Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 21 / What to expect Nov 11, 2024 thru Nov 15, 2024

Last Week: Insights & Trends

The U.S. markets were shaped by a blend of political and economic events this past week, setting a strong tone for the coming months. With the U.S. election results confirming a Republican win in the White House and Senate, and an anticipated but uncertain Republican hold on the House, markets began recalibrating to potential policy shifts. The election itself removed a significant element of uncertainty, catalyzing a post-election rally in equities. This rally, alongside the Federal Reserve’s recent decision to cut interest rates by 25 basis points, had substantial effects on various market sectors, including stocks, bonds, and cryptocurrencies.

Key Takeaways from the Election Outcome

Markets were quick to respond positively to the election, pushing the S&P 500, NASDAQ, and Dow to record levels, with gains of 5-6% for the week. The clarity around the election outcome lifted a cloud of uncertainty, which, coupled with hopes for pro-growth policies, led to significant sectoral performance, especially in financial services, energy, and consumer discretionary sectors. Notably, smaller-cap companies and financials surged amid expectations of lighter regulations and favorable fiscal policies. Defensive sectors, including utilities and staples, also saw gains, possibly reflecting an investor preference for stability amid fluctuating bond yields.

Potential Policy Shifts and Market Impact

A central theme in market discussions was the potential for extended tax cuts and deregulation under a Republican-led government. Expectations of a renewed focus on corporate tax cuts and regulatory rollbacks are anticipated to spur corporate spending, benefitting cyclical and domestically focused companies. Conversely, the fiscal implications of these tax cuts raise concerns about inflation and increased debt. The administration’s potentially aggressive stance on tariffs and immigration may further fuel inflation, though a strengthening U.S. dollar might mitigate some of the impact on prices.

Federal Reserve Rate Cut and Bond Market Reactions

The Fed’s decision to cut rates for the second time in this cycle brought the federal funds target range to 4.5% - 4.75%, reflecting a cautious approach towards easing. Chair Powell emphasized that monetary policy would remain steady in response to campaign proposals until they manifest into actionable policy. In the bond market, Treasury yields saw volatility, with the 10-year yield rising briefly midweek before easing post-Fed decision. The bond market, now pricing in a slower pace of future rate cuts, anticipates three more cuts by year-end, down from six expected a month ago. As a result, longer-term rates may settle slightly higher than previously projected, between 3.5% and 4.0%.

Underlying Economic Fundamentals Remain Strong

Despite the political changes, the fundamentals sustaining the U.S. market’s record highs remained robust. Consumer spending, rising incomes, stable employment, and strong corporate earnings continue to bolster economic resilience. Corporate profits are projected to rise in the coming years, with S&P 500 earnings expected to grow from 0.5% in 2023 to 9% in 2024. Interest rates are now likely past their peak, with inflation stabilizing, presenting opportunities for a soft landing. These fundamentals support continued bullish sentiment, which is further enhanced by the ability of U.S. companies to adapt to changing policies.

Opportunities in Equities and Fixed-Income Markets

Value-style investments and small- to mid-cap stocks, which have lagged since the bull market’s inception in late 2022, stand to benefit from broadening market participation, potentially driven by pro-growth policies. While equities look set to gain from tax incentives and deregulation, the anticipated increase in fiscal deficits and debt levels could pressure bonds. Given the attractive yield levels, investors may find value in extending the maturity of their bond portfolios to lock in high yields, especially as short-term rates on cash investments are likely to follow the Fed’s policy rate lower.

Economic Data and Market Sentiment

Investor sentiment received a boost from a strong consumer sentiment index, rising to a seven-month high, and upbeat earnings reports from leading sectors. The University of Michigan’s consumer sentiment data reflected growing consumer confidence in the economy, driven by low unemployment and resilient growth. The sentiment was further supported by solid labor market and productivity numbers, reflecting continued economic momentum.

Cryptocurrency and Alternative Assets

In the crypto market, Bitcoin saw a record high, reflecting optimism that the new administration might adopt a favorable stance towards digital currencies. With cryptocurrency markets rising in tandem with equities, the sector’s growth aligned with investor expectations of regulatory clarity.

Looking Forward: Long-Term Market Fundamentals

With the election behind, attention now shifts to the longer-term market dynamics, including the influence of potential fiscal policies and economic data on future Fed decisions. The upcoming Consumer Price Index (CPI) report, scheduled for release this Wednesday, could offer insights into the inflationary landscape, providing additional clarity on the Fed’s rate cut trajectory. Investors are reminded of the value of a well-diversified portfolio, which can mitigate risks from policy shifts and ensure steady progress toward long-term financial objectives.

Futures Markets

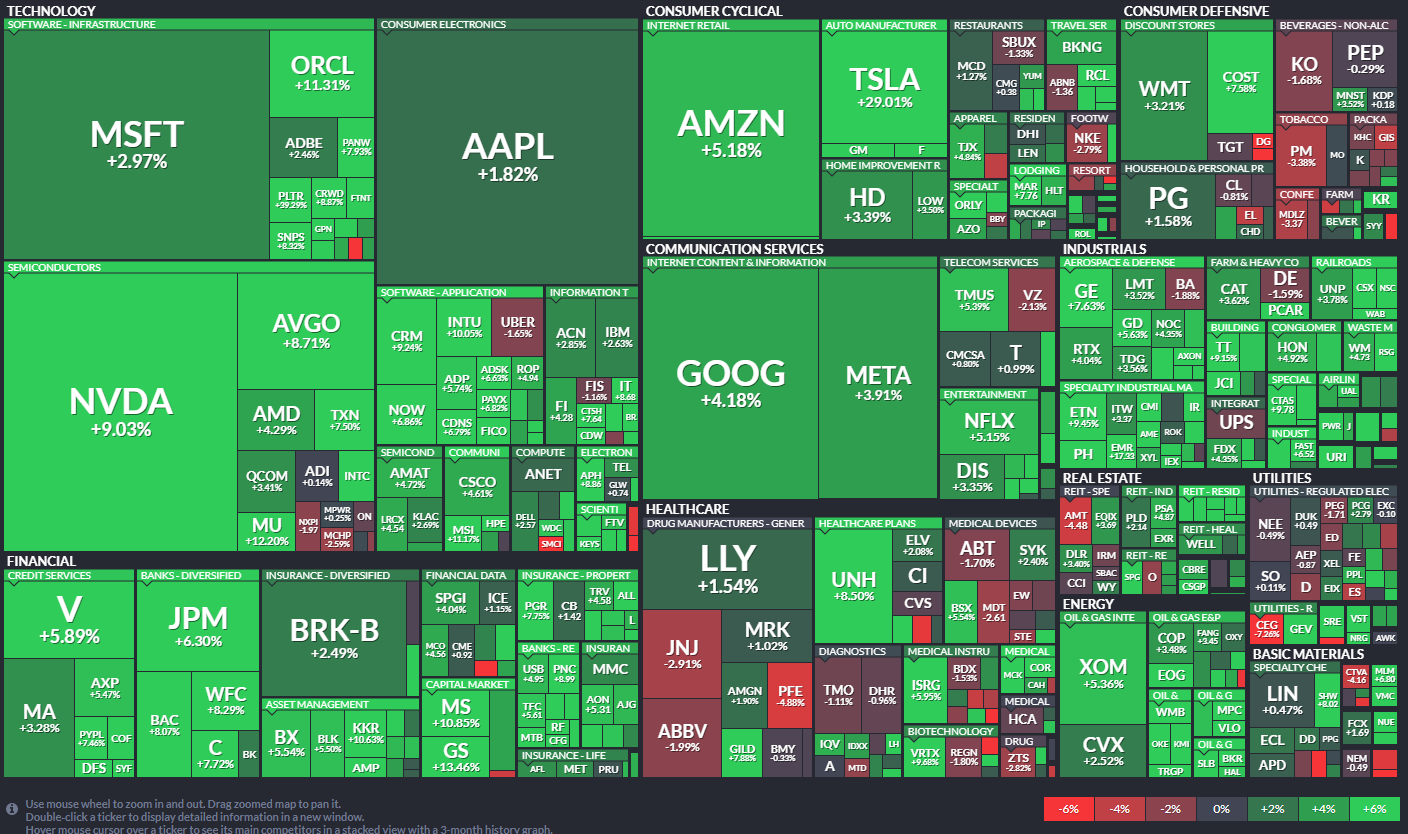

S&P 500: By Size & Sector

S&P 500: Sectors Scorecard

ETFs

US Investor Sentiment

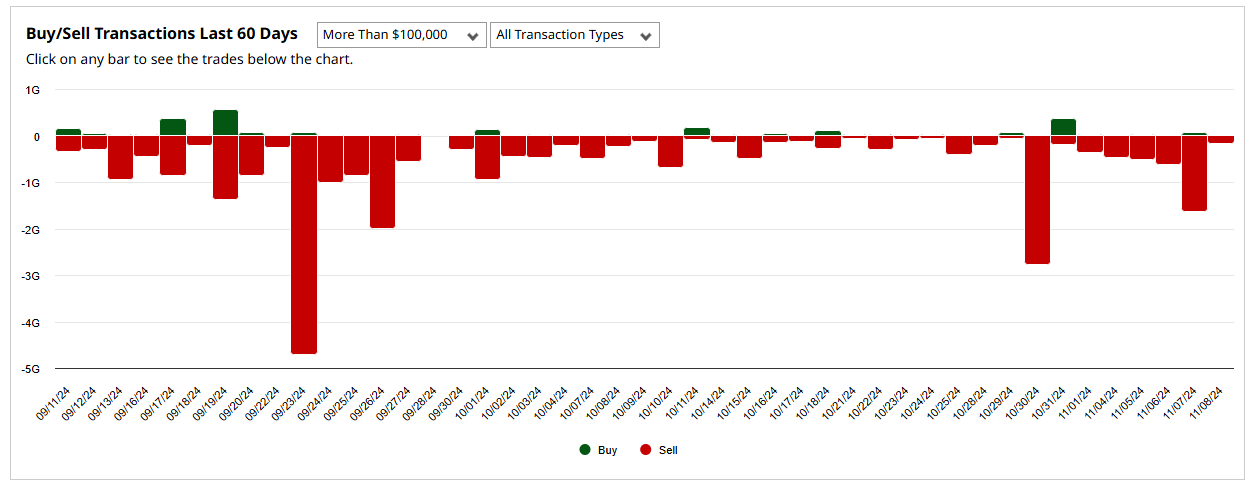

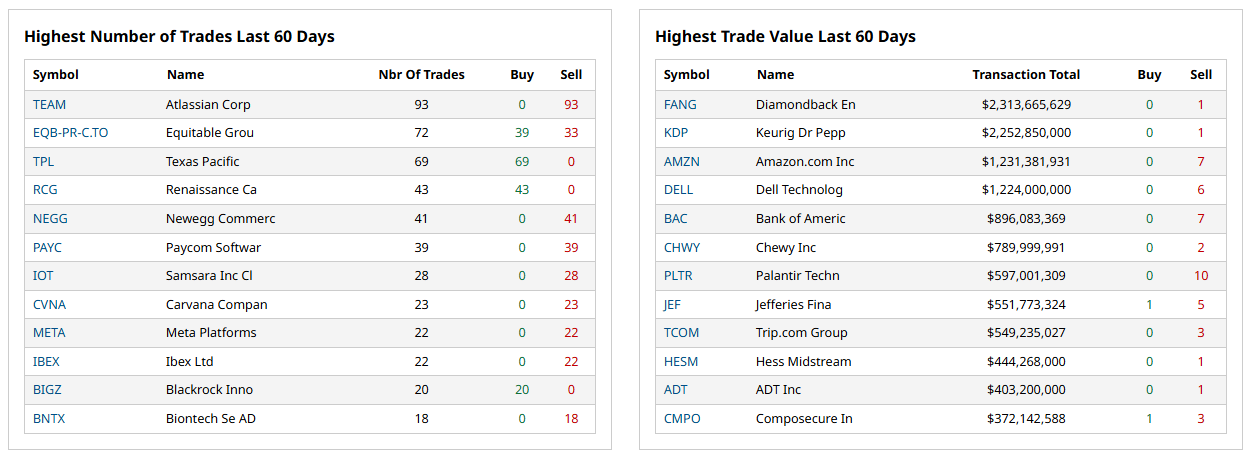

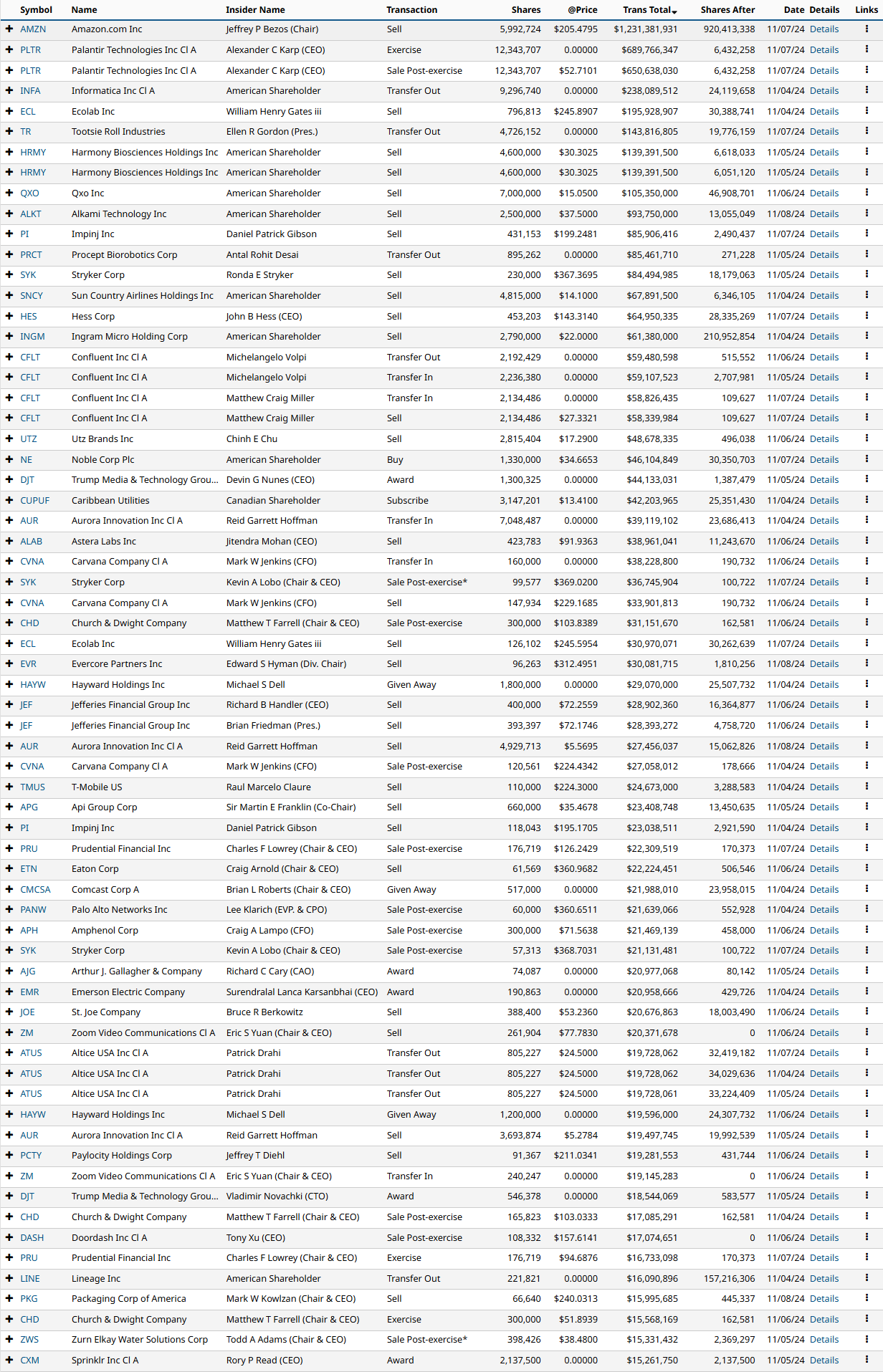

Insider Trading

Insider trading occurs when a company’s leaders or major shareholders trade stock based on non-public information. Tracking these trades can reveal insider expectations about the company’s future. For example, large purchases before an earnings report or drug trial results might indicate confidence in upcoming good news.

Last Week’s Insider Transactions Over $15M

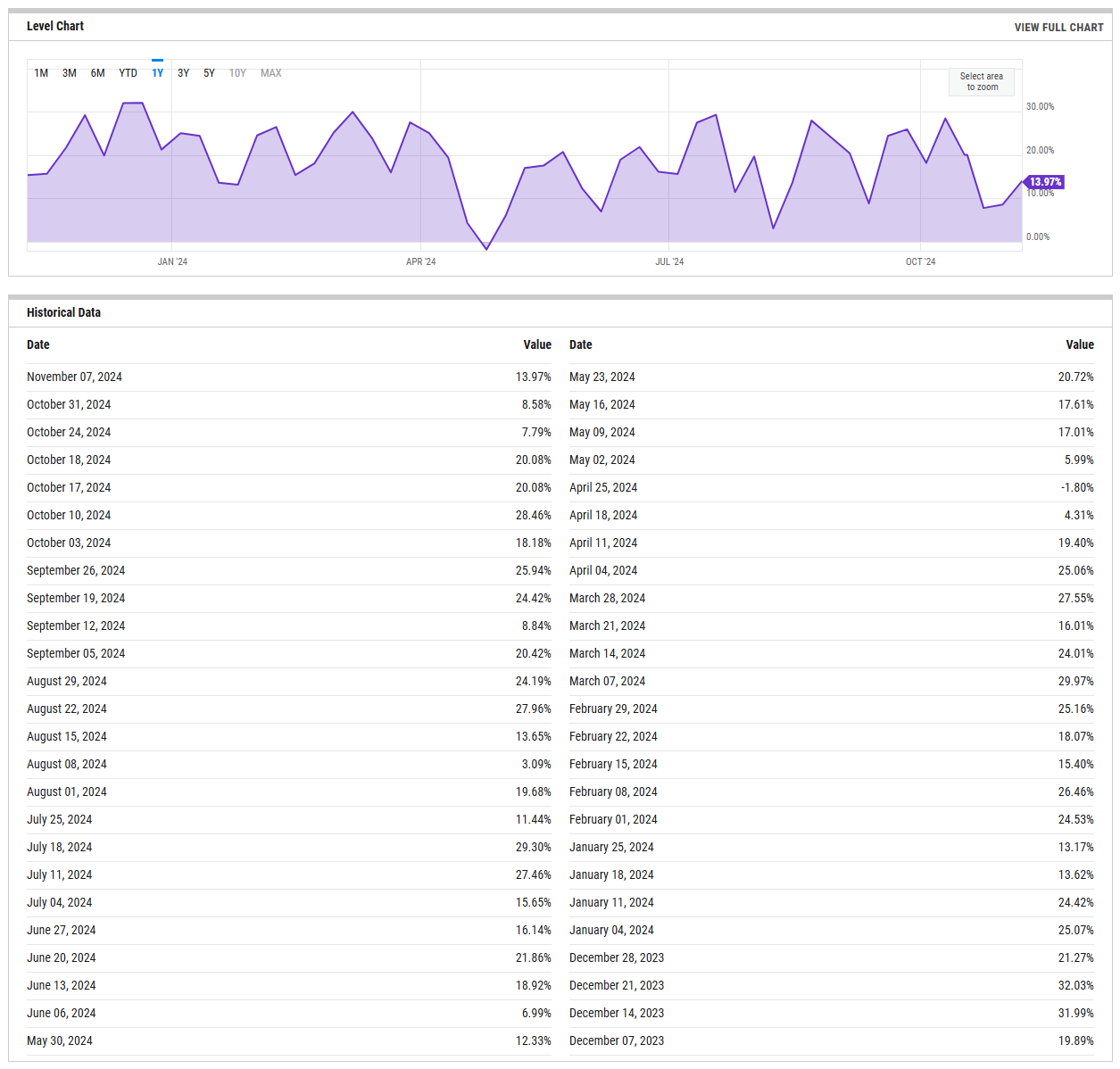

%Bull-Bear Spread

The %Bull-Bear Spread chart is a sentiment indicator that shows the difference between the percentage of bullish and bearish investors, often derived from surveys or sentiment data, such as the AAII (American Association of Individual Investors) sentiment survey. This spread tells investors about the prevailing mood in the market and can provide insights into market extremes and potential turning points.

Bullish or Bearish Sentiment:

When the spread is positive, it means more investors are bullish than bearish, indicating optimism about the market’s direction.

A negative spread indicates more bearish sentiment, meaning more investors expect the market to decline.

Contrarian Indicator:

The %Bull-Bear Spread is often used as a contrarian indicator. For example, extremely high levels of bullish sentiment might suggest that the market is overly optimistic and could be due for a correction.

Similarly, when bearish sentiment is extremely high, it might indicate that the market is overly pessimistic, and a rally could be on the horizon.

Market Extremes and Reversals:

Historically, extreme values of the spread (both positive and negative) can signal turning points in the market. A very high positive spread can signal market exuberance, while a very low or negative spread may indicate fear or capitulation.

