Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 18 / What to expect Oct 21, 2024 thru Oct 25, 2024

Last Week: Insights & Trends

The U.S. stock market has had a stellar run with significant gains that have left many investors optimistic. Since early August 2024, the market has rallied more than 12%, pushing its year-to-date return to nearly 23%. This two-year performance, if sustained, could mark the second consecutive year in which the S&P 500 has delivered a return exceeding 20%. Such a feat would be remarkable, as back-to-back annual gains of this magnitude are somewhat rare, and achieving them depends on a combination of favorable economic conditions, corporate profitability, and interest-rate policies.

Historically, strong consecutive years in the stock market are not without precedent, but they are uncommon. Since 1950, there have been five instances where the market followed a 20%-plus gain with another 20% gain the next year. These periods often aligned with significant economic growth and favorable market environments. For example, the 1950s saw gains of 32% and 24% in 1950-51 and then an extraordinary 53% and 32% in 1954-55. Similarly, in the mid-1970s, 1980s, and the tech-boom years of the late 1990s, the stock market experienced similar patterns. However, these were exceptional circumstances, and in many cases, the market did not extend the streak for a third consecutive year of such gains.

The prospect of a "three-peat," or three consecutive years of 20%-plus gains, is even rarer. The only instance of this happening occurred during the bull market of the 1990s, where the market posted five consecutive years of returns exceeding 20%, fueled by the dot-com boom. This era serves as a cautionary tale, as it eventually led to the formation of a bubble. However, outside of this anomaly, a three-year streak of such gains has occurred only sporadically, with more moderate returns typically following back-to-back strong years.

To understand the potential for continued gains in 2025, it is essential to examine the factors that have contributed to the market's current rally. Several key drivers of this performance include economic growth, corporate earnings, and interest-rate policies. As the table of historical data on previous two-year market rallies suggests, the conditions that supported these past gains were varied, from post-war expansion to recovery from stagflation and economic boom periods.

Currently, the economic environment differs in several respects from those earlier periods. GDP growth, while positive, is not as robust as in some past instances, though a recession does not appear imminent. Additionally, the Federal Reserve is easing policy, whereas in many previous two-year rallies, it was tightening. Corporate earnings, meanwhile, are on the rise, contrasting with weakening profit trends seen in some earlier periods. These conditions suggest that, while another 20%-plus year in 2025 might be a stretch, the fundamental backdrop remains supportive of continued gains, albeit at a more moderate level.

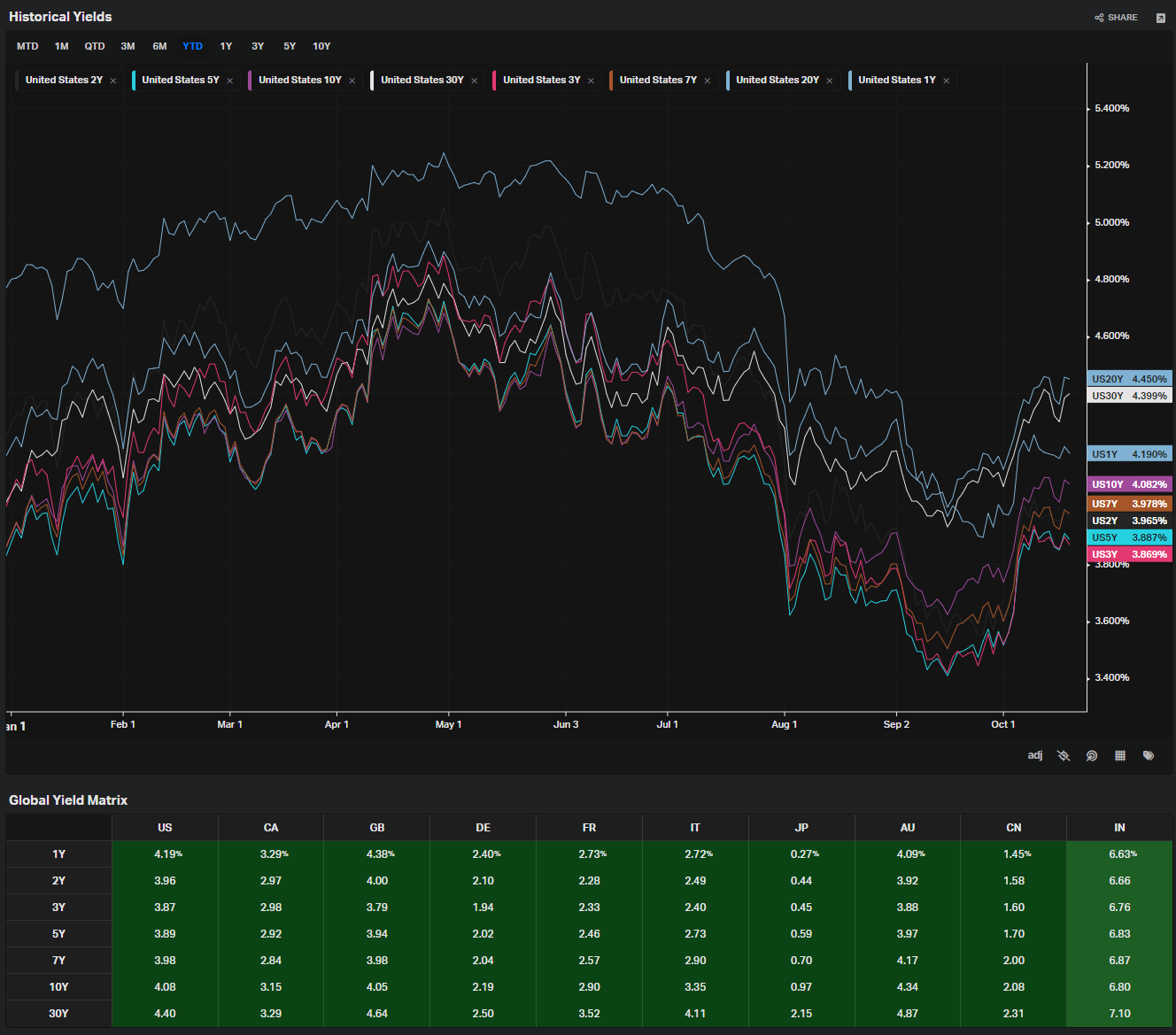

Interest rates play a significant role in the stock market's performance, and the recent trend in rising U.S. Treasury yields has been a focal point for investors. The yield on the 10-year U.S. Treasury note has climbed steadily, reaching 4.08% in early October 2024, up from 3.98% at the end of the previous week. This increase reflects market expectations that the Federal Reserve may slow the pace of interest-rate cuts, given the strong economic data and persistent inflation concerns. Higher yields can affect corporate borrowing costs and valuations, making it more challenging for stocks to maintain their upward momentum.

Earnings season, however, has provided a boost to the market. Several major U.S. banks reported strong third-quarter results, exceeding analysts' expectations and lifting their stock prices. Overall, earnings for companies in the S&P 500 are expected to rise by an average of 4.1%, a positive signal for investors. Strong earnings growth is a key ingredient in sustaining market rallies, as it demonstrates that companies are able to generate profits despite economic challenges.

Inflation remains a concern for both the Federal Reserve and investors. The Consumer Price Index (CPI) for September 2024 came in slightly higher than expected, rising at an annual rate of 2.4%, down from 2.5% in August but still above the consensus forecast. Core inflation, which excludes volatile energy and food prices, rose to 3.3%, further complicating the outlook for interest rates. While inflation has moderated from its peak levels, it remains above the Fed's target, and policymakers continue to debate the appropriate pace of rate cuts.

The Federal Reserve's minutes from its September 2024 meeting revealed a robust debate among policymakers over the size of the most recent rate cut. While the majority of voting members supported a half-percentage point reduction, some argued for a smaller quarter-point cut, reflecting concerns over inflation and the strength of the economy. The Fed's path forward remains uncertain, but the market is pricing in high odds of another rate cut in the coming months.

Consumer sentiment, another critical factor influencing the market, slipped for the first time in three months in September 2024. The University of Michigan's Consumer Sentiment Index fell to 68.9, down from 70.1 in August, surprising economists who had expected a small increase. Consumer sentiment is closely watched because it can provide early indications of changes in spending behavior, which drives a significant portion of economic activity.

Stock buybacks, a common practice by corporations to return capital to shareholders, have also been on the rise. Companies in the S&P 500 spent nearly $878 billion on stock repurchases in the 12-month period ending in June 2024, up 8% from the previous year. However, buyback activity slowed slightly in the second quarter of 2024, with spending down 0.4% compared to the first quarter. Stock buybacks can provide a tailwind for market performance by reducing the number of shares outstanding and boosting earnings per share.

Looking ahead, investors will be watching closely for the release of the U.S. retail sales report for September 2024. Retail sales rose 0.1% in August, following a stronger-than-expected gain of 1.1% in July. Consumer spending accounts for a significant portion of U.S. GDP, and continued strength in retail sales could help support the case for further stock market gains.

As of mid-October 2024, U.S. stocks have extended their rally, with the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite each rising more than 1% for the fifth consecutive week. The Nasdaq, in particular, has been buoyed by strong earnings from technology companies, including Netflix, which saw its stock surge following a robust earnings report.

The yield on the 10-year Treasury note remains a focal point for investors, as it influences borrowing costs and the relative attractiveness of stocks versus bonds. While yields have risen recently, they remain below the levels seen earlier in the year, and the market is still pricing in high odds of additional rate cuts from the Federal Reserve.

Crude oil prices have also been a key factor influencing market sentiment. As of October 2024, crude oil prices had fallen to their lowest level since the beginning of the month, reflecting easing tensions in the Middle East and muted demand from China. Lower oil prices can benefit corporate profit margins and help keep inflation in check, though they have negatively impacted the energy sector.

In conclusion, while the stock market's performance in 2024 has been impressive, there are reasons to remain cautious about the outlook for 2025. History suggests that back-to-back years of 20%-plus gains are rare, and the conditions that supported these gains in the past were varied. While the current economic environment is favorable, with strong corporate earnings and easing monetary policy, challenges remain, particularly in the form of inflation and rising interest rates. Investors should be prepared for a more moderate pace of gains in the coming year, but the fundamental backdrop remains supportive of continued positive performance.

