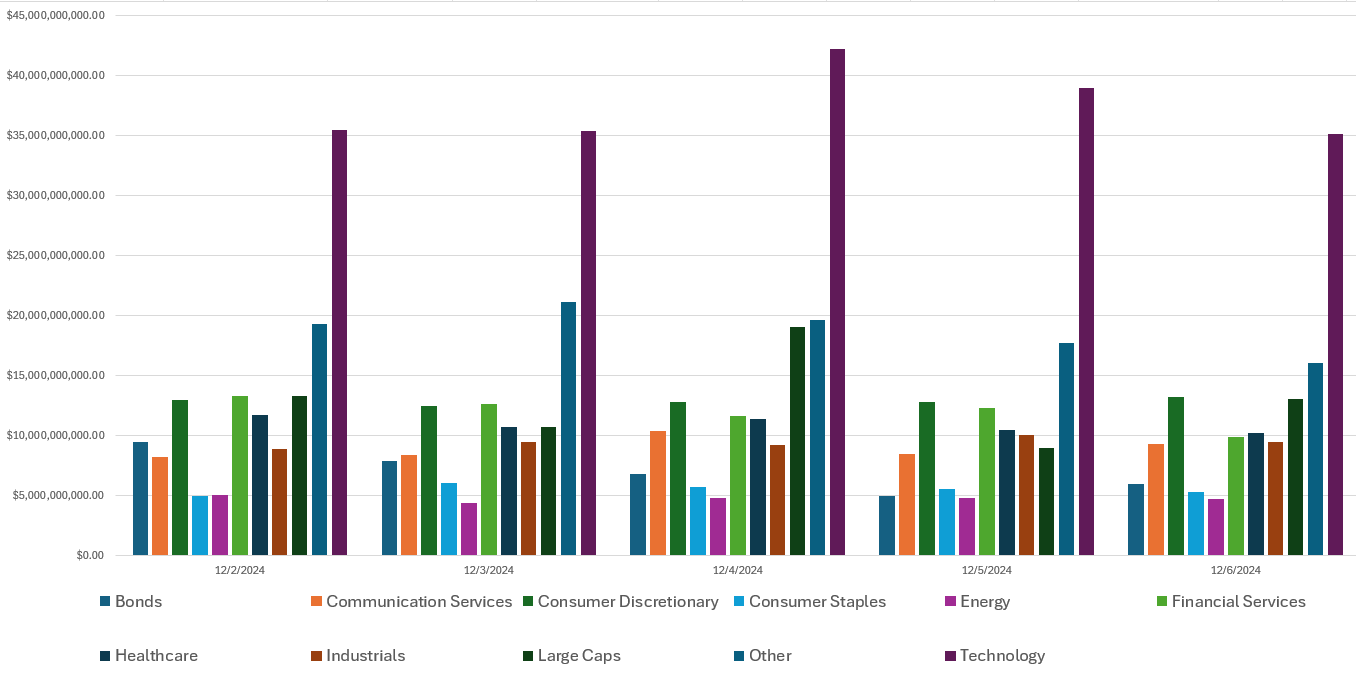

Last Week’s Institutional Activity By Sector

This is an incredibly important chart to watch as it contains lots of nuanced suggestions at a thematic level. Watch this chart closely week-to-week to stay informed about where institutional money is flowing, adjust your strategies based on momentum, align your portfolio with macroeconomic and market trends, and manage risks more effectively by avoiding sectors losing institutional favor. The Top 10 active sectors are identified and the rest grouped as “Other”.

Sector Rotation Insights: The chart highlights which sectors are attracting institutional activity and which are losing favor. Institutions often lead market trends, so tracking shifts in their focus can indicate sector rotations.

Sentiment Analysis: The level of institutional activity reflects confidence in specific sectors. Rising activity in traditionally defensive sectors (e.g., healthcare, utilities) may indicate caution, while a surge in growth sectors (e.g., technology, consumer discretionary) could suggest optimism.

Emerging Trends: Sudden spikes in a previously overlooked sector, like industrials or consumer staples, might hint at emerging opportunities or structural shifts.

Macro Themes: Changes in sector activity often align with broader macroeconomic themes like inflation, interest rates, or geopolitical events. For instance:

Increased activity in energy might indicate concerns about oil supply or rising prices.

Growth in technology could align with innovations or favorable policies.

Risk Management: Declining institutional activity in a sector might signal weakening fundamentals or heightened risks.

Spotting Overcrowding: Excessive activity in a single sector over multiple weeks may suggest overcrowding, which could lead to heightened volatility if institutions begin to exit.