1-Year View

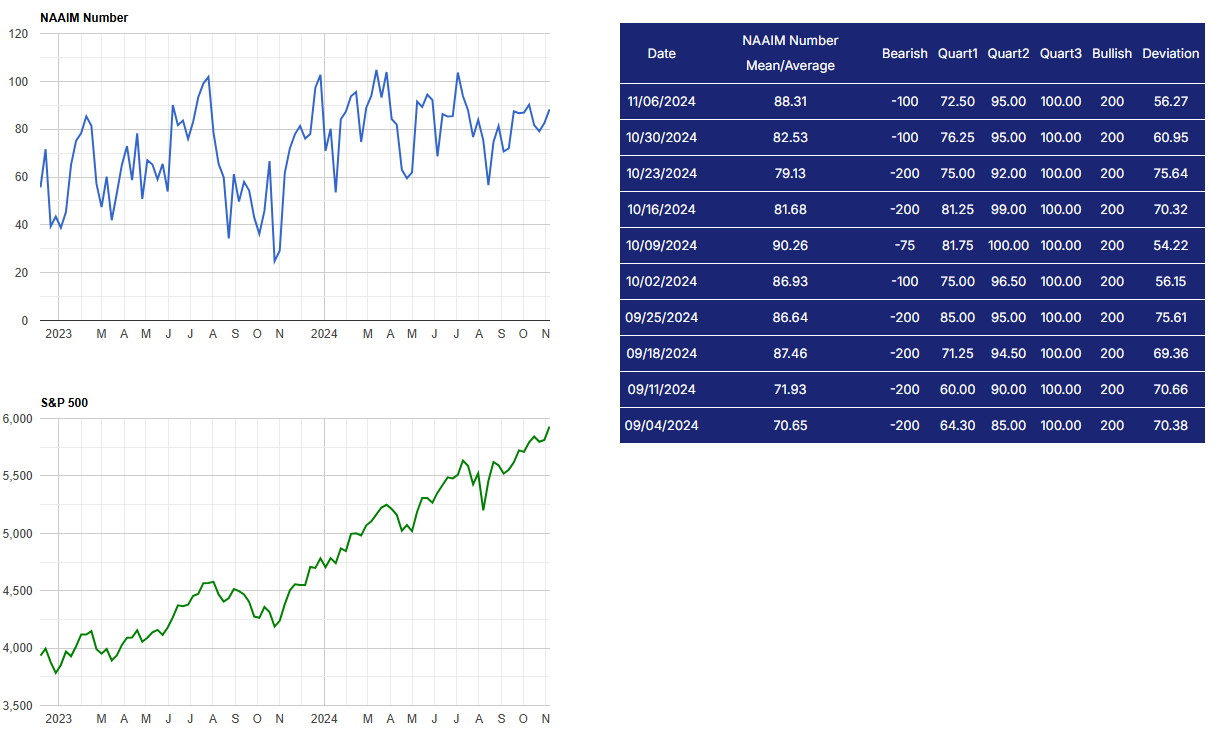

NAAIM Exposure Index

The NAAIM Exposure Index (National Association of Active Investment Managers Exposure Index) measures the average exposure to U.S. equity markets as reported by its member firms. These are typically active money managers who provide their equity exposure levels weekly. The index offers insight into how much these managers are investing in equities at any given time, ranging from being fully short (-100%) to leveraged long (up to +200%).

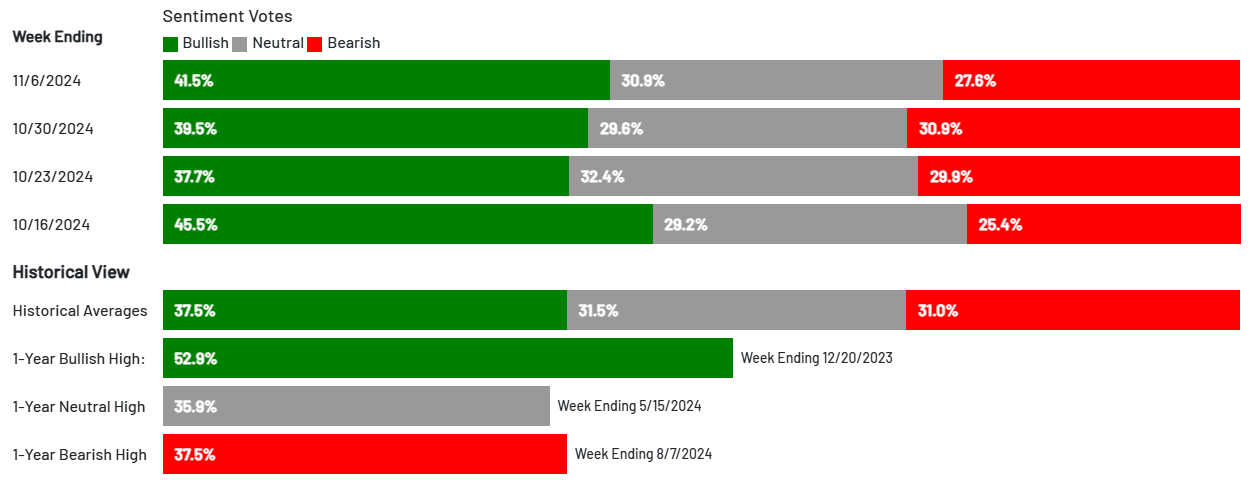

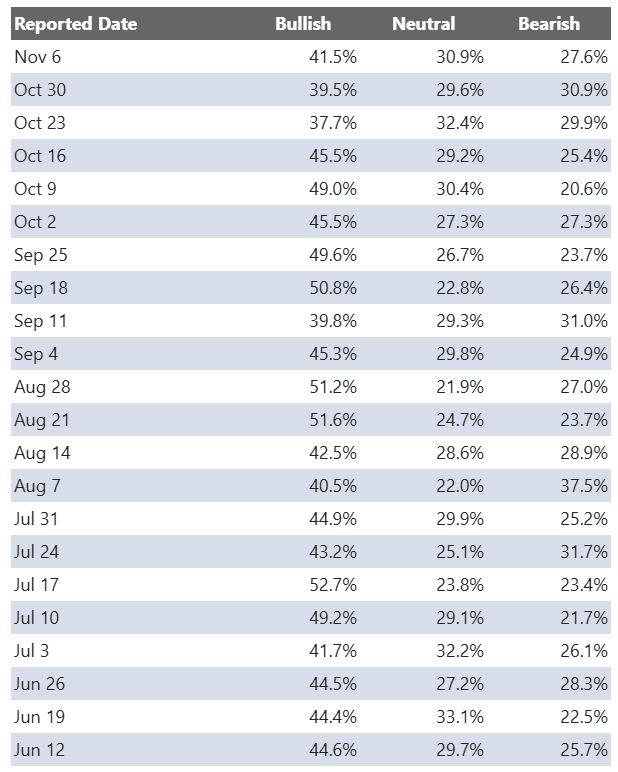

AAII Investor Sentiment Survey

The AAII Investor Sentiment Survey is a weekly survey conducted by the American Association of Individual Investors (AAII) to gauge the mood of individual investors regarding the direction of the stock market over the next six months. It provides insights into whether investors are feeling bullish (expecting the market to rise), bearish (expecting the market to fall), or neutral (expecting the market to stay about the same).

Key Points:

Bullish Sentiment: Reflects the percentage of investors who believe the stock market will rise in the next six months.

Bearish Sentiment: Represents those who expect a decline.

Neutral Sentiment: Reflects investors who anticipate little to no market movement.

The survey is widely followed as a contrarian indicator, meaning that extreme levels of bullishness or bearishness can sometimes signal market turning points. For example, when a large number of investors are overly optimistic (high bullish sentiment), it could suggest a market top, while excessive pessimism (high bearish sentiment) may indicate a market bottom is near.

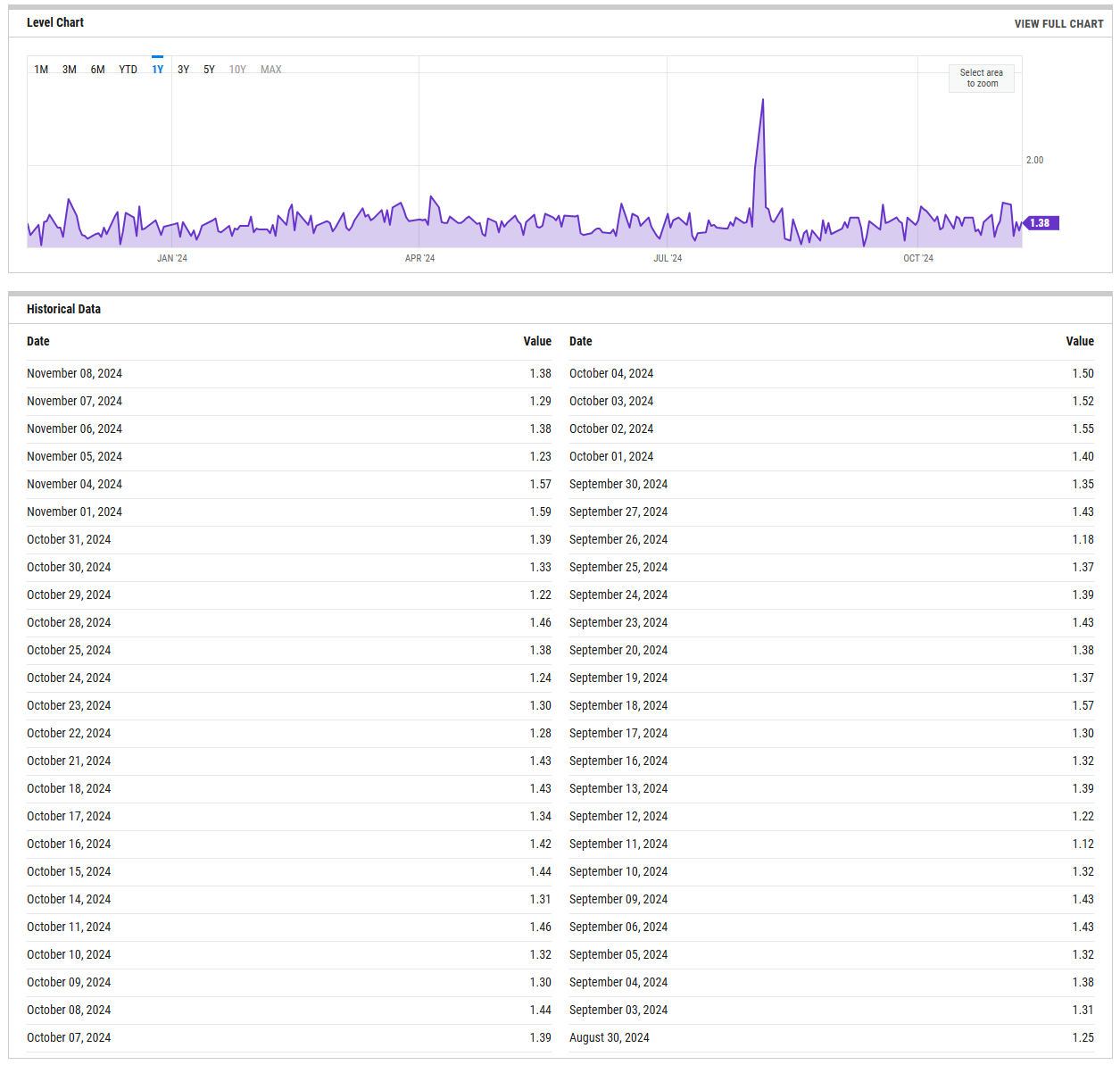

SPX Put/Call Ratio

The SPX Put/Call Ratio is an indicator that is used to gauge market sentiment. This is calculated as the ratio between trading S&P 500 put options and S&P call options. A high put/call ratio can indicate fear in the markets, while a low ratio indicates confidence. For example, in 2015, the Put-Call ratio was as high as 3.77 because of market fears stemming from various global economic issues like a GDP growth slowdown in China and a Greek debt default.

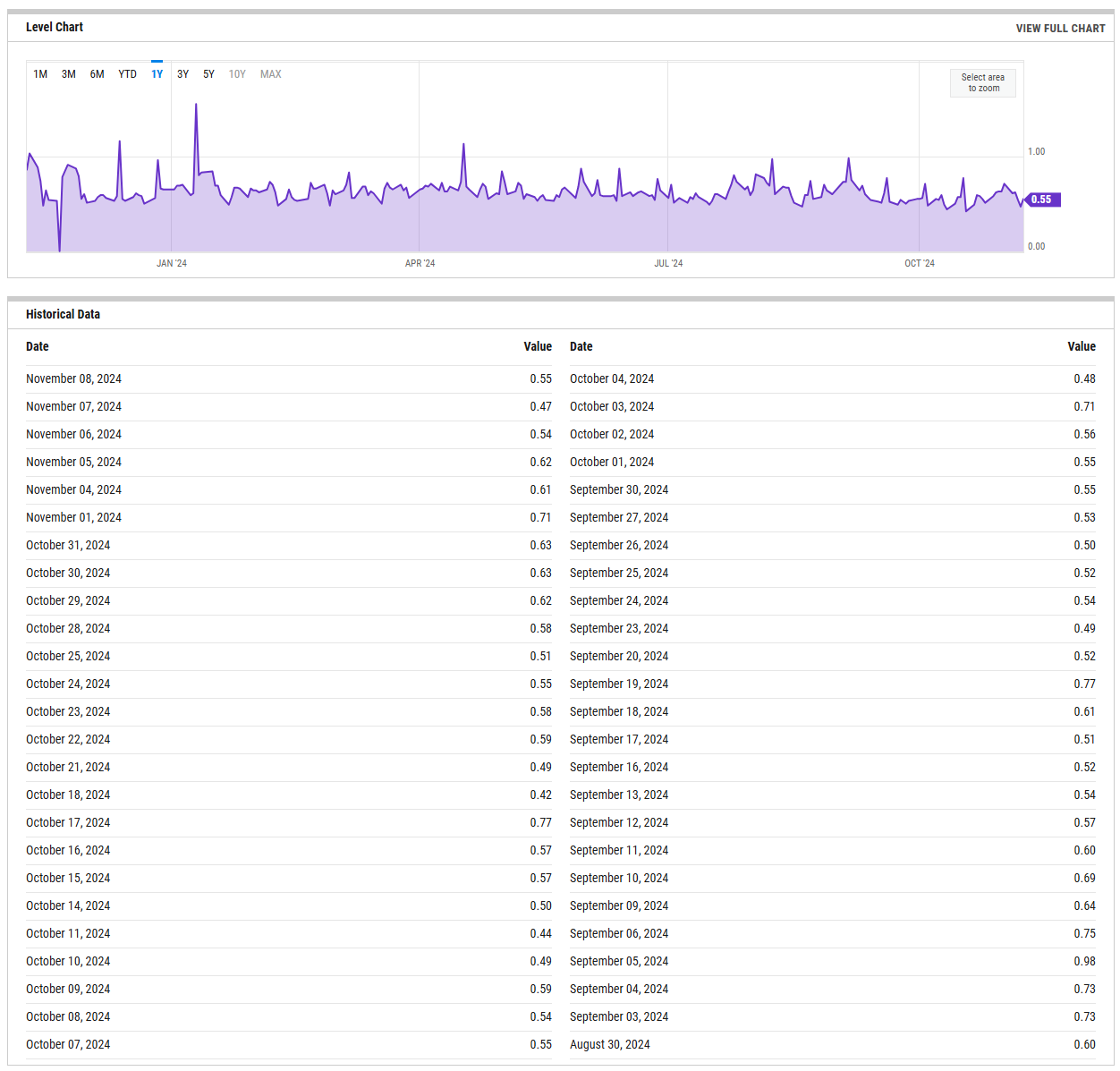

CBOE Equity Put/Call Ratio

The CBOE (Chicago Board Options Exchange) equity put/call ratio is a sentiment indicator used by traders and analysts to gauge market sentiment and potential shifts in investor behavior. It is calculated by dividing the volume of put options by the volume of call options on equities. Here’s what it reveals and how it is generally interpreted:

High Put/Call Ratio: When the put/call ratio is high (above 1.0), it suggests that there is more demand for put options than call options. This typically reflects a more bearish sentiment, as investors may be hedging against potential declines or expecting the market to fall.

Low Put/Call Ratio: Conversely, a low put/call ratio (below 0.7) indicates a higher volume of call options compared to puts, reflecting bullish sentiment. Investors may be expecting upward momentum and are positioning themselves to profit from price gains.

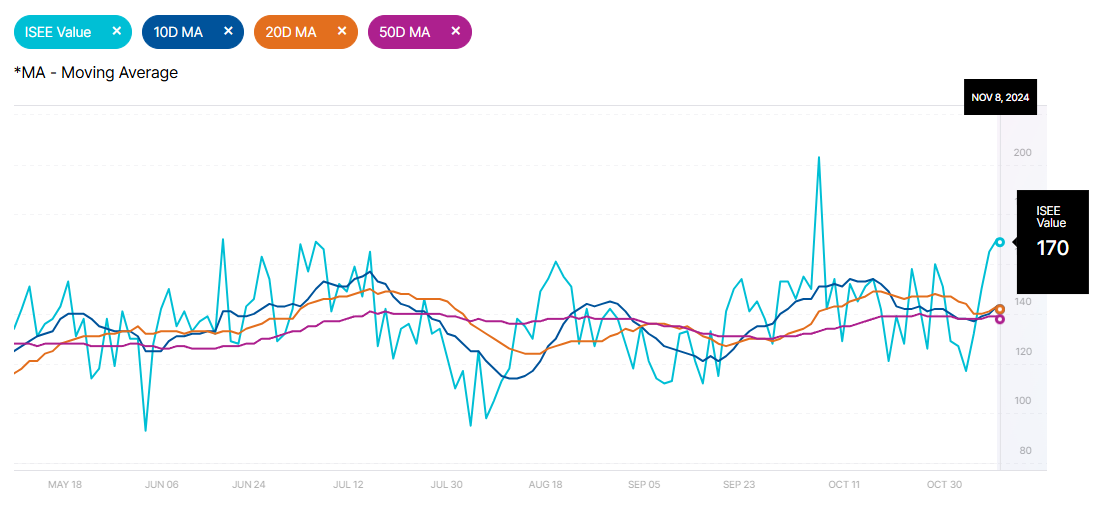

ISEE Sentiment Index

The ISEE (International Securities Exchange Sentiment) Index is a measure of investor sentiment derived from options trading. Unlike traditional put/call ratios, the ISEE Index focuses only on opening long customer transactions and is adjusted to remove market-maker and firm trades, providing a purer sentiment reading.

The ISEE Index typically ranges from 0 to 200, with readings above 100 indicating more call options being bought relative to put options, suggesting bullish sentiment. Conversely, readings below 100 suggest bearish sentiment, with more puts being purchased relative to calls.

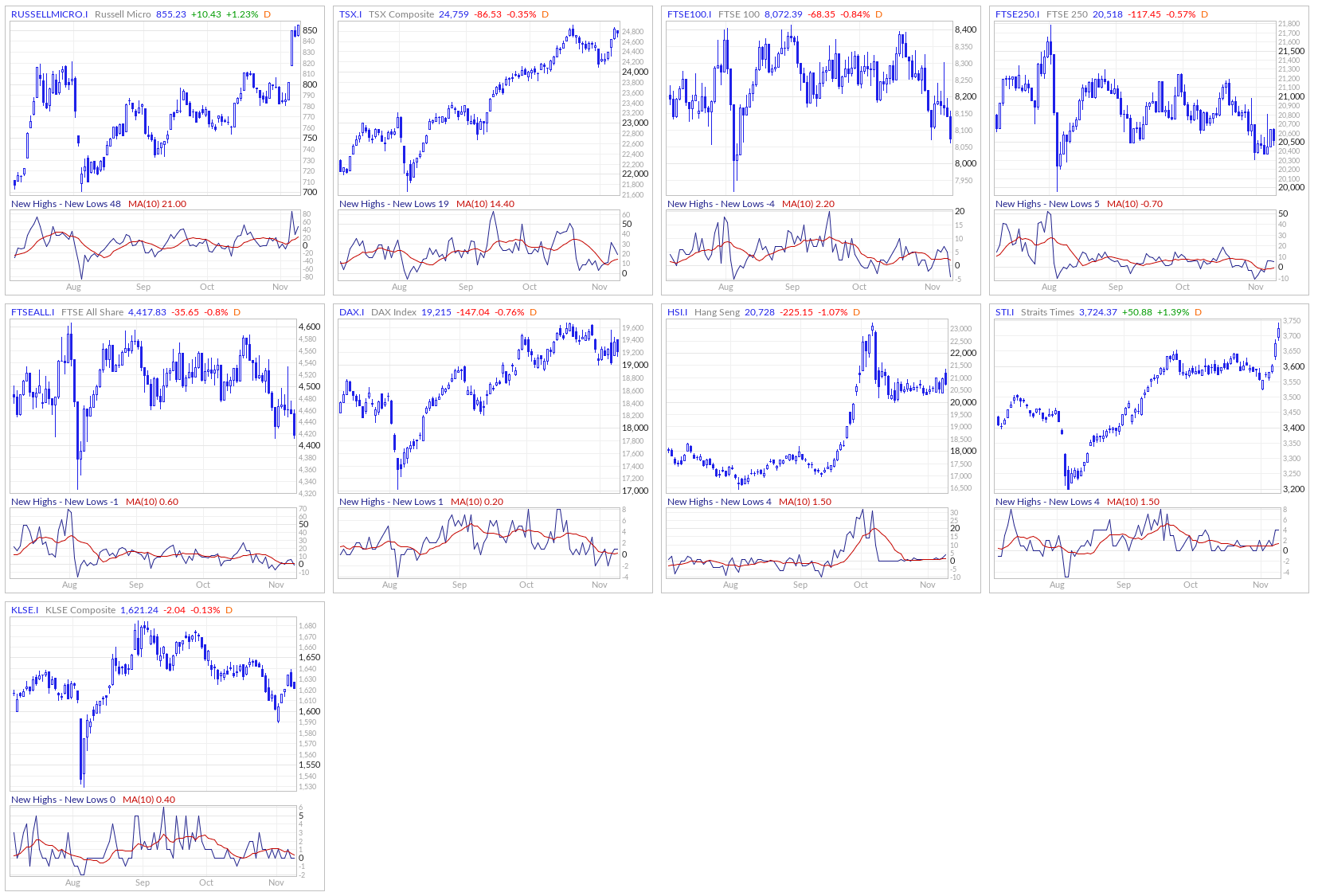

New Highs - New Lows

The New Highs - New Lows indicator (NH-NL) displays the daily difference between the number of stocks reaching new 52-week highs and the number of stocks reaching new 52-week lows. The NH-NL indicator generally reaches its extreme lows slightly before a major market bottom. As the market then turns up from the major bottom, the indicator jumps up rapidly. During this period, many new stocks are making new highs because it's easy to make a new high when prices have been depressed for a long time. The NH-NL indicator oscillates around zero. If the indicator is positive, the bulls are in control. If it is negative, the bears are in control. As the cycle matures, a divergence often occurs as fewer and fewer stocks are making new highs (the indicator falls), yet the market indices continue to reach new highs. This is a classic bearish divergence that indicates that the current upward trend is weak and may reverse.