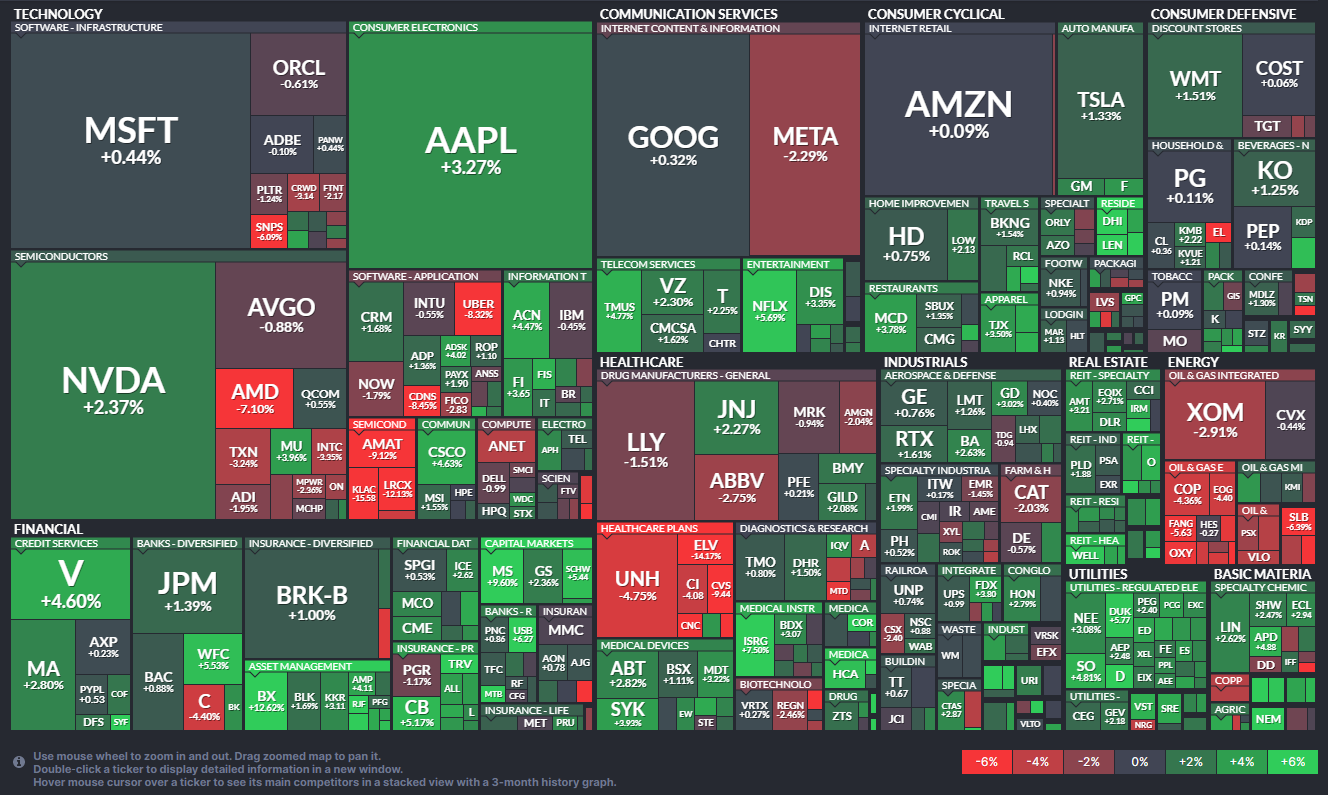

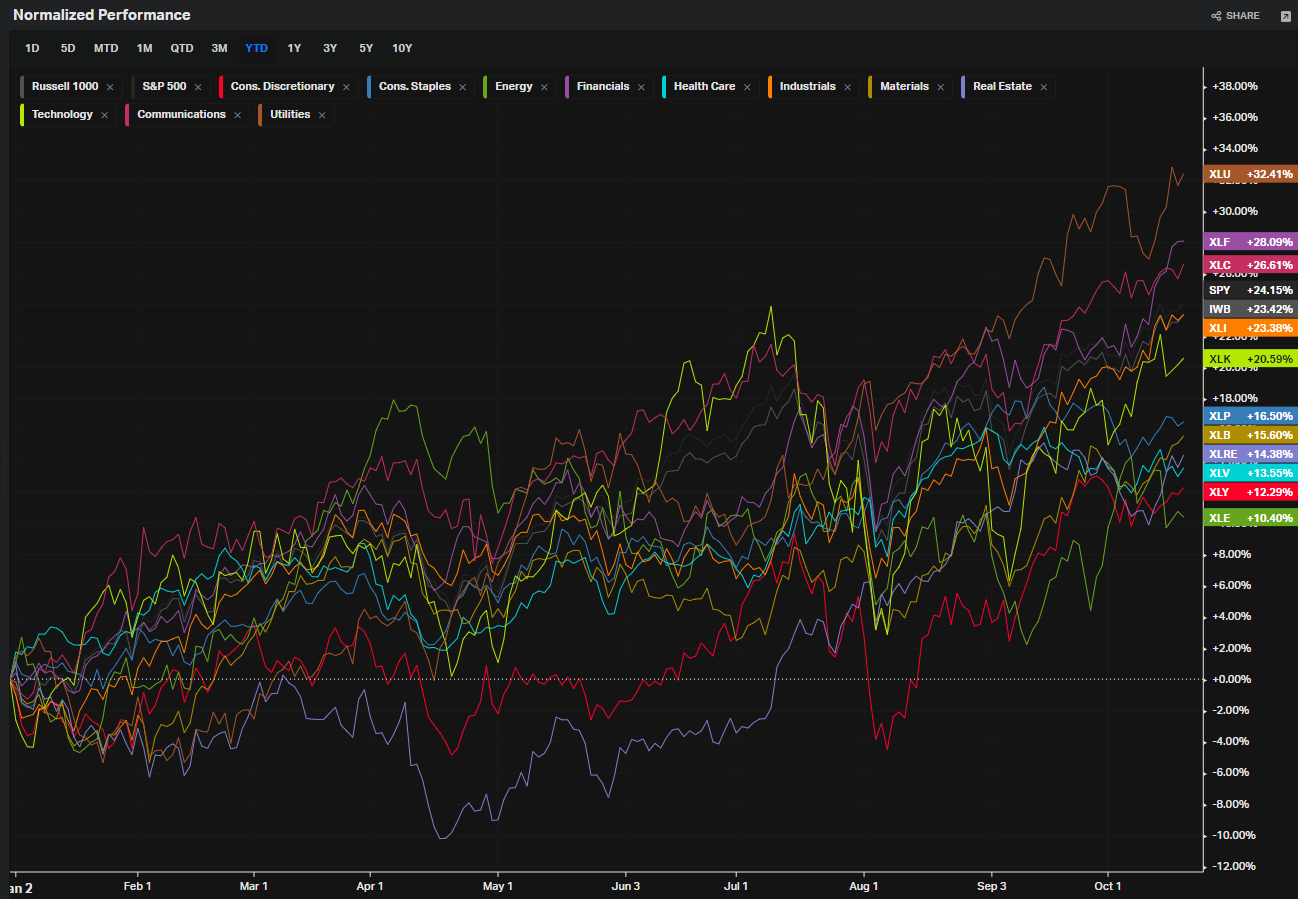

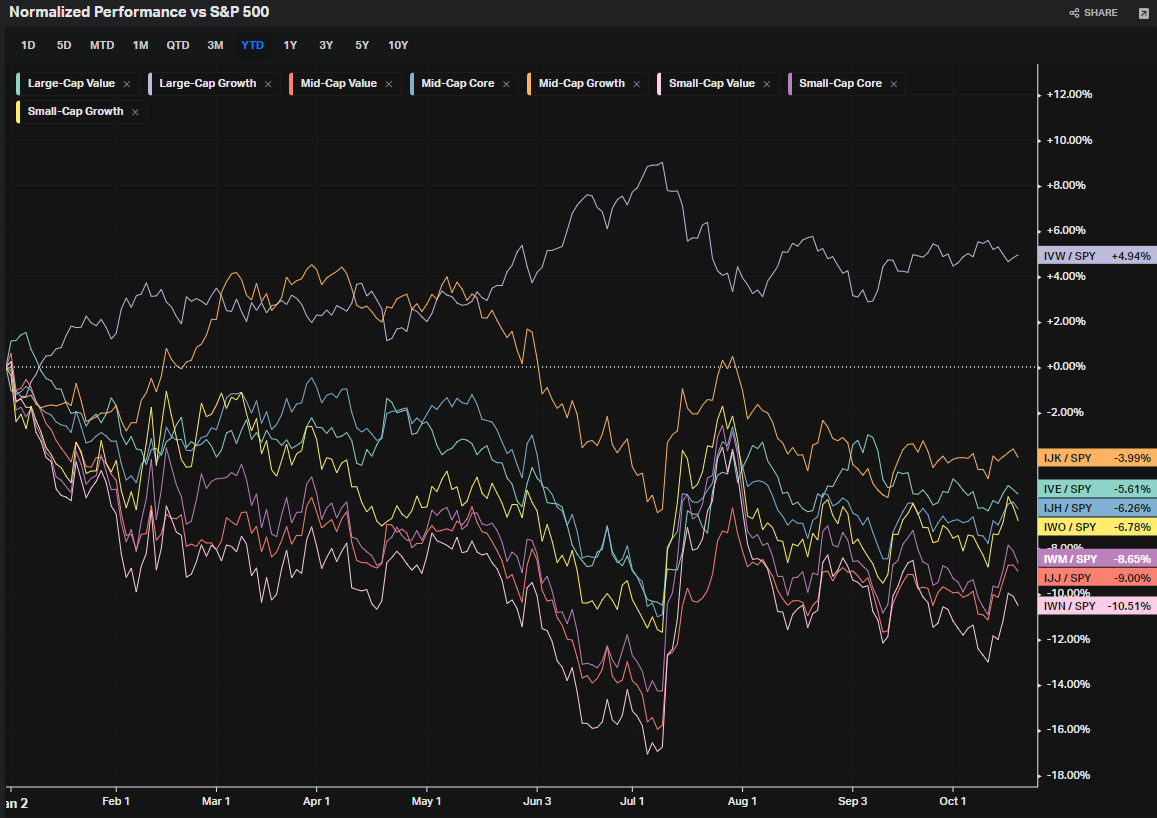

S&P 500 By Size & Sector

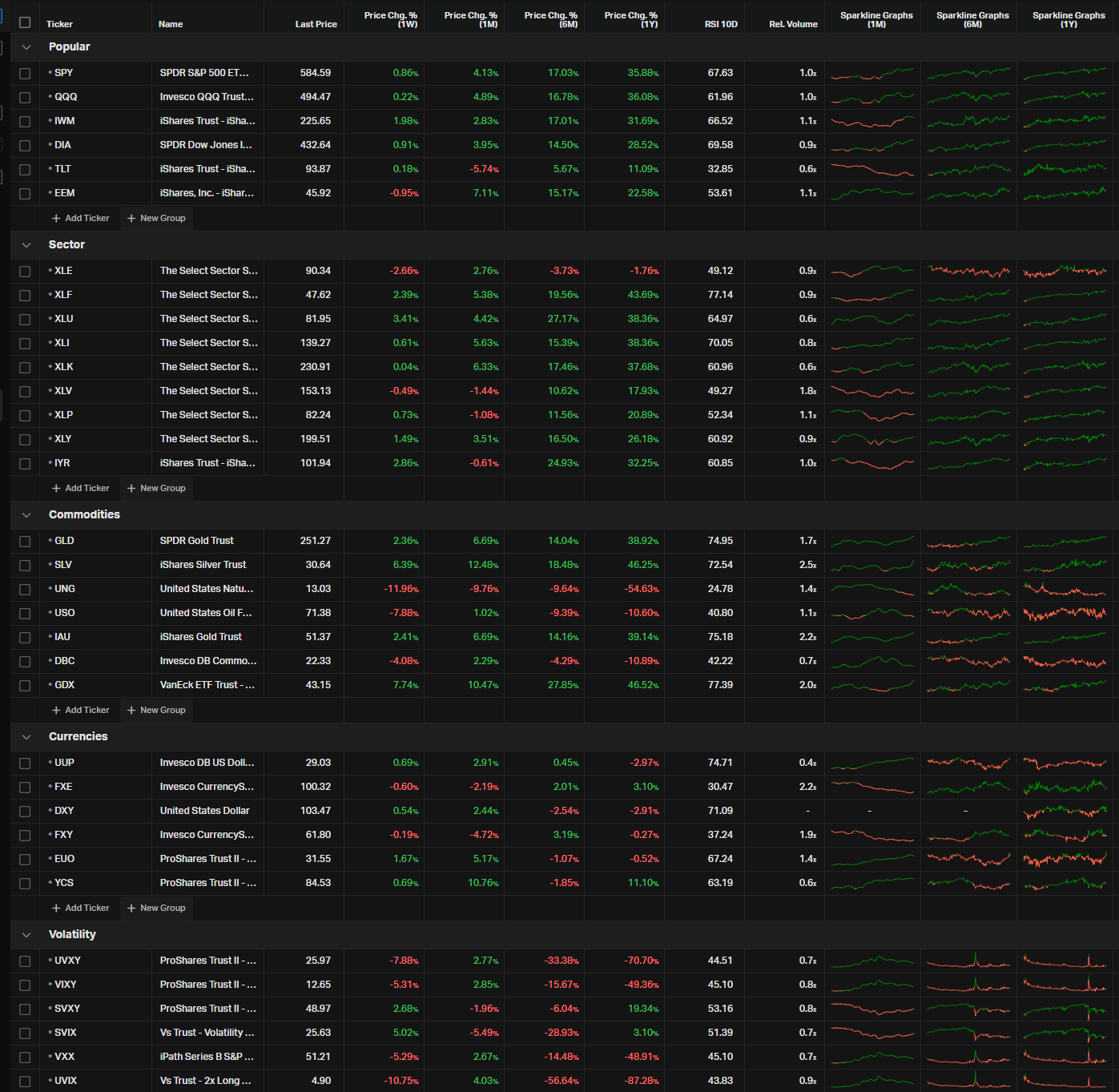

ETF Snapshots

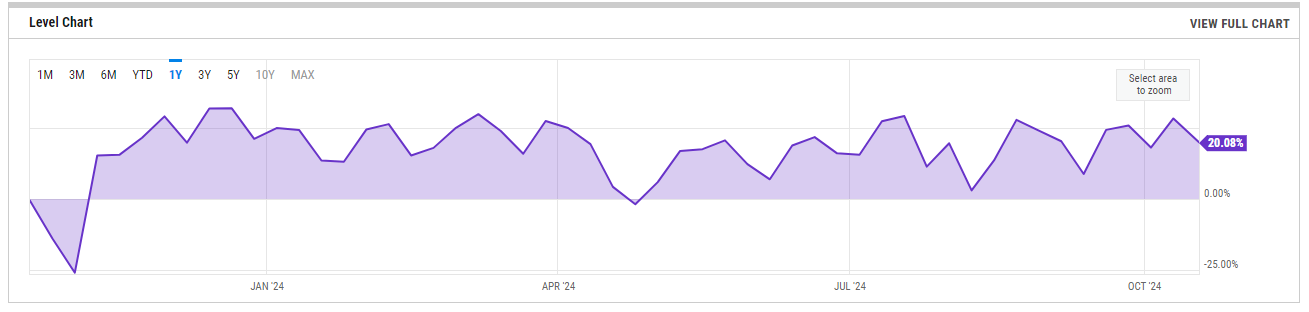

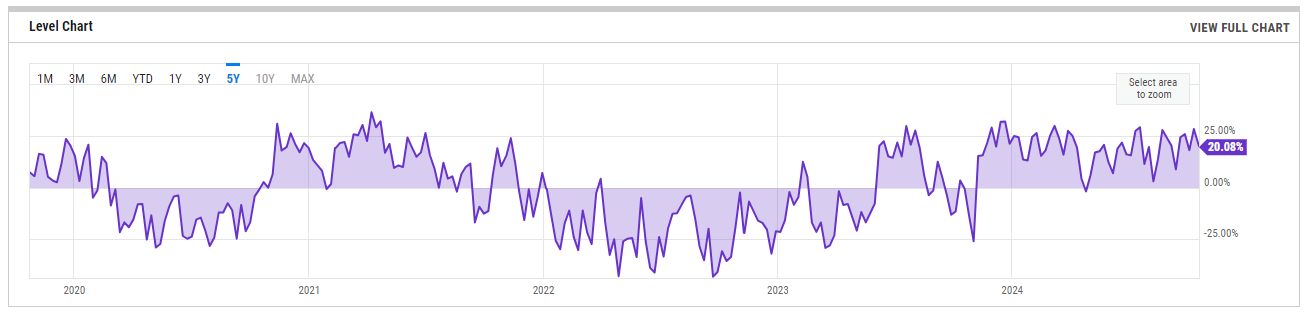

US Investor Sentiment

%Bull-Bear Spread

The %Bull-Bear Spread chart is a sentiment indicator that shows the difference between the percentage of bullish and bearish investors, often derived from surveys or sentiment data, such as the AAII (American Association of Individual Investors) sentiment survey. This spread tells investors about the prevailing mood in the market and can provide insights into market extremes and potential turning points.

Bullish or Bearish Sentiment:

When the spread is positive, it means more investors are bullish than bearish, indicating optimism about the market’s direction.

A negative spread indicates more bearish sentiment, meaning more investors expect the market to decline.

Contrarian Indicator:

The %Bull-Bear Spread is often used as a contrarian indicator. For example, extremely high levels of bullish sentiment might suggest that the market is overly optimistic and could be due for a correction.

Similarly, when bearish sentiment is extremely high, it might indicate that the market is overly pessimistic, and a rally could be on the horizon.

Market Extremes and Reversals:

Historically, extreme values of the spread (both positive and negative) can signal turning points in the market. A very high positive spread can signal market exuberance, while a very low or negative spread may indicate fear or capitulation.

1-Year View

5-Year View

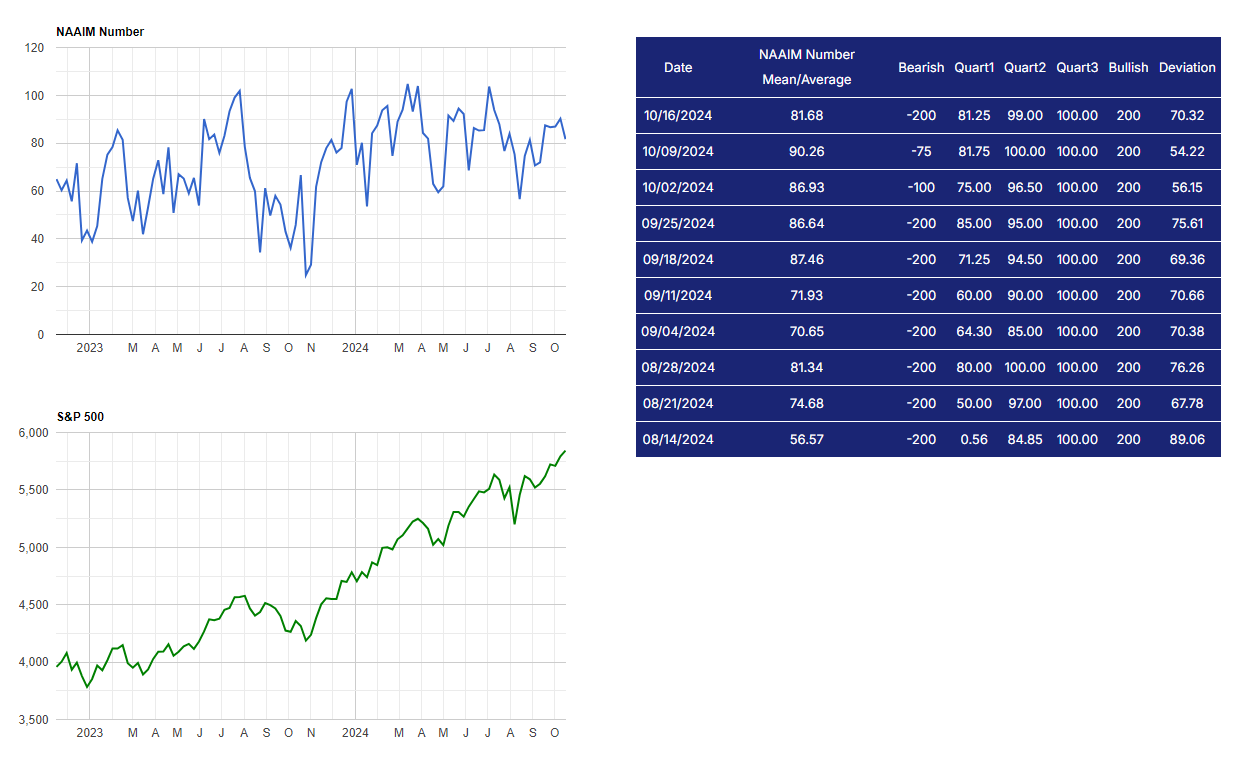

NAAIM Exposure Index

The NAAIM Exposure Index (National Association of Active Investment Managers Exposure Index) measures the average exposure to U.S. equity markets as reported by its member firms. These are typically active money managers who provide their equity exposure levels weekly. The index offers insight into how much these managers are investing in equities at any given time, ranging from being fully short (-100%) to leveraged long (up to +200%).

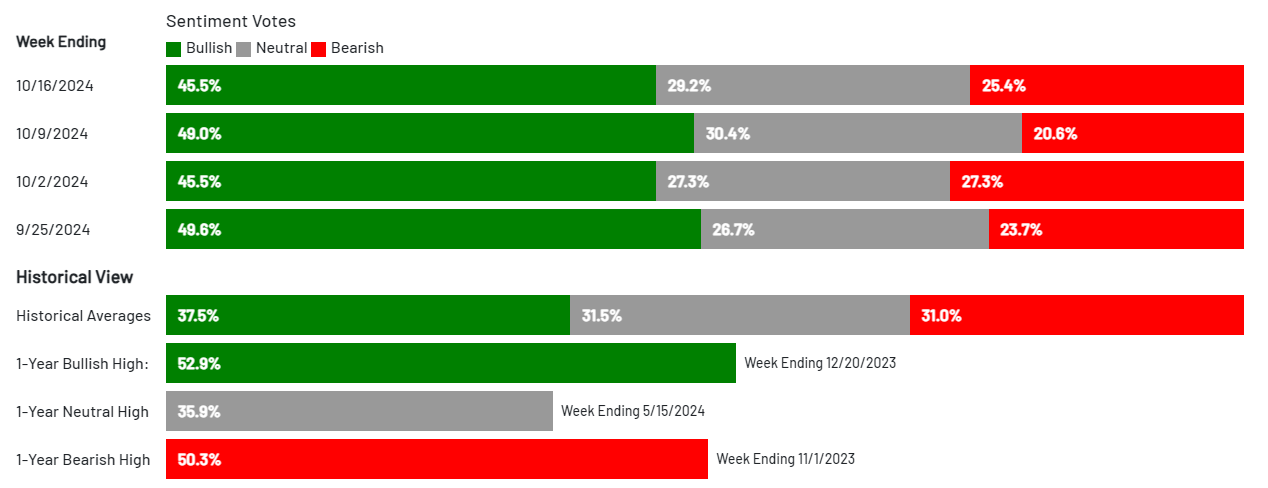

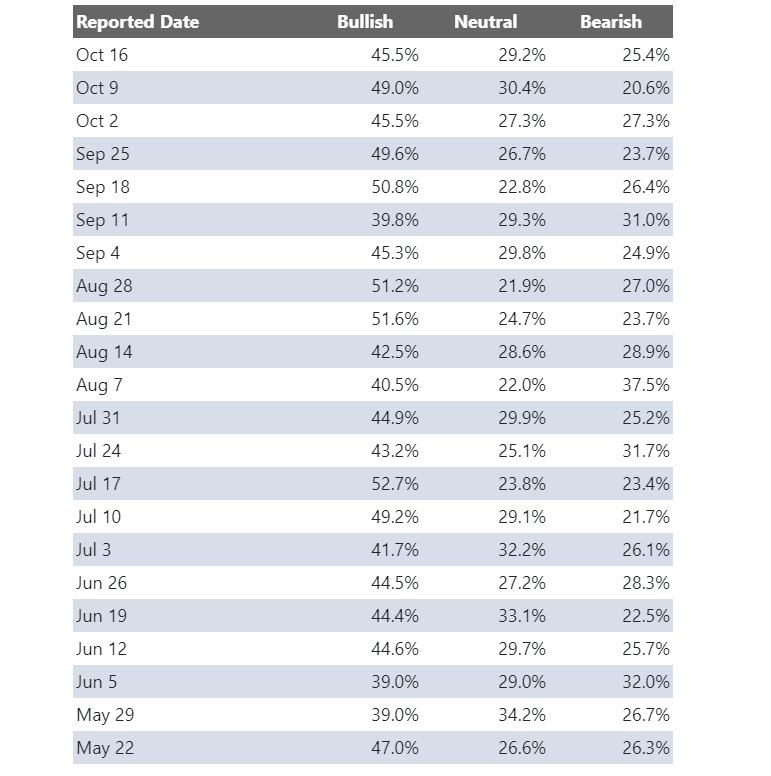

AAII Investor Sentiment Survey

The AAII Investor Sentiment Survey is a weekly survey conducted by the American Association of Individual Investors (AAII) to gauge the mood of individual investors regarding the direction of the stock market over the next six months. It provides insights into whether investors are feeling bullish (expecting the market to rise), bearish (expecting the market to fall), or neutral (expecting the market to stay about the same).