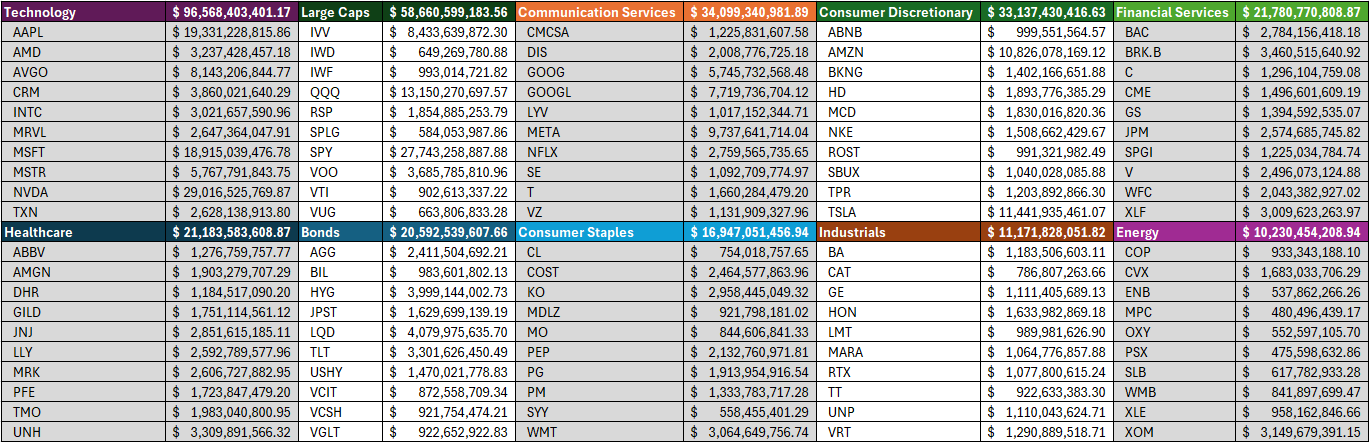

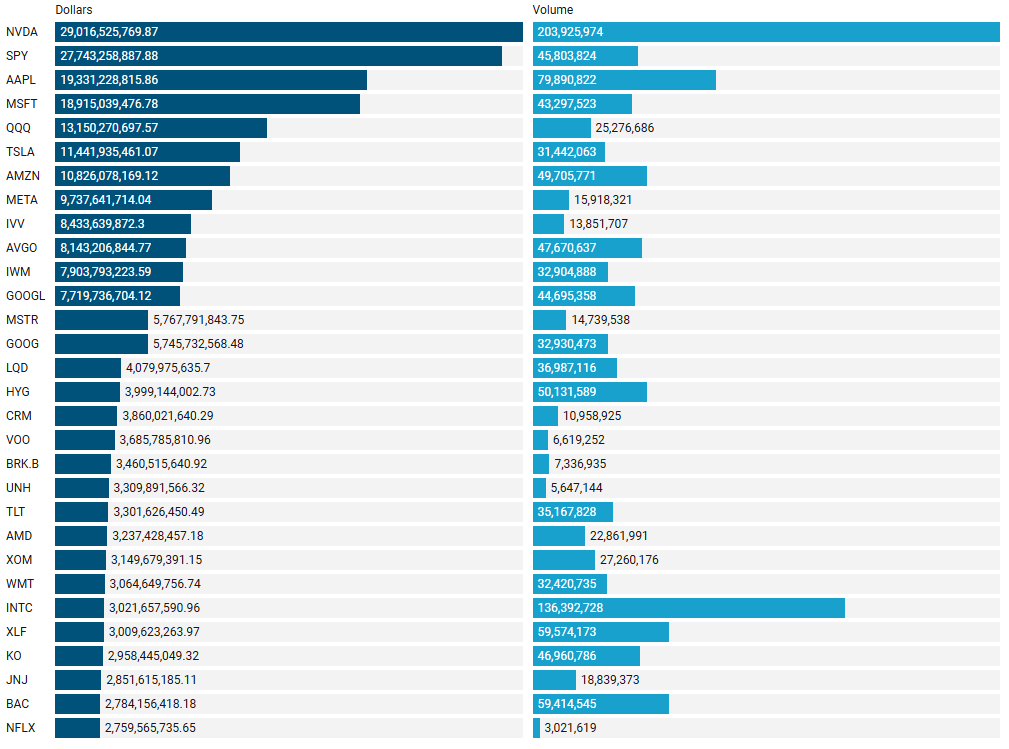

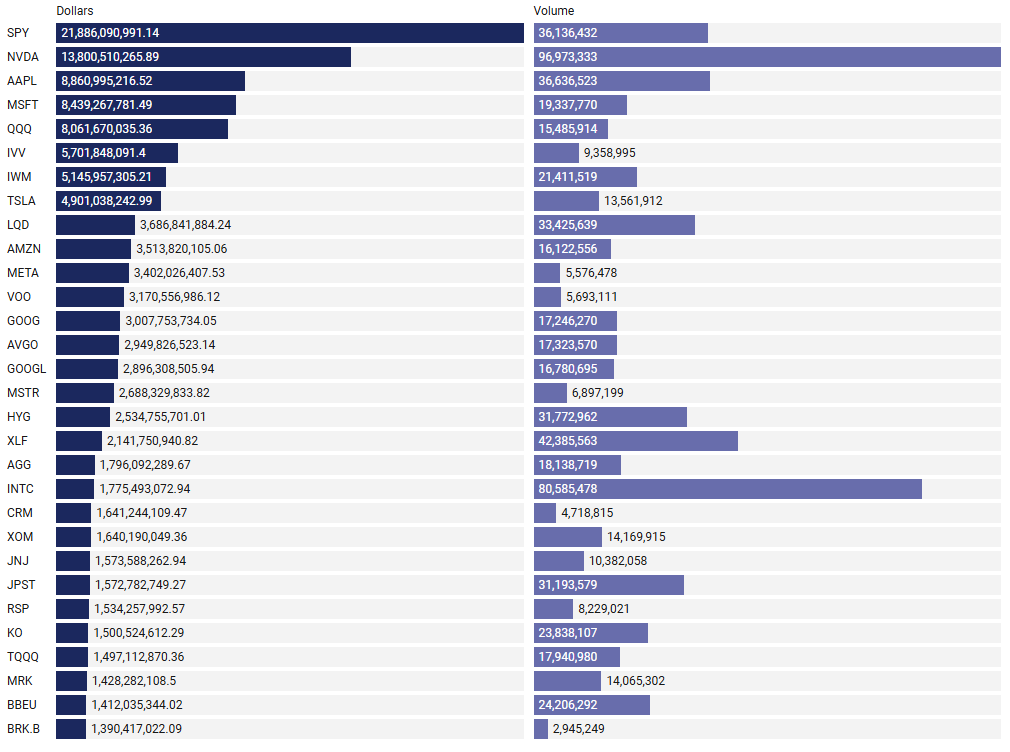

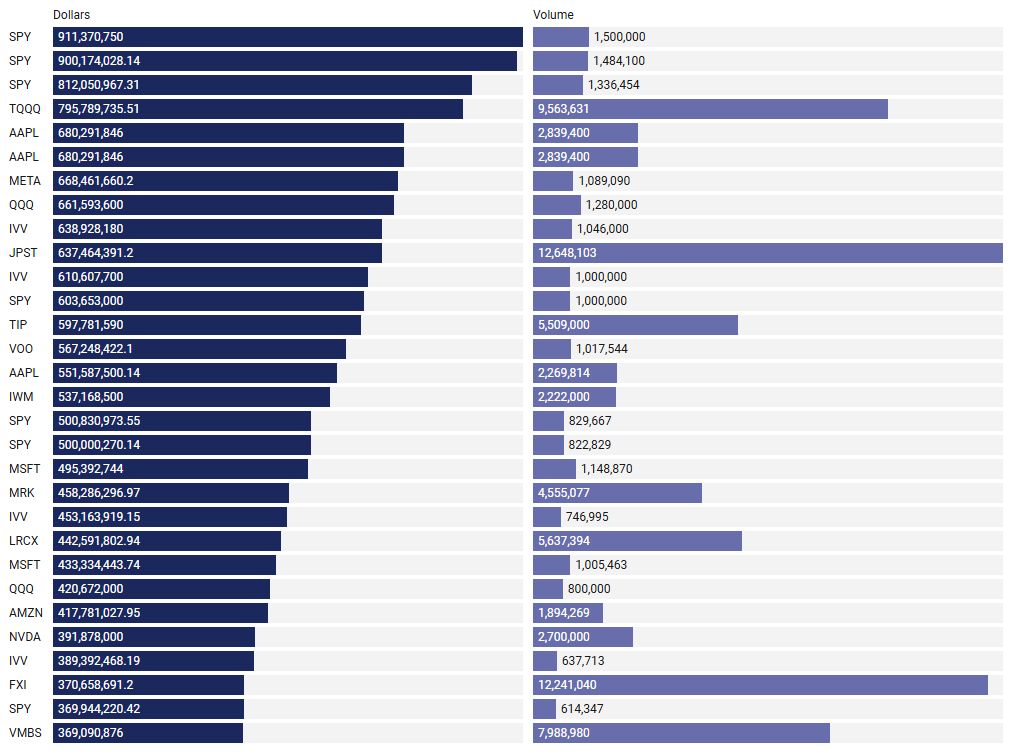

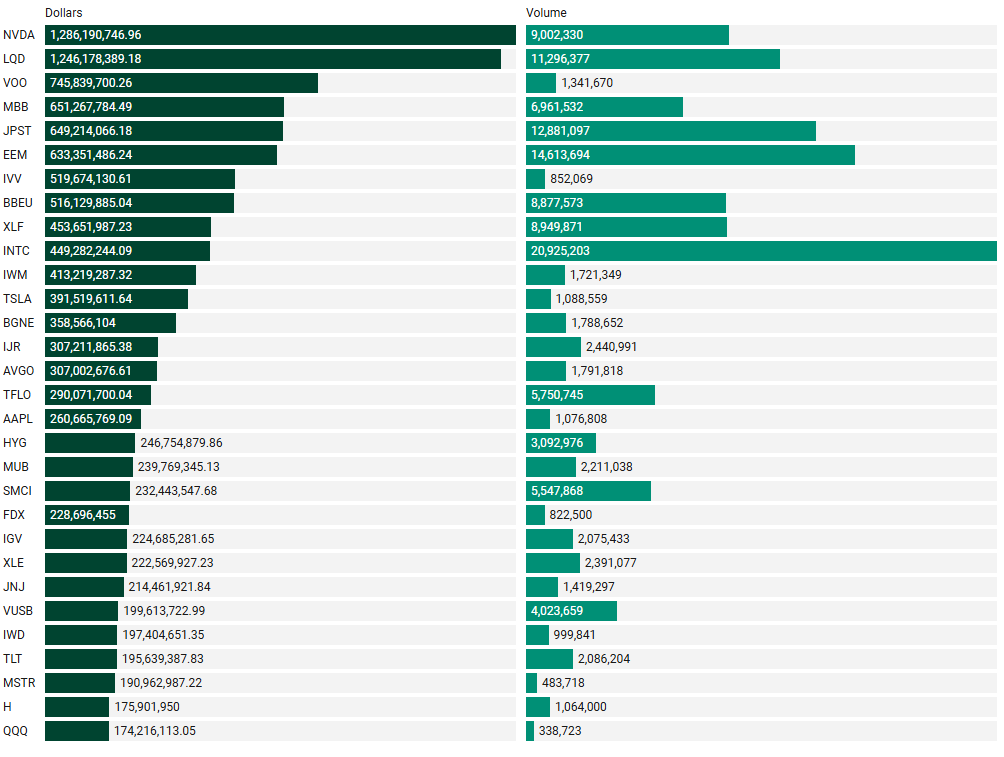

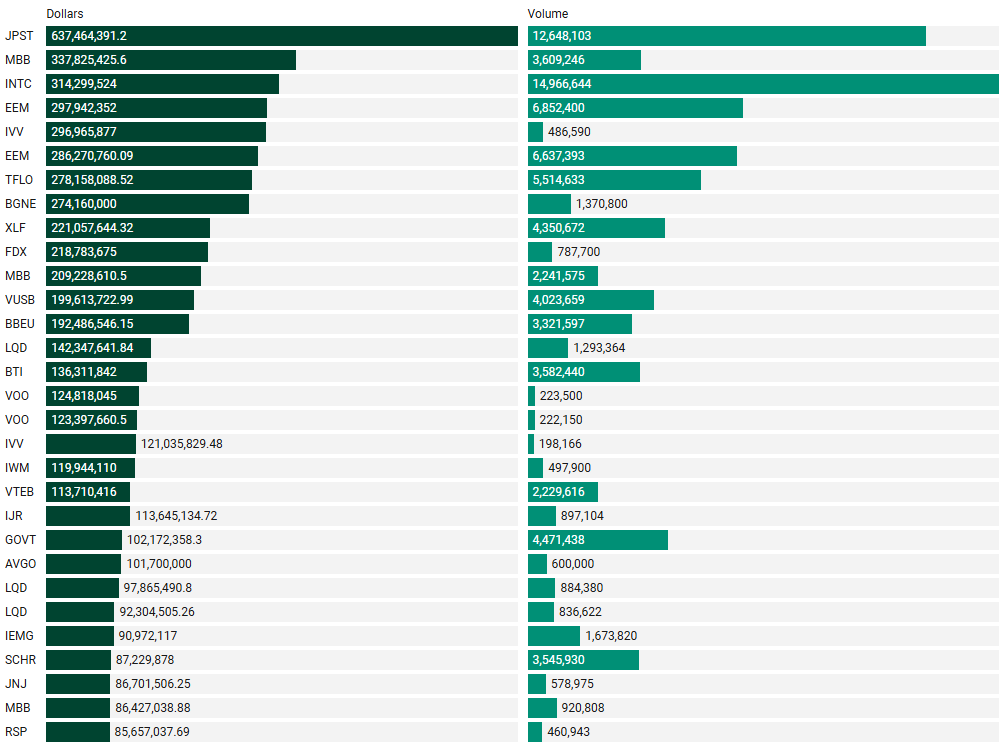

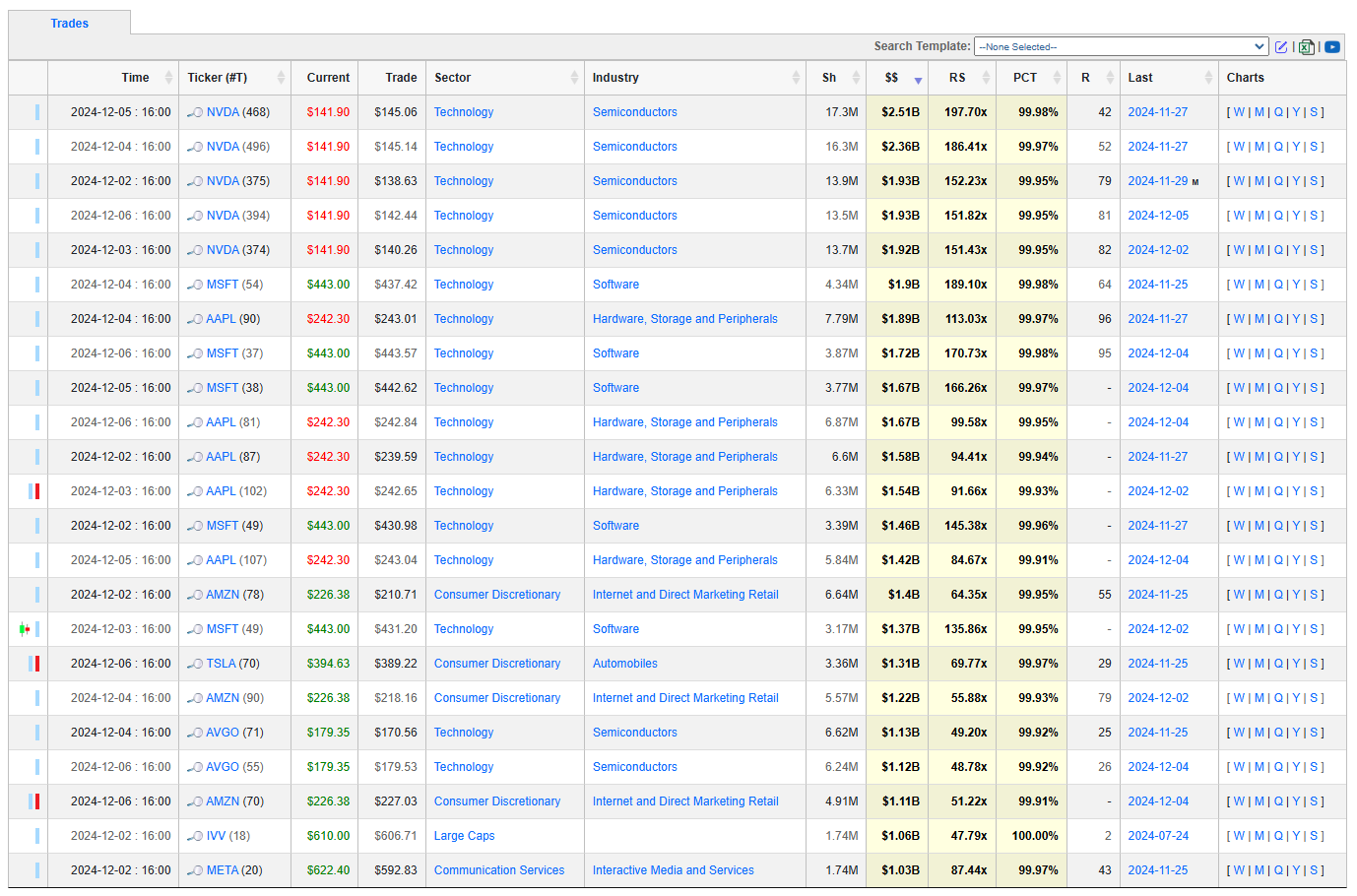

Top Institutional Orderflow In Individual Names

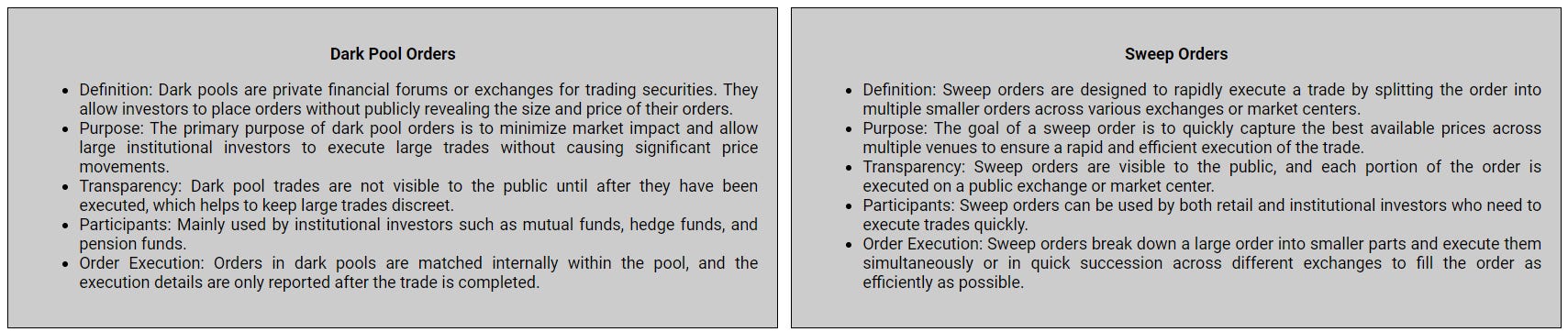

Many excellent trade ideas and sources of inspiration can be found in these prints. While only the top 30 from each group are displayed, the complete results are accessible in VolumeLeaders.com for you to explore at your convenience any time. Remember to configure trade alerts within the platform to ensure you never overlook institutional order flows that capture your interest or are significant to you. The blue charts encompass all types of trades, including blocks on lit exchanges; the purple charts exclusively depict dark pool trades; and the green charts represent sweeps only.