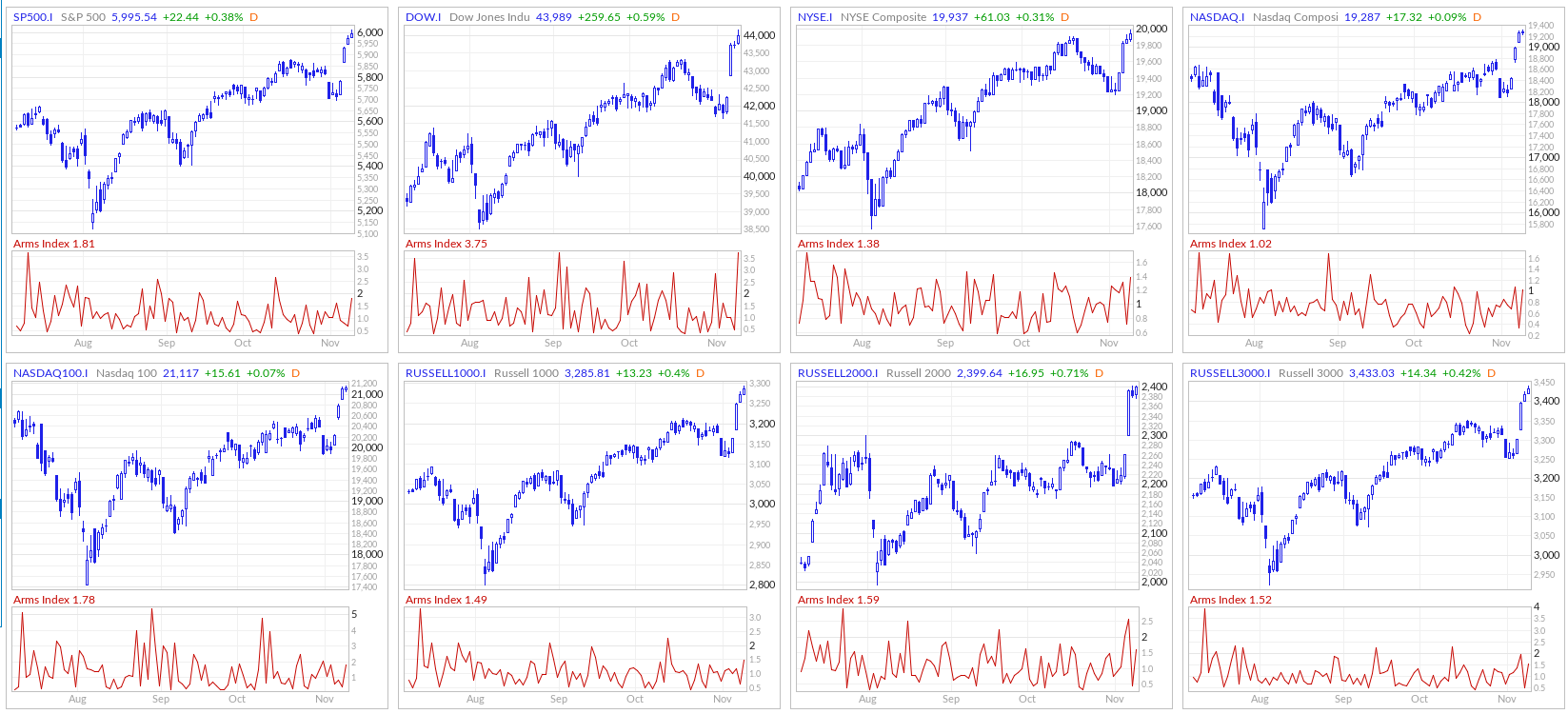

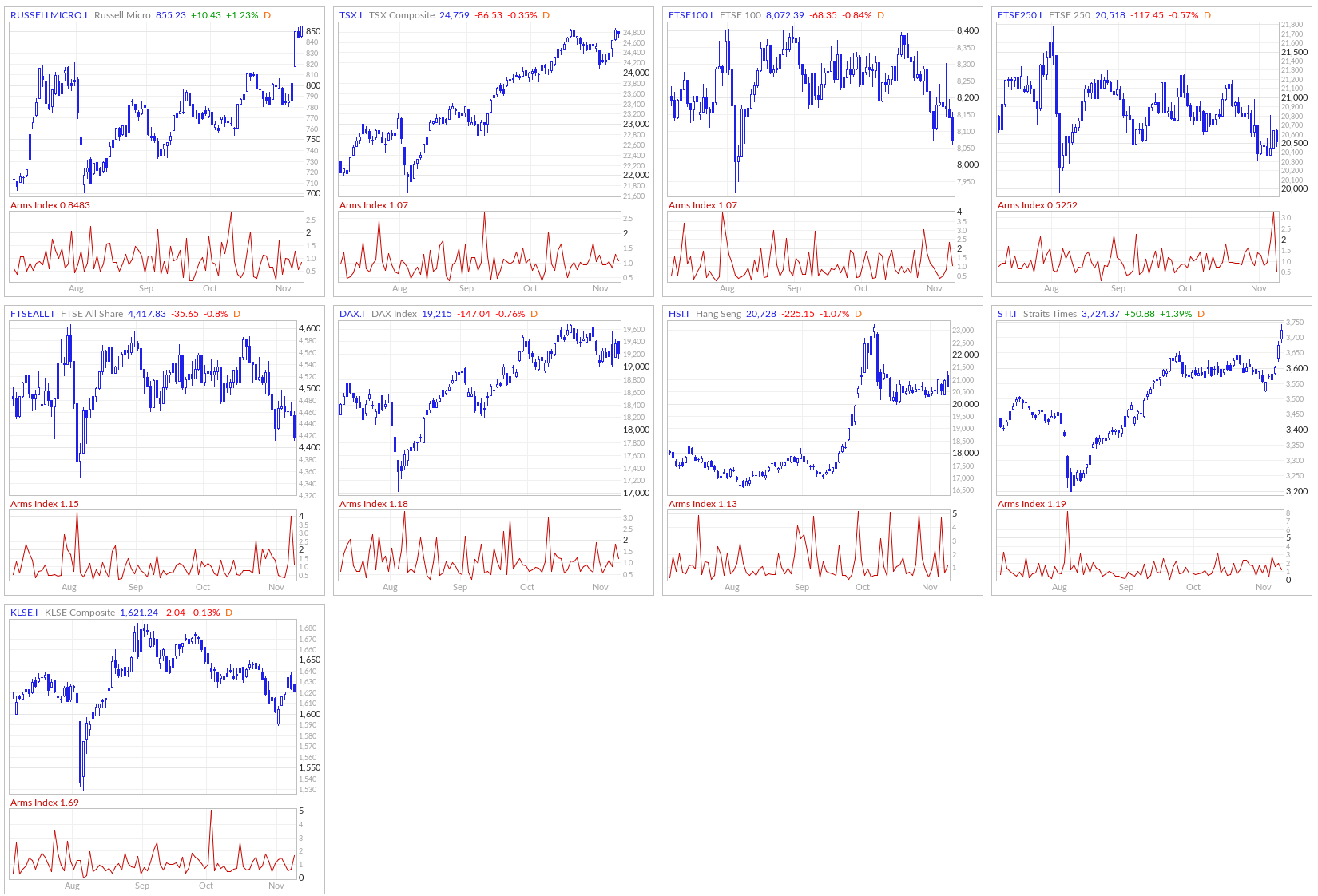

ARMS Index

The Arms Index, also known as the TRIN (Short-Term TRading INdex), was developed by Richard Arms in the 1960s. It is calculated by dividing the ratio of advancing stocks to declining stocks by the ratio of advancing volume to declining volume. Interpreting the Arms Index involves looking at its value in relation to certain thresholds. A value below "1" is considered bullish, indicating that advancing stocks and volume dominate the market. Conversely, a value above "1" is considered bearish, suggesting that declining stocks and volume are more prevalent. Extremely low values (below 0.5) or high values (above 2) are often seen as potential reversal signals.

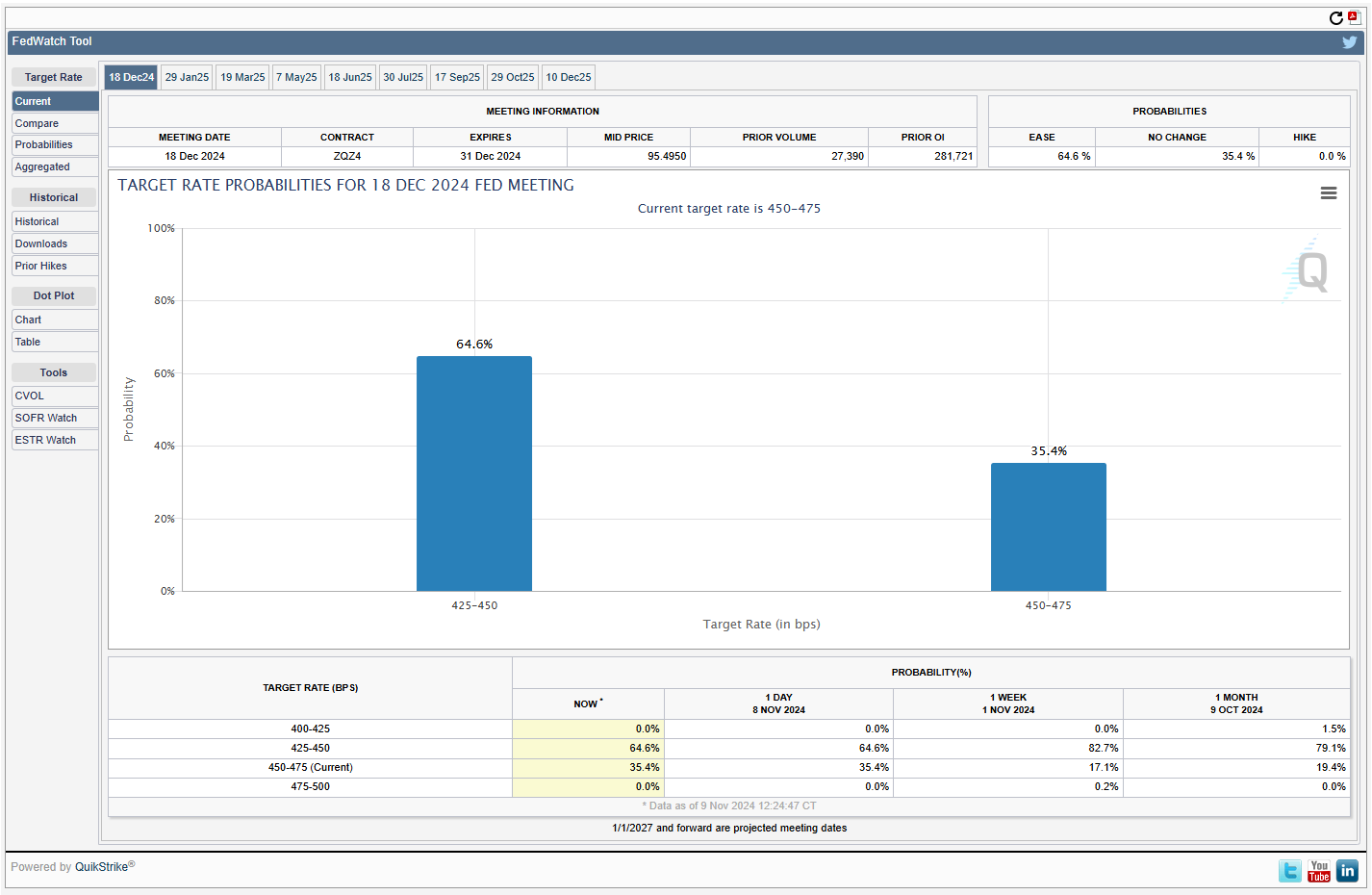

CME Fedwatch

What is the likelihood that the Fed will change the Federal target rate at upcoming FOMC meetings, according to interest rate traders? Use CME FedWatch to track the probabilities of changes to the Fed rate, as implied by 30-Day Fed Funds futures prices.

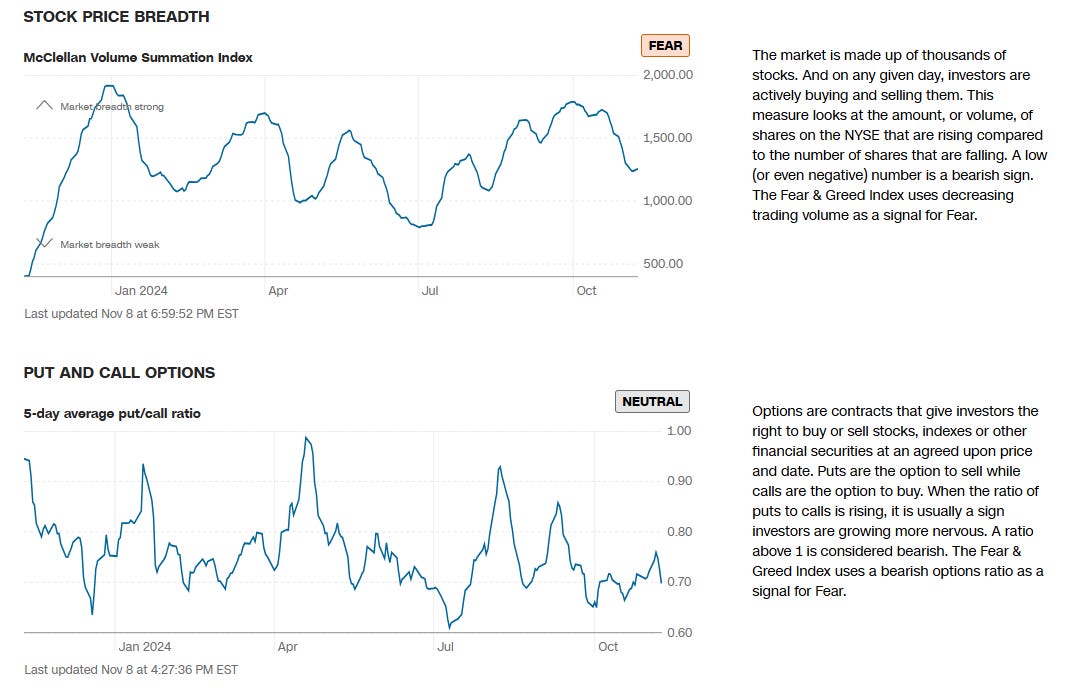

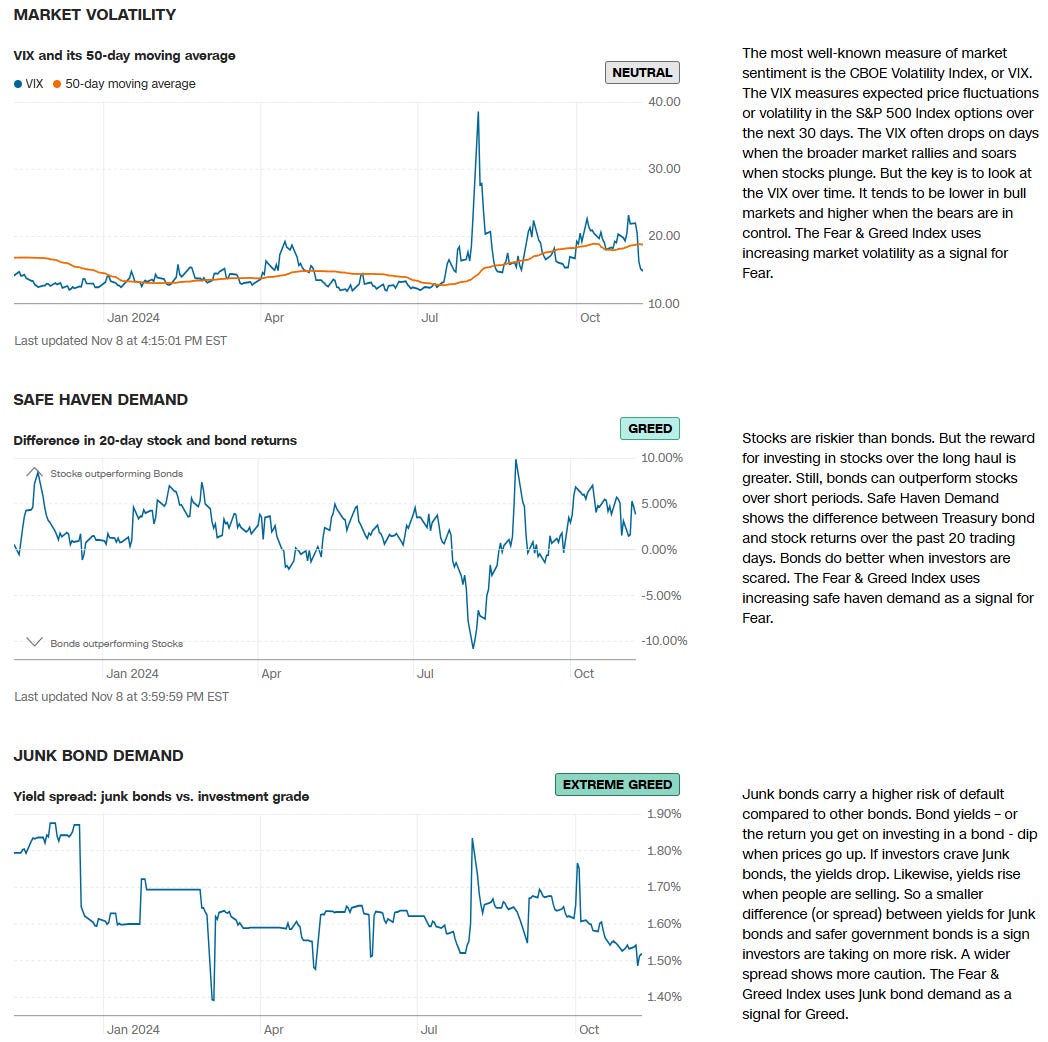

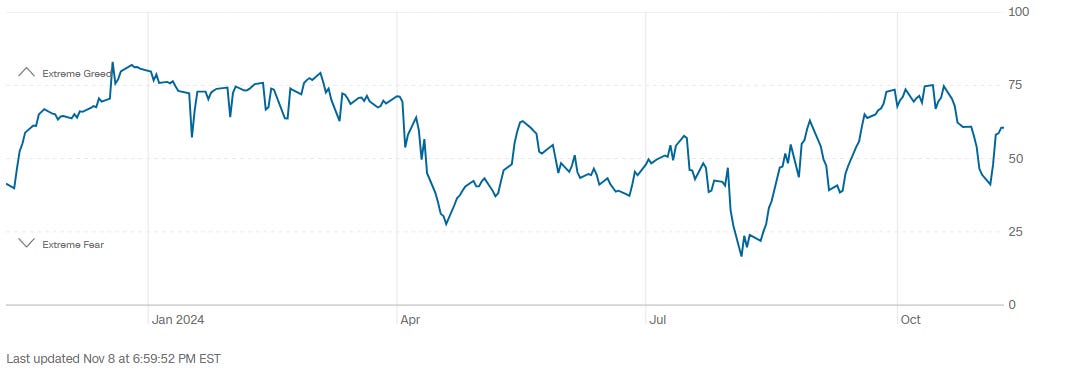

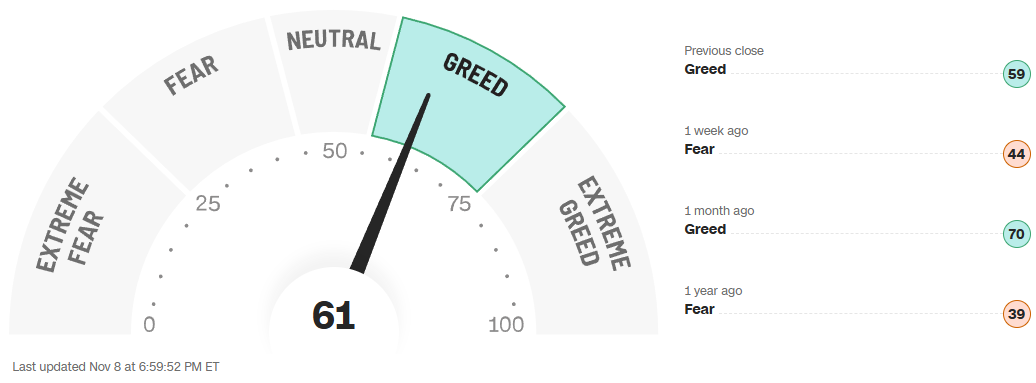

CNN 7 Fear & Greed Constituent Data Points + Composite Index

Final Composite Fear & Greed Index Reading

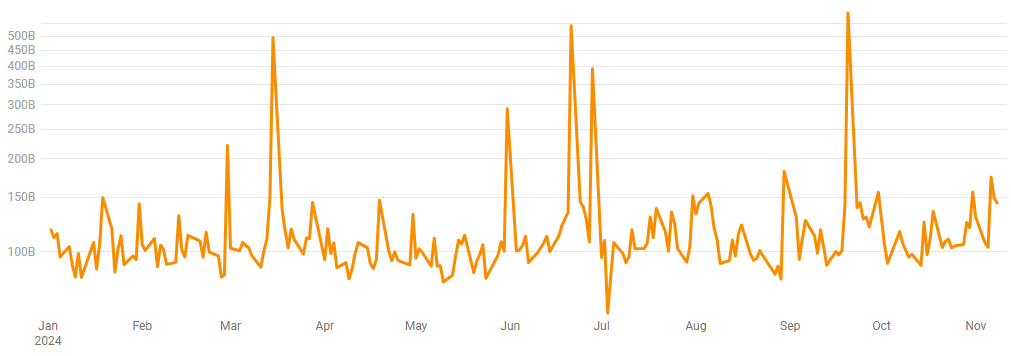

Dollars By Day

This chart shows institutional activity by dollars on a daily basis YTD. A log scale is used to dampen the effects of OpEx-days and to help highlight more nuanced activity at the lows.