Key Points:

Bullish Sentiment: Reflects the percentage of investors who believe the stock market will rise in the next six months.

Bearish Sentiment: Represents those who expect a decline.

Neutral Sentiment: Reflects investors who anticipate little to no market movement.

The survey is widely followed as a contrarian indicator, meaning that extreme levels of bullishness or bearishness can sometimes signal market turning points. For example, when a large number of investors are overly optimistic (high bullish sentiment), it could suggest a market top, while excessive pessimism (high bearish sentiment) may indicate a market bottom is near.

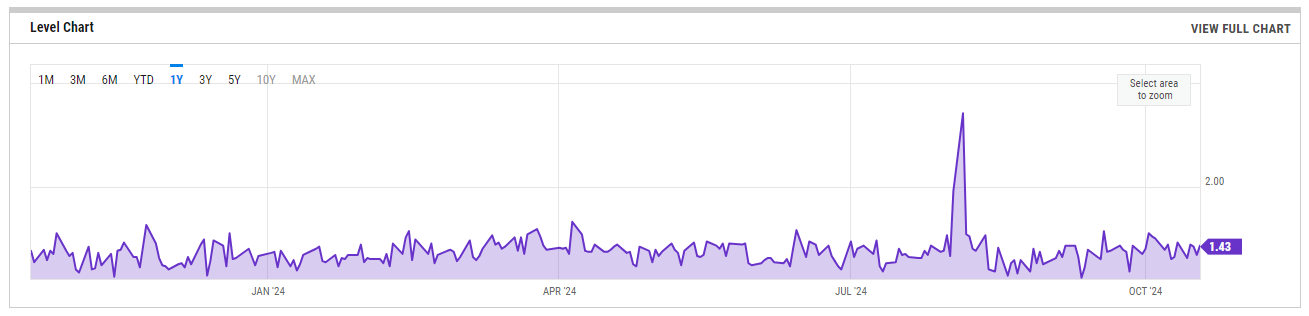

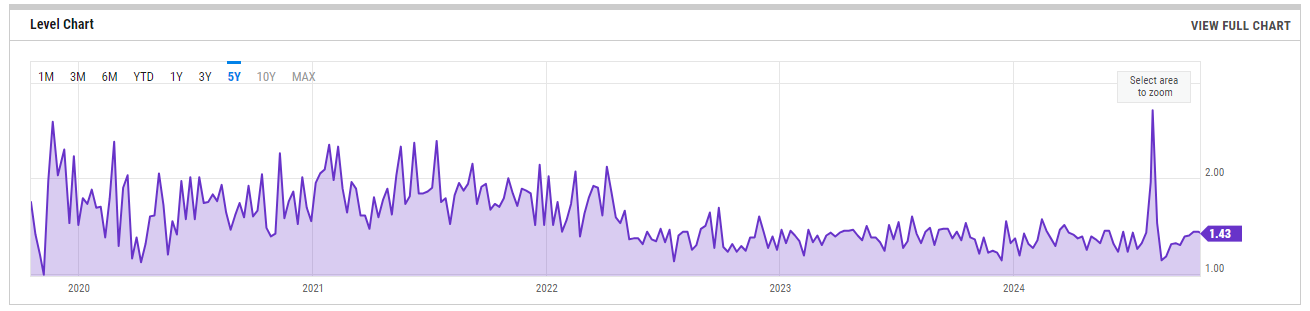

SPX Put/Call Ratio

The SPX Put/Call Ratio is an indicator that is used to gauge market sentiment. This is calculated as the ratio between trading S&P 500 put options and S&P call options. A high put/call ratio can indicate fear in the markets, while a low ratio indicates confidence. For example, in 2015, the Put-Call ratio was as high as 3.77 because of market fears stemming from various global economic issues like a GDP growth slowdown in China and a Greek debt default.

1-Year View

5-Year View

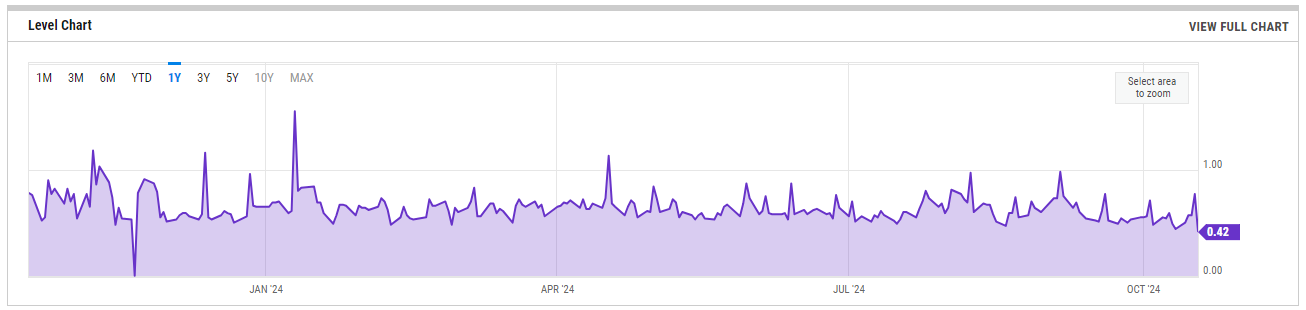

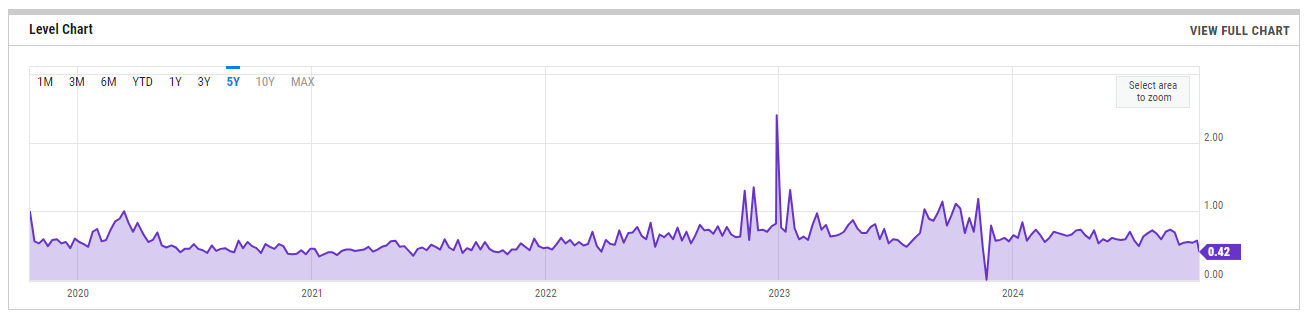

CBOE Equity Put/Call Ratio

1-Year View

5-Year View

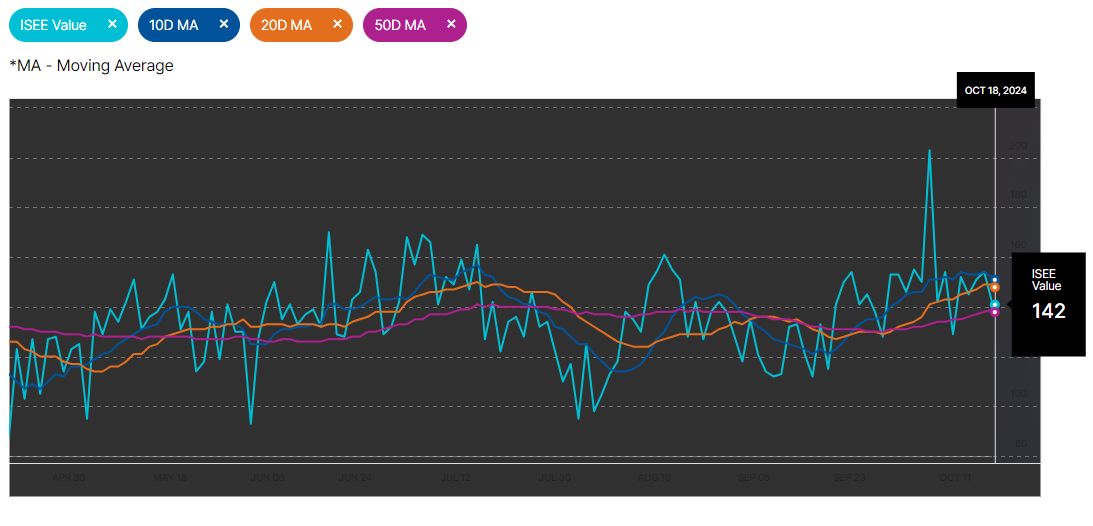

ISEE Sentiment Index

The ISEE (International Securities Exchange Sentiment) Index is a measure of investor sentiment derived from options trading. Unlike traditional put/call ratios, the ISEE Index focuses only on opening long customer transactions and is adjusted to remove market-maker and firm trades, providing a purer sentiment reading.

The ISEE Index typically ranges from 0 to 200, with readings above 100 indicating more call options being bought relative to put options, suggesting bullish sentiment. Conversely, readings below 100 suggest bearish sentiment, with more puts being purchased relative to calls.

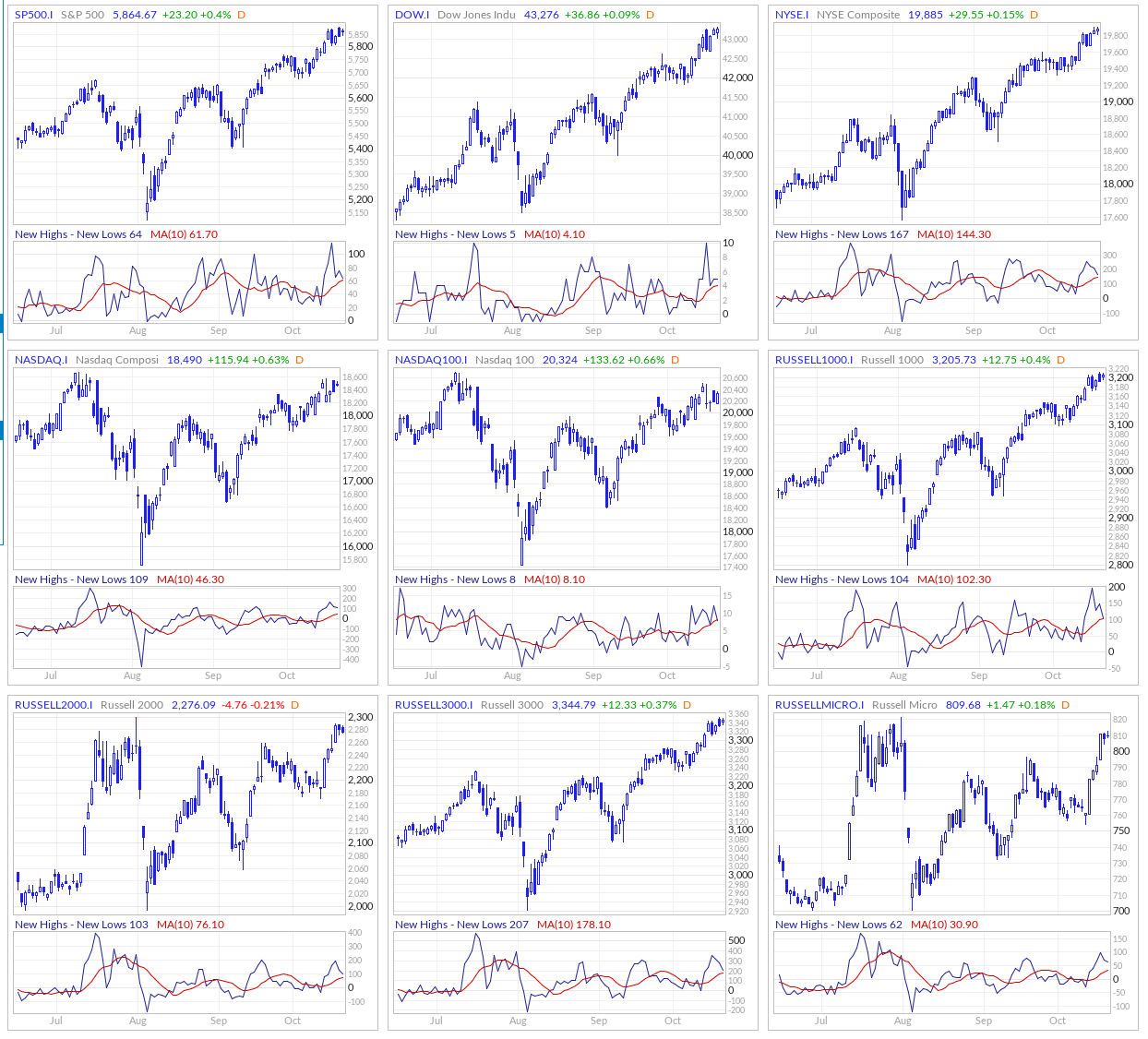

New Highs - New Lows

The New Highs - New Lows indicator (NH-NL) displays the daily difference between the number of stocks reaching new 52-week highs and the number of stocks reaching new 52-week lows. The NH-NL indicator generally reaches its extreme lows slightly before a major market bottom. As the market then turns up from the major bottom, the indicator jumps up rapidly. During this period, many new stocks are making new highs because it's easy to make a new high when prices have been depressed for a long time. The NH-NL indicator oscillates around zero. If the indicator is positive, the bulls are in control. If it is negative, the bears are in control. As the cycle matures, a divergence often occurs as fewer and fewer stocks are making new highs (the indicator falls), yet the market indices continue to reach new highs. This is a classic bearish divergence that indicates that the current upward trend is weak and may reverse.

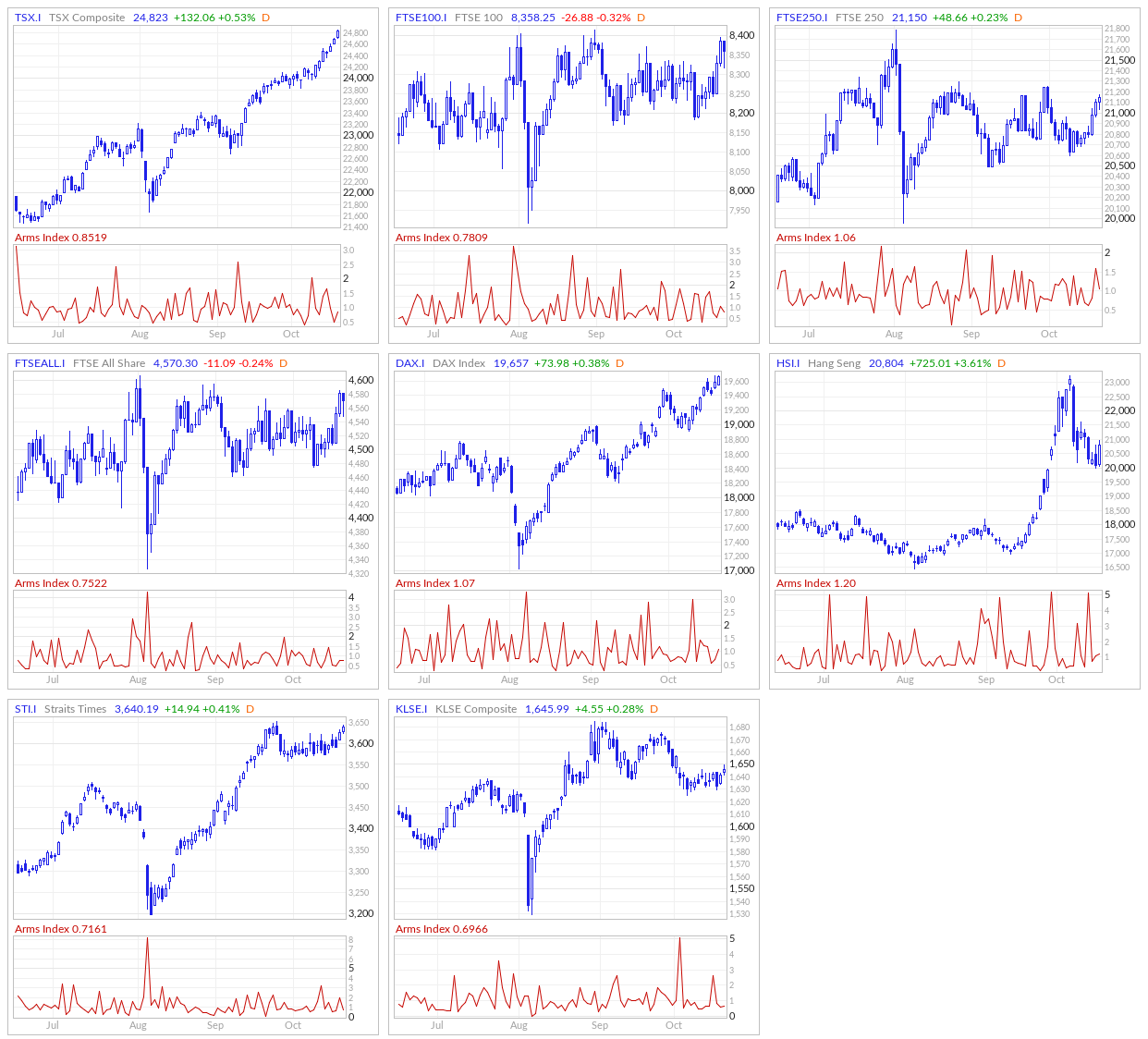

ARMS Index

The Arms Index, also known as the TRIN (Short-Term TRading INdex), was developed by Richard Arms in the 1960s. It is calculated by dividing the ratio of advancing stocks to declining stocks by the ratio of advancing volume to declining volume. Interpreting the Arms Index involves looking at its value in relation to certain thresholds. A value below "1" is considered bullish, indicating that advancing stocks and volume dominate the market. Conversely, a value above "1" is considered bearish, suggesting that declining stocks and volume are more prevalent. Extremely low values (below 0.5) or high values (above 2) are often seen as potential reversal signals.