Top Aggregate Dollars Transacted by Ticker

Largest Individual Trades by Dollars Transacted

Top Aggregate Dark Pool Activity by Ticker

Largest Individual Dark Pool Blocks by Dollars

Top Aggregate Sweeps by Ticker

Top Individual Sweeps by Dollars Transacted

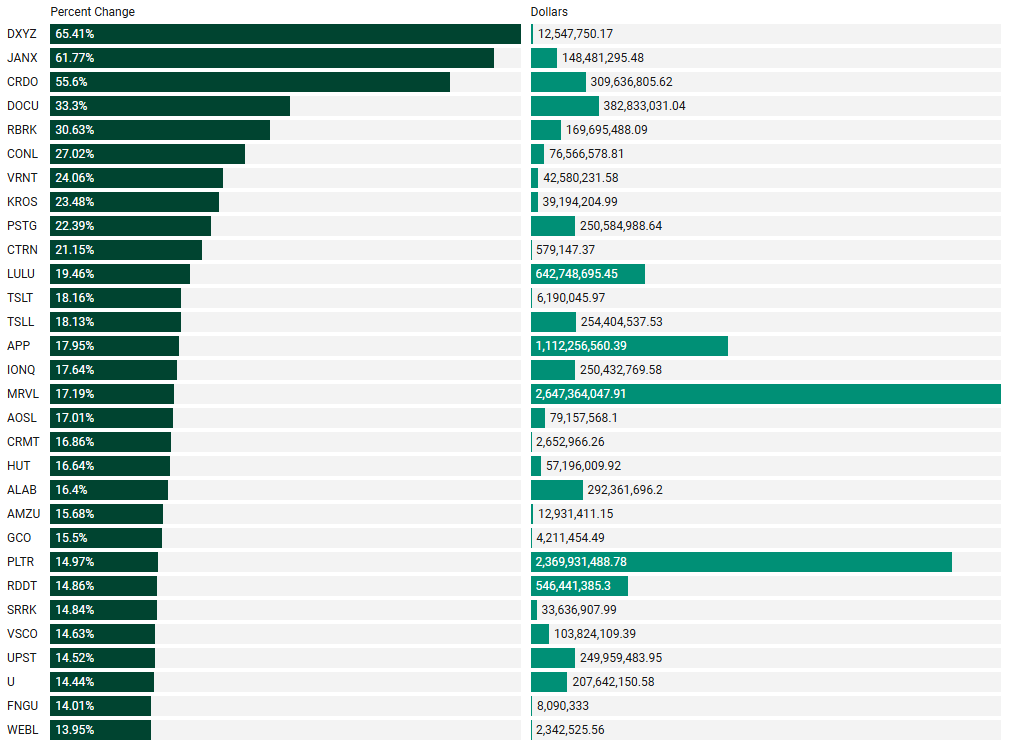

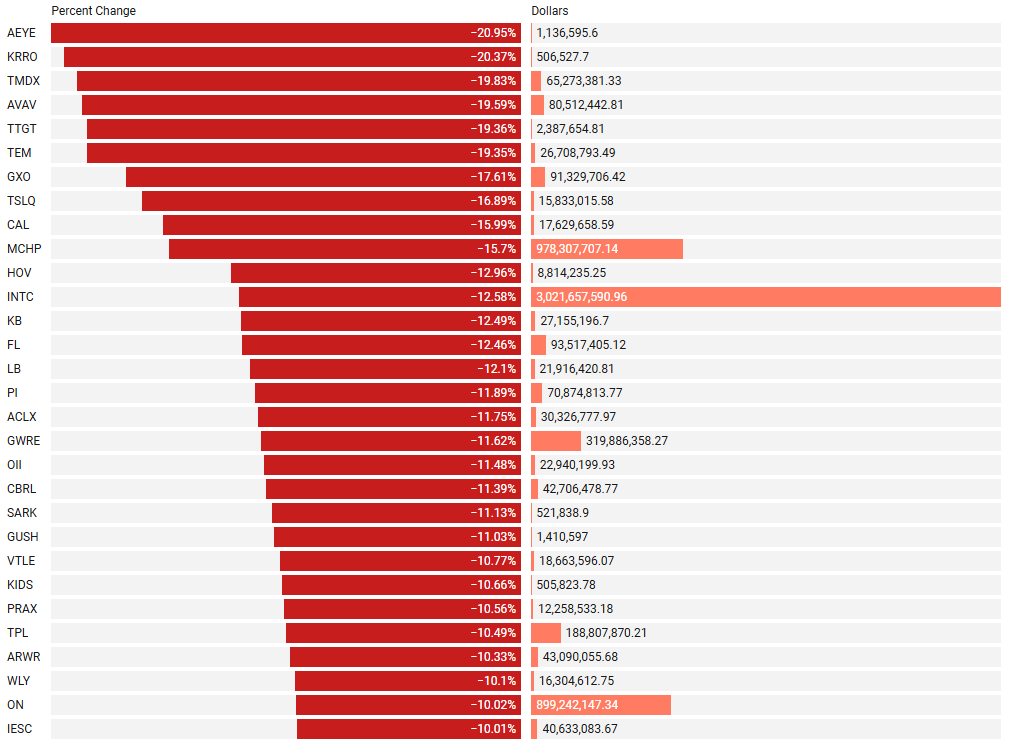

Last Week’s Institutionally-Backed Gainers & Losers

If you’re going to bet on a name, consider one that is officially endorsed by an institution! These are the top percent gainers (green) and percent losers (red) from this week’s open-to-close that had a trade price greater than $20 and institutional involvement. Continue watching tickers from this and prior stacks as these names frequently turn into multi-leg trades with a lot of movement!

Top Institutionally Backed Gainers

Top Institutionally Backed Losers

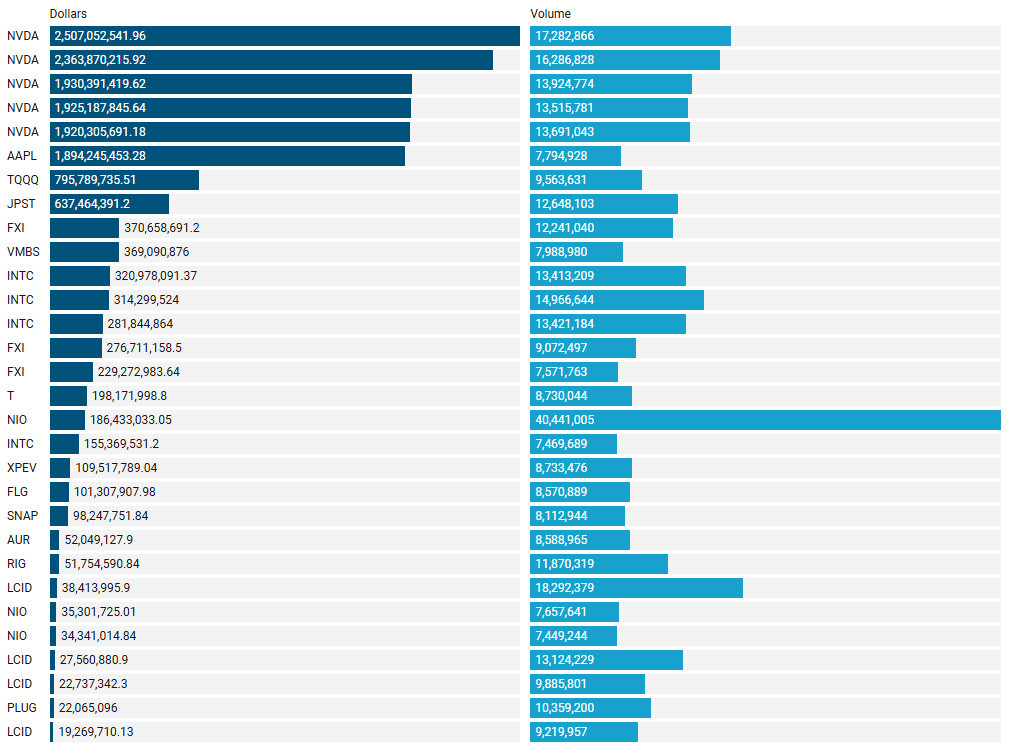

Last Week’s Billion-Dollar Prints

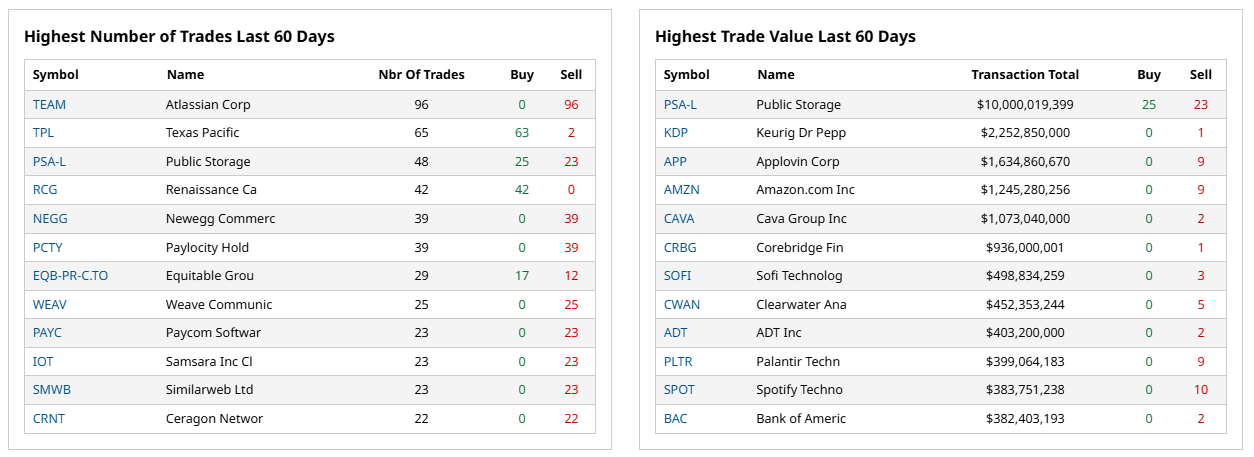

Tickers that printed a trade worth at least $1B last week get a special shout-out… Welcome to the club. Subs should login to VolumeLeaders.com to get the exact trade price and relevant institutional levels around the trade - these are massive commitments by institutions that should not be ignored.

Investments In Focus: Bull vs Bear Arguments

Please read “Institutional S/R Levels For Major Indices” at the top of this stack to understand the nature and importance of what we’re looking at here visually. Institutions leave footprints that VolumeLeaders.com can illustrate for you while providing context to assess things like institutional conviction and urgency. Theses and data given below are not financial advice, just personal observations that may be wrong; consult a certified financial advisor before making any investment decisions.

FDX 0.00%↑

Bull Thesis for FedEx Corporation (FDX):

Operational Consolidation: FedEx is integrating its Express, Ground, and Services divisions into a unified entity by June 2024, aiming for $4 billion in cost savings and enhanced operational efficiency.

Financial Performance: In fiscal 2024, FedEx reported a diluted EPS of $17.21 and adjusted diluted EPS of $17.80, reflecting strong profitability.

Shareholder Returns: The company returned $3.8 billion to shareholders through stock repurchases and dividends during fiscal 2024, demonstrating a commitment to shareholder value.

Technological Advancements: FedEx is investing in technology to optimize supply chains and enhance service predictability, positioning itself competitively in the logistics industry.

Market Position: Despite increased competition, FedEx maintains a strong market presence and is actively pursuing small business customers through competitive pricing strategies.

Bear Thesis for FedEx Corporation (FDX):

Analyst Downgrade: Bernstein downgraded FedEx from 'Buy' to 'Hold', citing execution risks in integrating its delivery networks and potential policy threats, leading to a stock price decline.

Competitive Pricing Pressures: FedEx and UPS are engaged in a price war to attract small business customers, which could compress profit margins.

Operational Challenges: The consolidation of operating companies involves execution risks, and any missteps could disrupt services and erode customer trust.

Market Competition: Amazon's delivery network has surpassed FedEx in package volume, intensifying competition in the logistics sector.

Economic Sensitivity: FedEx's performance is sensitive to global economic conditions, and downturns can lead to reduced shipping volumes and revenue.

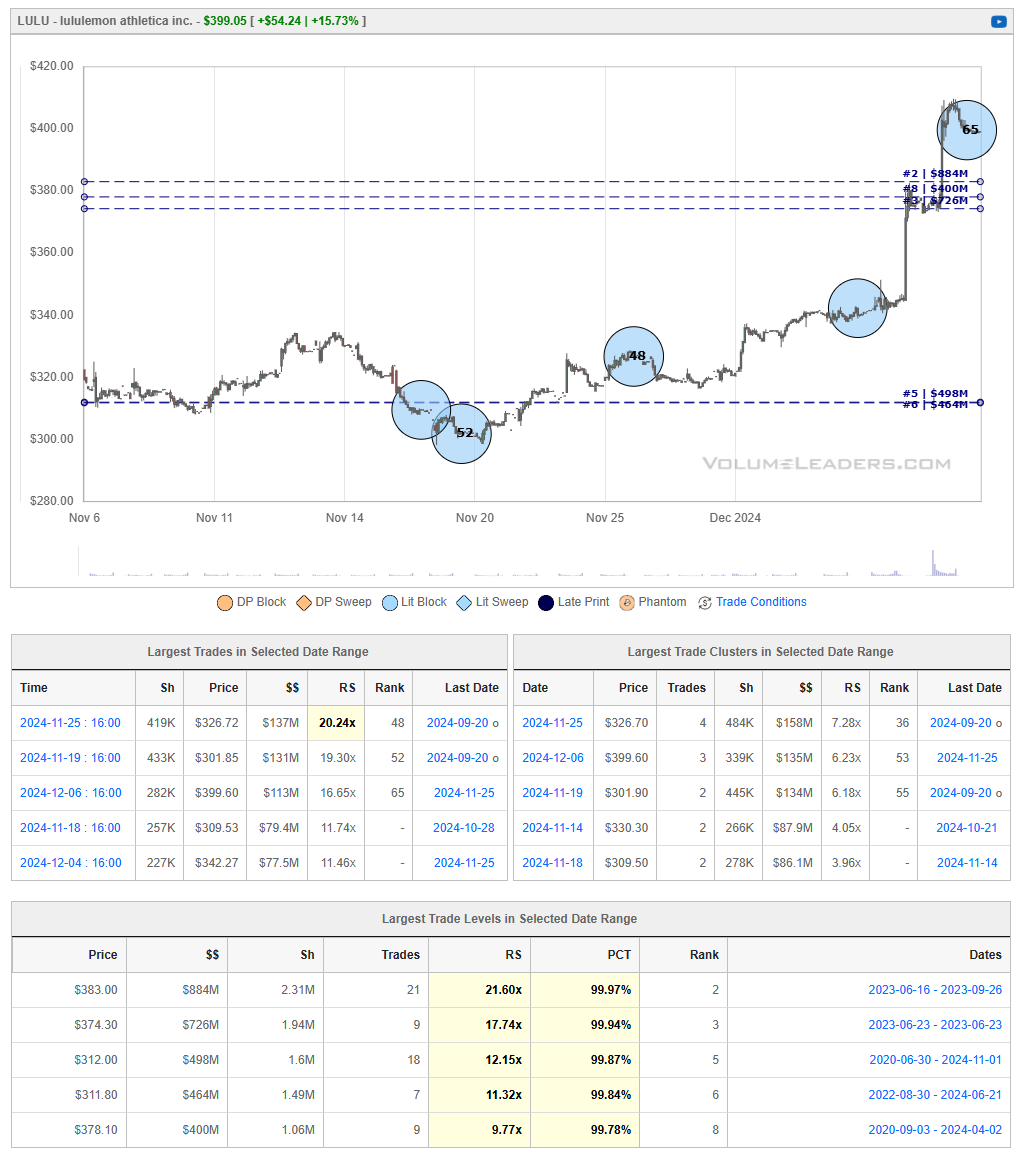

LULU 0.00%↑

Bull Thesis for Lululemon Athletica Inc. (LULU):

Robust Financial Performance: In Q3 2024, Lululemon reported a 9% year-over-year increase in net revenue, reaching $2.4 billion, surpassing analyst expectations.