Institutional S/R Levels for Major Indices

When you’re a large institutional player, your primary goal is to find liquidity - places to do a ton of business with the least amount of slippage possible. VolumeLeaders.com automatically identifies and visually plots the exact spots where institutions are doing business and where they are likely to return for more. It’s one of the primary reasons “support” and “resistance” concepts work and truly one of the reasons “price has memory”.

Levels from the VolumeLeaders.com platform can help you formulate trades theses about:

Where to add or take profit

Where to de-risk or hedge

What strikes to target for options

Where to expect support or resistance

And this is just a small sample; there are countless ways to leverage this information into trades that express your views on the market. The platform covers thousands of tickers on multiple timeframes to accommodate all types of traders. Observe for yourself how accurate the levels are by marking-up your charts with the information in the “Trade Levels” boxes I’m giving for free below and play-along in real-time this week. These charts cover recent sessions, but subs will get new levels as they develop, see the latest trades and institutional positioning, have access to levels from other time frames and so much more. When you watch these levels this week, I’m confident you’ll see how clear, intuitive and actionable this information is for yourself.

SPY 0.00%↑

1. 5 Largest Trades (Blue Circles)

Significant Institutional Trades (Oct 29 - Nov 6): The largest recent trade occurred on Nov 6 at $591.04 with a relative size (RS) of 119.28%, indicating strong buying interest. This high level of activity suggests continued bullish momentum as institutions are actively purchasing at higher prices.

Earlier Support Trades Around $577 - $583 (Oct 23 - Oct 29): Several large trades around $577 to $583 with RS values up to 99.42% indicate strong accumulation at these levels, which now act as support.

2. Key Institutional Activity Price Levels (Dashed Blue Lines)

$569.60 - $570.00: This range has significant volume and institutional support, with total dollar amounts in the $9.8B and $5.56B ranges. Given the high trading volume here, this level represents a critical support zone.

$591.04: The recent large trade at this level suggests that this could act as a new support level if SPY maintains upward momentum.

3. Volume and Relative Size (RS)

Largest Trade on Nov 6 at $591.04: The trade with an RS of 119.28% highlights a significant buying interest at this price, likely establishing it as an area of support.

Consistent Large Trades in the $577 - $583 Range: The high RS values in this range confirm institutional buying activity, suggesting that this range now acts as a strong support zone.

4. Support and Resistance Zones

Support Levels:

$569.60 - $570.00: This level is a solid support zone due to consistent institutional interest.

$577 - $583: This range, with multiple large trades, is another support zone that will likely hold if there’s a retracement.

$591.04: The recent large trade here may establish this level as a new support level in the current uptrend.

Resistance Levels:

SPY is currently testing all-time highs with no clear resistance levels above the recent highs, which indicates potential for further upward movement.

Conclusion:

Bullish Momentum: The recent institutional trades indicate strong bullish momentum, with significant support in the $577 - $583 range and recent buying activity at $591.04.

Key Levels to Watch: Support at $569.60 - $570, $577 - $583, and $591.04. With SPY testing highs, a break above these recent levels could lead to continued bullish momentum.

QQQ 0.00%↑

1. Largest Trades (Blue Circles)

Significant Trades in Early November (Nov 6): The largest recent trade occurred on Nov 6 at $504.22 with a relative size (RS) of 134.02%, showing strong institutional buying interest at this level. This indicates continued bullish momentum as institutions are actively buying at higher prices.

Support Trades in the $488 - $497 Range (Oct 23 - Oct 31): Several large trades were made in this range, with RS values up to 133.11%. This buying activity suggests that this area serves as a strong support zone.

2. Key Institutional Activity Price Levels (Dashed Blue Lines)

$487.60 and $488.40: These levels have significant volume and institutional interest, with dollar amounts at $2.74B and $2.53B, respectively. This range acts as a solid support level.

$504.22: The recent trade at this price with high institutional buying activity suggests that this level could be a new support level if QQQ continues to rise.

3. Volume and Relative Size (RS)

Largest Trade on Nov 6 at $504.22: This trade with an RS of 134.02% reflects strong institutional demand at this price, potentially establishing $504 as a new support in an uptrend.

Consistent Large Trades Between $488 - $497: The strong RS values in this range confirm institutional accumulation, making it a robust support zone.

4. Support and Resistance Zones

Support Levels:

$487.60 - $488.40: This area has strong institutional support and is likely to hold in case of a pullback.

$497.25: Another potential support level, with significant buying activity in late October.

$504.22: With recent high-volume trades, this level could now act as a short-term support in the current uptrend.

Resistance Levels:

$514: QQQ is approaching all-time highs, and any further upward movement will likely face resistance around psychological levels like $515.

Conclusion:

Bullish Momentum: The recent institutional trades indicate strong bullish momentum, with substantial support between $487 - $497 and further buying at $504.

Key Levels to Watch: Watch for support at $487.60 - $488.40, $497.25, and $504.22. With QQQ reaching new highs, a sustained break above these levels could signal continued upside potential.

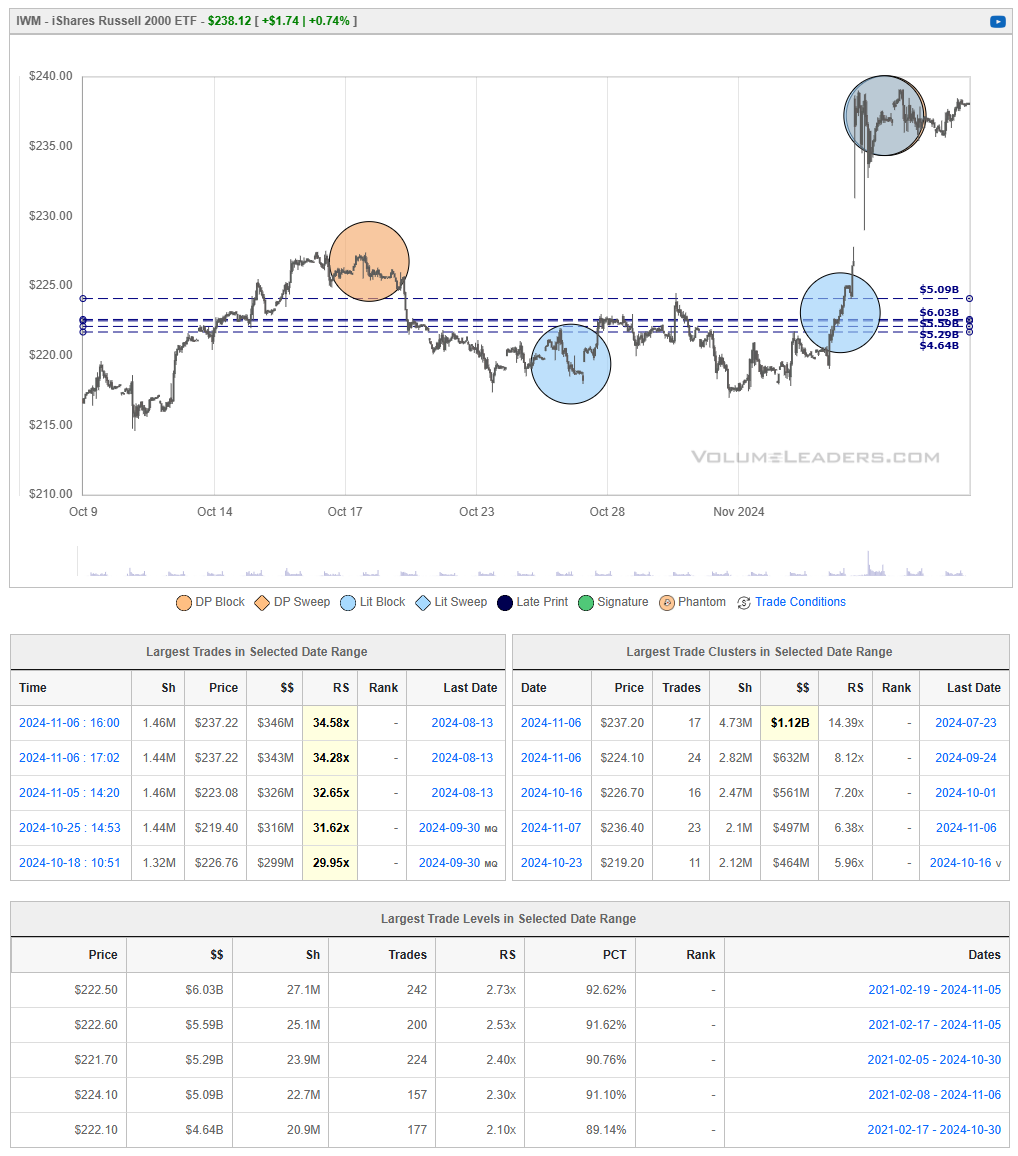

IWM 0.01%↑

1. Largest Trades (Highlighted Circles)

Notable Trades on Nov 6 ($237 Range): Significant trades took place on Nov 6 at $237.22 with a relative size (RS) of 34.58% and $237.03 with an RS of 34.28%. This indicates strong institutional buying interest around this price, likely establishing it as a key resistance level given the recent run-up.

Support Trades in the $220 - $222 Range (Late October): Large trades occurred around $220 to $222 in late October with RS values of 31.62% and 29.95%, showing institutional accumulation. This range now acts as a support zone.

2. Key Institutional Activity Price Levels (Dashed Blue Lines)

$222.50: This level saw heavy activity, with a cumulative total of $6.03B and an RS of 2.73x, indicating strong institutional support. This price level is expected to hold as a critical support zone.

$237 Range: The recent institutional buying around $237 suggests that this level could act as resistance if IWM attempts to move higher, as this is where selling pressure from profit-taking might occur.

3. Volume and Relative Size (RS)

Largest Trade on Nov 6 at $237.22: This trade, with an RS of 34.58%, highlights significant institutional interest, suggesting that $237.22 could act as a key short-term resistance.

Consistent Trades in $220 - $222 Range: The large trades and high RS values in this range suggest that it has strong institutional support.

4. Support and Resistance Zones

Support Levels:

$222.50: This level is well-supported by institutional trades, acting as a strong support zone if IWM retraces.

$220 - $221.70: This range, with consistent large trades, should provide additional support.

Resistance Levels:

$237 - $238: This area is likely to serve as a resistance zone based on the high-volume institutional trades that occurred recently.

Conclusion:

Bullish Bias with Resistance in Play: The recent institutional trades indicate strong support around $220 - $222. However, the price is approaching the $237 - $238 resistance zone, where institutional sellers might look to take profits.

Key Levels to Watch: Support at $222.50 and resistance around $237 - $238. If IWM can break above $238 with sustained buying, it may indicate further upside; otherwise, we may see consolidation or a pullback to the support zones.

DIA 0.00%↑

1. Largest Trades (Orange Circles)

Significant Trades Around $437 and $440 (Nov 1 - Nov 7): Notable trades took place at $437.39 with a relative size (RS) of 15.55% on Nov 1 and $440.00 on Nov 7. These trades indicate strong institutional buying interest, suggesting these levels could serve as a potential support zone if the price consolidates after the recent rally.

Support Trades in the $417 - $421 Range (Late October): Large trades around $417.67 - $421.80 with RS values up to 30.78% indicate institutional accumulation, making this range a critical support zone.

2. Key Institutional Activity Price Levels (Dashed Blue Lines)

$417.70 - $421.80: This range has substantial volume and institutional interest, with significant dollar amounts, marking it as a primary support zone.

$429.30: This level also shows notable activity and could act as intermediate support in case of a pullback.

$437 - $440: The recent institutional trades in this range indicate it may now act as a support area in the event of a minor retracement.

3. Volume and Relative Size (RS)

Largest Trade on Oct 31 at $417.67: This trade, with an RS of 30.78%, reflects strong institutional demand around this level, establishing it as a key support zone.

Consistent Large Trades Between $437 - $440: The high RS values in this range confirm institutional buying activity, suggesting it could act as a short-term support in an uptrend.

4. Support and Resistance Zones

Support Levels:

$417.70 - $421.80: This level is reinforced by consistent institutional activity and is expected to serve as a solid support zone.

$429.30: This price level has institutional backing and could provide intermediate support if DIA pulls back.

$437 - $440: The recent trades suggest this area may act as near-term support given the recent buying interest.

Resistance Levels:

DIA is currently trading near its recent highs, so a move above the current levels may face psychological resistance around $445 - $450.

Conclusion:

Bullish Momentum with Strong Support Zones: The recent institutional trades indicate strong bullish momentum, with substantial support between $417 - $421, as well as $437 - $440 providing near-term backing.

Key Levels to Watch: Support at $417.70 - $421.80, intermediate support at $429.30, and near-term support around $437 - $440. DIA's movement above these levels could signal continued bullish momentum, but a break below $417 could suggest further downside pressure.

Last Week’s Top Institutional Order Flow

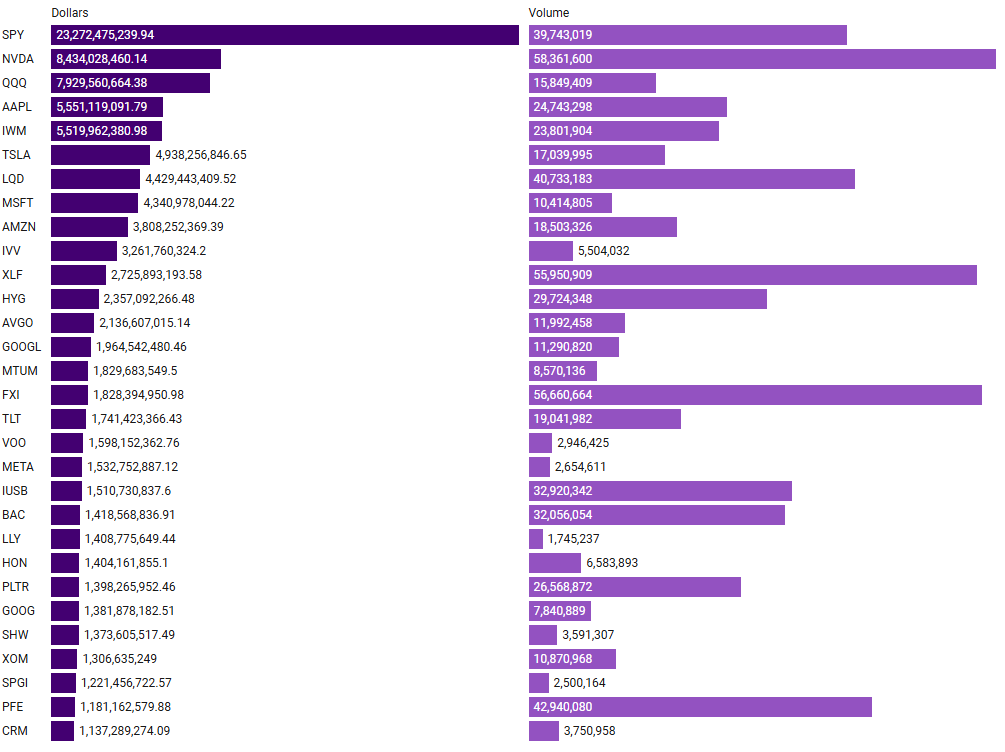

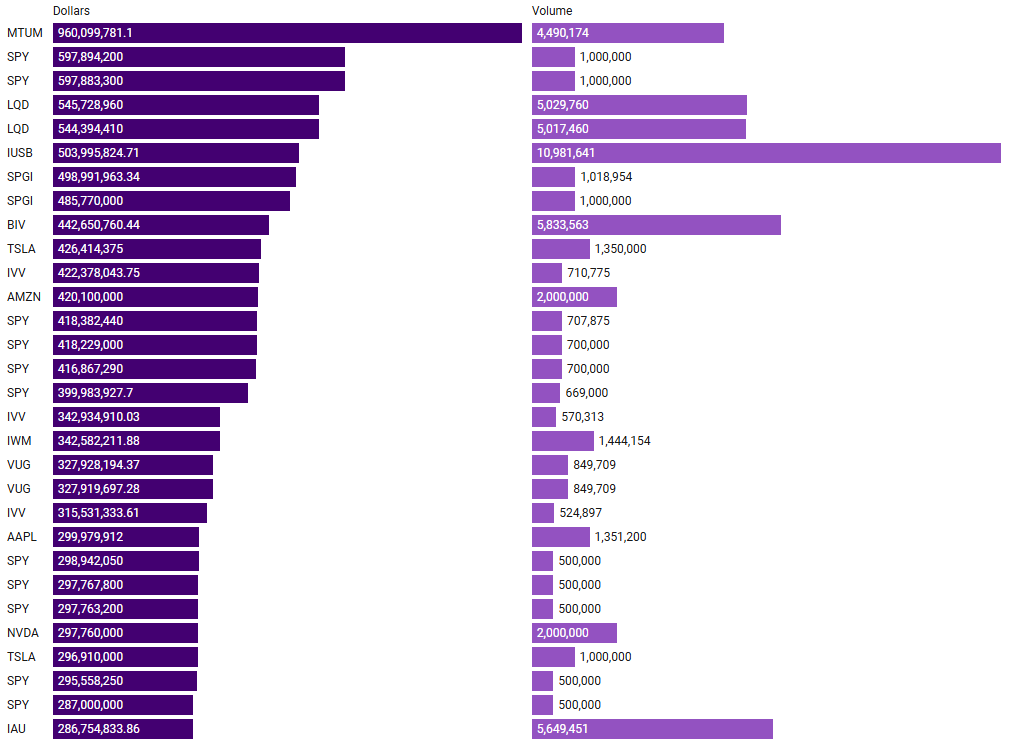

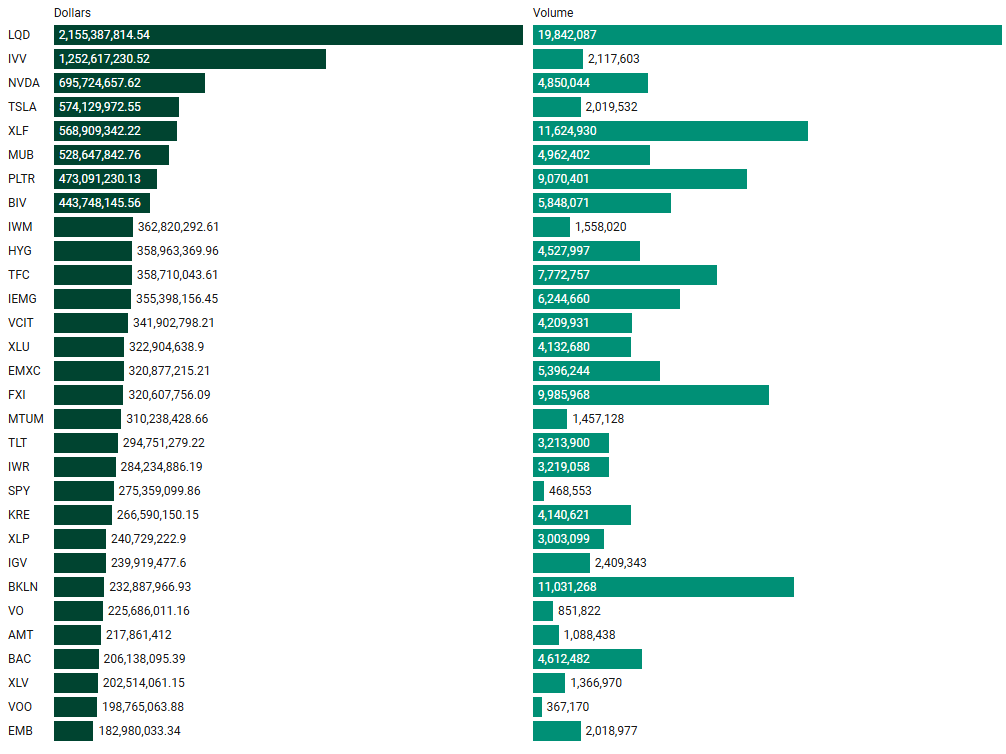

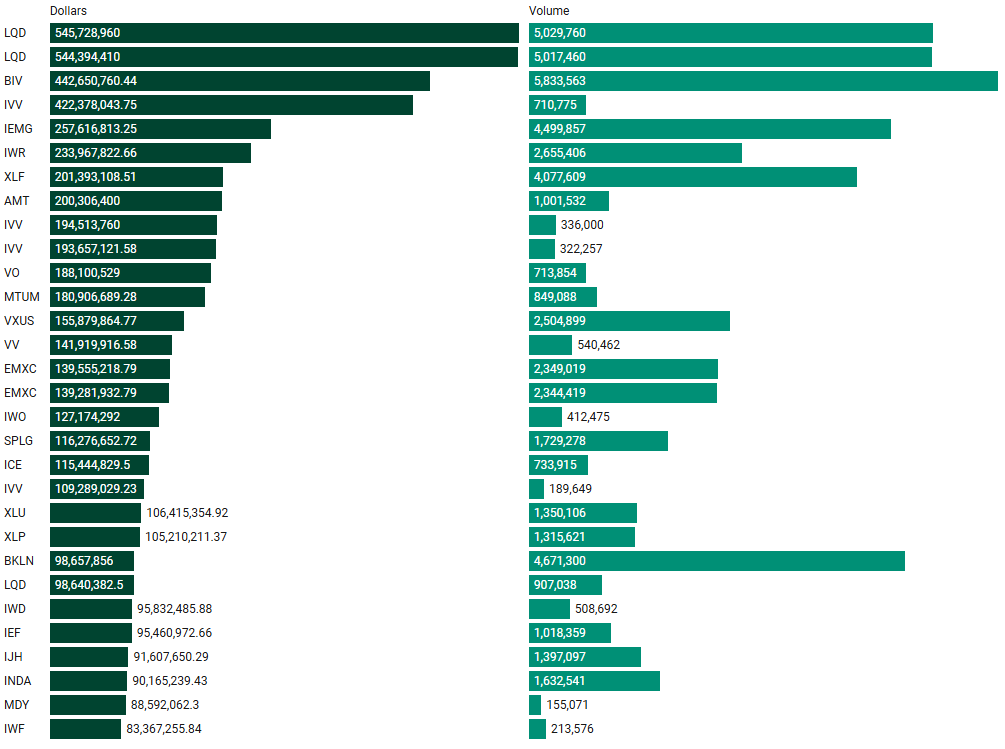

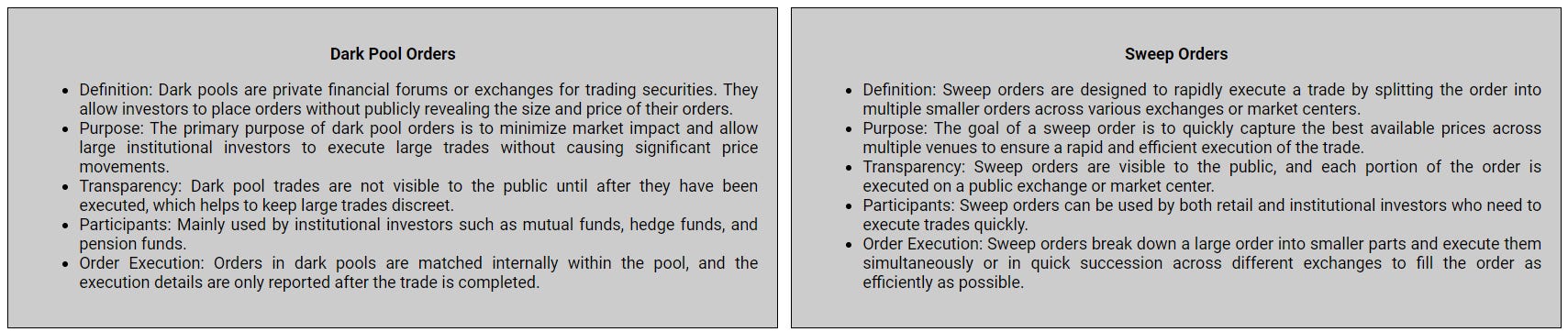

Many excellent trade ideas and sources of inspiration can be found in these prints. While only the top 30 from each group are displayed, the complete results are accessible in VolumeLeaders.com for you to explore at your convenience any time. Remember to configure trade alerts within the platform to ensure you never overlook institutional order flows that capture your interest or are significant to you. The blue charts encompass all types of trades, including blocks on lit exchanges; the purple charts exclusively depict dark pool trades; and the green charts represent sweeps only.