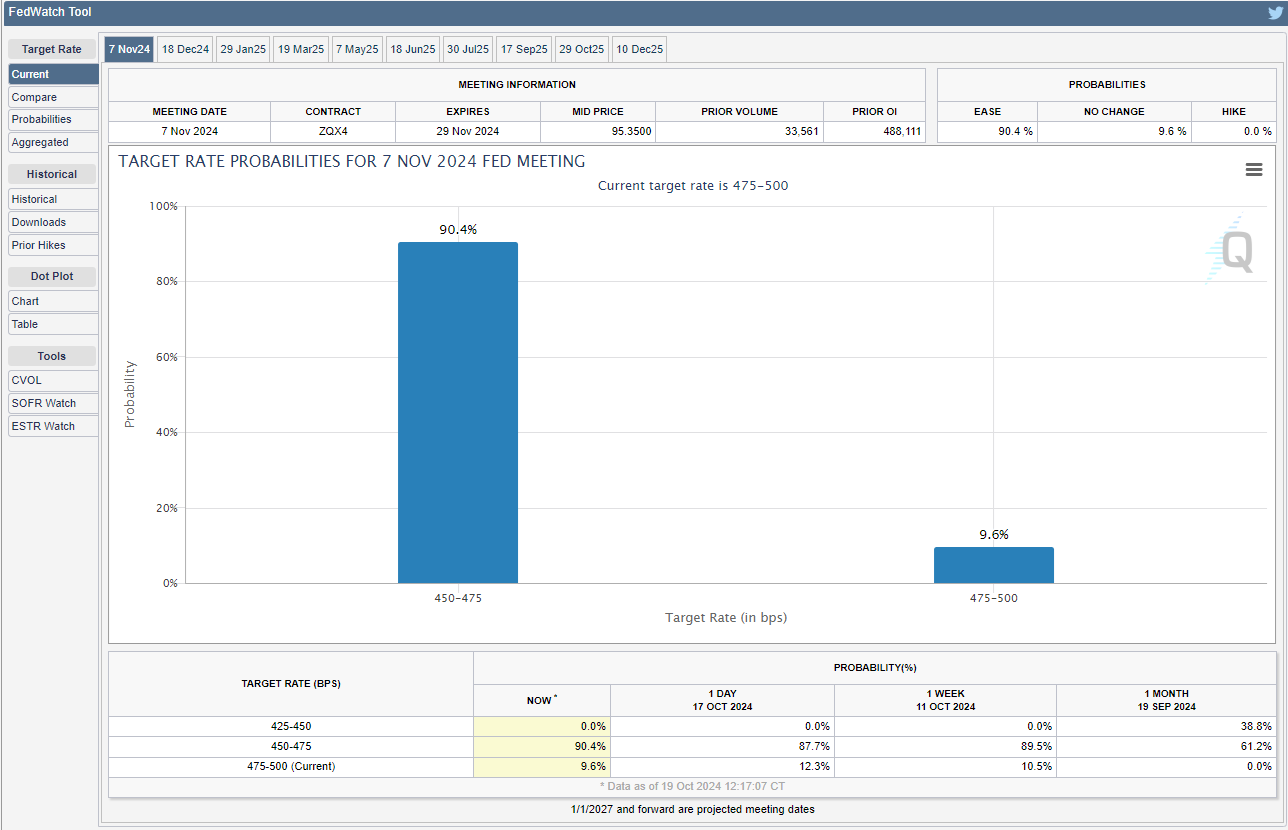

CME Fedwatch

What is the likelihood that the Fed will change the Federal target rate at upcoming FOMC meetings, according to interest rate traders? Use CME FedWatch to track the probabilities of changes to the Fed rate, as implied by 30-Day Fed Funds futures prices.

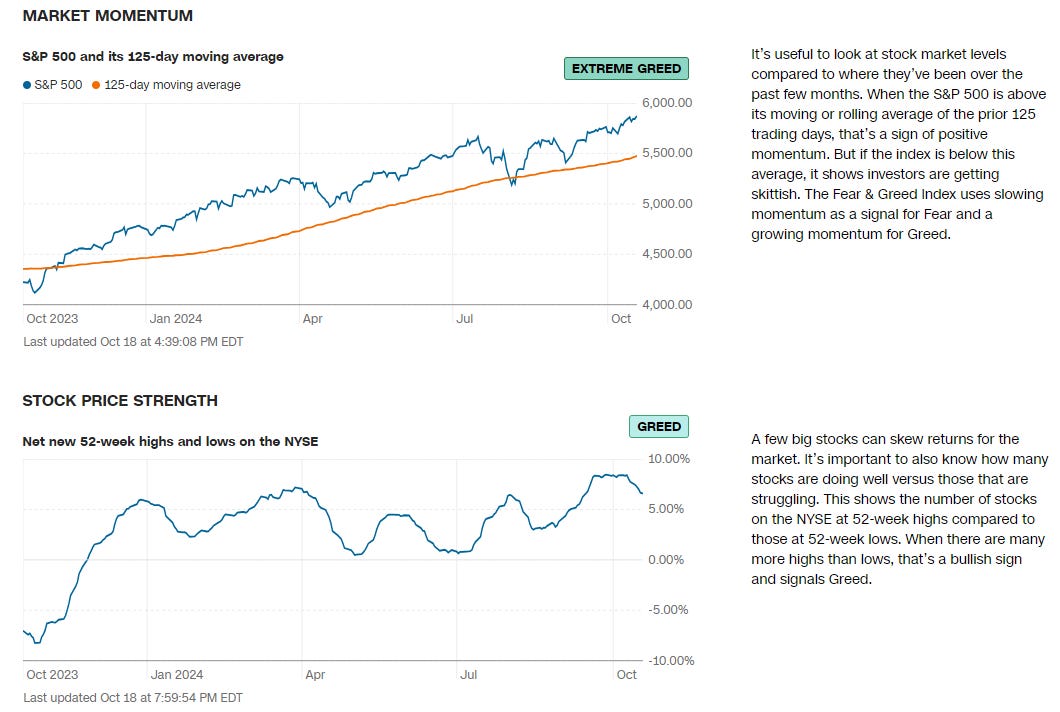

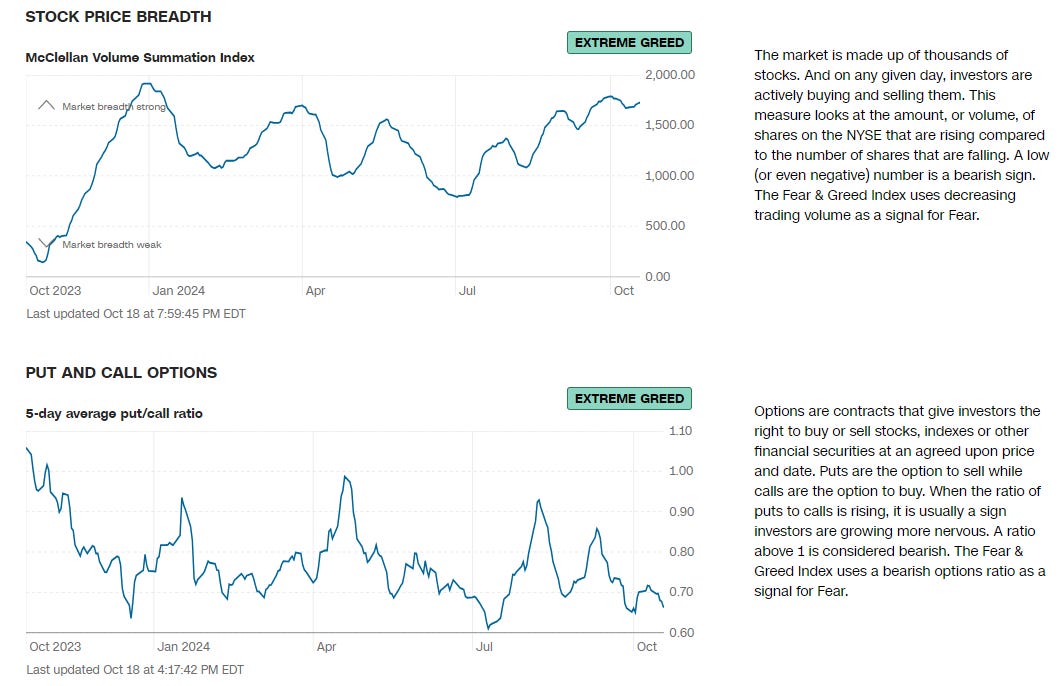

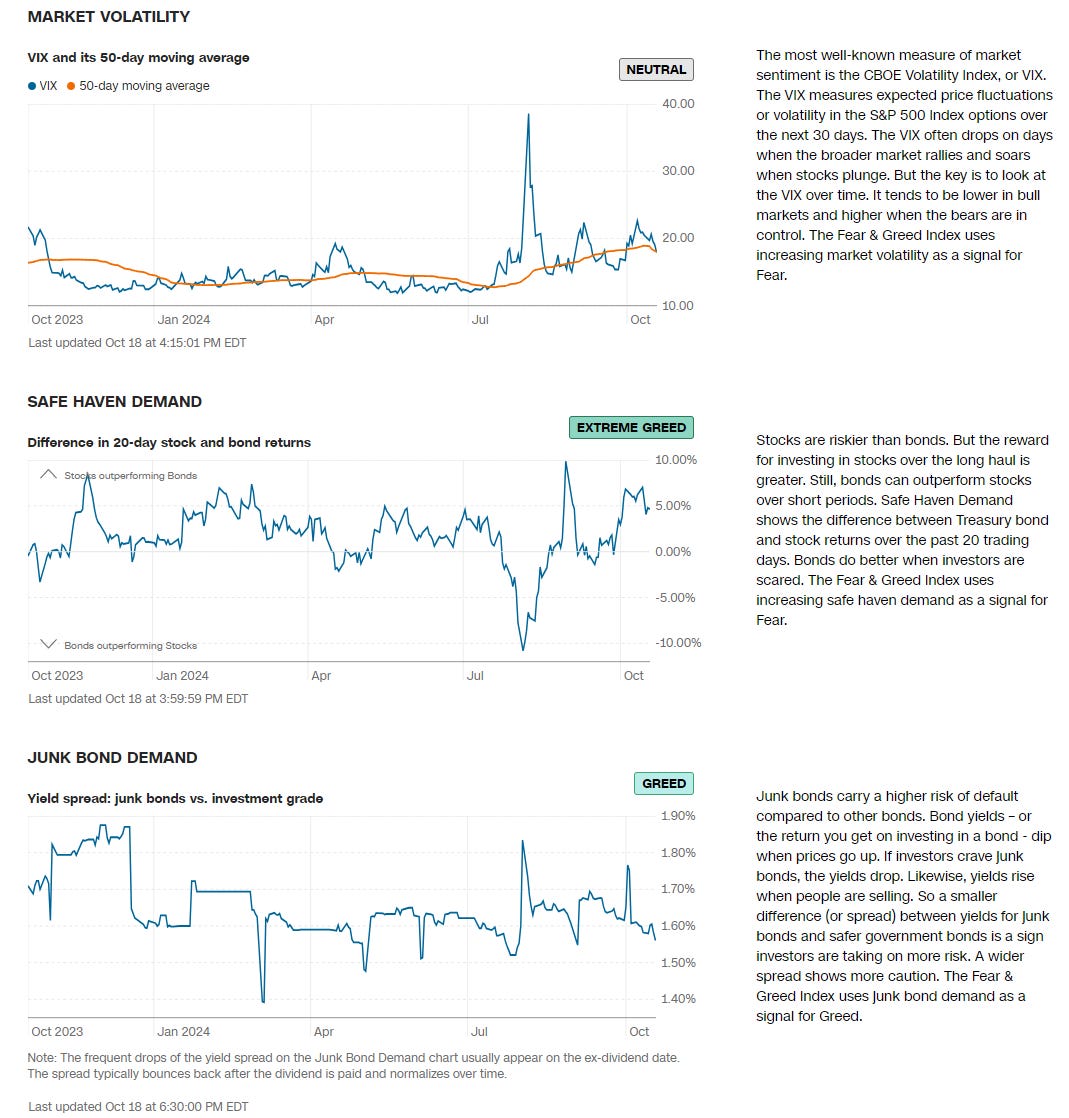

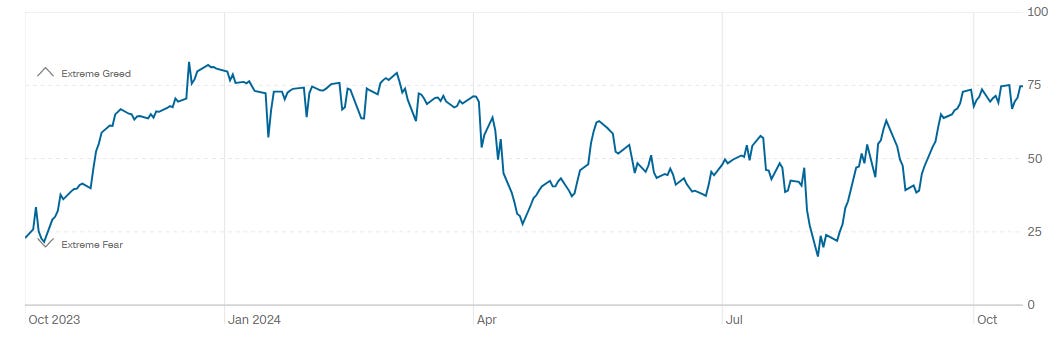

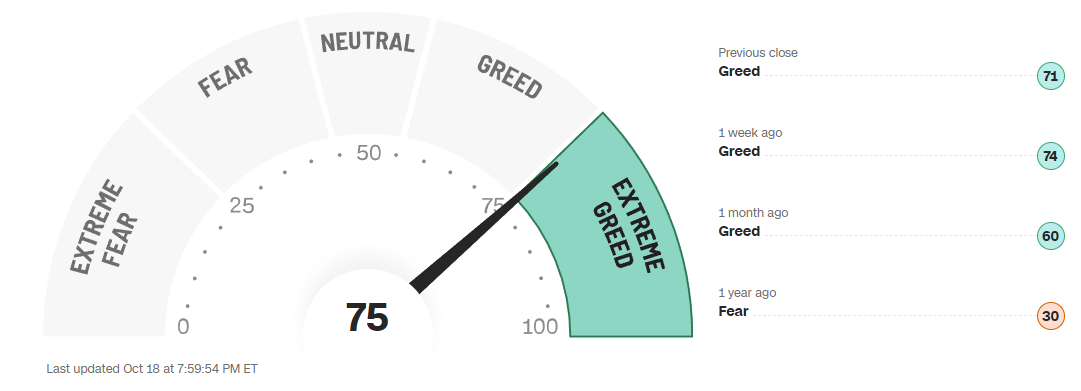

CNN 7 Fear & Greed Constituent Data Points + Composite Index

Final Composite Fear & Greed Index Reading

Institutional S/R Levels for Major Indices

When you’re a large institutional player, your primary goal is to find liquidity - places to do a ton of business with the least amount of slippage possible. VolumeLeaders.com automatically identifies and visually plots the exact spots where institutions are doing business and where they are likely to return for more. It’s one of the primary reasons “support” and “resistance” concepts work and truly one of the reasons “price has memory”.

Levels from the VolumeLeaders.com platform can help you formulate trades theses about:

Where to add or take profit

Where to de-risk or hedge

What strikes to target for options

Where to expect support or resistance

And this is just a small sample; there are countless ways to leverage this information into trades that express your views on the market. The platform covers thousands of tickers on multiple timeframes to accommodate all types of traders. Observe for yourself how accurate the levels are by marking-up your charts with the information in the “Trade Levels” boxes I’m giving for free below and play-along in real-time this week. These charts cover recent sessions, but subs will get new levels as they develop, see the latest trades and institutional positioning, have access to levels from other time frames and so much more. When you watch these levels this week, I’m confident you’ll see how clear, intuitive and actionable this information is for yourself.

SPY -0.27%↓

Key Observations from the Chart:

Largest Trades (Blue Circles): The 5 largest trades are highlighted with blue circles. These points represent significant institutional interest and large-volume transactions. These types of trades often serve as critical areas of support or resistance because large orders can influence future price movement.

First Circle (Sept 18): Occurs at a low point on the chart, where price stabilizes after a downward move. This could be interpreted as an area where buying pressure stepped in, preventing further decline.

Second to Fourth Circles (Sept 19 to Sept 25): These represent consolidation zones, where institutional trades occur within a tight range. The price action here suggests accumulation, as large trades are clustered around similar price levels, indicating potential future bullish behavior.

Fifth Circle (Oct 15): The final large trade occurs after a significant upward movement. This could represent profit-taking or additional buying interest, but it marks a key resistance level.

Price Levels with Greatest Institutional Activity (Dashed Blue Lines): The horizontal dashed lines highlight price levels where institutional activity was most concentrated. These zones are key areas of support and resistance:

$561.30: The largest activity happened at this level ($9.94B notional value, 17.7M shares). This price acted as support several times throughout the chart, most notably on Sept 18 and Sept 24.

$569.60: This level also saw substantial trades ($7.53B, 13.3M shares), which marks a zone where price action consolidated before breaking out.

$580 region: Institutional activity is seen near $579 and $584 levels, which are serving as significant resistance levels after the upward move on Oct 15.

These price levels are likely to serve as reference points in the near term, with the potential for reversals or breakouts depending on how the price interacts with these zones in the future.