Positive Earnings Outlook: The company raised its full-year revenue forecast to a range of $10.452 billion to $10.487 billion, with an earnings projection between $14.08 and $14.16 per share, indicating confidence in sustained growth.

International Market Expansion: Lululemon's international revenue grew by 33% in Q3, with a notable 36% increase in China, highlighting successful global expansion strategies.

Product Innovation and Appeal: The brand's updated clothing styles and effective marketing have attracted younger consumers, contributing to strong sales and market presence.

Analyst Confidence: Following strong earnings, multiple analysts raised their price targets for Lululemon, reflecting a positive outlook on the company's future performance.

Bear Thesis for Lululemon Athletica Inc. (LULU):

Declining U.S. Same-Store Sales: In Q3, Lululemon experienced a 2% decline in same-store sales within the U.S., raising concerns about domestic market saturation and competition.

Increased Competition: The rise of new athletic apparel brands like Vuori and Alo presents competitive challenges, potentially impacting Lululemon's market share and pricing power.

Dependence on International Markets: With significant growth driven by international sales, particularly in China, Lululemon faces risks related to geopolitical tensions and foreign market dynamics.

Stock Volatility: Despite recent gains, Lululemon's stock has experienced significant fluctuations, including a 33% decline earlier in the year, indicating potential instability.

Supply Chain Challenges: Global supply chain disruptions could affect product availability and increase costs, potentially impacting profit margins and customer satisfaction.

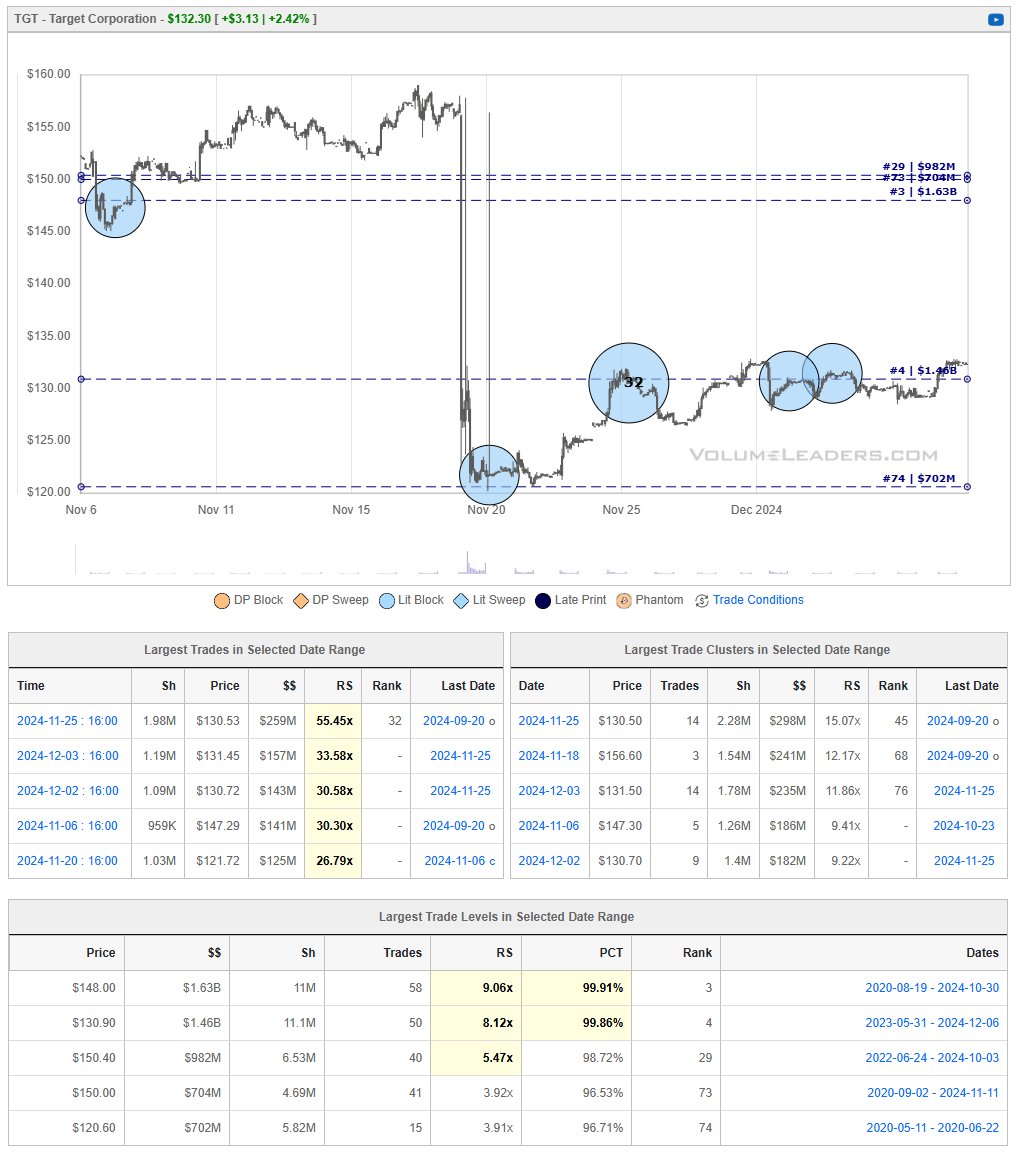

TGT 0.00%↑

Bull Thesis for Target Corporation (TGT):

Exclusive Partnerships: Target's collaboration with high-profile artists, such as the exclusive release of Taylor Swift's "The Eras Tour Book," enhances brand appeal and attracts dedicated customer segments.

Digital Sales Growth: Despite challenges in physical store sales, Target reported a 10.8% increase in digital transactions, indicating successful e-commerce strategies and adaptation to changing consumer behaviors.

Loyalty Program Expansion: The introduction of the Target Circle 360 loyalty program aims to boost customer retention and spending by offering benefits like free same-day delivery, enhancing the overall shopping experience.

Community Engagement: Target's longstanding commitment to community support, including donating 5% of profits, fosters positive public perception and customer loyalty.

Holiday Season Initiatives: Aggressive pricing strategies and exclusive product offerings during the holiday season are designed to drive sales and improve market competitiveness.

Bear Thesis for Target Corporation (TGT):

Earnings Miss and Guidance Cut: In the third quarter, Target's adjusted earnings per share fell to $1.85, missing analyst expectations of $2.30, leading to a 22% stock decline and a reduction in full-year earnings guidance.

Legal Challenges: A U.S. judge ruled that Target must face a shareholder lawsuit alleging the company misled investors about risks associated with its LGBTQ-themed merchandise, potentially leading to financial and reputational repercussions.

Customer Experience Issues: Reports of long wait times due to anti-theft policies, such as locking essential items behind glass, have frustrated customers, potentially driving them to competitors like Amazon.

Competitive Disadvantages: Competitors like Walmart and Costco have outperformed Target by effectively integrating e-commerce and offering lower grocery prices, attracting budget-conscious consumers and impacting Target's market share.

Stock Performance Decline: Target's stock has declined approximately 15% in 2024, underperforming competitors and reflecting investor concerns about the company's strategic direction and financial health.

ALT 0.00%↑

Bull Thesis for Altimmune, Inc. (ALT):

Advancement in Clinical Trials: Altimmune has successfully completed enrollment in its Phase 2b IMPACT trial for pemvidutide, targeting metabolic dysfunction-associated steatohepatitis (MASH), with top-line efficacy data expected in Q2 2025.

Positive Financial Indicators: Over the past six months, ALT stock has risen by 34.93%, indicating growing investor confidence in the company's prospects.

Strategic Leadership Appointments: The company appointed Greg Weaver as Chief Financial Officer in November 2024, bringing extensive experience to strengthen financial operations.

Pipeline Diversification: Altimmune plans to submit Investigational New Drug (IND) applications for pemvidutide in up to three additional indications beginning in Q4 2024, expanding its therapeutic reach.

Recognition in Scientific Community: The company presented new data on the lipidomic profile in subjects treated with pemvidutide at the 17th International Conference of the Society on Sarcopenia, Cachexia & Wasting Disorders, highlighting its commitment to advancing scientific knowledge.

Bear Thesis for Altimmune, Inc. (ALT):

Stock Volatility: ALT stock has experienced significant fluctuations, with a 16.84% change over the last five trading sessions, indicating potential instability.

Unusual Options Activity: Recent bearish options activity suggests that some investors anticipate a decline in ALT's stock price, reflecting market skepticism.

Clinical Development Risks: As a clinical-stage biopharmaceutical company, Altimmune's success heavily depends on the outcomes of its clinical trials, which carry inherent uncertainties.

Financial Losses: The company reported a net loss of $103.52 million over the trailing twelve months, which may raise concerns about its financial sustainability.

Market Competition: Altimmune operates in a highly competitive biopharmaceutical sector, facing challenges from companies with more established products and greater resources.

FIS 0.00%↑

Bull Thesis for Fidelity National Information Services, Inc. (FIS):

Strategic Divestitures: FIS has announced plans to spin off its Merchant Solutions business, Worldpay, by early 2025, aiming to enhance shareholder value and focus on core operations.

Cost Management Initiatives: The company is implementing a comprehensive cost-cutting program targeting $1.25 billion in savings, which is expected to improve profitability.

Market Position: As a leading provider of financial technology solutions, FIS serves a diverse client base, including banks, capital markets, and merchants, positioning it well to capitalize on industry growth.

Product Innovation: FIS continues to invest in innovative solutions, such as its Modern Banking Platform, to meet evolving customer demands and maintain a competitive edge.

Dividend Commitment: The company has a history of returning capital to shareholders through dividends, reflecting financial stability and a commitment to shareholder value.

Bear Thesis for Fidelity National Information Services, Inc. (FIS):

Leadership Transition: The recent nomination of CEO Frank Bisignano to lead the Social Security Administration introduces uncertainty regarding future leadership and strategic direction.

Stock Underperformance: FIS shares have experienced volatility, with a slight year-to-date increase of 0.42%, underperforming broader market indices.

Analyst Downgrade: Bank of America removed FIS from its "US 1 List," indicating reduced confidence in the stock's near-term performance.

Competitive Pressures: The financial technology sector is highly competitive, with FIS facing challenges from both established firms and emerging fintech companies, which could impact market share and margins.

Client Concentration Risks: Dependence on a limited number of large clients for a significant portion of revenue exposes FIS to potential financial instability if key clients reduce or terminate their engagements.

TSM -0.11%↓

Bull Thesis for Taiwan Semiconductor Manufacturing Company (TSMC):

Robust Financial Performance: In Q3 2024, TSMC reported a 54.2% year-over-year increase in net income, reaching NT$325.3 billion ($10.2 billion), surpassing analysts’ expectations.

Strategic U.S. Expansion: TSMC is set to receive up to $6.6 billion in CHIPS Act funding to support its investment in three new semiconductor fabrication plants in Phoenix, Arizona, enhancing its global footprint and aligning with U.S. supply chain initiatives.

Advanced Technology Leadership: The company leads in advanced semiconductor manufacturing, with 69% of its Q3 revenue derived from 7nm or smaller chips, positioning it at the forefront of technological innovation.

Strong Client Relationships: TSMC's clientele includes major tech firms like Apple, Nvidia, and AMD, ensuring consistent demand for its cutting-edge manufacturing capabilities.

Positive Analyst Outlook: Analysts forecast TSMC's earnings to grow by 32% this year, with a 30% increase in 2025, reflecting confidence in the company's growth trajectory.

Bear Thesis for Taiwan Semiconductor Manufacturing Company (TSMC):

Geopolitical Risks: TSMC's operations are significantly exposed to geopolitical tensions, particularly between the U.S. and China, which could impact its supply chain and market access.

Supply Chain Challenges: The necessity to ship U.S.-manufactured chips back to Taiwan for packaging introduces logistical complexities and potential delays.

High Capital Expenditure: The substantial investment of $65 billion in new U.S. facilities represents a significant financial commitment, with returns dependent on successful project execution and market conditions.

Market Competition: The semiconductor industry is highly competitive, with TSMC facing challenges from other leading manufacturers, which could pressure margins and market share.

Economic Sensitivity: TSMC's performance is sensitive to global economic cycles, with downturns potentially leading to reduced demand for semiconductors and impacting revenue.

GFS 0.00%↑

Bull Thesis for GlobalFoundries Inc. (GFS):

Strategic Partnerships: GlobalFoundries has partnered with Soitec to supply 300mm RF-SOI wafers for its 9SW radio platform, enhancing its capabilities in producing next-generation 5G and Wi-Fi chips.

Government Funding: The company received a $1.5 billion grant from the U.S. Commerce Department to expand semiconductor production in New York and Vermont, supporting its $13 billion investment plan over the next decade.

Technological Advancements: GlobalFoundries is advancing GaN chip manufacturing with an additional $9.5 million in federal funding, aiming for large-scale production of GaN on silicon semiconductors.