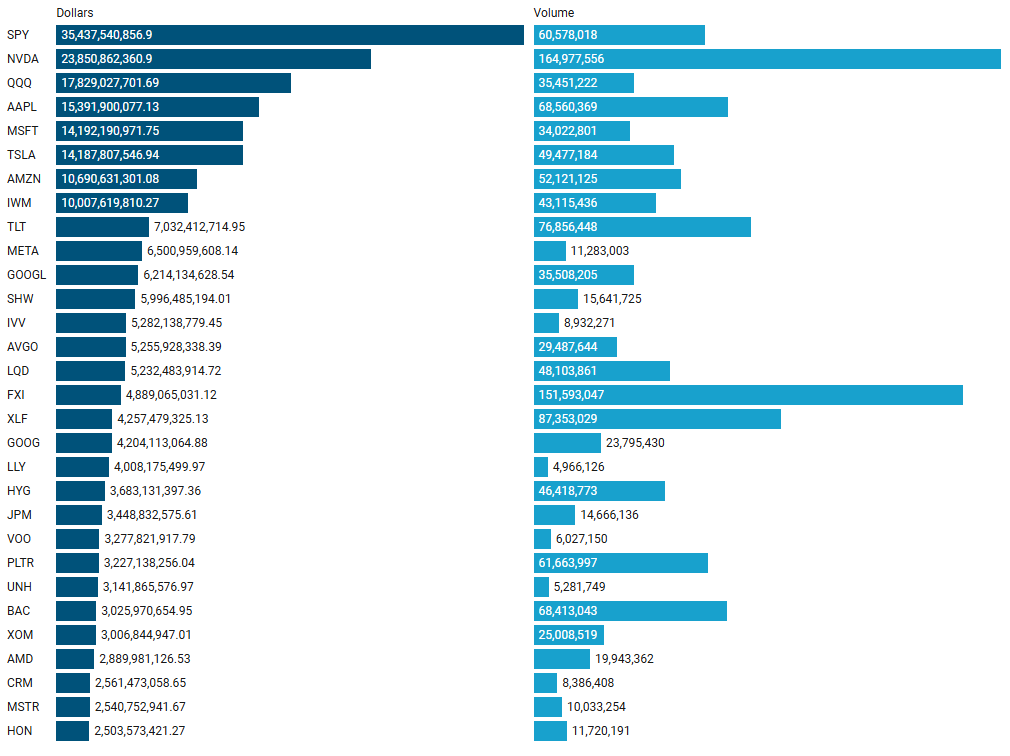

Top Aggregate Dollars Transacted by Ticker

Largest Individual Trades by Dollars Transacted

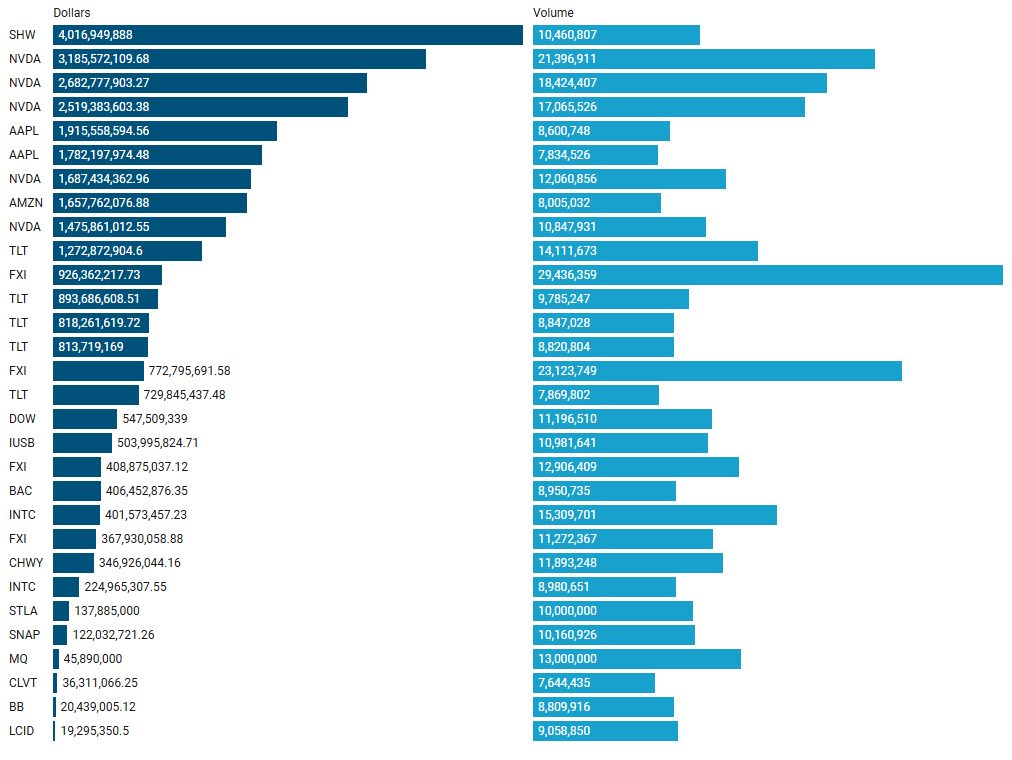

Top Aggregate Dark Pool Activity by Ticker

Largest Individual Dark Pool Blocks by Dollars

Top Aggregate Sweeps by Ticker

Top Individual Sweeps by Dollars Transacted

Investments In Focus: Bull vs Bear Arguments

Please read “Institutional S/R Levels For Major Indices” at the top of this stack to understand the nature and importance of what we’re looking at here visually. Institutions leave footprints that VolumeLeaders.com can illustrate for you while providing context to assess things like institutional conviction and urgency. Theses and data given below are not financial advice, just personal observations that may be wrong; consult a certified financial advisor before making any investment decisions.

PTON 0.11%↑

🐂 Bull Thesis 🐂

Strategic Leadership Appointment: Peloton has appointed Peter Stern, co-founder of Apple Fitness+, as its new CEO, effective January 1, 2025. Stern's extensive experience in hardware, software, and subscription services is expected to drive innovation and growth.

Improved Financial Performance: In the fiscal first quarter ending September 30, 2024, Peloton reported a net loss of $1 million, significantly narrower than the $159.3 million loss in the same period the previous year. Revenue reached $586 million, surpassing analyst expectations.

Expansion of Subscription Services: Peloton's subscription revenue increased to $426.3 million, up from $415 million year-over-year, indicating a growing and engaged user base. The company ended the quarter with over 6 million members and 2.9 million paid connected fitness subscribers.

Cost-Saving Initiatives: Peloton aims to achieve more than $200 million in run-rate cost savings by the end of fiscal 2025 through restructuring plans, including workforce reductions and operational efficiencies.

Strategic Partnerships and Market Expansion: The company announced a partnership with Costco to sell its Bike+ in 300 stores and online, aiming to attract new and younger customers. Additionally, Peloton is testing small-store concepts and targeting more male customers to diversify its user base.

🐻 Bear Thesis 🐻

Declining Hardware Sales: Sales from connected fitness products fell to $159.6 million from $180.6 million year-over-year, reflecting a continued decline in hardware sales since Q3 2022.

Post-Pandemic Demand Challenges: Peloton experienced a surge in demand during the COVID-19 pandemic, but as restrictions eased, the company faced challenges in maintaining growth, leading to supply chain issues and receding demand.

Operational and Financial Struggles: The company has faced significant financial challenges, including workforce reductions and strategic pivots towards subscription services, indicating ongoing operational difficulties.

Competitive Market Landscape: The at-home fitness market has become increasingly competitive, with new entrants and existing companies offering alternative products and services, potentially impacting Peloton's market share.

Uncertain Long-Term Profitability: Despite recent improvements, Peloton's path to sustained profitability remains uncertain, with concerns about its ability to balance growth initiatives with cost management effectively.

META -0.16%↓

🐂 Bull Thesis 🐂

Strong Financial Performance: In Q3 2024, Meta reported revenues of $40.6 billion, a 19% year-over-year increase, driven by a 7% rise in ad impressions and an 11% growth in average price per ad.

Robust User Growth: The company experienced a 5% rise in family daily active people, reaching 3.29 billion users, indicating sustained engagement across its platforms.

AI Integration and Innovation: Meta's strategic focus on artificial intelligence has enhanced its advertising capabilities and user experience, contributing to revenue growth and operational efficiency.

Diversified Revenue Streams: Beyond advertising, Meta is expanding into areas like virtual reality and the metaverse through its Reality Labs segment, aiming to create new revenue opportunities and reduce reliance on ad income.

Positive Market Sentiment: Analysts maintain a favorable outlook on Meta, with price targets ranging from $600 to $640, reflecting confidence in the company's growth prospects and strategic direction.

🐻 Bear Thesis 🐻

Rising Operational Costs: Meta's expenses are expected to increase significantly in 2025 due to substantial investments in AI and infrastructure, which could pressure profit margins.

Regulatory Challenges: The company faces ongoing scrutiny over data privacy and antitrust issues, which may result in fines, operational restrictions, or increased compliance costs.

Intense Competition: Meta contends with strong competitors in social media, advertising, and emerging technologies, potentially impacting user growth and market share.

Reality Labs Financial Losses: The Reality Labs division, focusing on AR, VR, and metaverse products, continues to incur heavy losses, with expectations for increased spending next year.

Market Volatility: Despite strong financial performance, Meta's stock has experienced fluctuations, with a recent dip of over 3% following the Q3 earnings call, indicating sensitivity to market sentiment and investor expectations.

HIMS 0.00%↑

🐂 Bull Thesis 🐂

Robust Revenue Growth: In Q3 2024, Hims & Hers reported revenues of $401.6 million, marking a 77% year-over-year increase. This substantial growth underscores the company's expanding market presence and effective business strategies.

Expanding Subscriber Base: The company achieved a 43% increase in subscribers, reaching 1.9 million. This growth reflects strong consumer demand for its telehealth services and successful customer acquisition efforts.

Diversified Product Offerings: Hims & Hers has broadened its product portfolio to include treatments for anxiety and weight loss, such as GLP-1 injections. This diversification caters to a wider range of healthcare needs, potentially attracting a broader customer base.

Positive Financial Outlook: The company raised its full-year sales forecast to $1.37-$1.4 billion, up from a previous estimate of $1.2-$1.23 billion, indicating confidence in sustained revenue growth.

Market Confidence and Stock Performance: Shares of Hims & Hers have doubled in value this year, reflecting strong market confidence in the company's growth trajectory and strategic direction.

🐻 Bear Thesis 🐻

Regulatory Uncertainties: The company's reliance on compounded versions of GLP-1 weight-loss treatments, which are not FDA-approved, exposes it to potential regulatory challenges that could impact product availability and sales.

Competitive Market Landscape: The telehealth sector is becoming increasingly competitive, with new entrants and established healthcare providers expanding their digital services, potentially affecting Hims & Hers' market share and pricing power.

Dependence on Specific Treatments: A significant portion of the company's growth is tied to specific treatments like hair-loss solutions and weight-loss drugs. Any negative developments or reduced demand in these areas could adversely affect overall performance.

Profitability Concerns: Despite strong revenue growth, the company has yet to achieve consistent profitability. Sustained investments in marketing and product development may continue to pressure margins in the near term.

Stock Volatility: The stock has experienced significant volatility, with recent fluctuations influenced by regulatory news and market sentiment. This volatility may pose risks for investors seeking stable returns.

CRM 0.09%↑

🐂 Bull Thesis 🐂

Strong Financial Performance: Salesforce reported a 19% year-over-year increase in revenue for Q3 2024, reaching $40.6 billion. This growth was driven by a 7% rise in ad impressions and an 11% increase in average price per ad.

Robust User Growth: The company experienced a 5% rise in family daily active people, reaching 3.29 billion users, indicating sustained engagement across its platforms.

AI Integration and Innovation: Salesforce's strategic focus on artificial intelligence has enhanced its advertising capabilities and user experience, contributing to revenue growth and operational efficiency.

Diversified Revenue Streams: Beyond advertising, Salesforce is expanding into areas like virtual reality and the metaverse through its Reality Labs segment, aiming to create new revenue opportunities and reduce reliance on ad income.

Positive Market Sentiment: Analysts maintain a favorable outlook on Salesforce, with price targets ranging from $600 to $640, reflecting confidence in the company's growth prospects and strategic direction.

🐻 Bear Thesis 🐻

Rising Operational Costs: Salesforce's expenses are expected to increase significantly in 2025 due to substantial investments in AI and infrastructure, which could pressure profit margins.

Regulatory Challenges: The company faces ongoing scrutiny over data privacy and antitrust issues, which may result in fines, operational restrictions, or increased compliance costs.

Intense Competition: Salesforce contends with strong competitors in social media, advertising, and emerging technologies, potentially impacting user growth and market share.

Reality Labs Financial Losses: The Reality Labs division, focusing on AR, VR, and metaverse products, continues to incur heavy losses, with expectations for increased spending next year.

Market Volatility: Despite strong financial performance, Salesforce's stock has experienced fluctuations, with a recent dip of over 3% following the Q3 earnings call, indicating sensitivity to market sentiment and investor expectations.

U 0.00%↑

🐂 Bull Thesis 🐂

Market Leadership in Real-Time 3D Development: Unity is a leading platform for creating and operating interactive, real-time 3D content, widely used across gaming, automotive, architecture, and other industries. This strong market position provides a solid foundation for growth.

Diversified Revenue Streams: Unity generates revenue through a combination of software subscriptions, services, and asset store sales, reducing dependence on any single income source and enhancing financial stability.

Strategic Initiatives and Partnerships: The company is actively pursuing strategic initiatives and partnerships to expand its market reach and enhance its product offerings, positioning it well for future growth.

Analyst Optimism: Analysts have expressed positive sentiments, with an average price target of $24.10, representing an 11.47% increase from the current price, and a consensus rating of "Hold."

Commitment to Innovation: Unity's focus on innovation, particularly in areas like augmented reality and virtual reality, positions it to capitalize on emerging trends and maintain its competitive edge.

🐻 Bear Thesis 🐻

Financial Challenges: Unity reported a net loss of $125.6 million in the latest quarter, indicating ongoing financial challenges that may impact its ability to invest in growth initiatives.

Revenue Decline: The company experienced a 16% drop in revenue for the latest quarter, totaling $449 million, which, despite surpassing analysts' expectations, reflects underlying business challenges.

Operational Restructuring: Unity is undergoing a transformation under new leadership, targeting the $150 billion mobile advertising market with plans to accelerate product innovation, which may involve execution risks.

Reduced Financial Outlook: Despite a better-than-expected second quarter, Unity decreased its full-year revenue outlook to $1.68-$1.69 billion from its previous $1.76-$1.80 billion, indicating a more cautious approach to recovery.

Management Turnover: The departure of CFO Luis Visoso and the appointment of an interim CFO may lead to potential disruptions in financial strategy and execution.

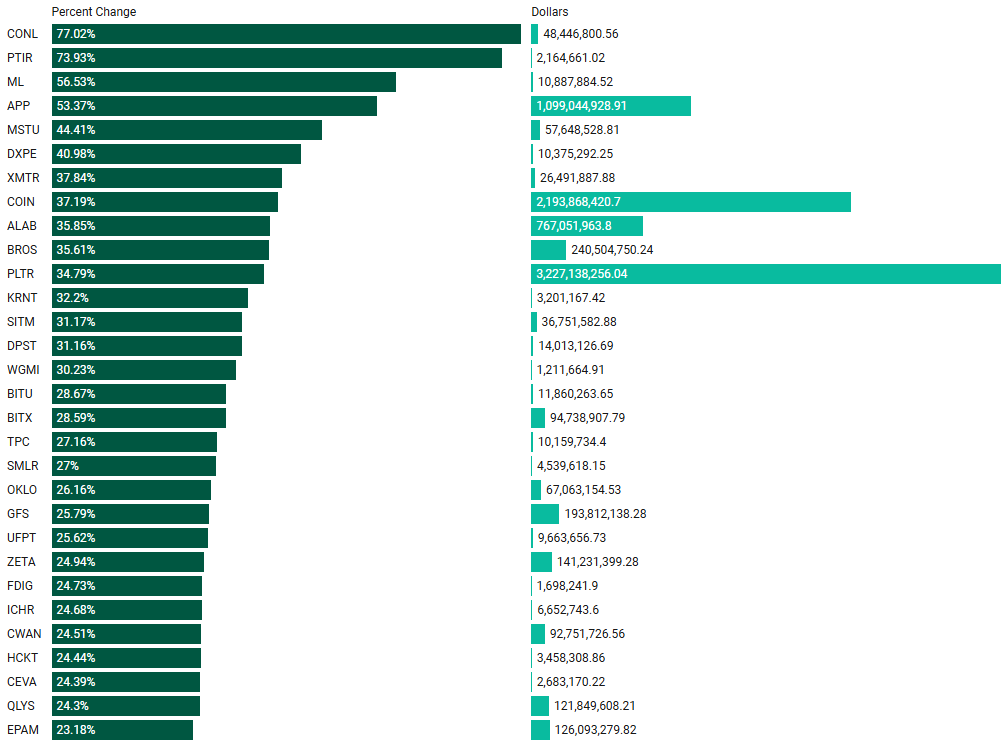

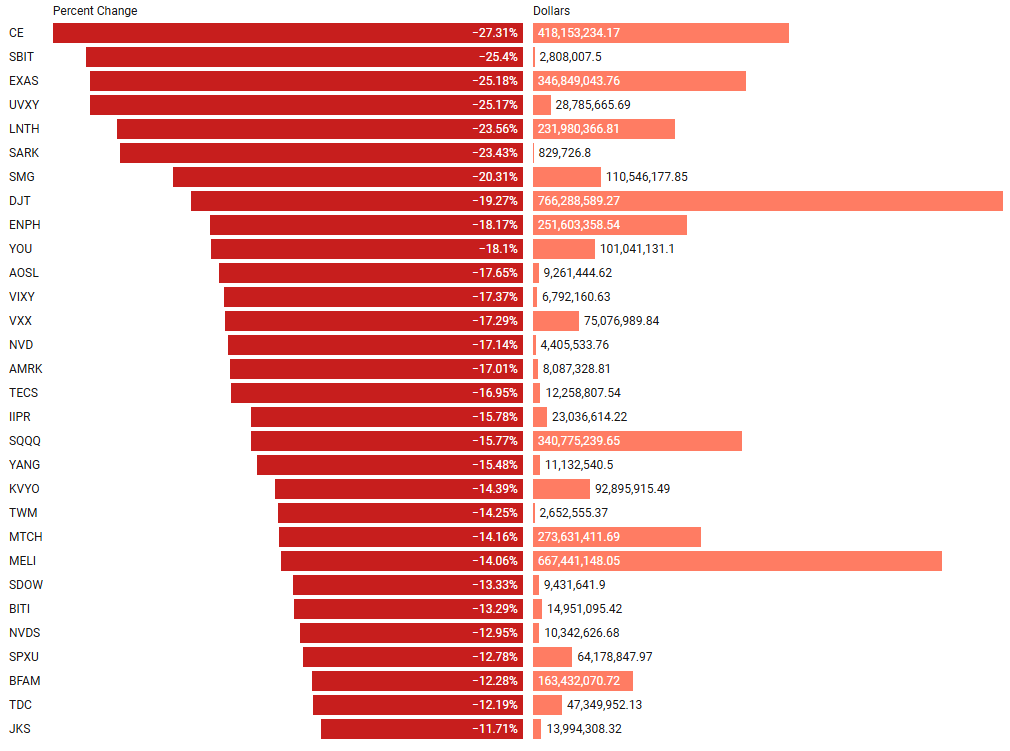

Last Week’s Institutionally-Backed Gainers & Losers

If you’re going to bet on a name, consider one that is officially endorsed by an institution! These are the top percent gainers (green) and percent losers (red) from this week’s open-to-close that had a trade price greater than $20 and institutional involvement. Continue watching tickers from this and prior stacks as these names frequently turn into multi-leg trades with a lot of movement!