Volume and Relative Size (RS):

Largest Trade on Sept 30: $1.86B with an RS of 135.81%, meaning this trade is over 1.3 times larger than the average size of other institutional trades. The price was around $571.82, suggesting this level is important. This coincides with resistance forming near this price.

Other Significant Trades: Between Sept 19 and Oct 18, we observe several large trades with RS values exceeding 90%, especially between the $561 and $570 range, indicating strong institutional interest in this price range. The persistence of large trades in this range suggests ongoing accumulation or distribution.

Technical Indicators:

Support Levels:

$561.30: This is the strongest support level, supported by high institutional activity.

$569.60: Another key support area, where price action found stability before the upward breakout.

Any retracement toward these levels may find strong buying support.

Resistance Levels:

$579–584 region: This area has seen significant resistance, as institutional activity seems concentrated here. It will be critical to watch if the price can break above this level, as it would open the door for further bullish momentum.

Consolidation Zones:

The period from Sept 19 to Sept 25 shows tight consolidation within the $565–570 range, suggesting that any future dip into this range could trigger accumulation by large players.

Conclusion:

Bullish Outlook: The overall trend appears to be bullish in the last 30 days, particularly after breaking out of consolidation around Sept 25. Institutional activity supports the price at key levels, suggesting the market is in accumulation mode, with potential for further upside.

Watch Key Levels: The $561.30 (support) and $579–584 (resistance) zones are crucial. A break above $584 could trigger another rally, while any retracement may find support around $561–570.

QQQ -0.47%↓

Key Observations from the Chart:

Largest Trades (Colored Circles): The five largest trades are highlighted with colored circles. These trades represent significant institutional interest and can serve as key support or resistance areas. Here's what we can infer:

First Circle (Sept 19): This area represents two large trades clustered together ($736M and $668M). The price stabilizes around $484.50 after a decline, indicating strong buying interest that potentially stopped the downward trend.

Second Circle (Sept 25): Another significant trade ($485.50, 1.18M shares) happens after consolidation, further indicating accumulation and likely support around this price level.

Third Circle (Oct 14): Occurs after a breakout from the consolidation range. This trade ($497.06, 1M shares) marks a potential resistance level around the $497 range.

Price Levels with Greatest Institutional Activity (Dashed Blue Lines): The dashed horizontal lines show where institutional activity was most concentrated. These zones will likely act as critical support or resistance:

$481.30: This level represents the largest activity ($4.24B in notional value, 8.81M shares). This is a strong support zone, where price held up after a pullback in late September. It coincides with the first large trade circle, reinforcing its importance as support.

$475.10: A support zone that saw considerable activity ($3.52B, 7.4M shares). This level held up during the price dip in mid-September.

$496.40: The most recent level of institutional activity, forming resistance after a substantial upward move in mid-October.

Volume and Relative Size (RS):

Largest Trade on Sept 19: The most significant trade during this period occurred at $484.58 with an RS of 93.68%, meaning it was 93% larger than the average trade size. This corresponds to one of the first blue circles, suggesting a key support level around $484.50. It also aligns with heavy institutional buying, implying strong interest in this price level.

Other Significant Trades: The trades from Sept 19 and Sept 25 have RS values above 70%, meaning these were all major institutional-sized trades that dominated trading volume. This reinforces that these dates were pivotal in determining the support and resistance zones.

Price Consolidation and Clusters:

$483–485 range: This consolidation zone between Sept 19 and Sept 25 marks an area of heavy institutional trading and accumulation. It has acted as a base for the rally seen afterward.

$496-497 range: This zone is serving as a current resistance level. It will be key to watch if the price can break above this range, as it could signal further bullish momentum.

Technical Indicators:

Support Levels:

$481.30: This level saw the largest institutional activity and should serve as strong support. If the price retraces to this area, it is likely to find buying interest.

$475.10: Another key support level, which has held up during past pullbacks and could be crucial in the event of a broader market correction.

Resistance Levels:

$496.40 to $497: This zone is serving as the main resistance in mid-October. Institutional activity is concentrated here, and a break above this could trigger further upward movement in the price of QQQ.

Accumulation Zones:

The range between $482 and $485 saw significant accumulation and institutional buying activity. It forms the base of the rally and is a key level for future price action.

Conclusion:

Bullish Outlook: The overall trend has been upward following the consolidation phase in mid-September. The price has since broken out of key support zones, and institutional activity suggests continued buying interest.

Watch Key Levels: Support is found around $481–$485, and resistance around $496–$497. A breakout above this resistance could signal another leg higher, while a pullback to the support zone may attract further buying interest.

IWM 0.07%↑

Key Observations from the Chart:

Largest Trades (Colored Circles): The five largest trades, marked by the colored circles, represent significant institutional involvement and critical points of price action. Let's break them down:

First Circle (Sept 30, $220.89): This trade stands out with the largest relative size (RS) of 32.65% and happens around a consolidation phase. The price holds near $221, indicating that this level served as support during this period.

Second Circle (Oct 2, $220.63): Another large trade happens near the same level as the previous one, reinforcing the support around $220-$221. These consecutive large trades suggest that institutions were accumulating shares in this zone.

Third Circle (Oct 10, $221.36): This occurs as the price breaks out from the previous range, which could signal a bullish move. This level ($221) becomes an important pivot point for future price action.

Fourth Circle (Oct 18, $225.65): This is the largest recent trade, representing a possible resistance level after the breakout. It's worth noting that the price did pull back slightly after hitting this high.

Price Levels with Greatest Institutional Activity (Dashed Blue Lines): The dashed blue lines indicate the price levels where institutions were most active, which often act as important support or resistance levels:

$222.50: The most significant activity occurred here with $5.6B notional value and 25.2M shares traded. This level marks a key resistance point, and the price struggled to move above it initially but broke out eventually.

$221.70: This level also saw strong activity ($5.02B, 22.6M shares) and acted as a support during the early consolidation phase.

$217.60: This lower level served as support when the price dipped in late September. With substantial institutional activity ($4.59B, 21.1M shares), this is a critical level to watch for future support in case of a retracement.

Volume and Relative Size (RS):

Largest Trade on Sept 30: The trade at $220.89, with a relative size (RS) of 32.65%, marks an important accumulation zone. Given the volume of shares and the RS, this level likely served as a significant accumulation area for institutions.

Other Significant Trades: Trades between Sept 24 and Oct 2 show RS values between 27% and 32%, reinforcing the importance of this price range as a critical accumulation zone. This suggests that large players were positioning themselves before the breakout that occurred later in October.

Price Clusters and Accumulation:

$220–$222 range: This zone saw several large trades and high activity, indicating a strong institutional interest in accumulation. Prices remained within this range for several days before breaking out.

$225–$226 range: After the breakout in early October, this zone acted as the next resistance level, where the price briefly consolidated before pulling back slightly. The high relative size of the trade at $225.65 suggests that this area could act as future resistance unless there is a strong push upward.

Technical Indicators:

Support Levels:

$220.50–$222.50: This zone saw the most institutional activity and served as a strong support during the consolidation phase. The price remained above this level throughout much of the time frame, suggesting that future retracements may find buying interest here.

$217.60: A key support zone from late September. If the price moves lower, this is another level to watch, where previous institutional buying took place.

Resistance Levels:

$225.65: This level coincides with the latest largest trade and marks a resistance area after the breakout. The price has struggled to move significantly higher from this level, so it will be key to watch if it can break through with strong momentum.

$226–$228: There are smaller clusters of resistance in this zone as well, where the price briefly tested but was unable to sustain the upward movement.

Breakout Potential:

Price broke out of the $220 range in early October, and institutional trades indicate that the momentum could continue higher. However, the resistance at $225.65 will be critical to watch. If the price can break above this, we could see a further rally.

Conclusion:

Bullish Bias: The trend has been bullish since early October after breaking out of the $220-$222 accumulation zone. Institutional activity supports this upward momentum, suggesting that large players are driving the price higher.

Key Levels: The $222.50 and $221.70 zones are strong support levels, with resistance near $225.65. If the price can break through this resistance, we may see further bullish movement. However, if price retraces, it is likely to find support around $220-$222.

DIA 0.23%↑

Key Observations from the Chart:

Largest Trades (Colored Circles): The largest trades are highlighted by the colored circles. Here’s the breakdown:

First Circle (Sept 18, $417.18): This large trade marks the beginning of the time frame, representing significant institutional accumulation after a price dip. The price stabilizes shortly after this trade, indicating that $417 is a strong support level.

Second Circle (Oct 1, $421.32): This large trade, which occurred during a consolidation phase, has a relative size (RS) of 7.28%. The price moves slightly higher after this, indicating potential accumulation at this level.

Third Circle (Oct 2, $421.40): Another large trade takes place at this price level, further solidifying the $421 area as an important support or accumulation zone. The back-to-back large trades suggest strong institutional interest here.

Fourth Circle (Oct 18, $432.24): This trade represents a more recent high, suggesting potential resistance around $432 after the breakout. The price appears to be testing this level for continuation or possible pullback.

Price Levels with Greatest Institutional Activity (Dashed Blue Lines): These horizontal dashed lines indicate price levels where institutional trades were most concentrated:

$421.40: This price level had the largest institutional activity ($314M notional value, 745K shares traded). It acts as a key support level during the price consolidation in late September and early October.

$417.20: Another support level, with $172M and 413K shares traded. This level held up during the price dips in mid-September and late September, suggesting a strong buying zone.

$416.50: This lower price level ($130M and 311K shares) served as a temporary support during the initial price drop in mid-September.

Volume and Relative Size (RS):

Largest Trade on Oct 1 ($421.32): The trade at $421.32, with an RS of 7.28%, represents one of the largest trades in this period. This level became a key pivot point and has acted as a strong accumulation area for institutional players.

Other Significant Trades: Trades between Sept 18 and Oct 18 show consistent RS values between 5.58% and 7.28%, indicating a significant number of institutional trades around the $417–$421 levels. These levels are important areas of support and accumulation during price consolidation.

Price Clusters and Accumulation:

$417–$421 range: This zone saw significant institutional accumulation and became the foundation for the price rally in mid-October. It is likely to act as strong support in case of a retracement.

$432 level: The price touched $432 and encountered resistance, as seen by the large trade in this zone on Oct 18. This will be a critical level to watch as it serves as the new resistance after the price breakout.

Technical Indicators:

Support Levels:

$421.40: The most significant institutional activity occurred at this level, making it a crucial support level. The price spent a lot of time consolidating around this zone, and it should serve as strong support in the event of a pullback.

$417.20: Another key support level, where institutional activity suggests accumulation. This is a secondary support level below $421.

Resistance Levels:

$432.24: This price level marks the most recent large trade and potential resistance. The price reached this level after a breakout but hasn’t yet moved significantly higher. A breakout above $432 would suggest further bullish momentum.

$428–$430 range: This zone acted as a temporary resistance during the price rally, though the price managed to break through this level.

Breakout Potential:

The price has broken out of the $417–$421 range and is now testing the $432 level. If the price can clear this resistance, we could see another leg higher. Conversely, if the price fails to break above this level, a pullback to the $421 support zone is possible.

Conclusion:

Bullish Bias: The overall trend appears bullish after breaking out of the $417–$421 accumulation zone. Institutional activity supports the idea that large players have been buying at these levels, providing a solid base for the recent rally.

Key Levels: Watch the $421.40 support level and the $432 resistance level. A break above $432 could lead to more upside, while any retracement is likely to find support near $421.

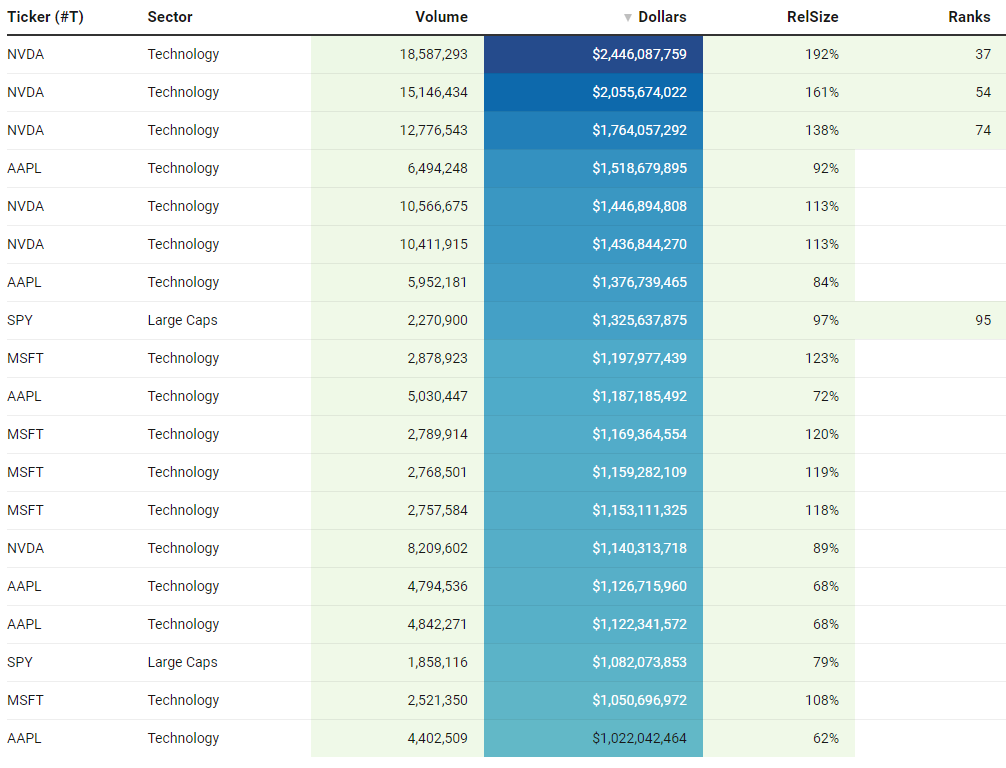

Top Institutional Order Flow

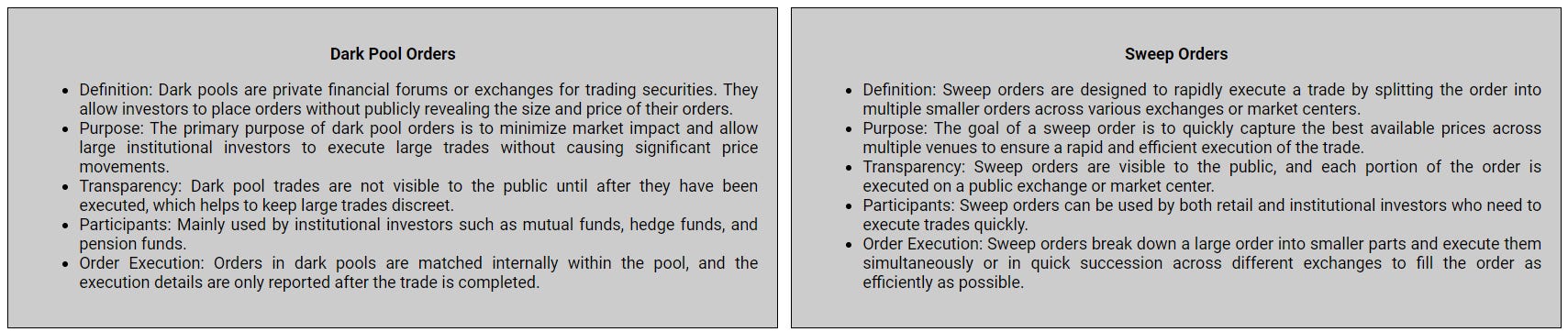

Many excellent trade ideas and sources of inspiration can be found in these prints. While only the top 30 from each group are displayed, the complete results are accessible in VolumeLeaders.com for your convenience to explore at any time. Remember to configure trade alerts within the platform to ensure you never overlook institutional order flows that capture your interest or are significant to you. The blue charts encompass all types of trades, including blocks on lit exchanges; the purple charts exclusively depict dark pool trades; and the green charts represent sweeps only.