Global Expansion: The company opened a $4 billion fabrication facility in Singapore, creating 1,000 new jobs and bolstering its global manufacturing footprint across Singapore, the U.S., and Europe.

Industry Recognition: GlobalFoundries was selected to host a national technology center in Albany, New York, receiving up to $825 million in federal funding to enhance U.S. competitiveness in the semiconductor industry.

Bear Thesis for GlobalFoundries Inc. (GFS):

Geopolitical Risks: The semiconductor industry faces geopolitical tensions, particularly between the U.S. and China, which could impact GlobalFoundries' operations and market access.

Market Competition: GlobalFoundries operates in a highly competitive sector, facing challenges from established firms like TSMC and emerging players, potentially affecting its market share.

Supply Chain Challenges: The company may encounter supply chain disruptions due to global events, affecting production schedules and increasing operational costs.

Financial Volatility: GlobalFoundries' stock has experienced fluctuations, with a recent decline of 0.23%, indicating potential instability.

Regulatory Scrutiny: The semiconductor industry is subject to stringent regulations, and any non-compliance could result in legal challenges and financial penalties for GlobalFoundries.

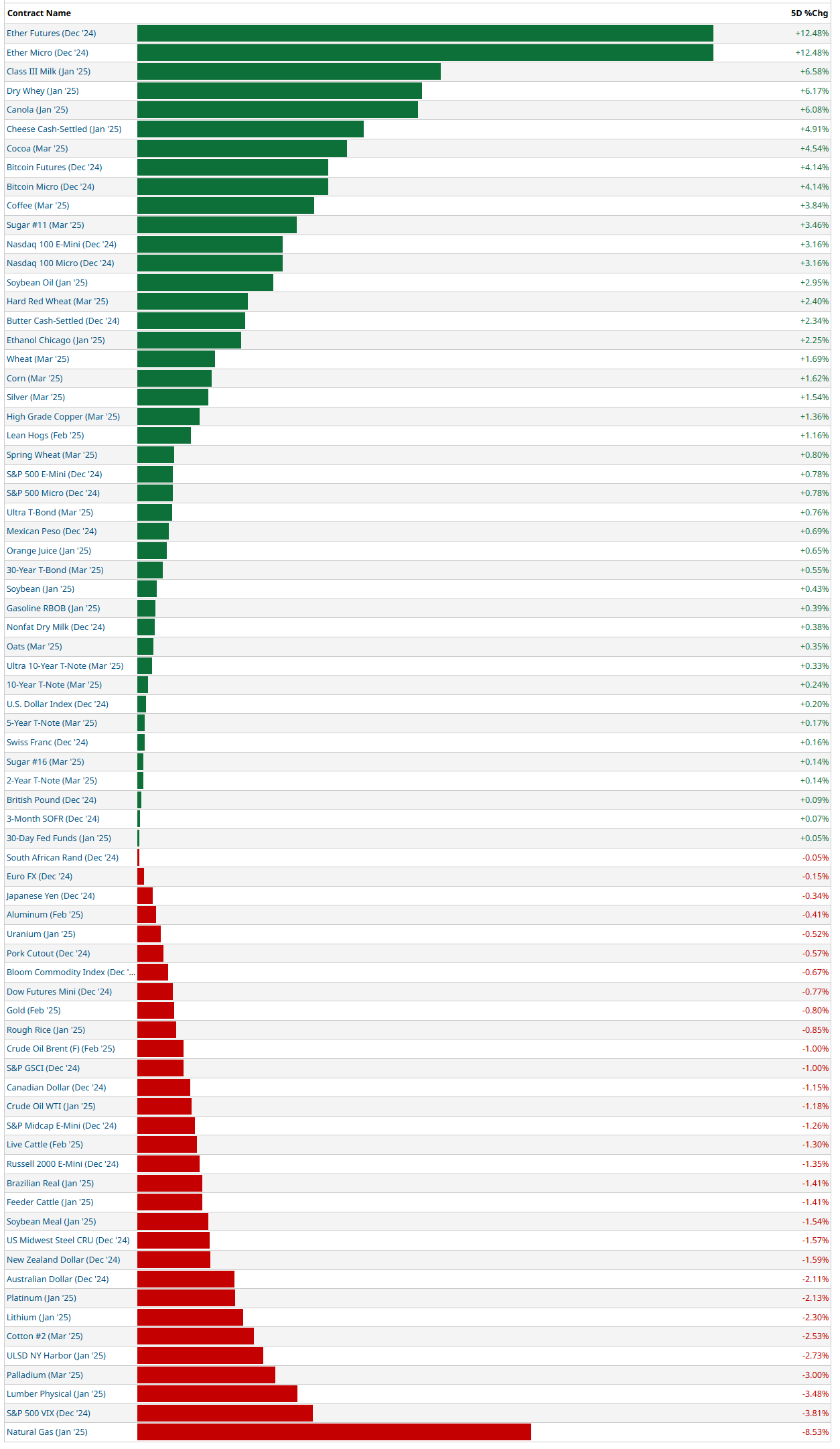

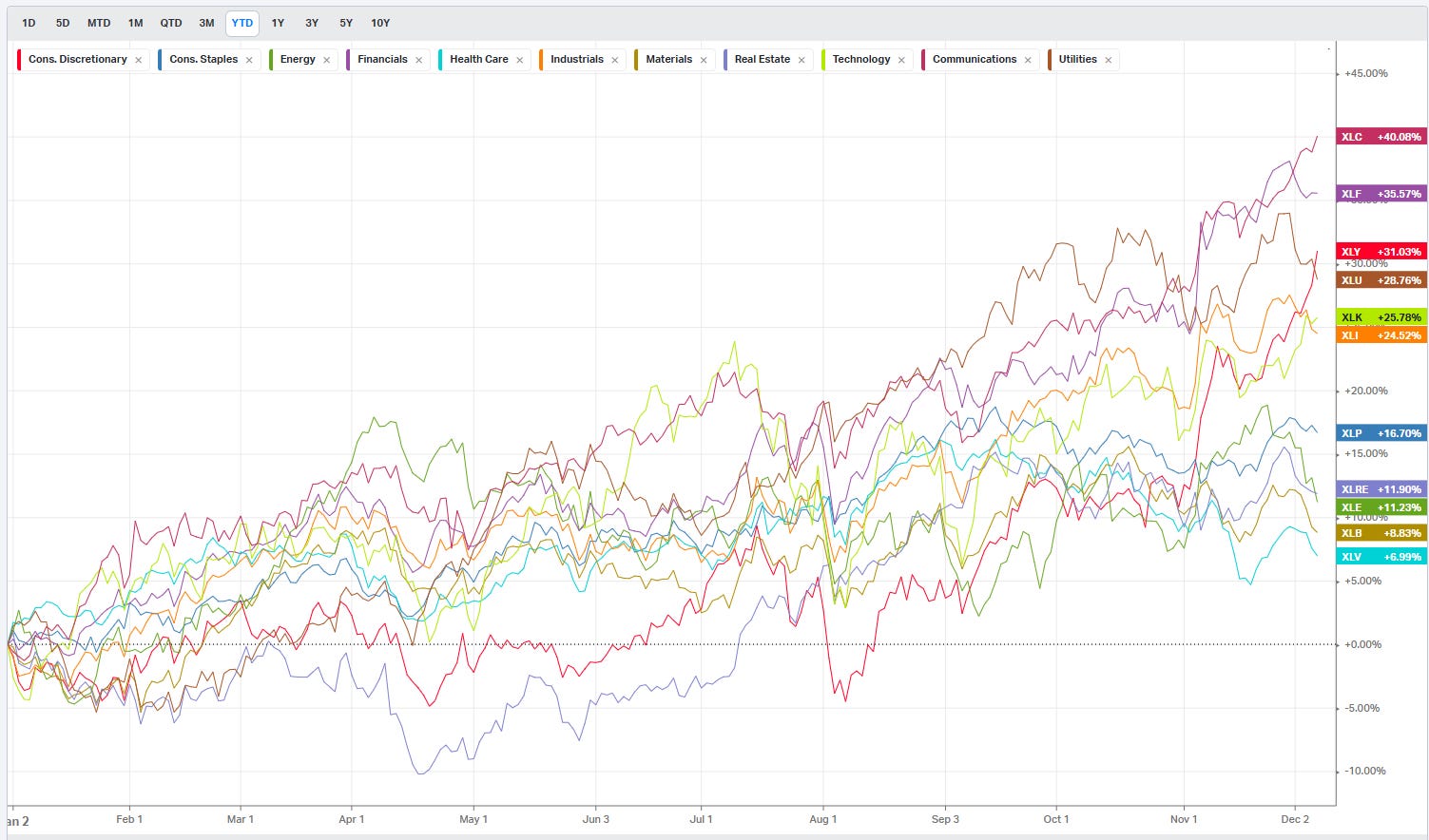