Top Institutionally Backed Gainers

Top Institutionally Backed Losers

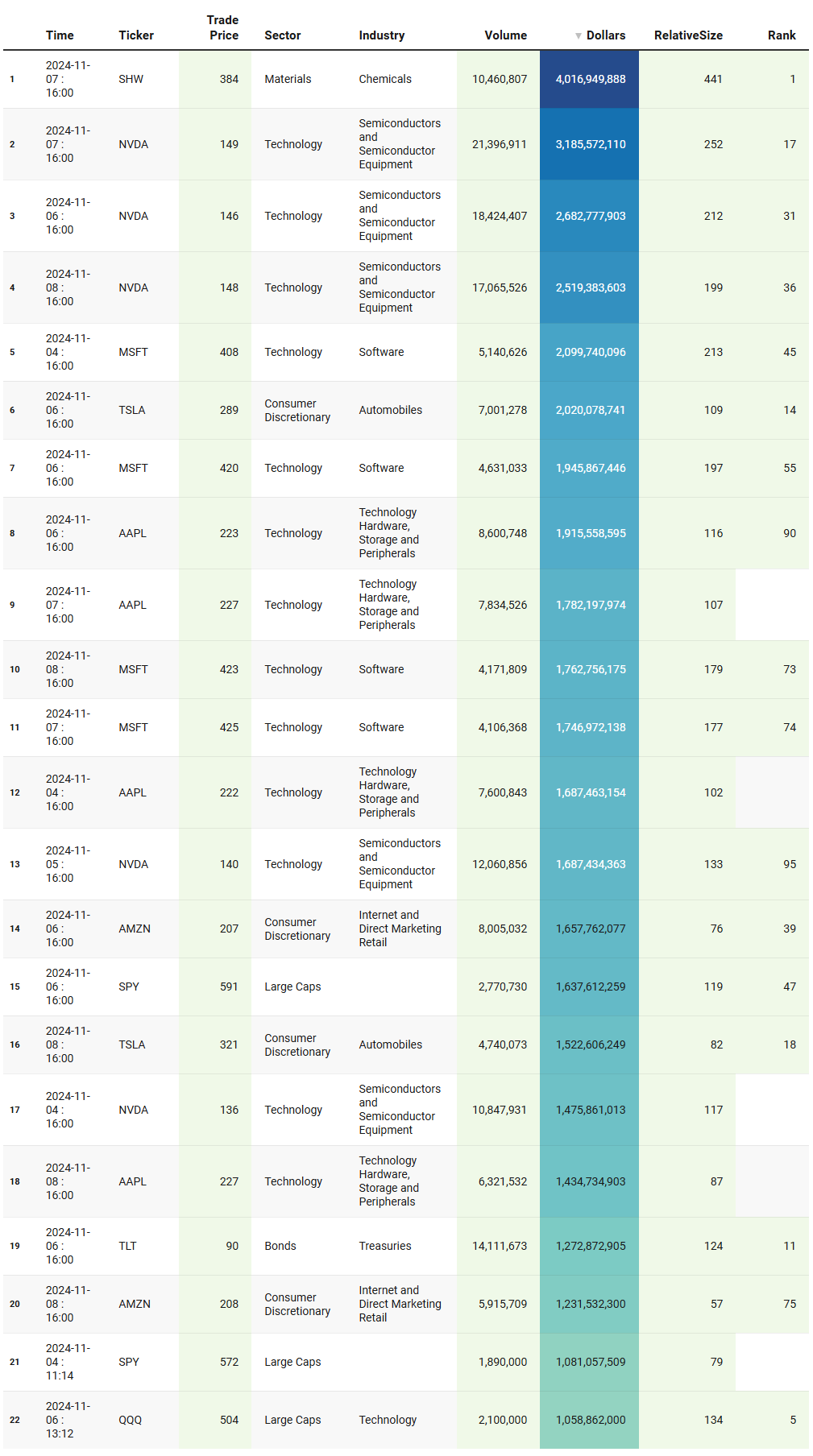

Last Week’s Billion Dollar Prints

Tickers that printed a trade worth at least $1B last week get a special shout-out… Welcome to the club. Subs should login to VolumeLeaders.com to get the exact trade price and relevant institutional levels around the trade - these are massive commitments by institutions that should not be ignored.

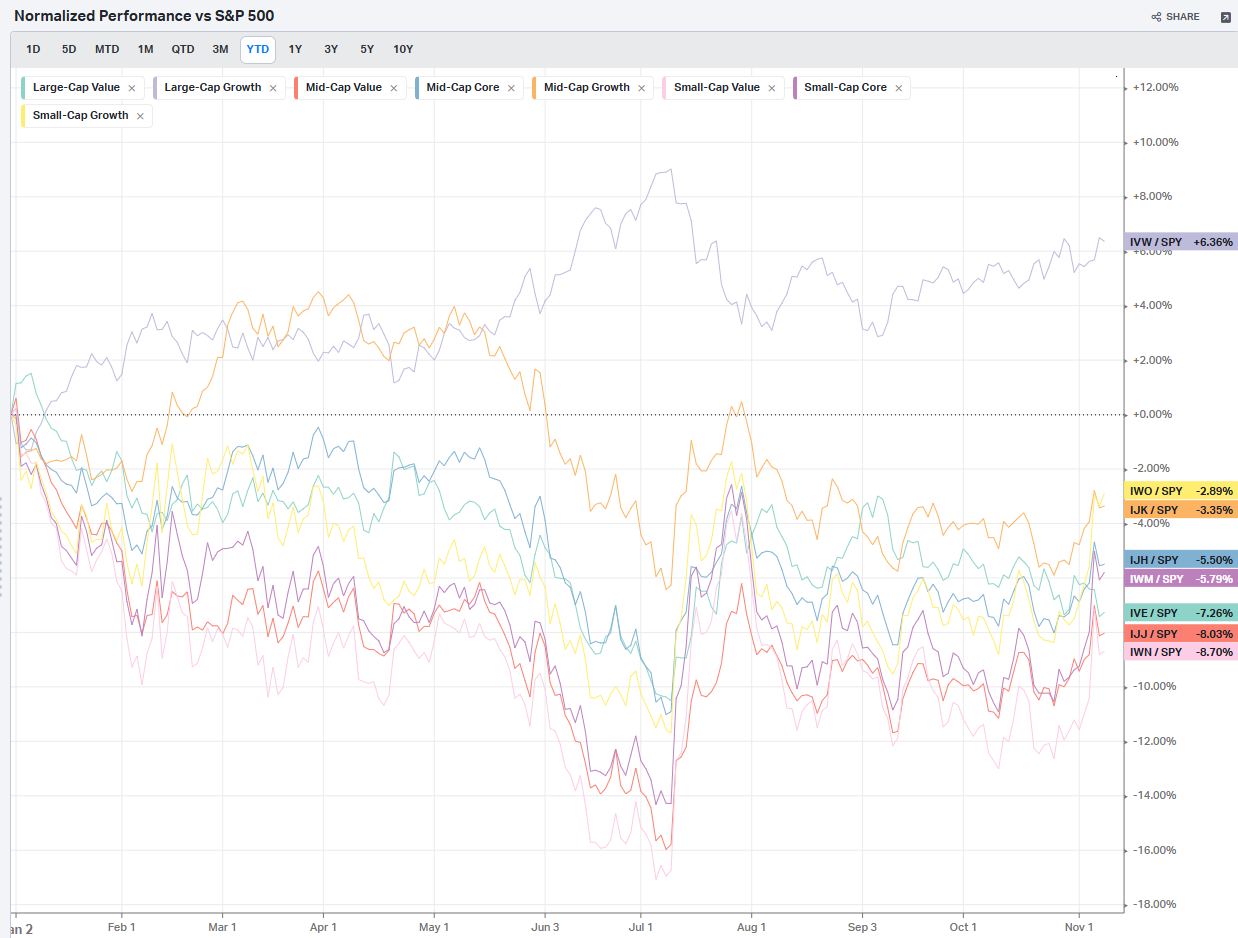

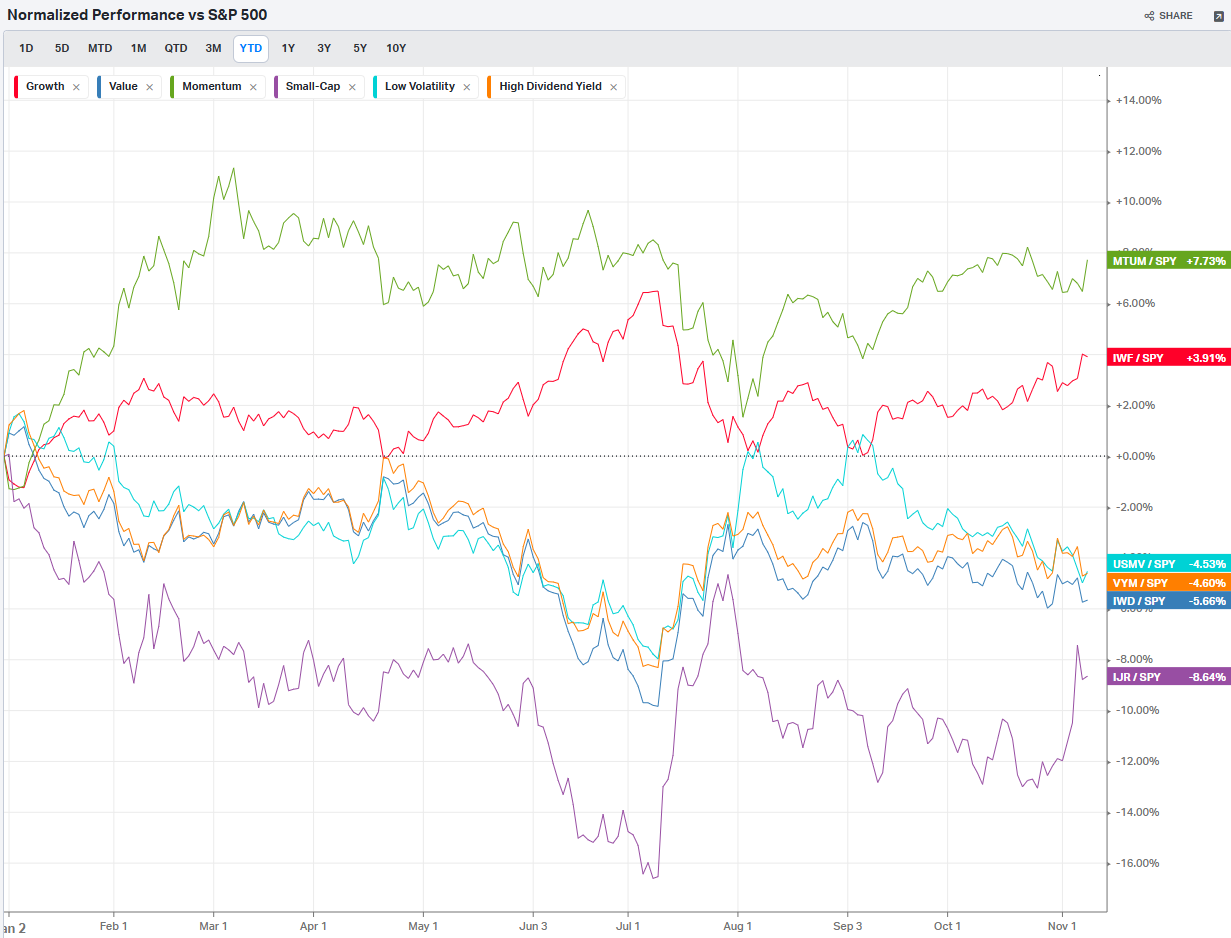

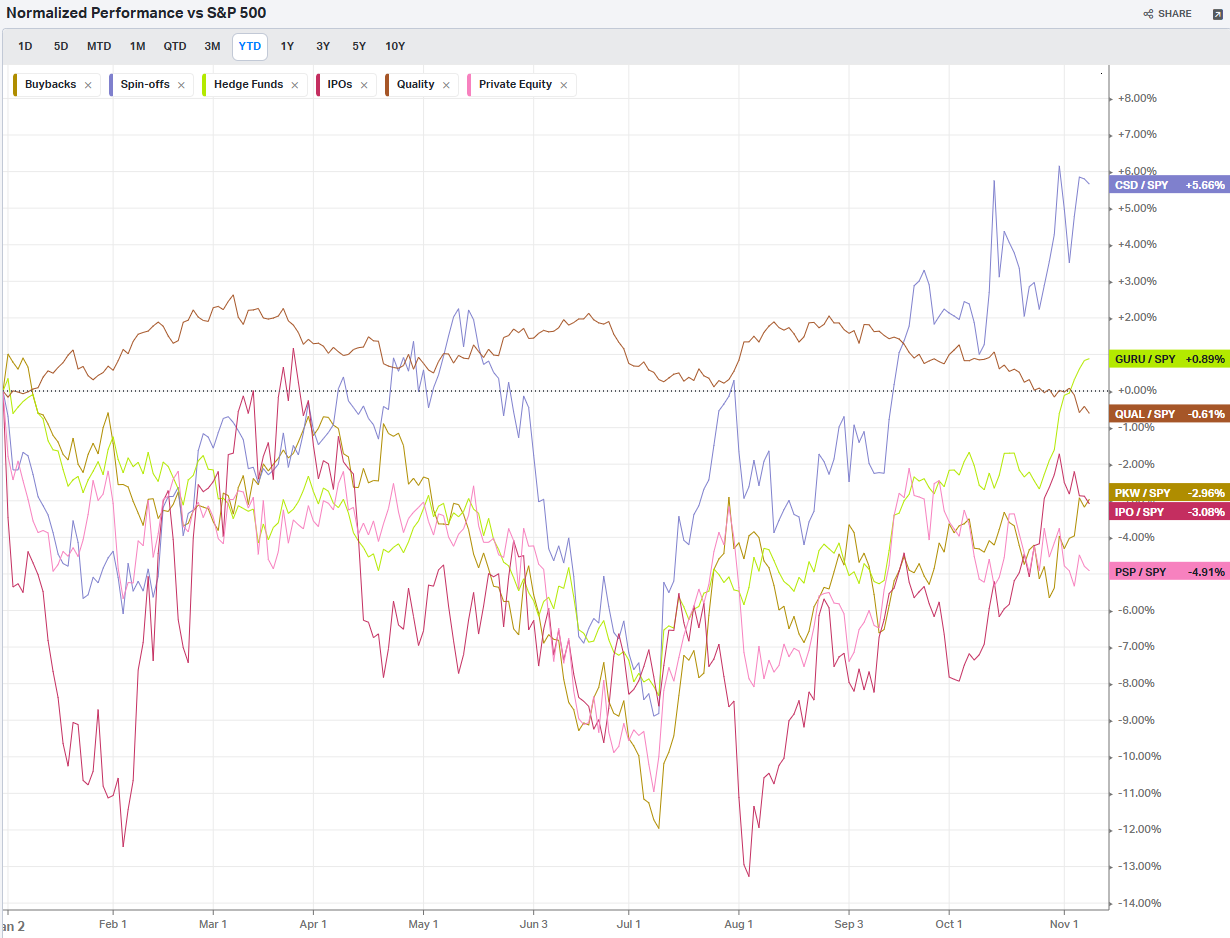

Summary Of Thematic Performance YTD

VolumeLeaders.com provides a lot of pre-built filters for thematics so that you can quickly dive into specific areas of the market. These performance overviews are provided here only for inspiration. Consider targeting leaders and/or laggards in the best and worst sectors, for example.