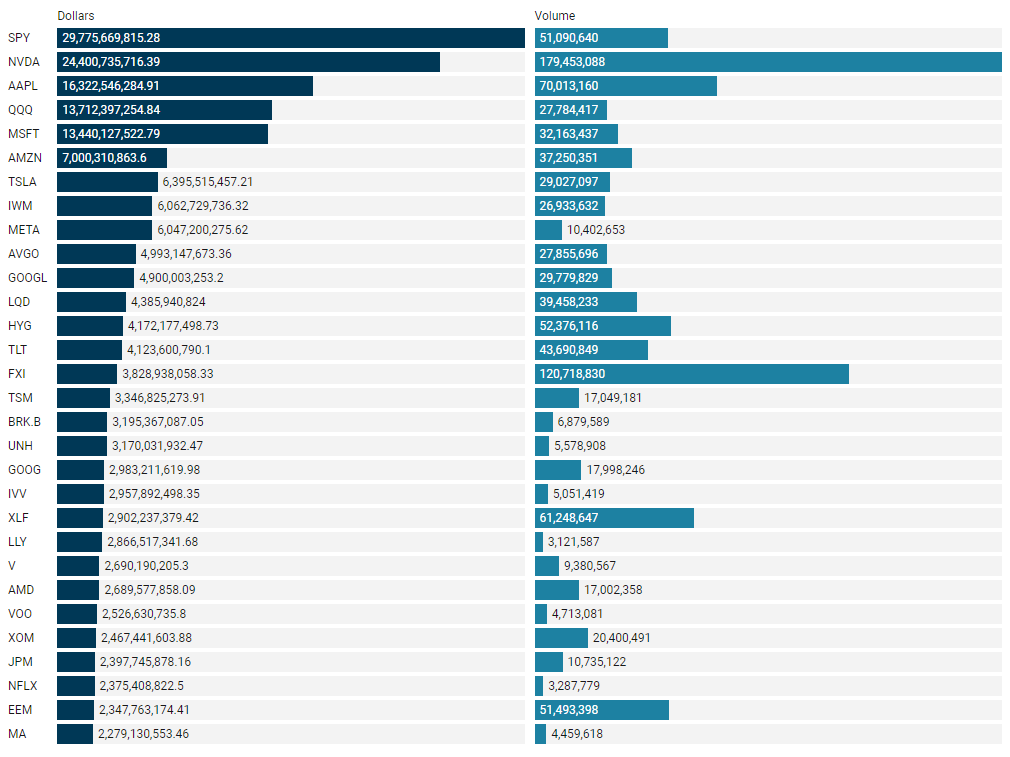

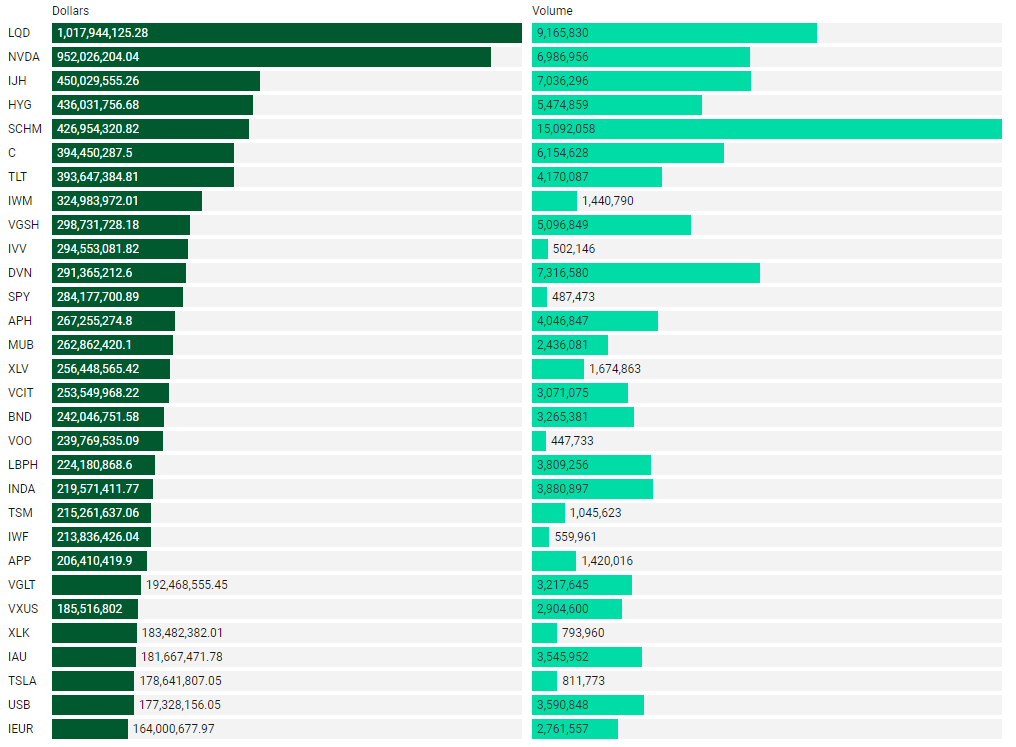

Top Aggregate Dollars Transacted by Ticker

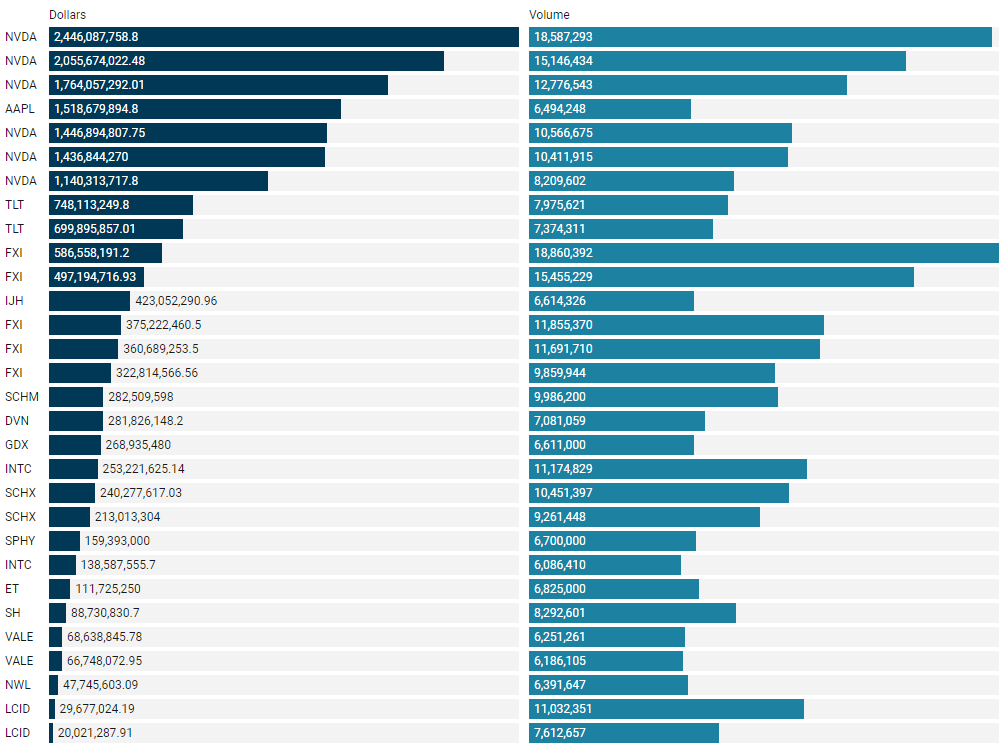

Largest Individual Trades by Dollars Transacted

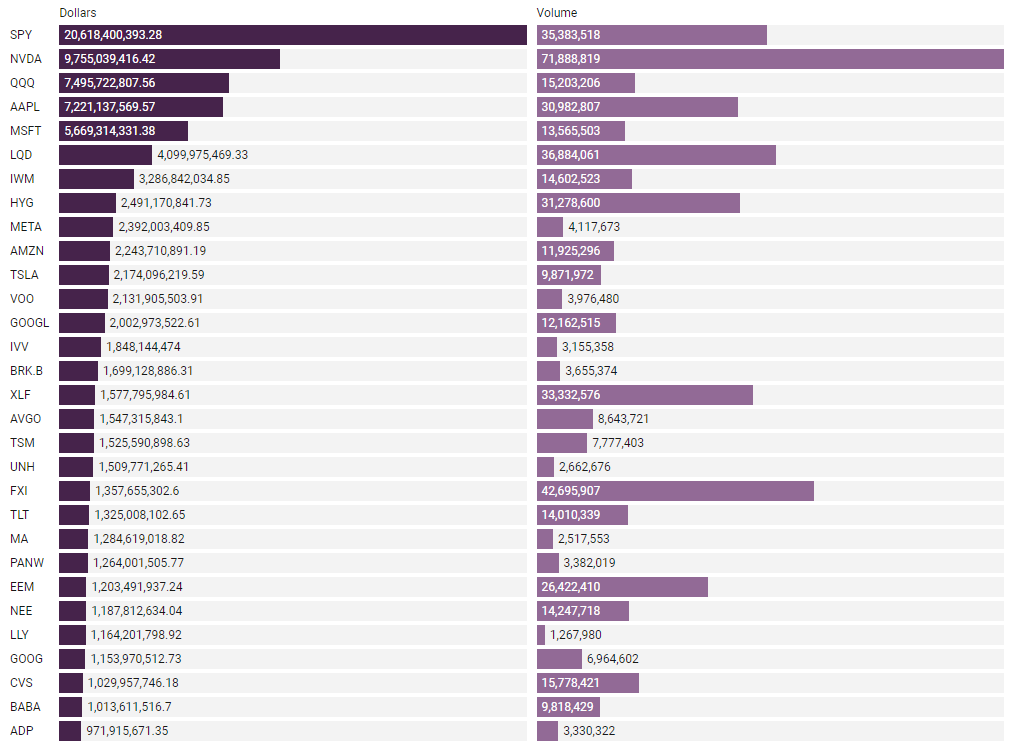

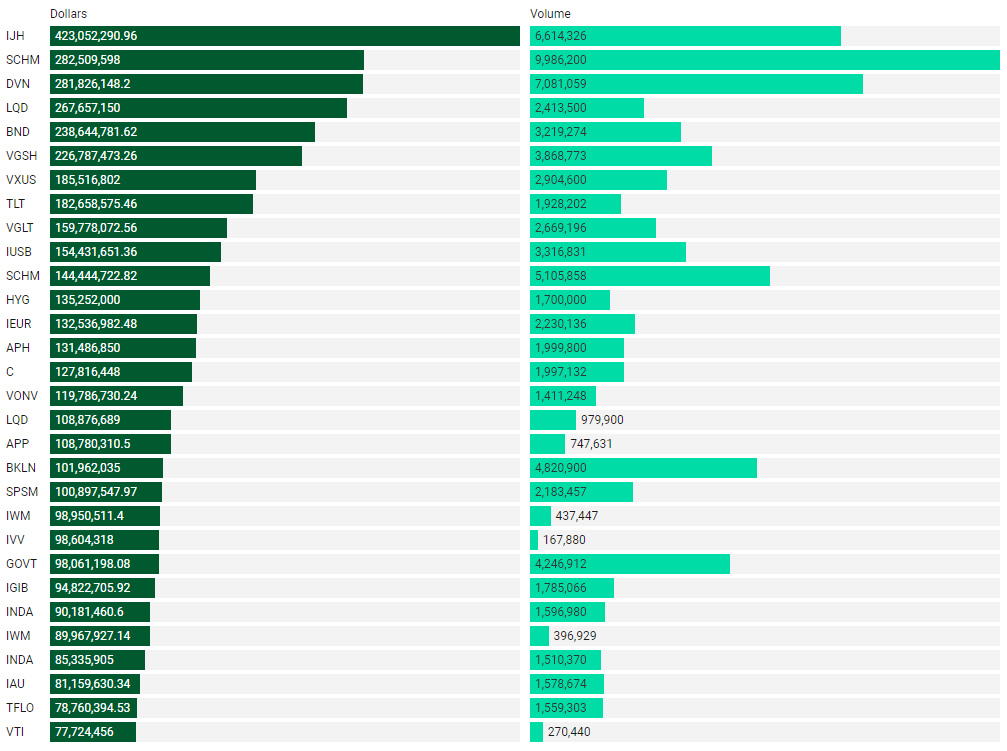

Top Aggregate Dark Pool Activity by Ticker

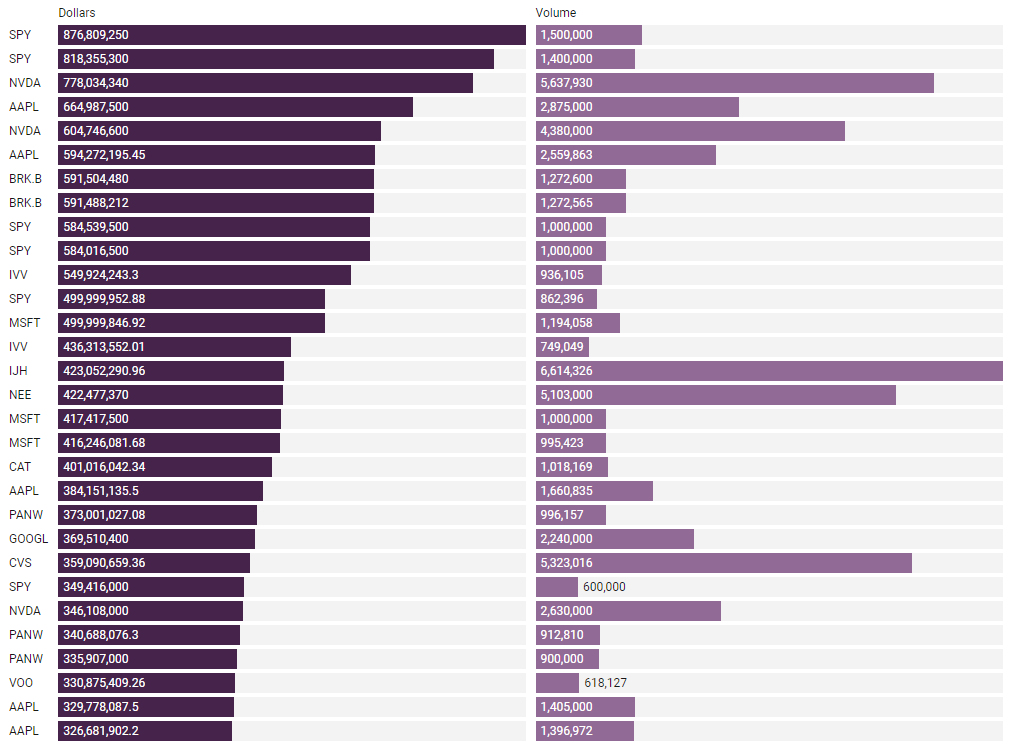

Largest Individual Dark Pool Blocks by Dollars

Top Aggregate Sweeps by Ticker

Top Individual Sweeps by Dollars Transacted

Institutional S/R Levels for Individual Tickers

Please read “Institutional S/R Levels For Major Indices” at the top of this stack to understand the nature and importance of what we’re looking at here visually. Institutions leave footprints that VolumeLeaders.com can illustrate for you while providing context to assess things like institutional conviction and urgency.

1. Largest Trades (Blue and Orange Circles)

The chart highlights several significant institutional trades, represented by the blue and orange circles. Here's what these areas indicate:

Blue Circles (Sept 19 to Sept 25): These represent large trades within the $86-$89 range. The high relative sizes (RS), with the largest at 99.62% on Oct 9 ($91.36), indicate substantial accumulation during this period. The cluster of large trades in this range suggests that this area served as a strong accumulation zone for institutional players.

Orange Circles (Oct 9): Large trades occurred after the breakout above $91, marking a possible distribution phase after the upward momentum. The RS values of 76.68% and 99.62% around $91.36 suggest that institutional players are actively involved at these levels, which could act as resistance moving forward.

2. Key Price Levels with Institutional Activity (Dashed Blue Lines)

The horizontal dashed lines mark the most important price levels where institutional activity was concentrated. These levels often serve as strong support or resistance points in future price action:

$86.00: The largest trade occurred at this price level ($1.98B, 23M shares), indicating significant support here. This level is critical, as it was tested multiple times and marked a low point in the chart.

$88.50 - $89.00: The price consolidated within this range during mid-September, with strong institutional interest around $1.8B - $1.7B. This range is likely to serve as support if the price retraces.

$91.00 to $92.00: This area saw significant trades on October 9, which may act as resistance in the future. A break above these levels could indicate the potential for further upward movement.

3. Volume and Relative Size (RS)

Largest Trade on Oct 9: The trade at $91.36 with a relative size (RS) of 99.62% is noteworthy. This indicates the largest relative size during the observed period, showing heavy institutional interest at this level, which may represent either accumulation for further upside or distribution, depending on future price action.

Consistent Large Trades: The high RS values across multiple trades from Sept 19 to Oct 9 (ranging from 43% to 76%) suggest consistent institutional activity. This supports the view that large players were positioning themselves for the breakout that occurred in early October.

4. Price Levels as Support and Resistance

Support Levels:

$86.00: This is a strong support level, backed by the largest institutional activity. If the price retraces, this level is likely to act as a floor.

$88.50 - $89.00: This zone saw significant trading volume and is another support level to watch.

Resistance Levels:

$91.00 - $92.00: The large trades occurring in this range indicate potential resistance, where institutional players might have begun taking profits after the breakout.

Conclusion:

Bullish Bias with Caution: The chart indicates a recent bullish breakout above $89, driven by substantial institutional buying activity. However, the $91-$92 zone is crucial resistance, and the price's ability to sustain above this level will determine if further gains are possible.

Key Levels to Watch: Support is found at $86.00 and $88.50, while resistance is expected around $91-$92. If the price clears $92 with strong volume, it could signal the potential for a continued rally. Conversely, failure to break this resistance could lead to a pullback toward the $88 support.

1. Largest Trades (Blue Circles)

Blue Circles (Sept 19 to Sept 24): These represent significant institutional trades around $240 to $250. The largest trade, with a 192.40% relative size (RS), occurred at $238.25 on Sept 19, signaling massive accumulation at that price point. Other notable trades in this period show relative sizes between 56% and 65%, suggesting strong institutional buying interest.

Late Trade on Oct 11 ($220): A large institutional trade occurred at $220.14 with an RS of 56.37%, likely marking a key price level for institutional support.

2. Key Institutional Activity Price Levels (Dashed Blue Lines)

$237.10: The highest institutional trade occurred here, with a value of $60.1B and 260M shares traded. This is a critical resistance level based on the volume of trades executed at this price.

$238.30 - $250.50: This price range has seen extensive institutional activity. The $238-$239 level, where the largest RS occurred (over 190%), is likely a support zone, while $250.50 may serve as near-term resistance.

$220.00: Institutional trades that occurred at this level during the price drop after Oct 10 suggest potential support here. Institutional buyers may step in around this price in case of further weakness.

3. Volume and Relative Size (RS)

Largest Trade on Sept 19: The largest trade, with a 192.40% RS, occurred at $238.25. This indicates a critical price level where institutions showed significant buying interest, which will likely serve as a support level moving forward.

Additional Significant Trades: Trades between Sept 19 and Sept 24 show strong institutional activity in the $240-$250 range, with relative sizes ranging from 49% to 65%. These trades suggest heavy buying pressure during this time.

4. Price Levels as Support and Resistance

Support Levels:

$220.00: This level saw a large trade on Oct 11, which may act as strong support in the near future.

$237.10 - $240: Given the institutional activity in this price range, expect strong support here if the price declines toward these levels.