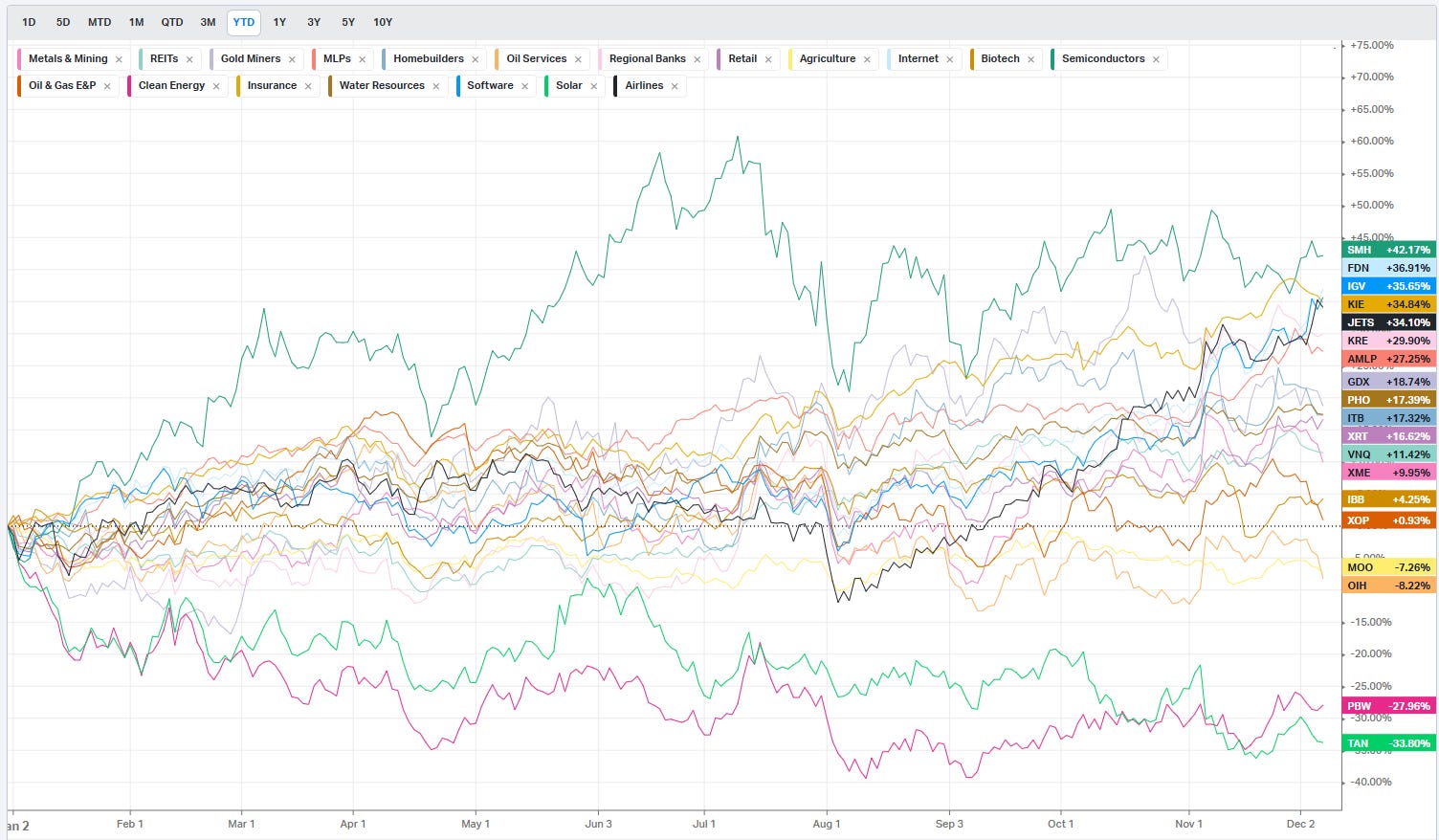

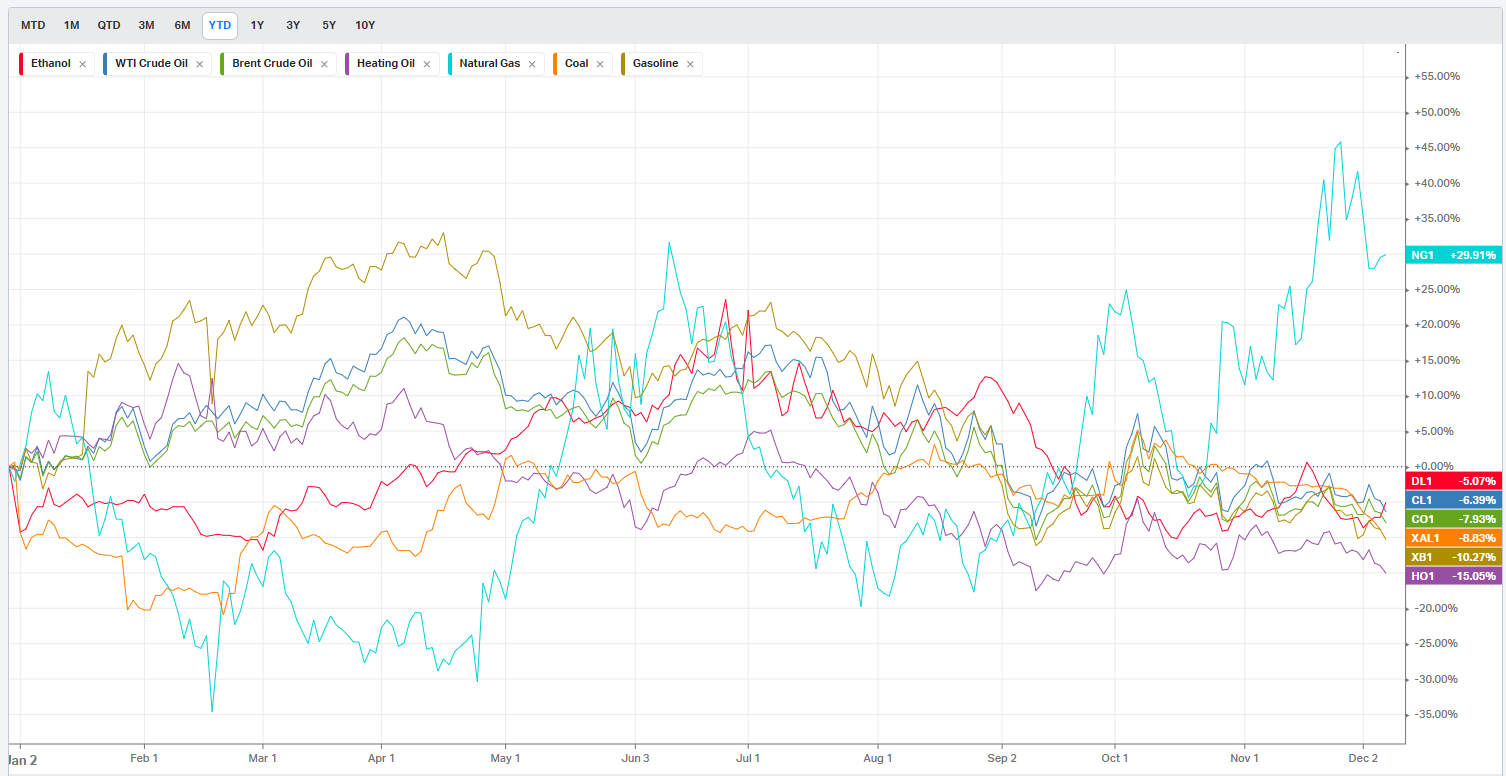

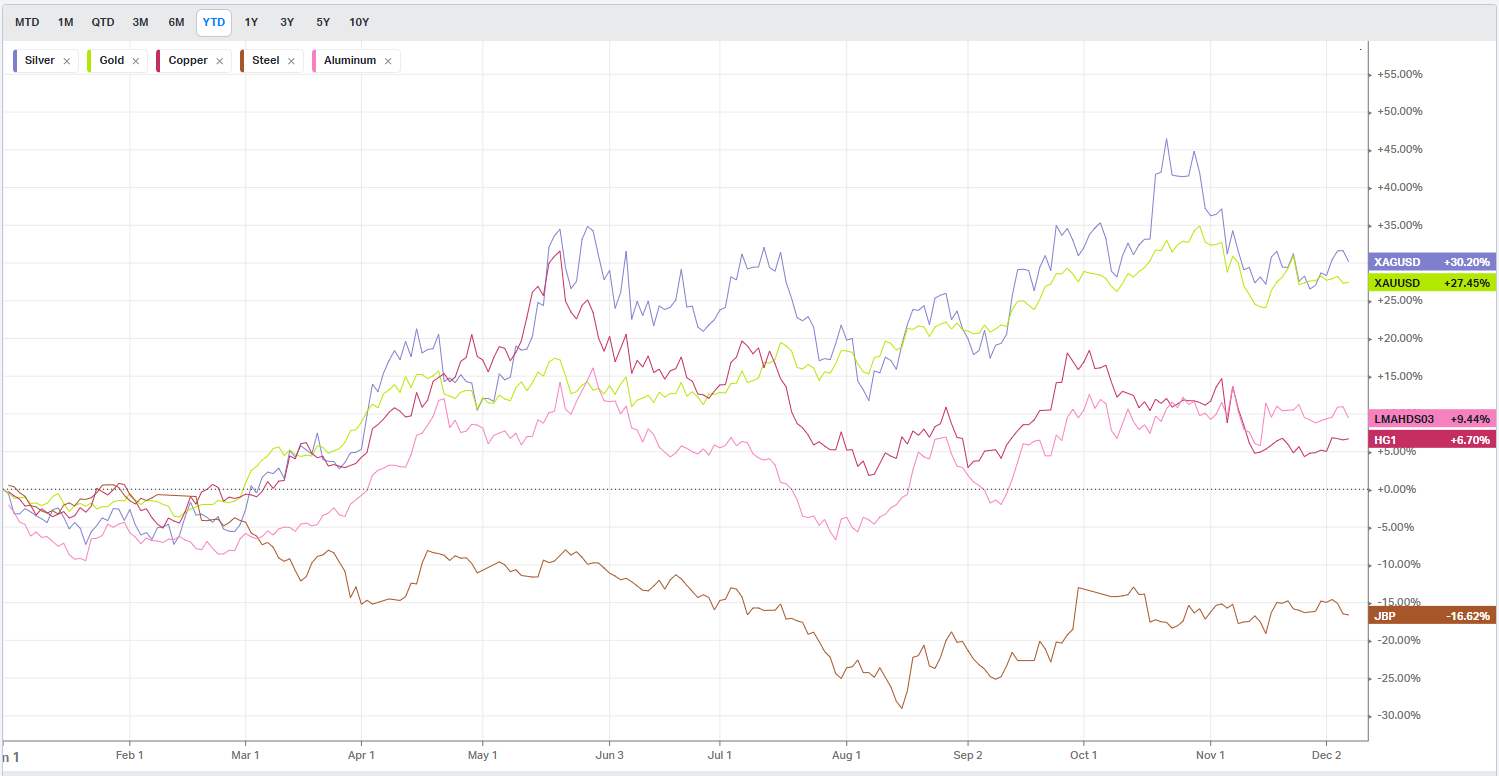

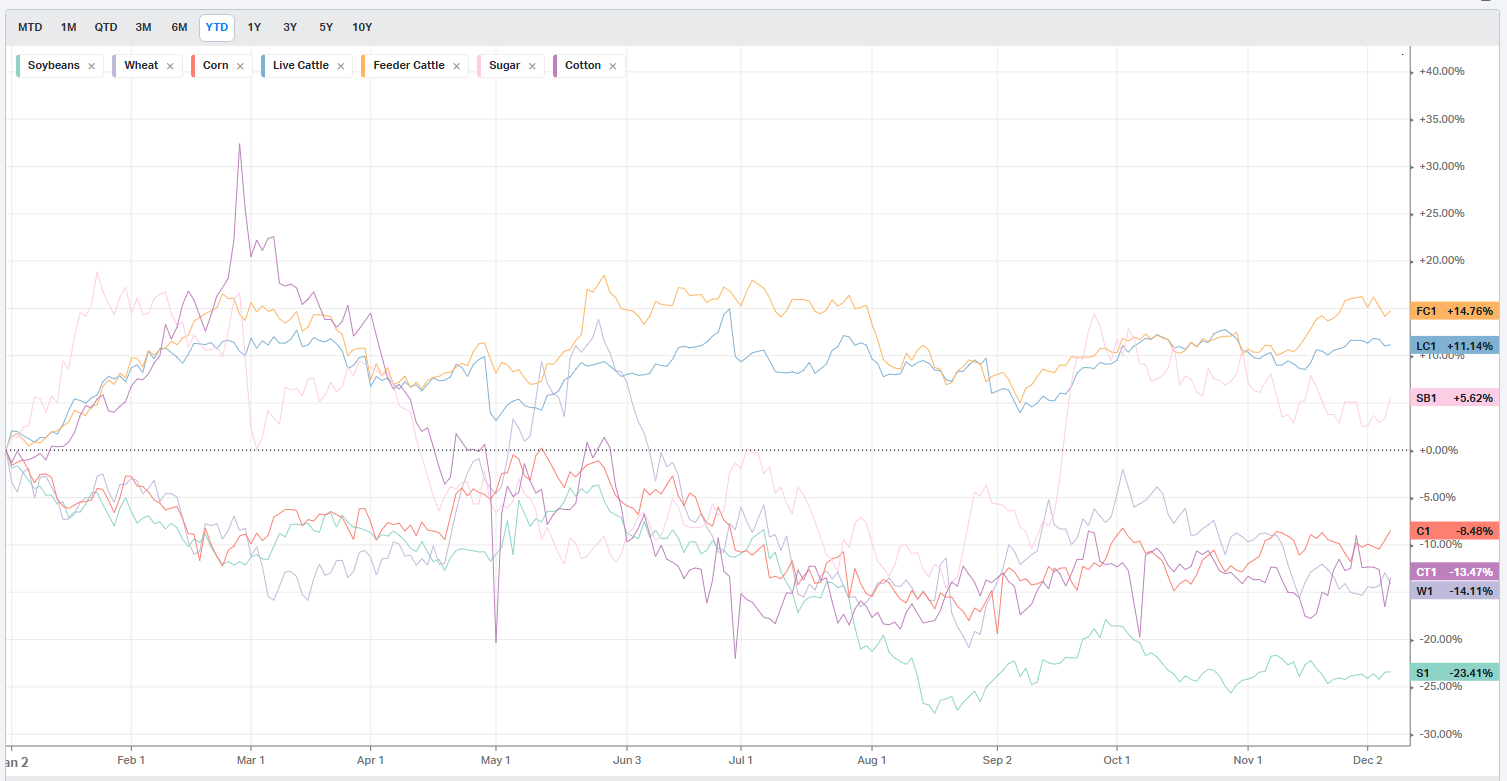

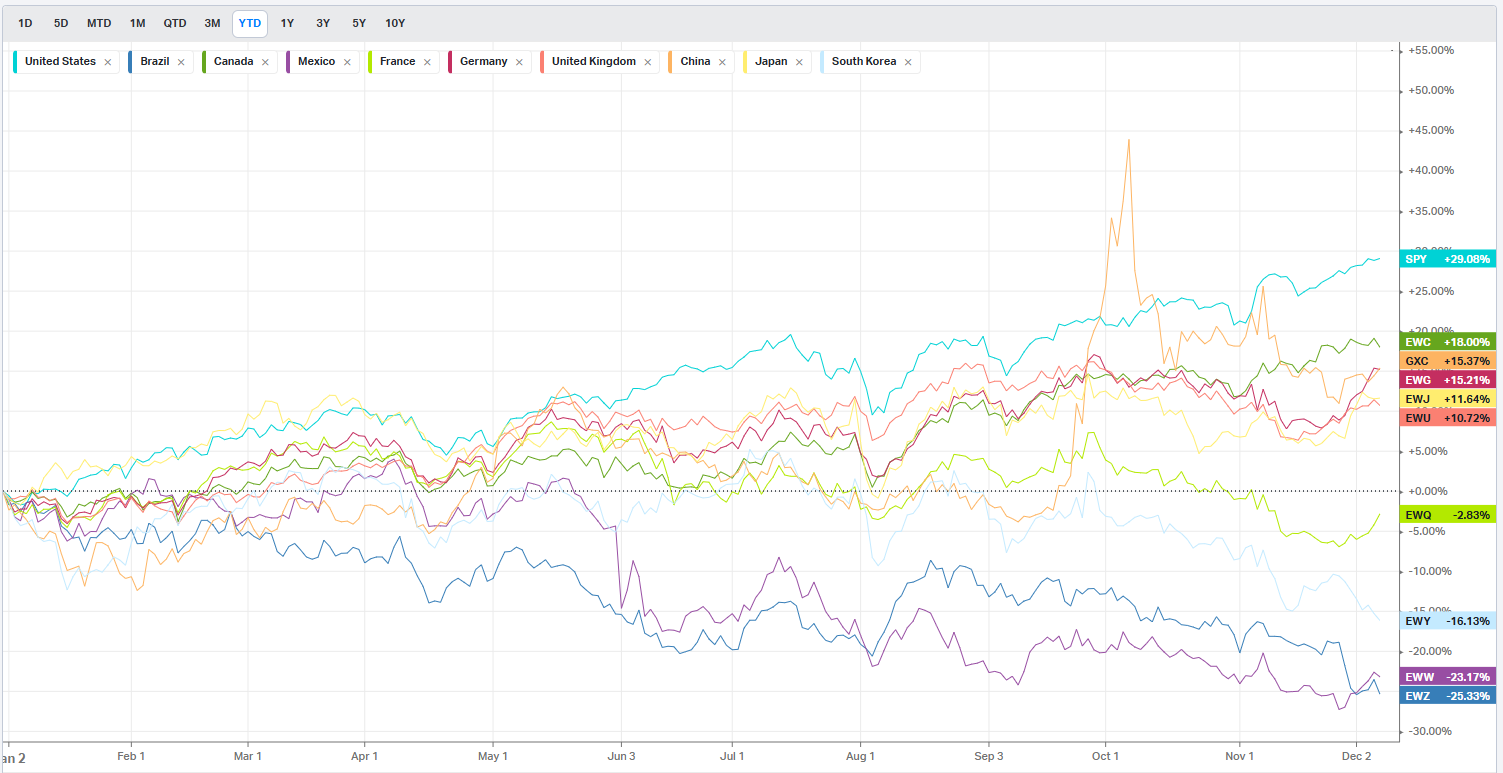

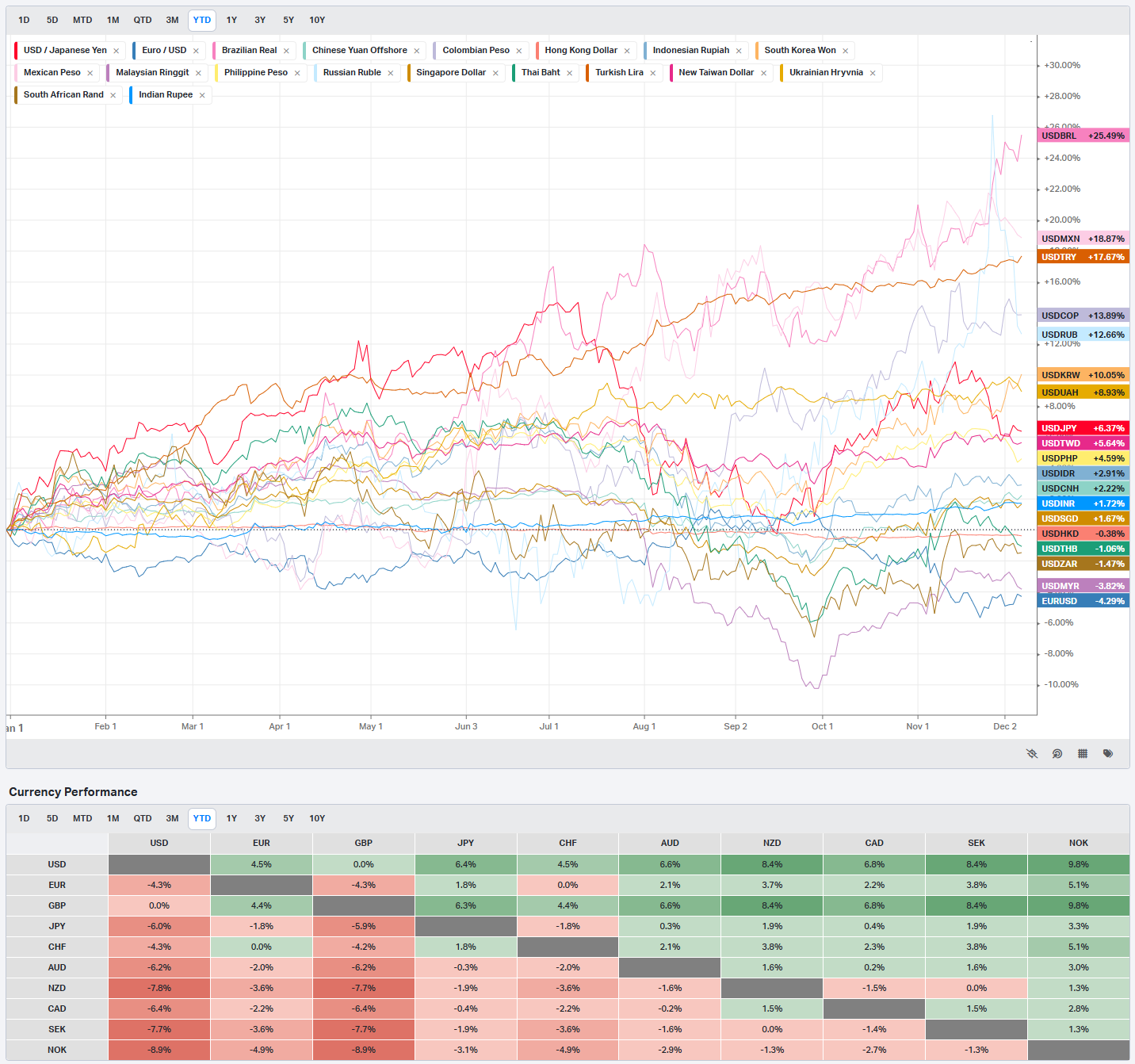

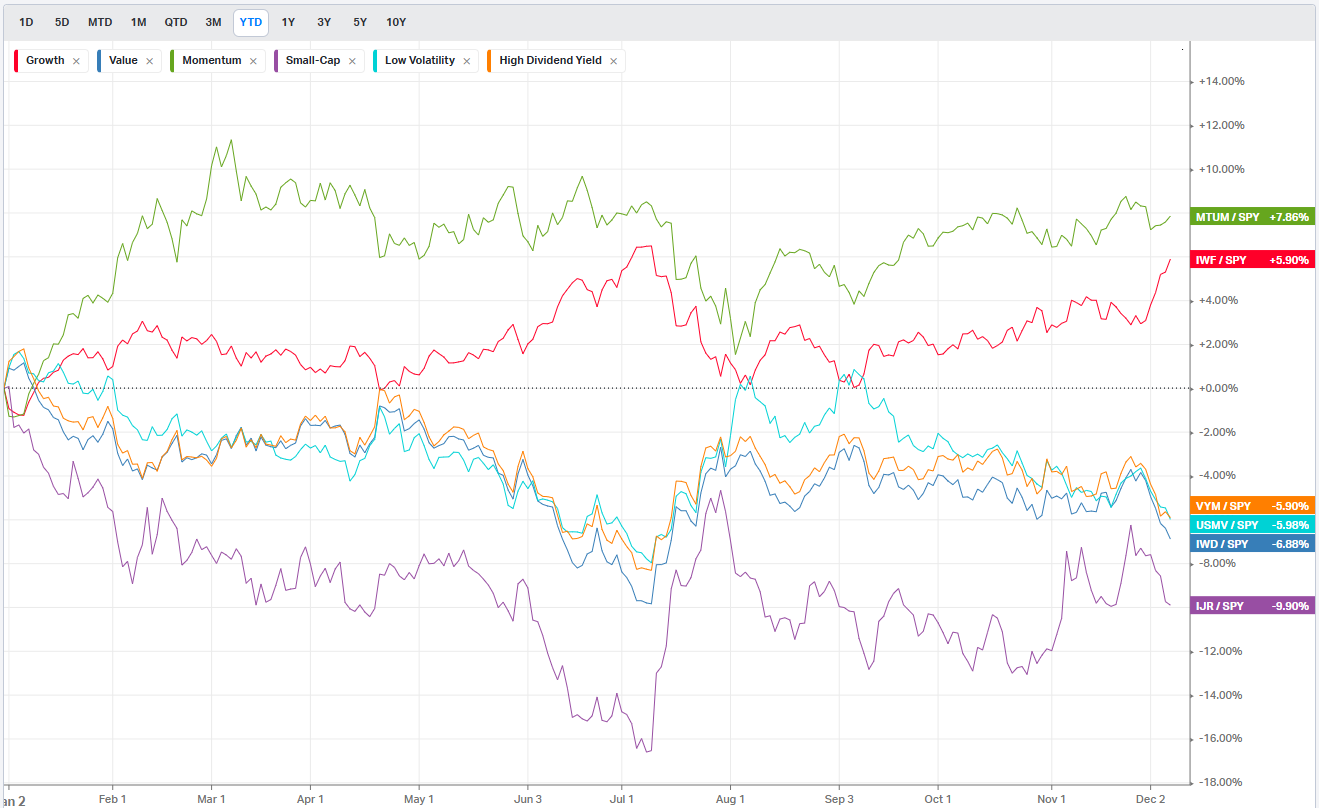

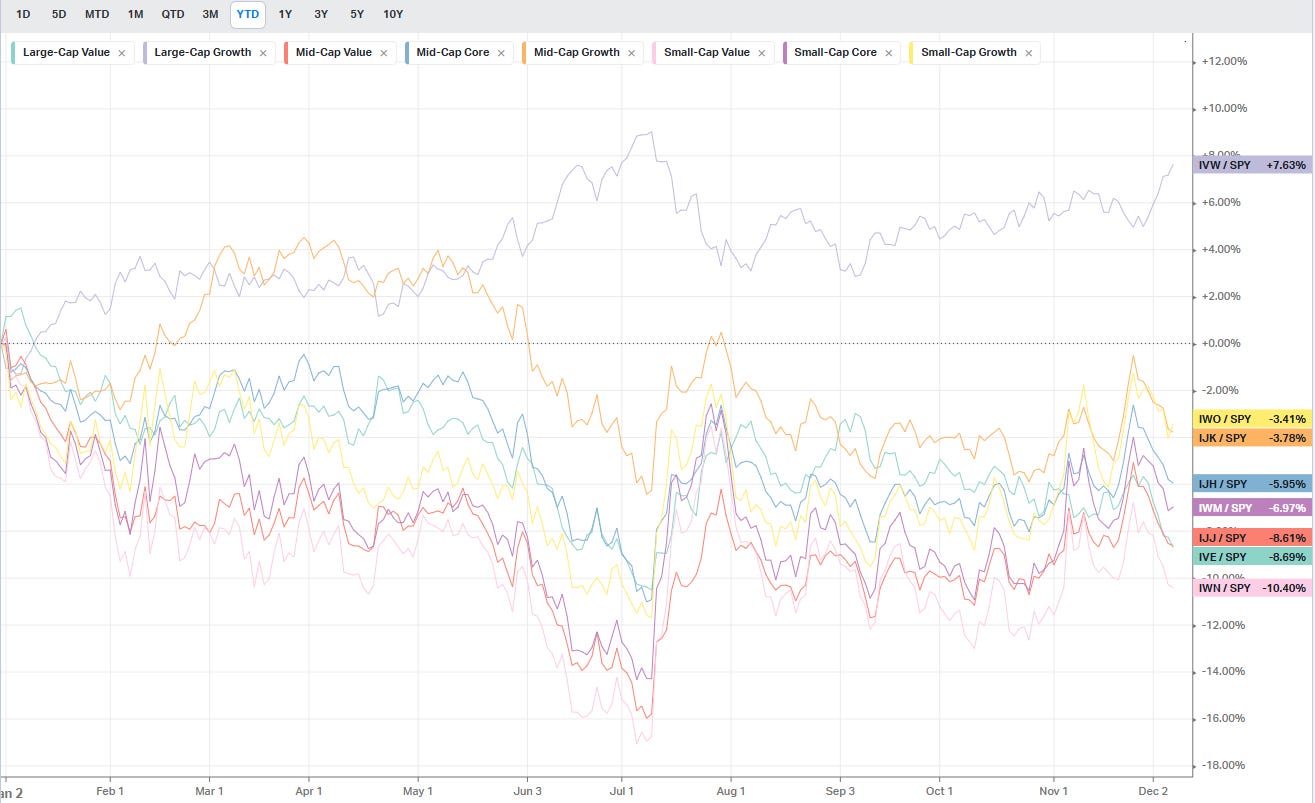

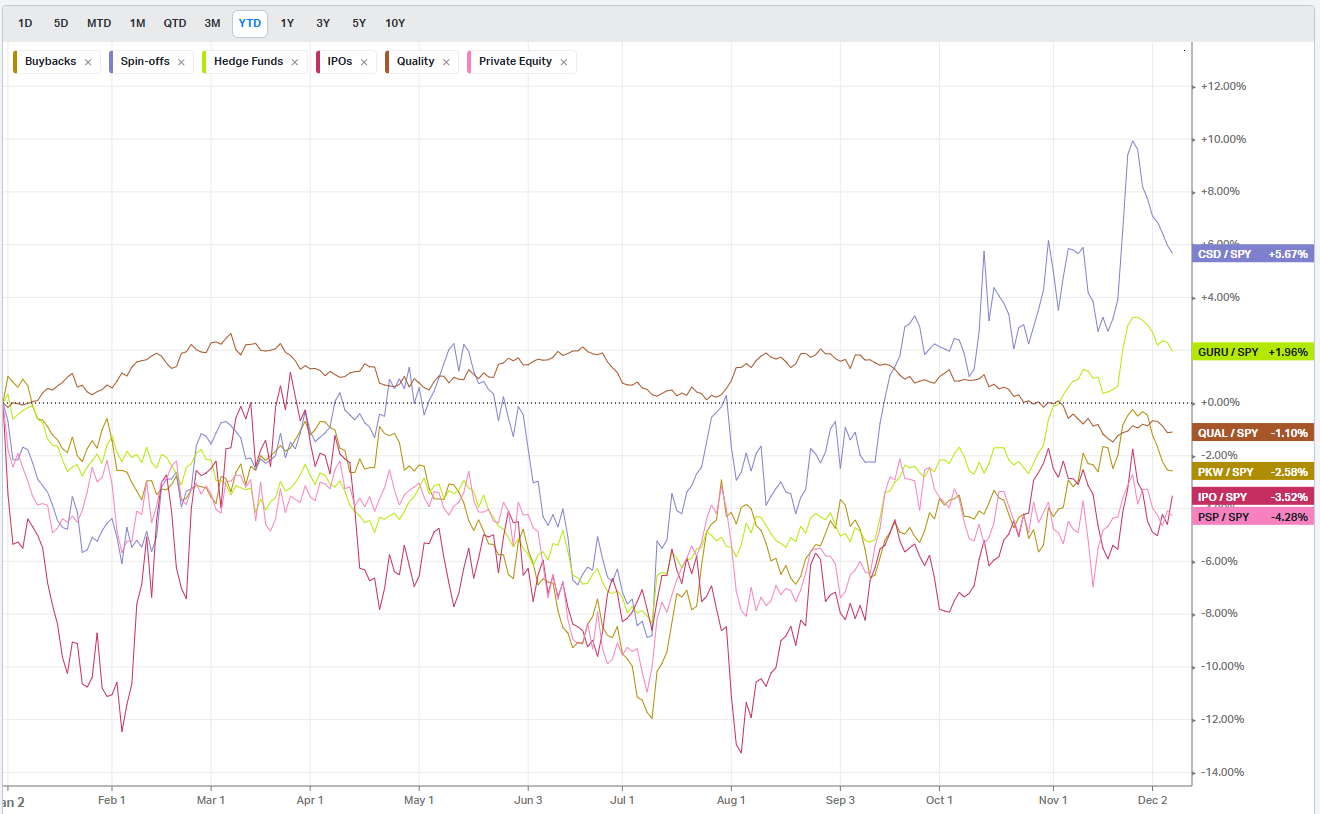

Summary Of Thematic Performance YTD

VolumeLeaders.com provides a lot of pre-built filters for thematics so that you can quickly dive into specific areas of the market. These performance overviews are provided here only for inspiration. Consider targeting leaders and/or laggards in the best and worst sectors, for example.