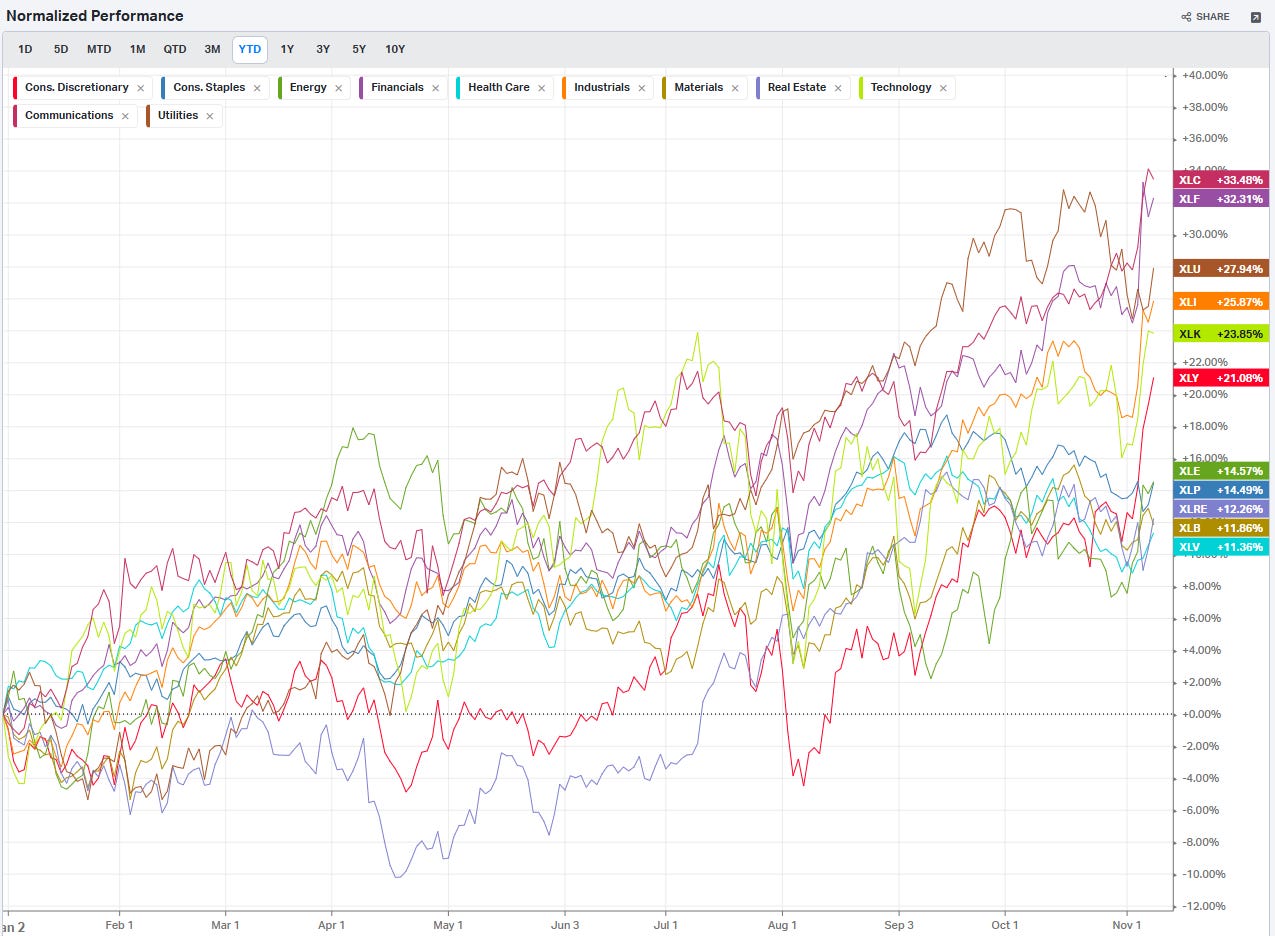

S&P By Sector

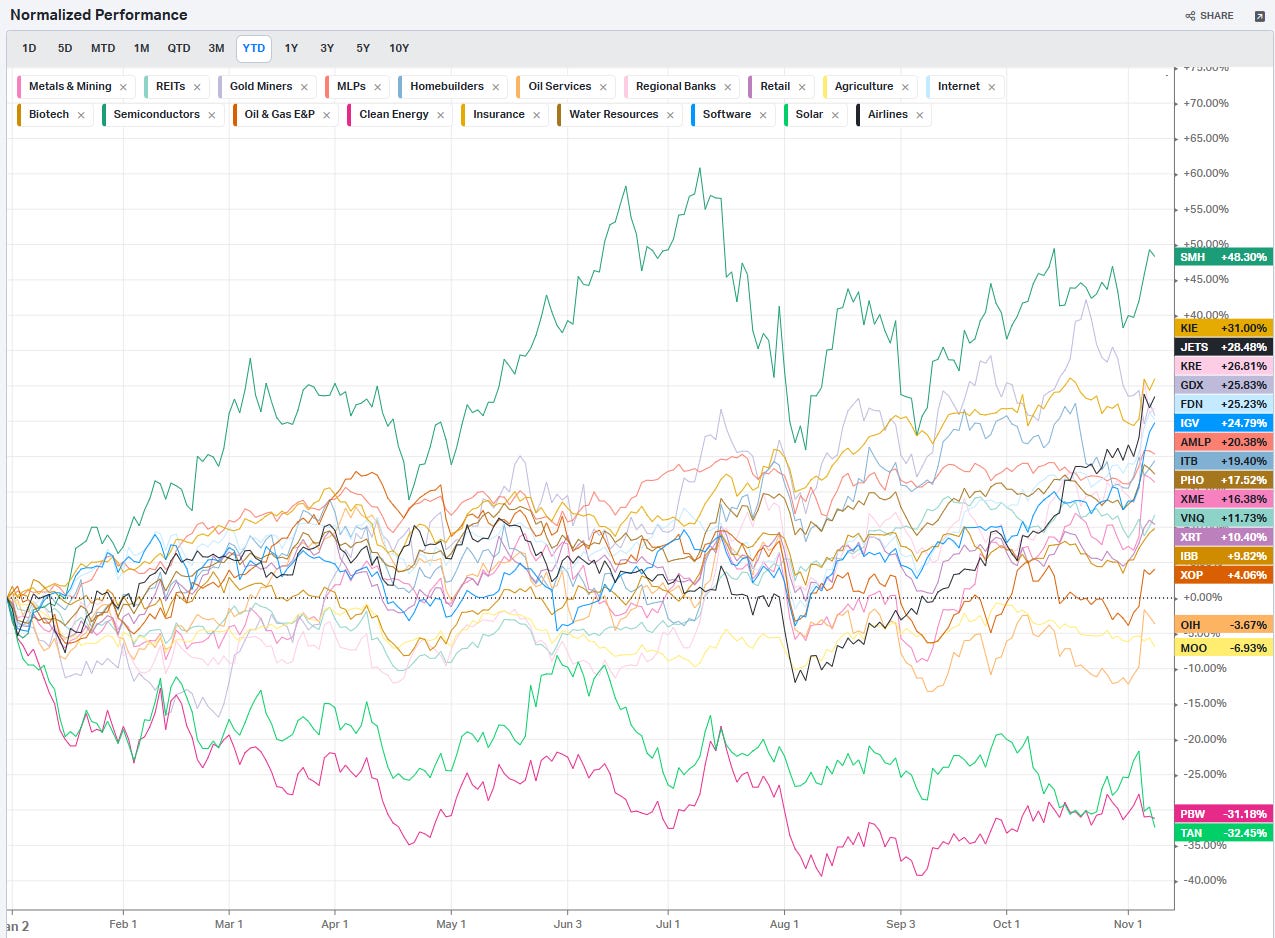

S&P By Industry

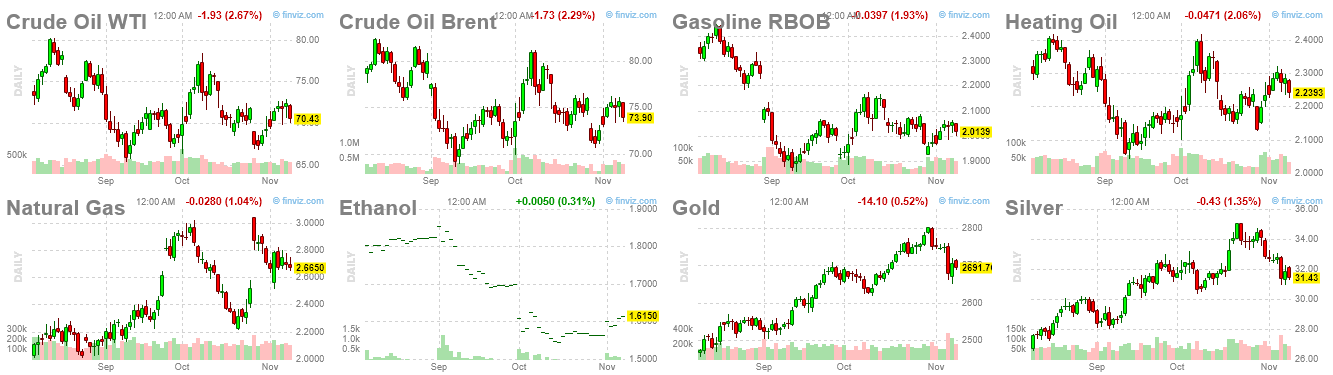

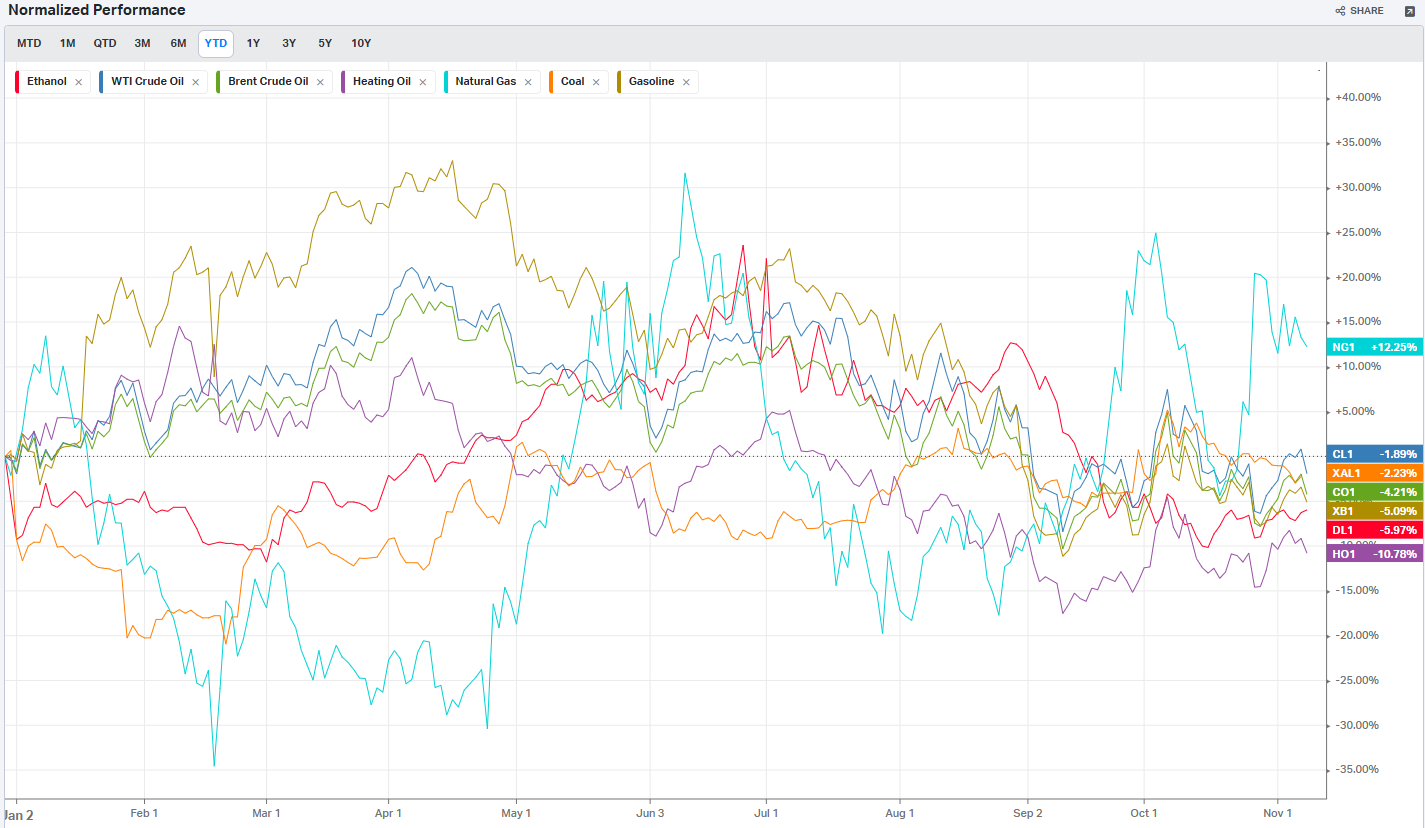

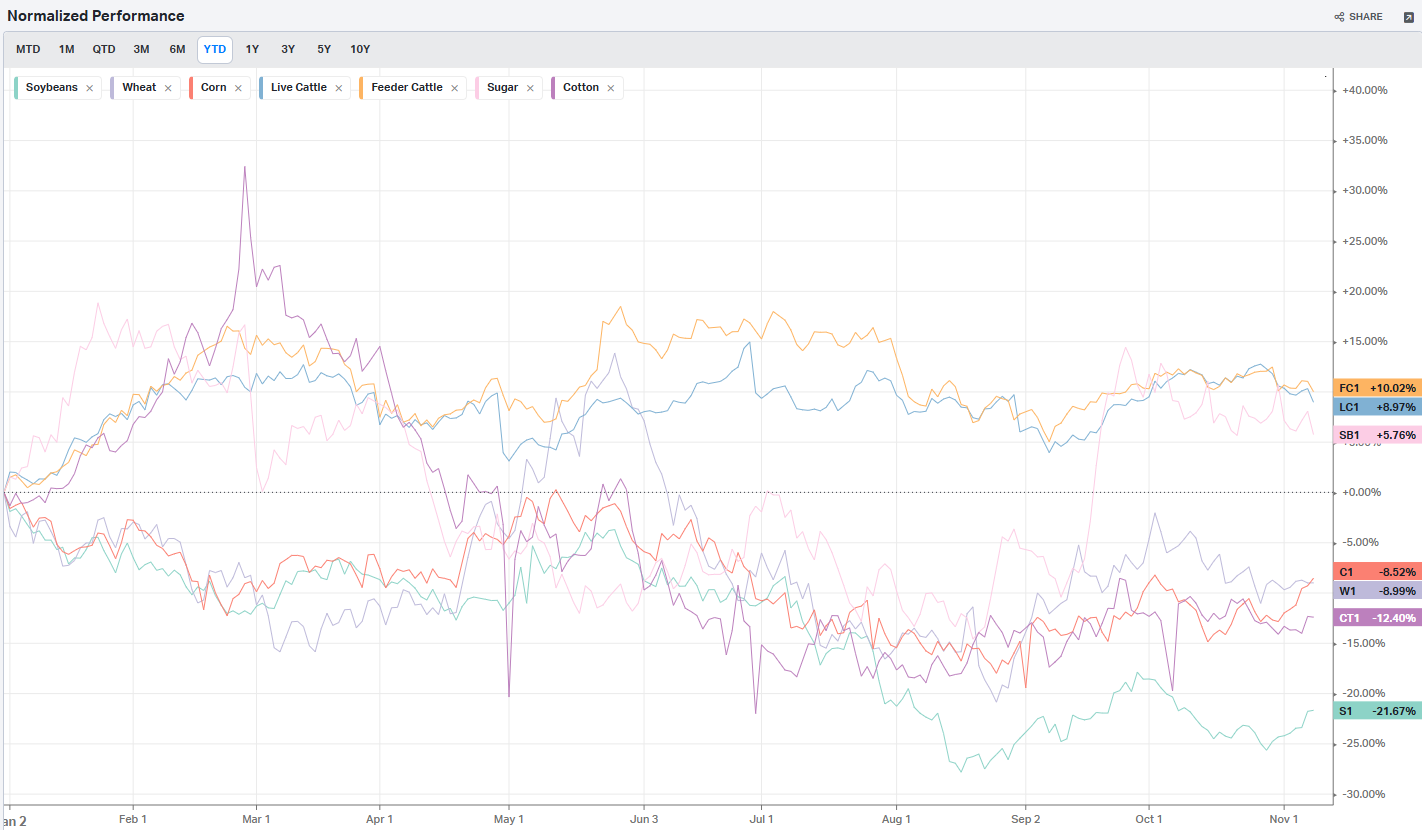

Commodities: Energy

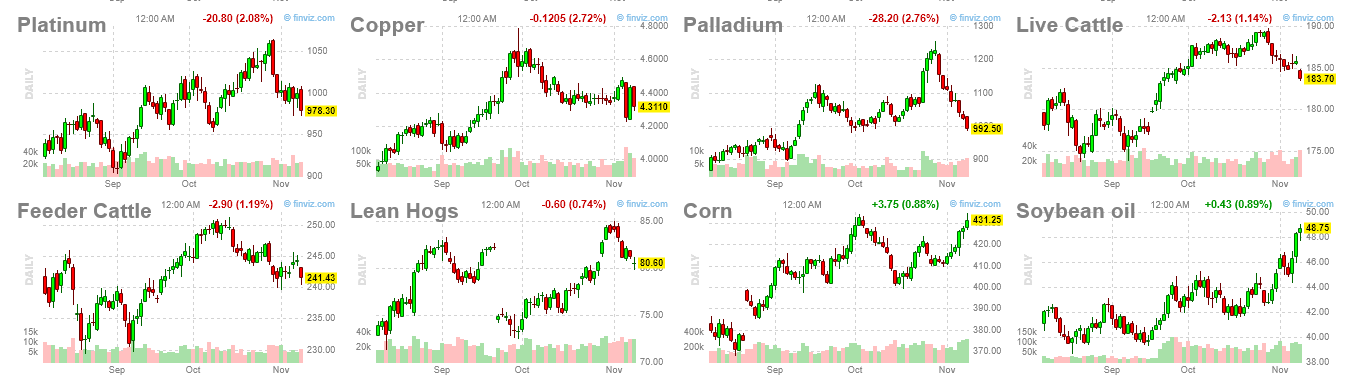

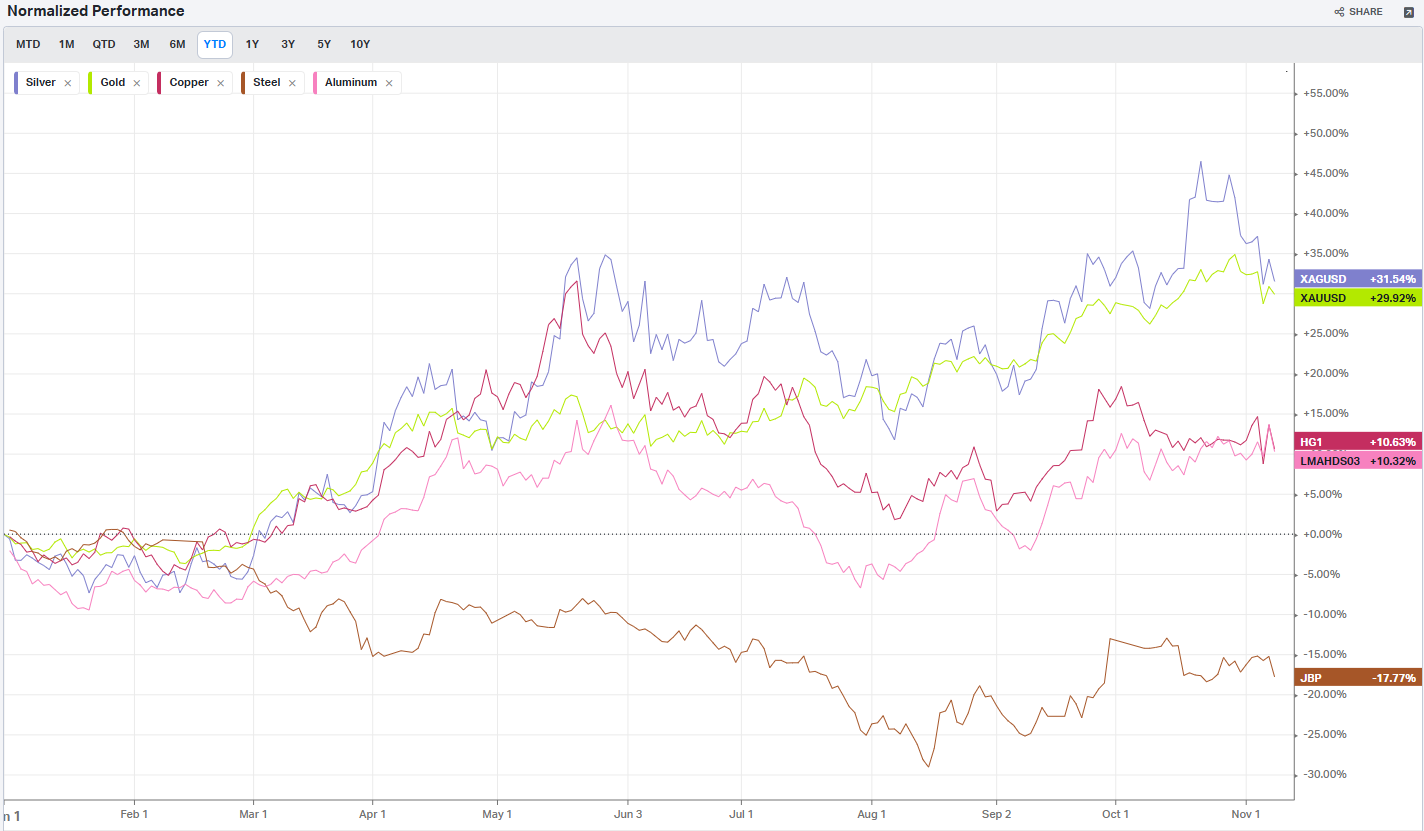

Commodities: Metals

Commodities: Agriculture

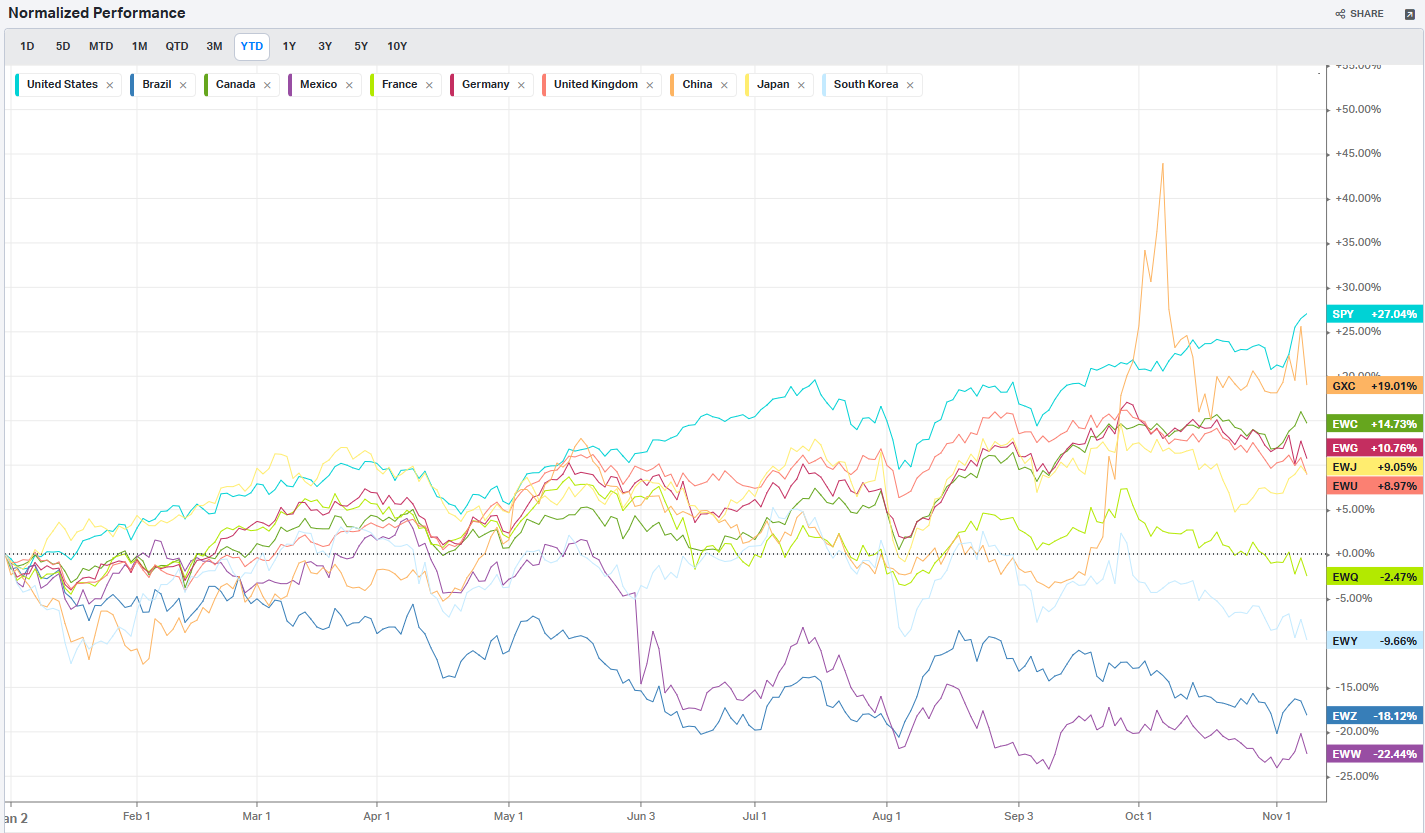

Country ETFs

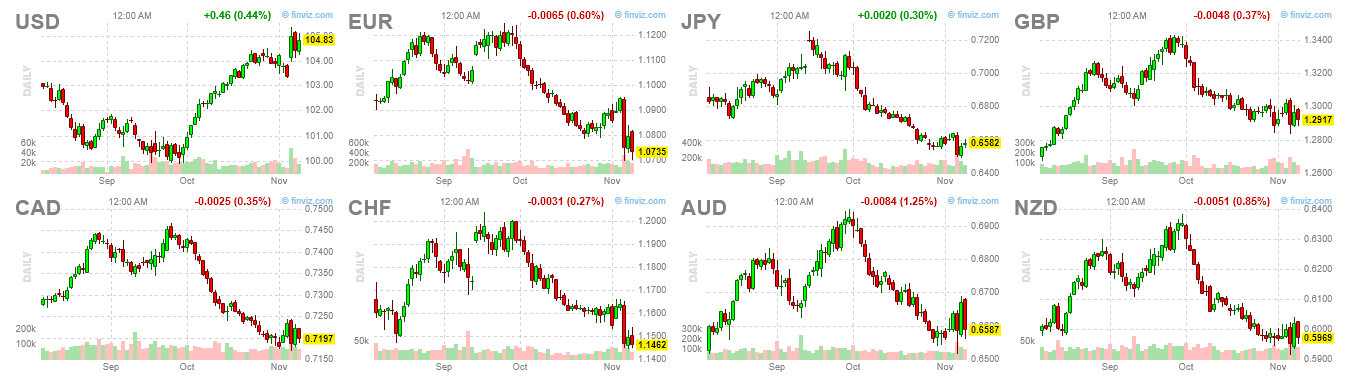

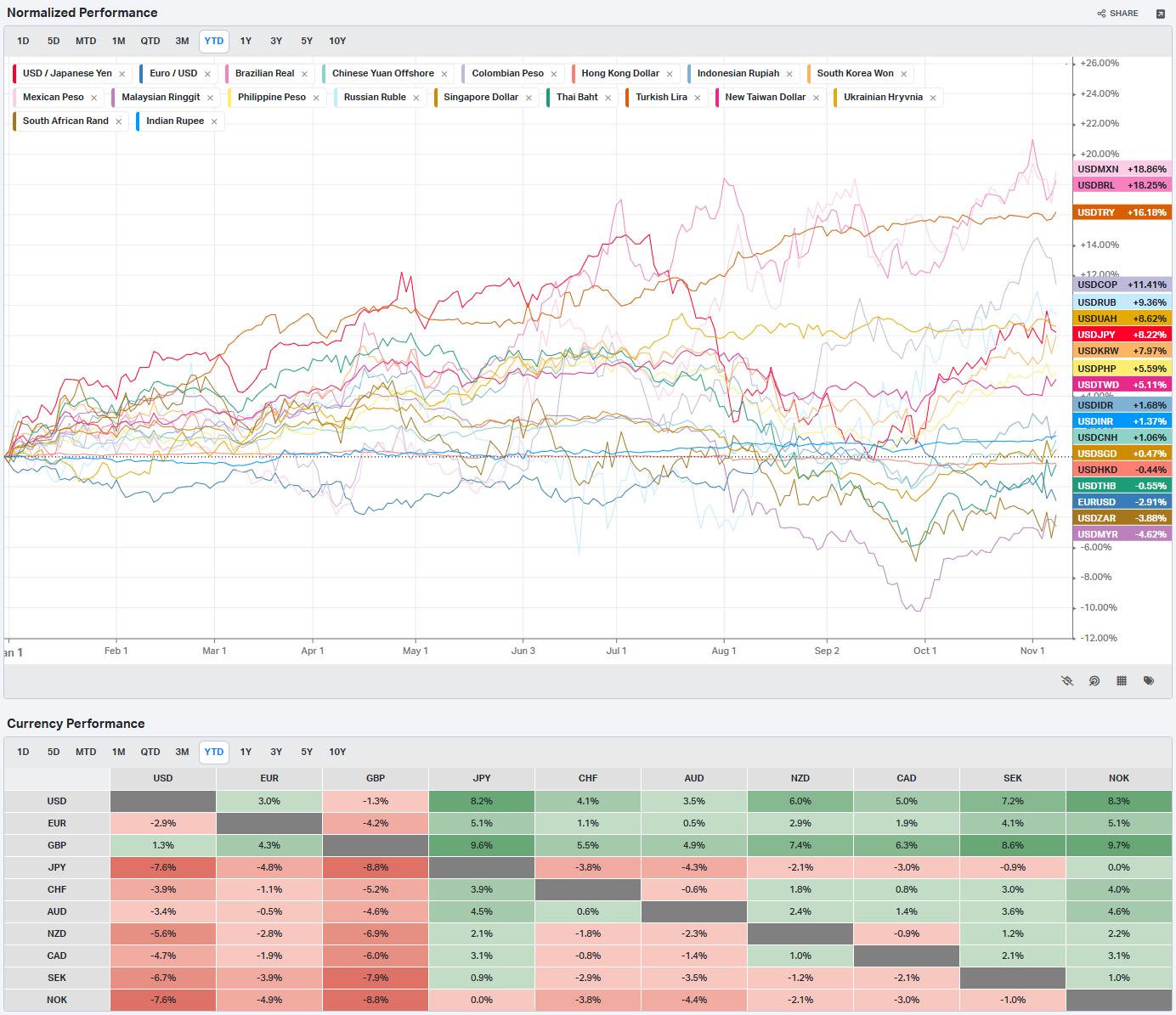

Currencies

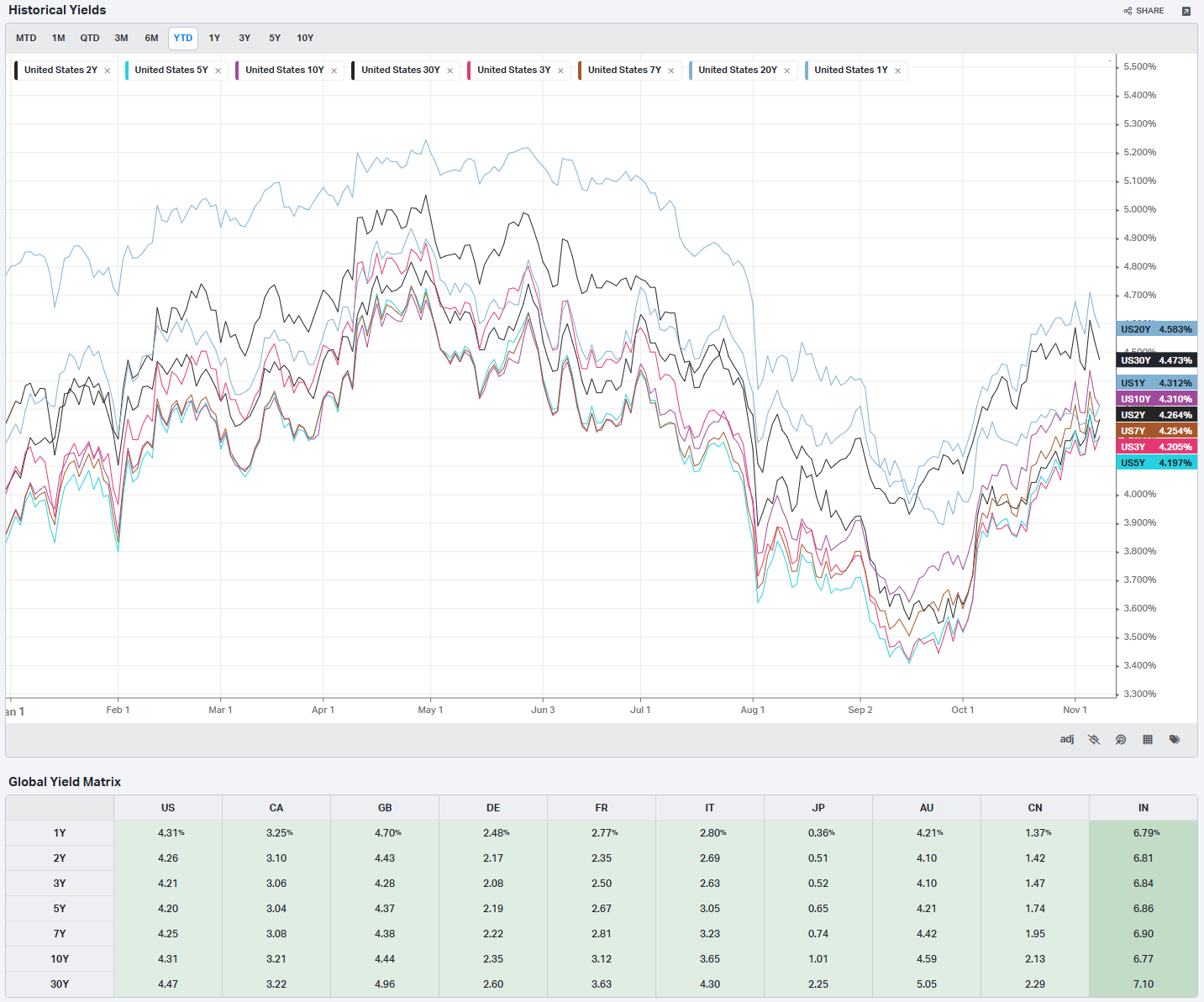

Global Yields

Factors: Size vs Value

Factors: Style

Factors: Qualitative

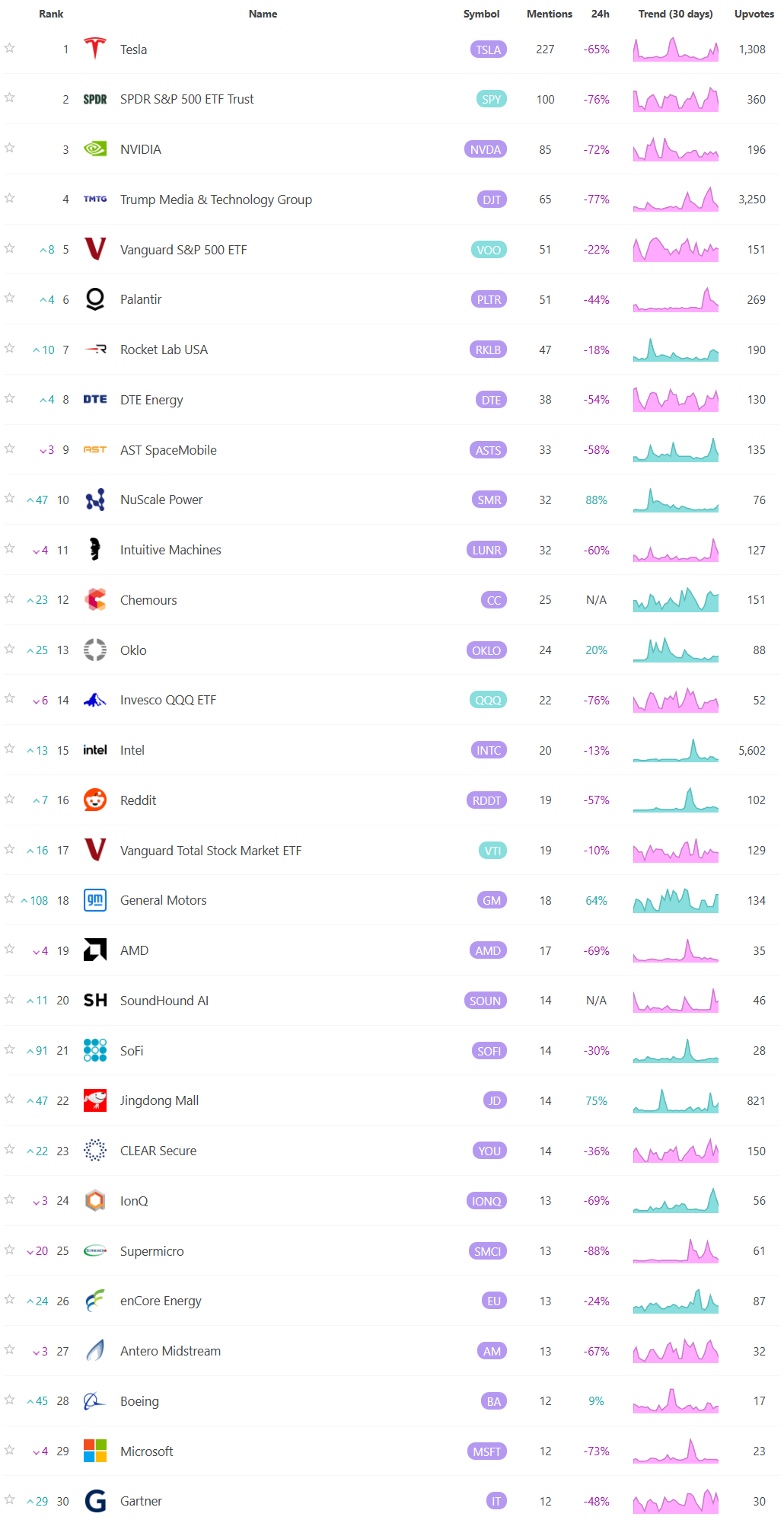

Social Media Favs

Analyzing social sentiment can provide valuable insights for investment strategies by offering a pulse on public perception, mood, and market sentiment that traditional financial indicators might not capture. Here’s how social sentiment analysis can enhance investment decisions:

Market Momentum: Positive or negative social sentiment can signal impending momentum shifts. When public opinion on a stock, sector, or asset class changes sharply, it can create buying or selling pressure, especially if that sentiment becomes widespread.

Early Detection of Trends: Social sentiment data can help investors spot trends before they show up in technical or fundamental data. For example, increased positive chatter around a particular company or sector might indicate growing interest or excitement, which could lead to price appreciation.

Gauge Retail Investor Impact: With the rise of retail investor platforms, collective sentiment on social media can lead to significant price movements (e.g., meme stocks). Understanding how retail investors view certain stocks can help in identifying high-volatility opportunities.

Event Reaction Monitoring: Social sentiment can provide real-time reactions to news events, product releases, or earnings reports. Investors can use this information to gauge market reaction quickly and adjust their strategies accordingly.