Resistance Levels:

$250.50: This price level saw large trades, making it a key resistance point to watch in the near term. If the price breaks above this, it could signal a move higher.

Conclusion:

Support Zones: The $220-$238 area represents the strongest support, with significant institutional buying interest in this range. If the price drops back to these levels, expect potential institutional buying to resume.

Resistance Levels: The $250-$255 range is a key resistance zone, and any breakout above this range could signal further upside.

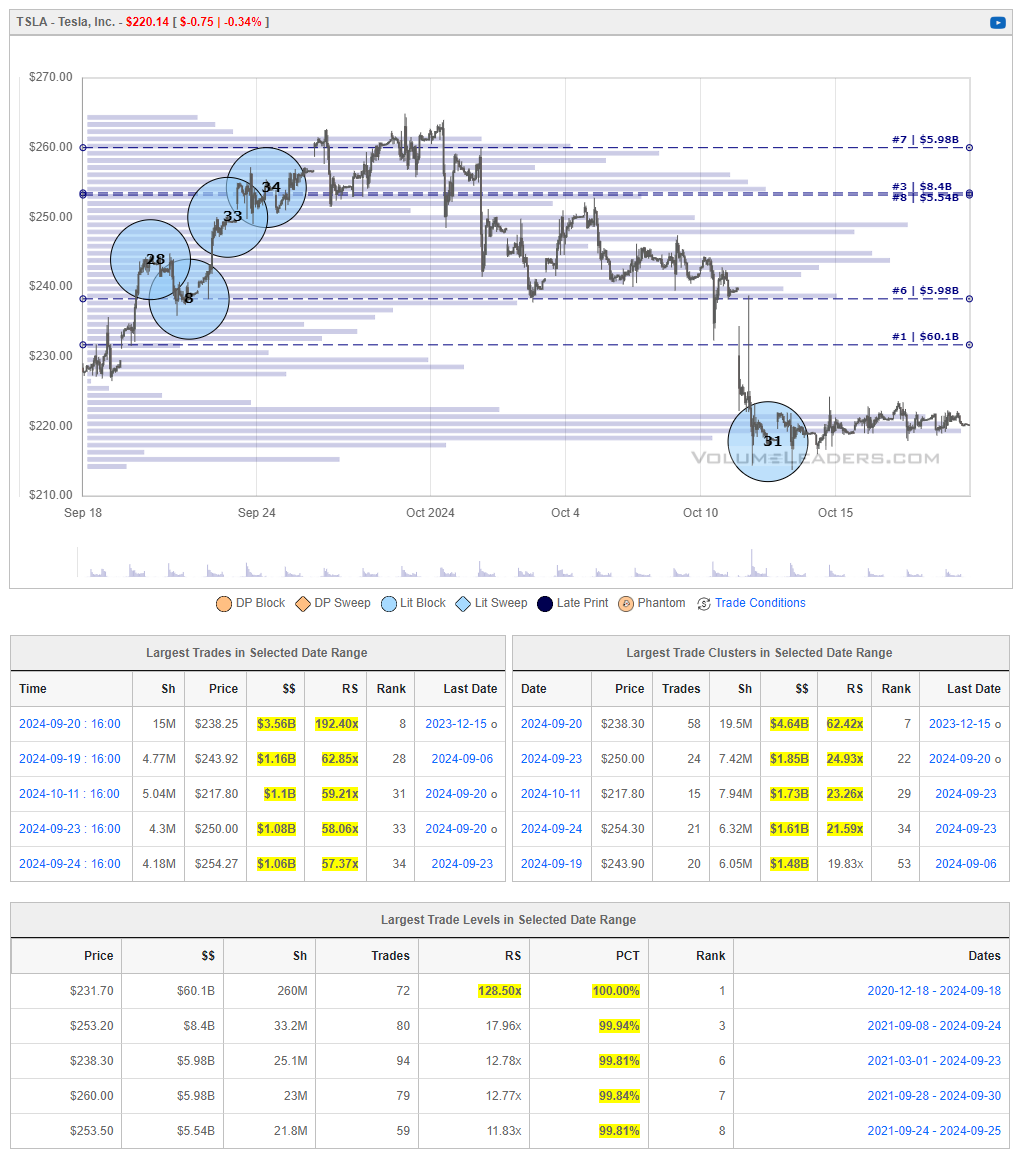

Tesla's price movement will largely depend on how it reacts to these key institutional price levels in the coming days, with $220 and $250 being critical zones to watch.

1. Largest Trades (Blue Circles)

First Circle (Sept 19-20): The most significant trade occurred at $79.06, with a 267.30% relative size (RS) on Sept 30, representing a substantial institutional buy of $1.08B (highlighted in the chart). This large trade, followed by other high RS values (ranging from 86% to 139%), indicates heavy accumulation around $79-80.

Other Large Trades: Institutional activity continued into early October around the $80.90 and $81.30 levels, with substantial relative sizes between 52% and 86%, marking those areas as key zones of interest.

2. Price Levels with Institutional Activity (Dashed Blue Lines)

$79.10: This price level saw the most significant institutional trading activity, with $2.1B in trades. This level, backed by the large size and volume, is a critical support zone.

$80.90 - $81.30: These price levels represent institutional trading activity in the range of $600M to $700M. This zone is likely to act as resistance if the price approaches it again, given the concentration of institutional selling.

3. Volume and Relative Size (RS)

Largest Trade on Sept 30: The trade at $79.06 with an RS of 267.30% is the most significant event in this period, representing an enormous volume of shares traded relative to the average. This suggests that institutional investors were aggressively accumulating around this level, making it a strong support level.

Additional Large Trades: Several other significant trades occurred at slightly higher levels ($80-$81), but with relatively smaller RS values, suggesting that this was more of a distribution zone.

4. Support and Resistance Levels

Support Levels:

$79.10: This is the most important support level, reinforced by massive institutional buying activity. Any price dips near this area will likely encounter strong buying interest.

$80.50: A secondary support level where institutional buyers showed interest.

Resistance Levels:

$81.30: A key resistance level based on institutional activity. There was significant selling around this level, and any upward movement toward this price will likely encounter resistance.

$80.90 - $81.00: Another resistance zone where several large trades occurred, indicating this price range may cap the price if it moves higher.

Conclusion:

Bullish Bias with Key Resistance: Walmart's price has seen heavy institutional accumulation around $79, which is now a critical support zone. If the price retraces to this level, expect institutional buyers to step in. However, the $81-$81.30 range is likely to act as strong resistance, with institutional sellers showing up at those levels.

Key Levels to Watch: Watch for support around $79-$80 and resistance at $81-$81.30. A break above $81.30 with strong volume could indicate further upside, while failure to hold the $79 support might lead to additional downside pressure.

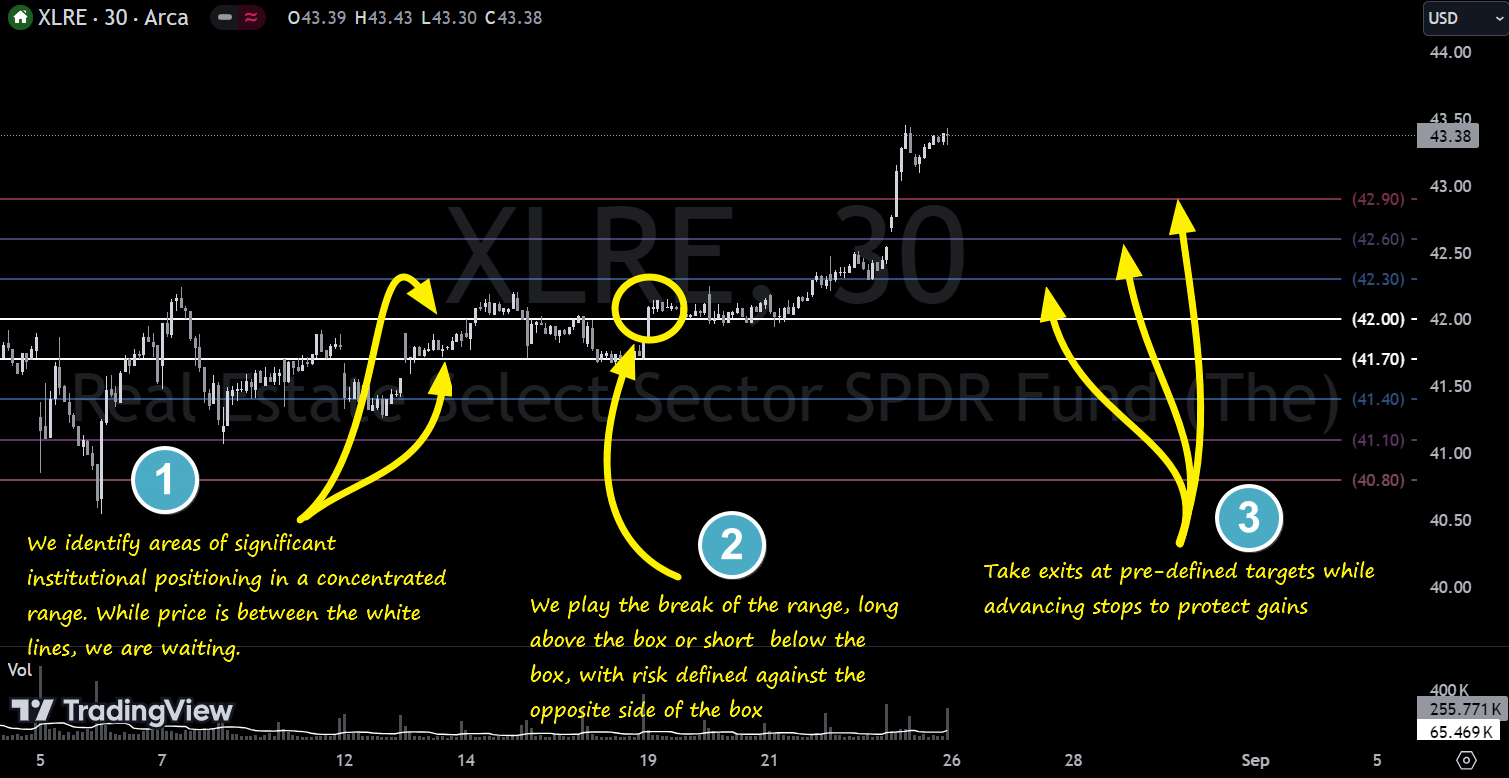

VL Precision Swings

This week we’re featuring additional screened trade ideas from one of our backtested proprietary signals for tactical swings called IBB - Institutional Breakout Boxes. The IBB Setup identifies an area of significant institutional positioning within a tight, concentrated price range, forming what we call a breakout box. This setup captures the potential energy built up as large players accumulate or distribute positions, creating a high-probability opportunity for explosive moves once the price breaks out of this zone. The precision of this setup allows traders to capitalize on the momentum generated by institutional forces, with clearly defined risk and reward parameters. These trades typically last from 2-days to 2-weeks and given targets are designed for tactical swings/base hits; more patient, longer-term swing traders frequently find that these ideas often provide excellent entries that help them get into risk-free runners quickly that fully play out over a longer time horizon. I highly encourage you to revisit prior recommendations - each week produces a couple tickers that make a large move all at once but the others often have more juice to keep running, all due to the power of institutional positioning.

Note, these are shared for educational and entertainment purposes only and do not constitute financial advice. Any trades referenced are done in simulated accounts with paper money.Here’s an example from XLRE:

Here is how last week’s setups played out:

AEP: +1.8%, all 3 targets met

AVTR: +3.95%, T1 and T2 met, runners stopped.

BND: 0%

DIS: +2.54%, all targets met

GMAB: +2.75%, T1 met, runners on for deeper targets

HDB: +1.95%, T1 achieved, runners stopped

INDA: +0.25%, no targets yet met, full position still on

PDD: +11%, T1+T2 met, runners still on for T3

SO: +2%, all targets met

XOP: +3.41%, T1+T2 met, runners still on for T3

Here are a few setups you can watch this week. If you’re a VL Subs, you can get all 22 setups and our market analysis on each in the #precision-swings channel in the VL Community Discord.

ALB 6.10%↑

1. Lithium Demand and Market Position: Albemarle remains a leader in the lithium industry, and demand for lithium continues to grow due to the rapid expansion of the electric vehicle (EV) market. Although Albemarle has faced some headwinds, the demand for lithium for EV batteries, driven by global shifts toward renewable energy and decarbonization, positions it well for long-term growth

2. Strategic Partnerships and Potential Acquisitions: Albemarle has been involved in potential deals and acquisitions, including rumors of Rio Tinto's interest in lithium. Such partnerships could bolster its market presence, helping the company take advantage of rising lithium prices as the EV market grows

3. Future Revenue Growth: Although revenue has taken a significant hit in 2024 due to market fluctuations and lithium pricing, Albemarle's revenue is projected to rebound significantly in the next few years. Analysts expect revenues to grow by around 11% in 2025, and EPS is forecasted to recover sharply from current lows

Risks to Consider:

Albemarle has faced recent volatility, with a 41% drop in revenue this year and significant fluctuations in lithium prices. Furthermore, some analysts have downgraded their price targets, citing concerns over lithium price volatility and production issues

The stock is currently trading well below its 52-week high, and analysts have issued mixed ratings, with some holding a cautious outlook

Overall, Albemarle's strong position in the lithium market and its potential for recovery make it an interesting long-term investment, particularly as lithium demand continues to grow. However, short-term volatility and risks related to pricing should be carefully monitored.

BA -2.62%↓

Boeing is facing several critical challenges that suggest a bearish outlook in the short to medium term:

Financial Struggles: Boeing recently released disappointing preliminary Q3 2024 results, projecting significant pre-tax charges of $3 billion for its 777X and 767 programs, coupled with $2 billion in charges for its defense programs. The company expects an overall GAAP loss per share of ($9.97) for the quarter and negative operating cash flow of ($1.3 billion)

Ongoing Labor Strikes and Delays: Boeing is grappling with a major work stoppage from the International Association of Machinists (IAM) union, which has severely impacted its production schedules, including delays in the 777-9 and 777-8 aircraft deliveries until 2026 and 2028, respectively. This disruption has also affected Boeing's key government contracts, such as the KC-46A

Analyst Downgrades: Several analysts have recently cut their price targets for Boeing, citing the ongoing strikes and increased costs. Despite some long-term optimism, analysts from JPMorgan and TD Cowen have lowered expectations, with potential further downside in the near term as Boeing faces a $15 billion equity raise in 2025 to address its cash burn

Given the combination of operational setbacks, financial challenges, and ongoing labor disputes, Boeing's stock may struggle to gain positive momentum in the coming months

HUM -2.50%↓

Strong Earnings Performance: Humana has demonstrated solid financial performance, with Q2 2024 earnings per share (EPS) of $6.96, significantly beating analyst expectations of $5.89. Additionally, the company's revenue increased by 10.4% year-over-year, indicating strong operational performance in a competitive sector

Undervalued Based on Recent Declines: Humana's stock has experienced a steep decline of over 30% in the last three months, primarily driven by Medicare-related regulatory challenges. Despite this, Humana's current price is now trading near its 52-week low, making it potentially undervalued with room for recovery as the regulatory headwinds ease

Institutional Confidence: Despite recent volatility, 92% of Humana’s shares are held by institutional investors, indicating long-term confidence in the company. This strong institutional backing can help support the stock as it navigates short-term challenges

Medicare and Healthcare Expansion: Humana's broad focus on Medicare and healthcare services, through its partnerships and contracts with government programs, provides steady growth opportunities as the aging population expands. Furthermore, analysts project an upside potential with price targets reaching up to $308

Risks to Consider:

Medicare Rating Declines: Humana has recently suffered from Medicare-related rating downgrades, which could impact its future financials, specifically regarding government reimbursements

Volatility and Downside Pressure: The stock remains highly volatile, trading well below its moving averages, and may continue to face downward pressure in the short term as it works through regulatory and operational challenges

Overall, Humana presents a compelling long-term buy opportunity, especially if it can navigate the current Medicare-related issues. However, short-term volatility should be considered when investing.