S&P By Sector

S&P By Industry

Commodities: Energy

Commodities: Metals

Commodities: Agriculture

Country ETFs

Currencies

Global Yields

Factors: Style

Factors: Size vs Value

Factors: Qualitative

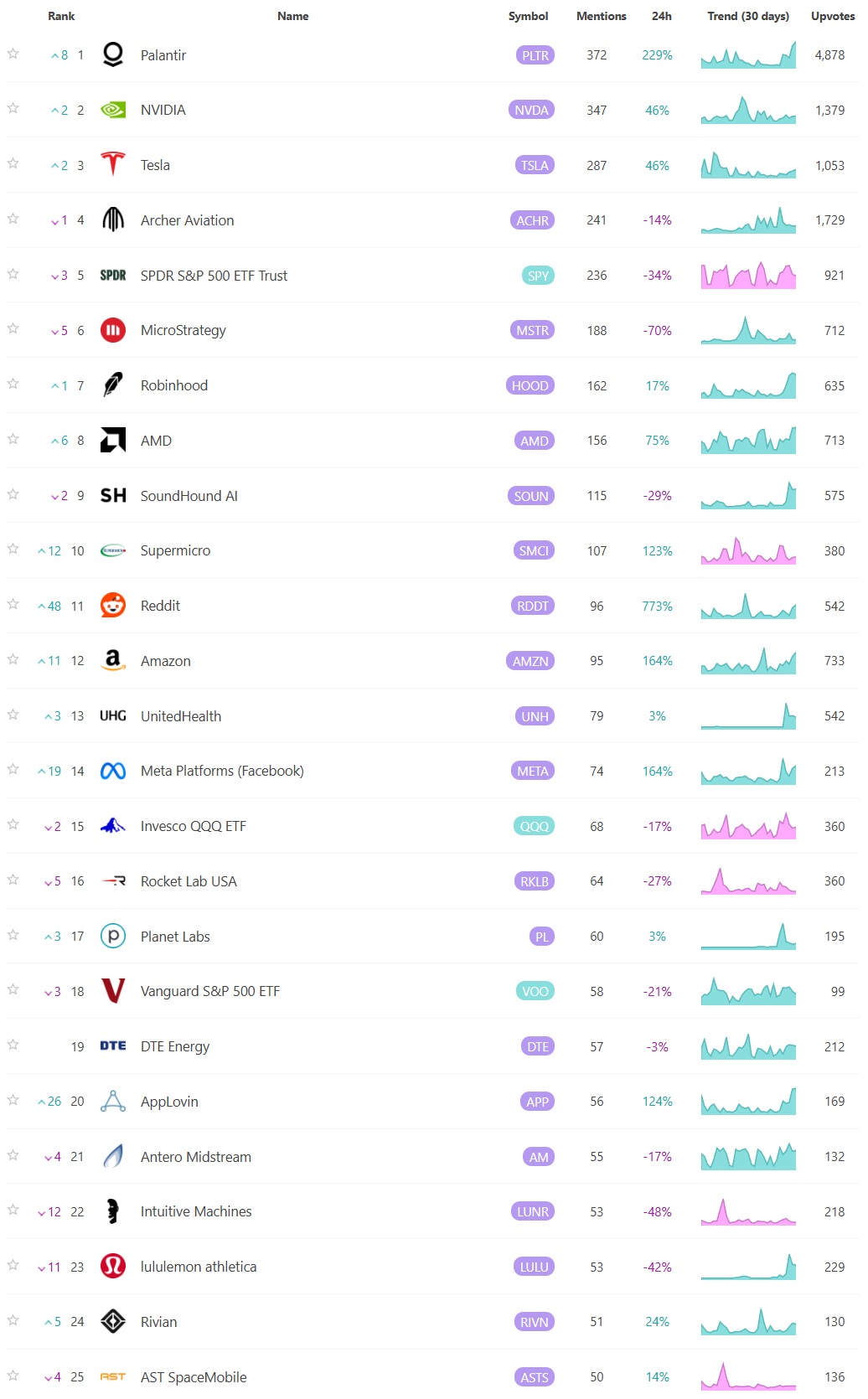

Social Media Favs

Analyzing social sentiment can provide valuable insights for investment strategies by offering a pulse on public perception, mood, and market sentiment that traditional financial indicators might not capture. Here’s how social sentiment analysis can enhance investment decisions:

Market Momentum: Positive or negative social sentiment can signal impending momentum shifts. When public opinion on a stock, sector, or asset class changes sharply, it can create buying or selling pressure, especially if that sentiment becomes widespread.

Early Detection of Trends: Social sentiment data can help investors spot trends before they show up in technical or fundamental data. For example, increased positive chatter around a particular company or sector might indicate growing interest or excitement, which could lead to price appreciation.

Gauge Retail Investor Impact: With the rise of retail investor platforms, collective sentiment on social media can lead to significant price movements (e.g., meme stocks). Understanding how retail investors view certain stocks can help in identifying high-volatility opportunities.

Event Reaction Monitoring: Social sentiment can provide real-time reactions to news events, product releases, or earnings reports. Investors can use this information to gauge market reaction quickly and adjust their strategies accordingly.

Complementing Quantitative Models: By adding a social sentiment layer to quantitative models, investors can enhance predictions. For example, a model that tracks historical price and volume data might perform even better when factoring in sentiment trends as a measure of market psychology.

Risk Management: Negative sentiment spikes can be a signal of potential downturns or increased volatility. By monitoring sentiment, investors might avoid or hedge against investments in companies experiencing a public relations crisis or facing negative perceptions.

Long-Term Sentiment Trends: Sustained sentiment trends, whether positive or negative, often mirror longer-term market cycles. Tracking sentiment trends over time can help identify shifts in investor psychology that could affect longer-term investments or sector rotations.

For these reasons, sentiment analysis, when combined with other tools, can provide a comprehensive view of both immediate market reactions and underlying investor attitudes, helping investors position themselves strategically across various time frames. Here are the most mentioned/discussed tickers on Reddit from some of the most active Subreddits for trading:

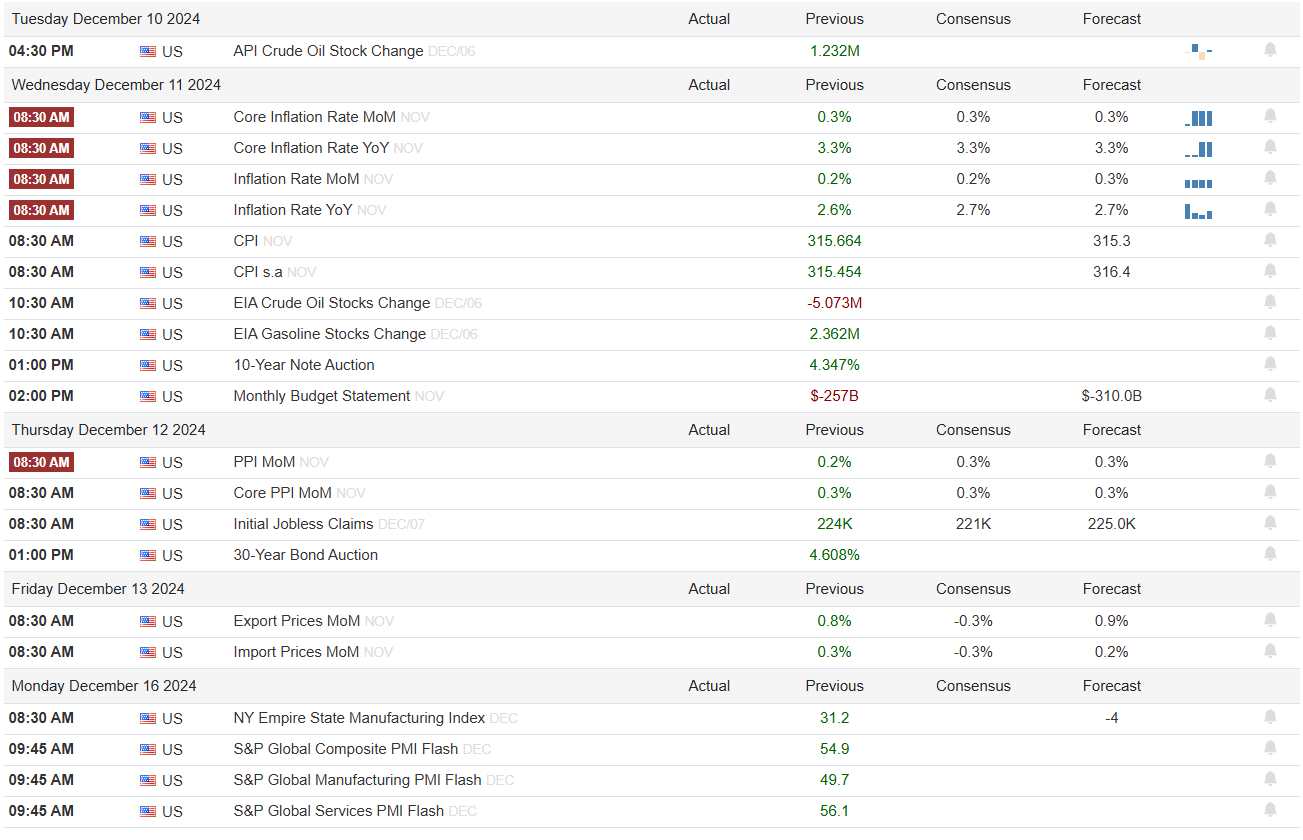

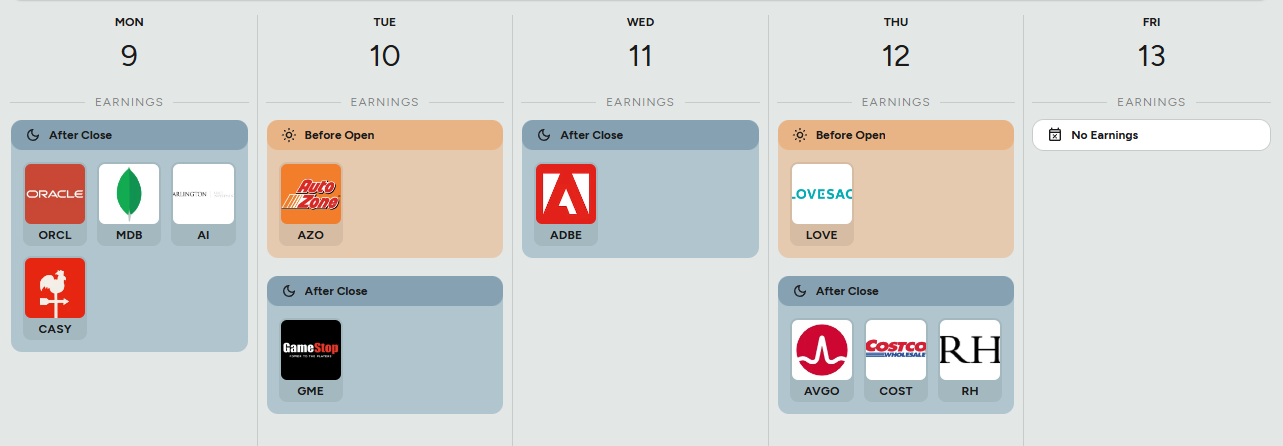

Events On Deck This Week

Here are key events happening this week that have the potential to cause outsized moves in the market or heightened short-term volatility.

Econ Events By Day of Week

Anticipated Earnings By Day of Week

Thank you for being part of our community and for taking the time to read this publication. Your engagement and insights mean a great deal to all of us, and we're genuinely grateful to share this space with such dedicated and thoughtful readers. Wishing you a productive and successful week ahead in the markets. May the coming days bring clarity and great opportunities. Happy trading!