Complementing Quantitative Models: By adding a social sentiment layer to quantitative models, investors can enhance predictions. For example, a model that tracks historical price and volume data might perform even better when factoring in sentiment trends as a measure of market psychology.

Risk Management: Negative sentiment spikes can be a signal of potential downturns or increased volatility. By monitoring sentiment, investors might avoid or hedge against investments in companies experiencing a public relations crisis or facing negative perceptions.

Long-Term Sentiment Trends: Sustained sentiment trends, whether positive or negative, often mirror longer-term market cycles. Tracking sentiment trends over time can help identify shifts in investor psychology that could affect longer-term investments or sector rotations.

For these reasons, sentiment analysis, when combined with other tools, can provide a comprehensive view of both immediate market reactions and underlying investor attitudes, helping investors position themselves strategically across various time frames. Here are the most mentioned/discussed tickers on Reddit from some of the most active Subreddits for trading:

Events On Deck This Week

Here are key events happening this week that have the potential to cause outsized moves in the market or heightened short-term volatility.

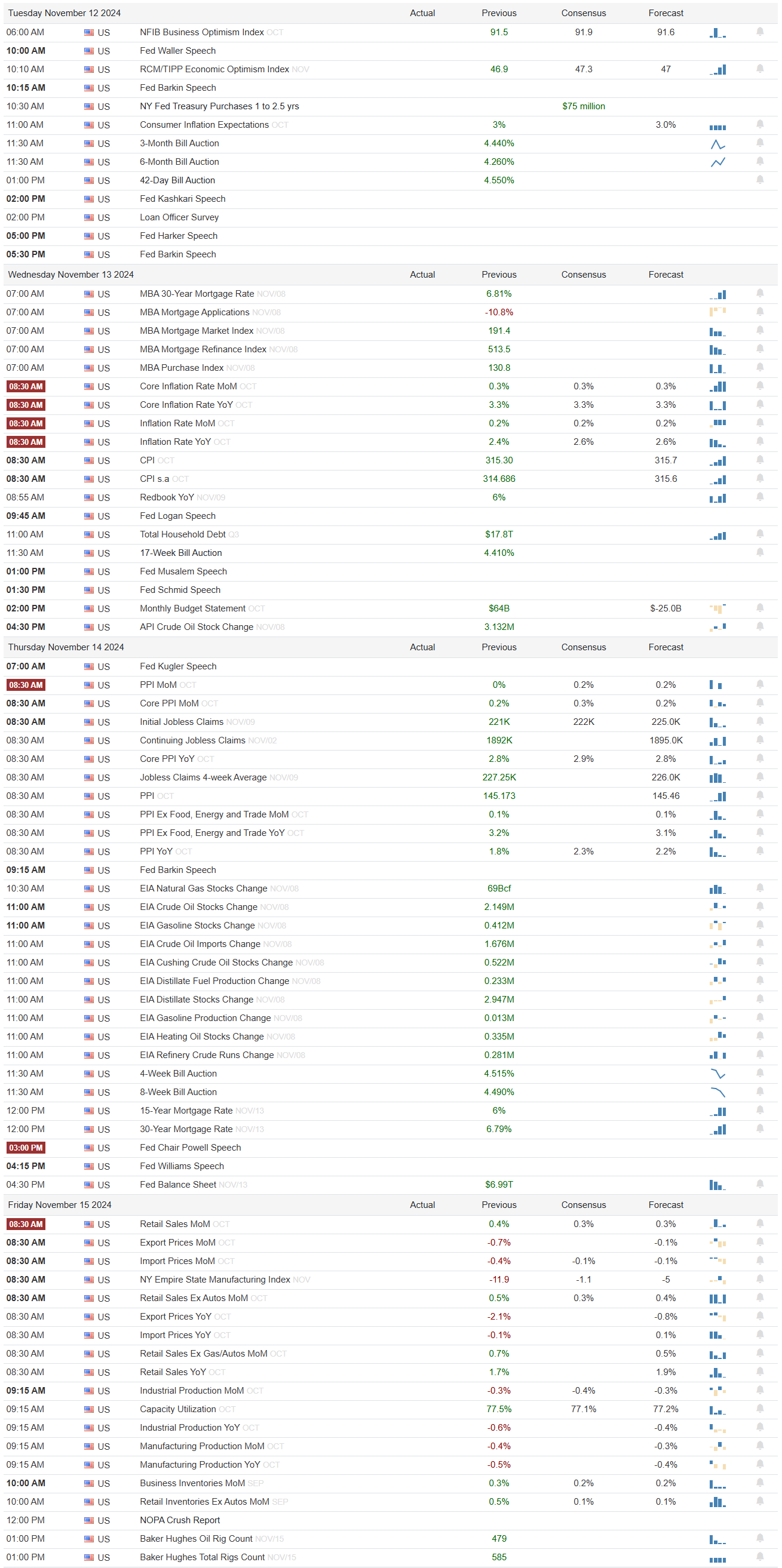

Econ Events By Day of Week

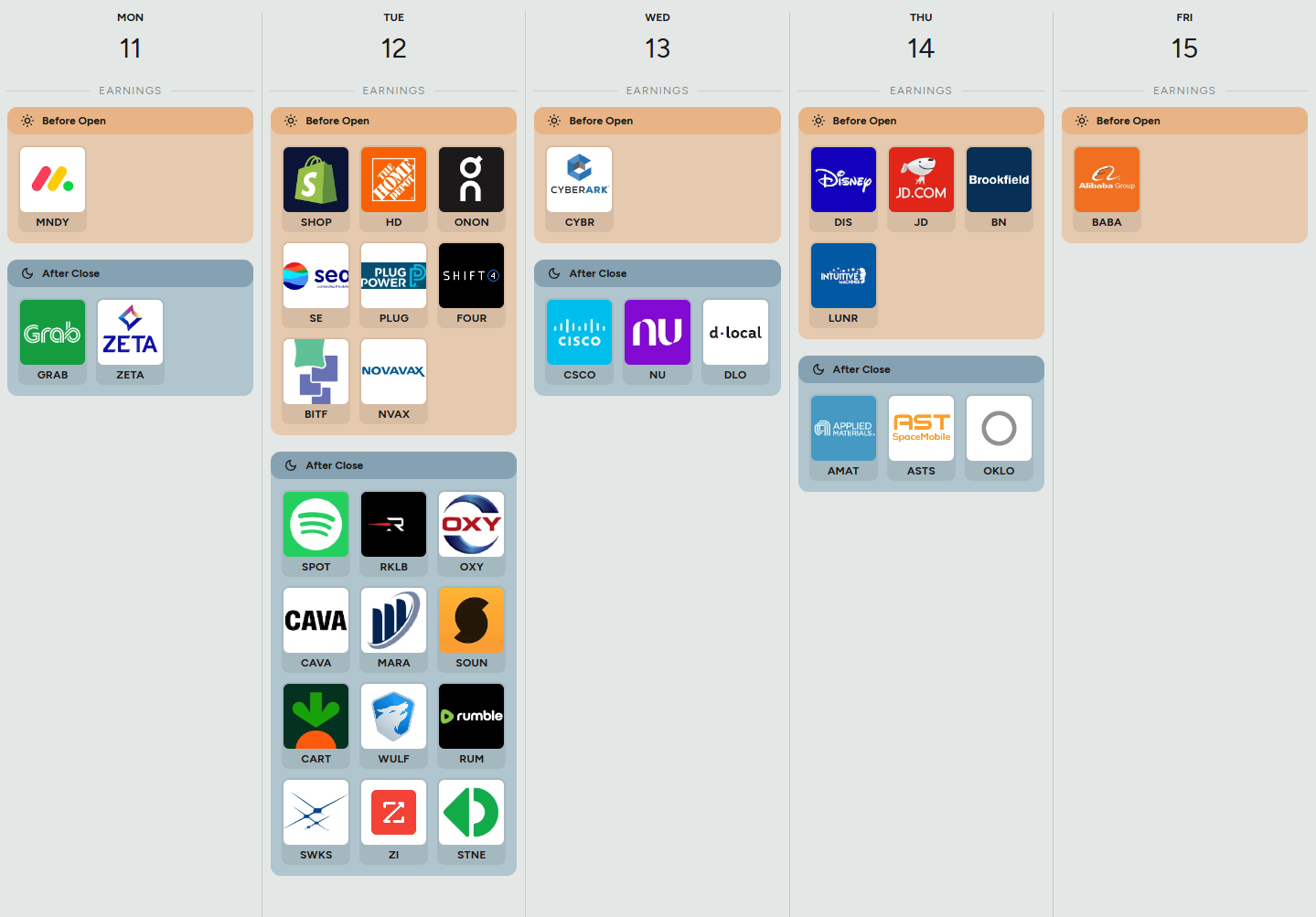

Anticipated Earnings By Day of Week

Thank you for being part of our community and for taking the time to read this publication. Your engagement and insights mean a great deal to all of us, and we're genuinely grateful to share this space with such dedicated and thoughtful readers. Now that the stack is a little more “closed-doors”, I’ll be sharing some really interesting stuff from my “lab” in coming stacks. Wishing you a productive and successful week ahead in the markets. May the coming days bring clarity and great opportunities. Happy trading!