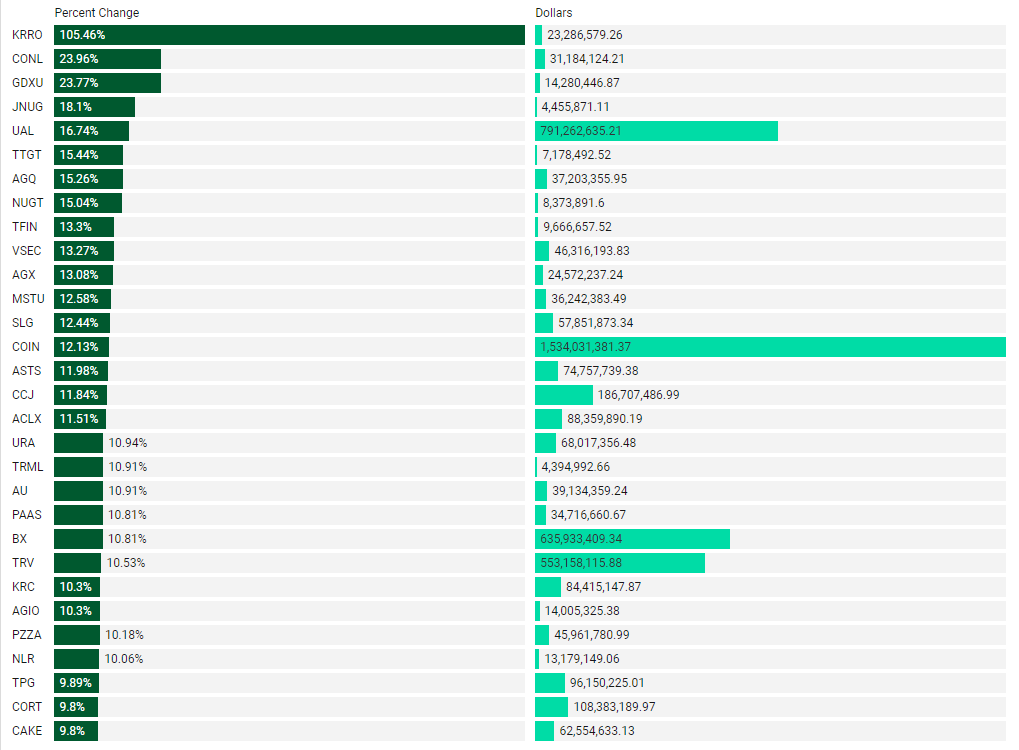

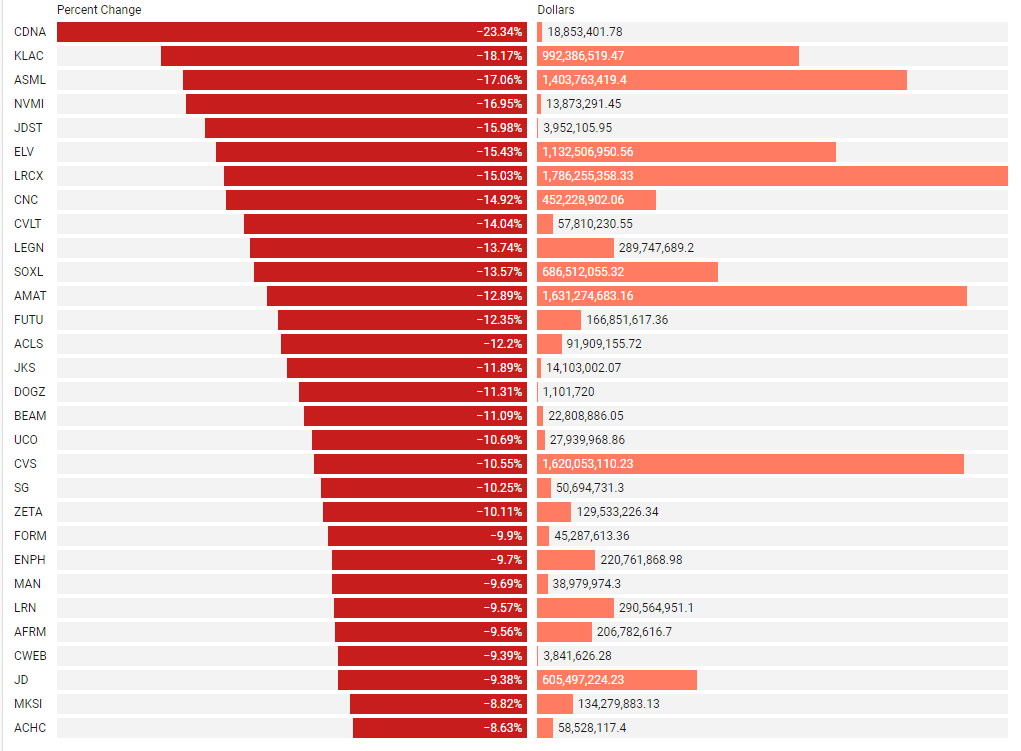

Institutionally-Backed Gainers & Losers

If you’re going to bet on a horse, consider one that is officially endorsed by an institution! These are the top percent gainers (green) and percent losers (red) from this week’s open-to-close that had a trade price greater than $20 and institutional involvement. Continue watching tickers from prior stacks as these frequently turn into multi-leg trades with a lot of movement!

Top Institutionally Backed Gainers

Top Institutionally Backed Losers

Billionaire Boys Club

Tickers that printed a trade worth at least $1B last week get a special shout-out… Welcome to the club. Subs should login to VolumeLeaders.com to get the exact trade price and relevant institutional levels around the trade - these are massive commitments by institutions that should not be ignored.

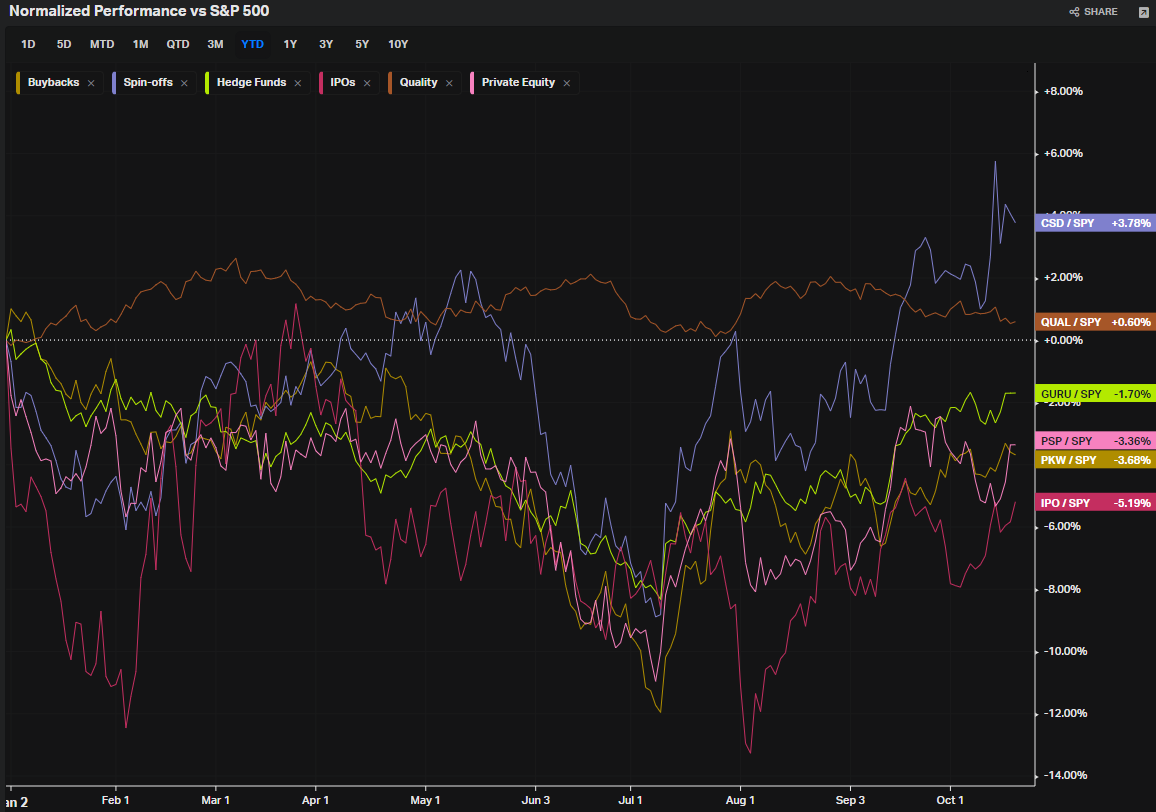

Summary Of Thematic Performance YTD

VolumeLeaders.com provides a lot of pre-built filters for thematics so that you can quickly dive into specific areas of the market. These performance overviews are provided here only for inspiration. Consider targeting leaders and/or laggards in the best and worst sectors, for example.

S&P By Sector

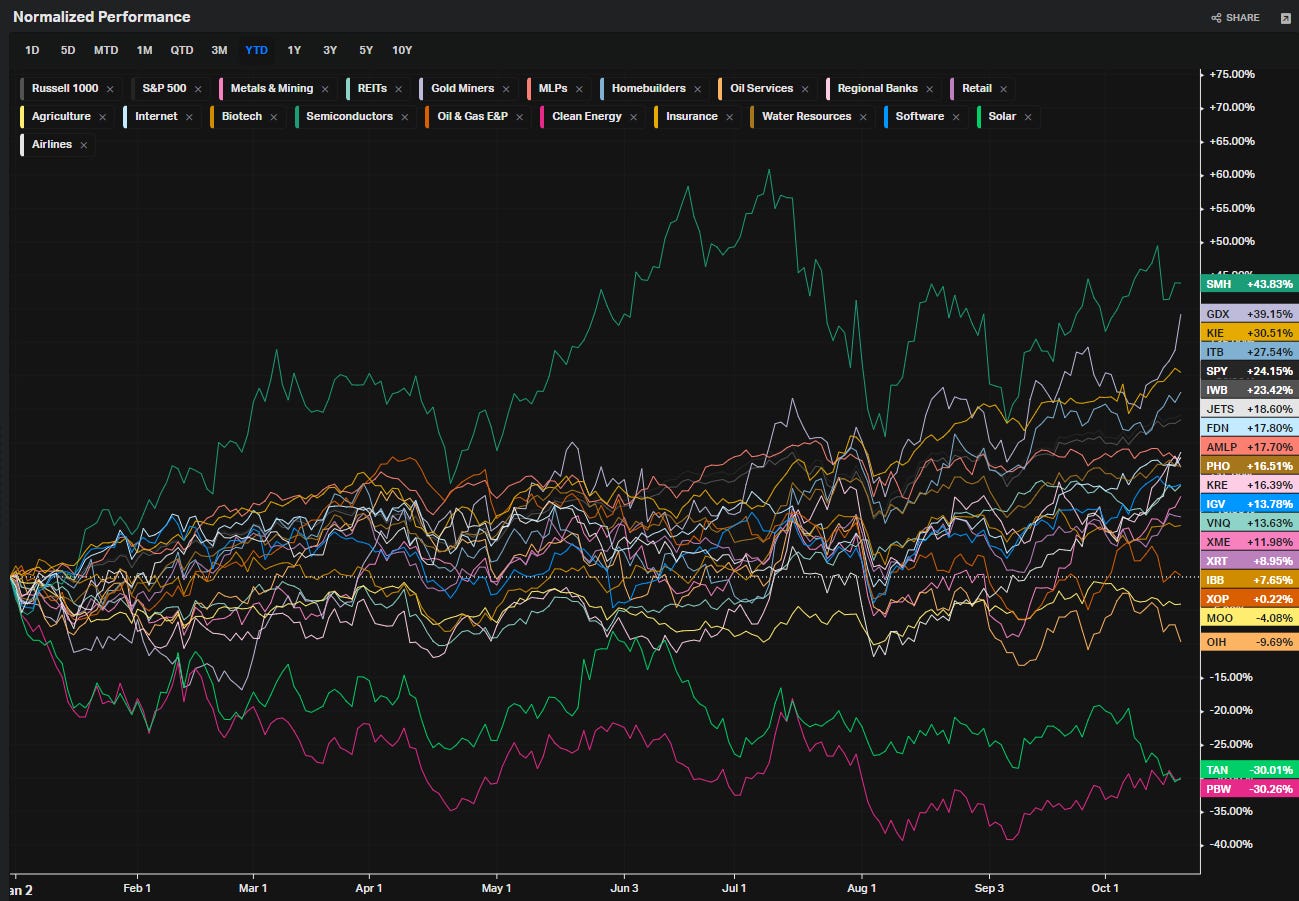

S&P By Industry

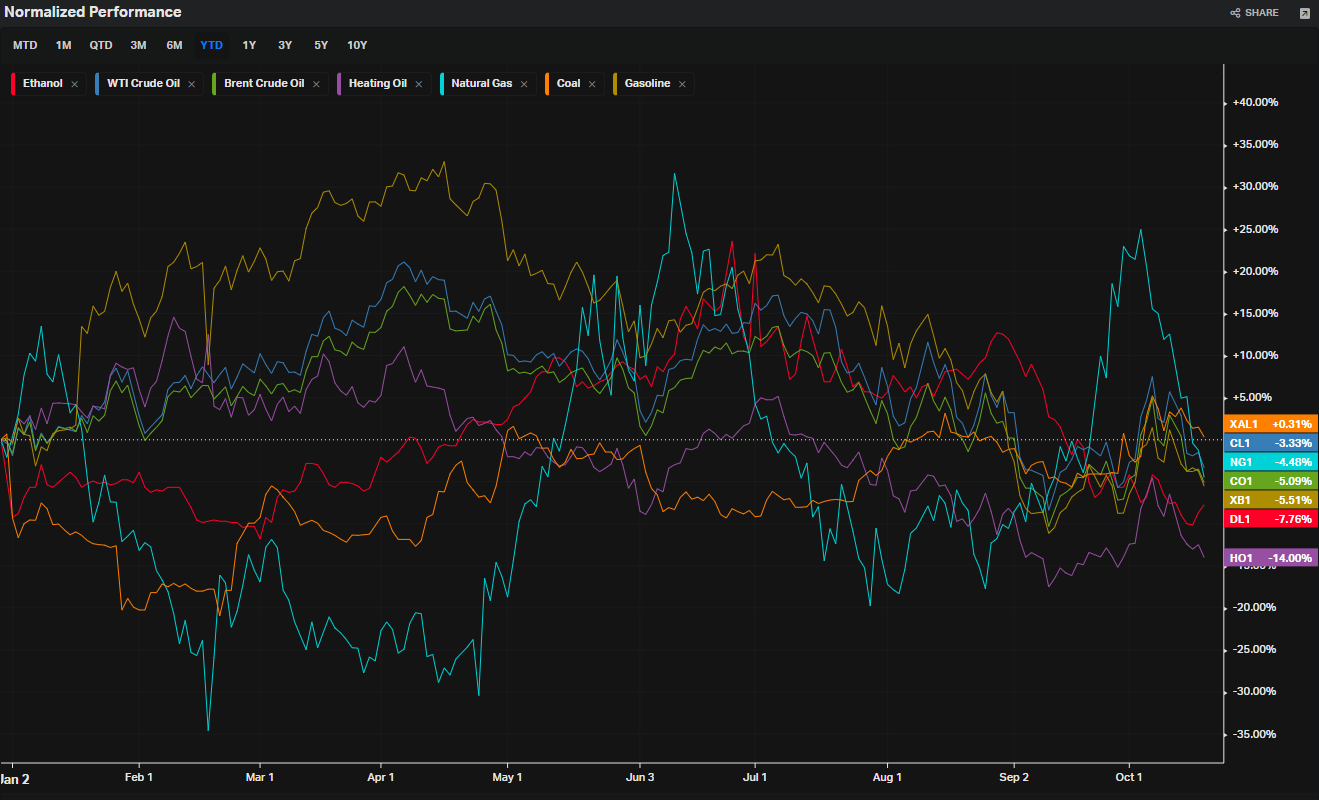

Commodities: Energy

Commodities: Metals

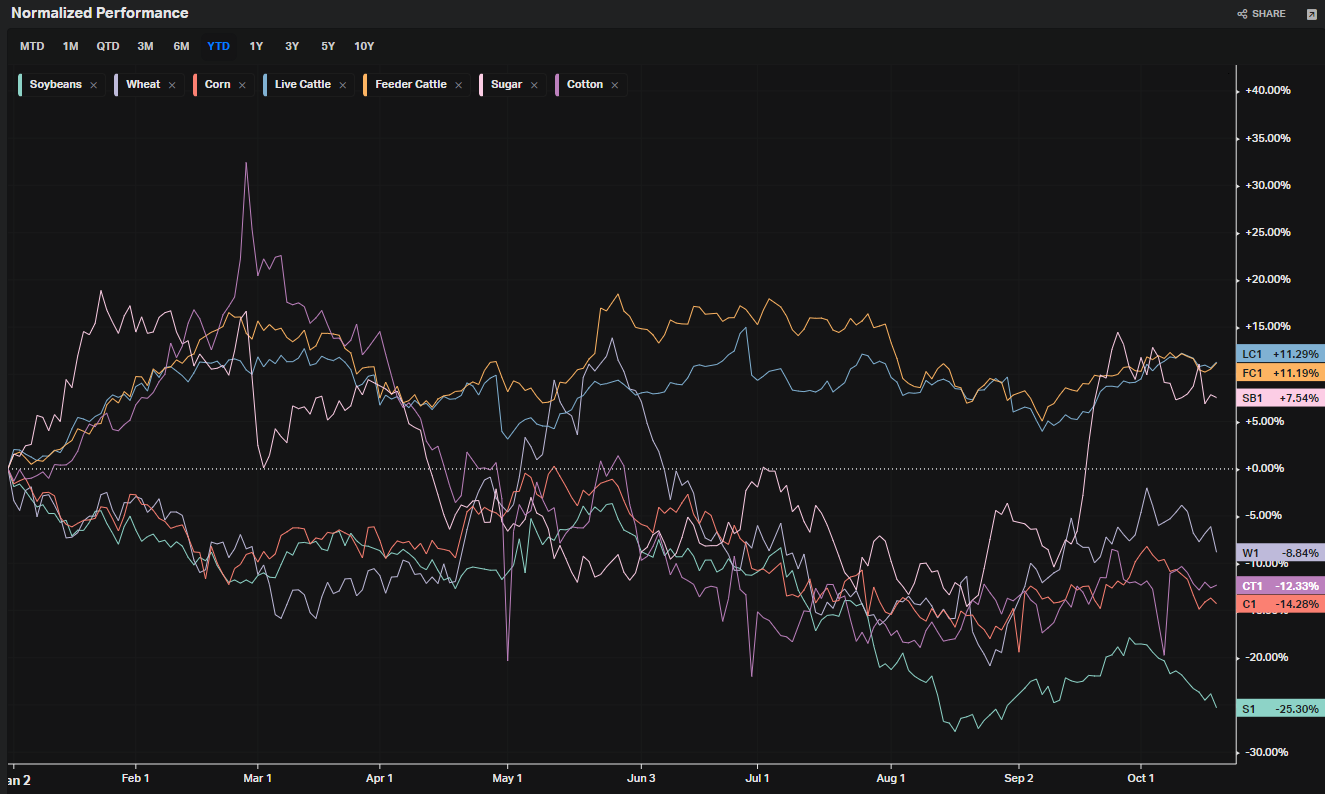

Commodities: Agriculture

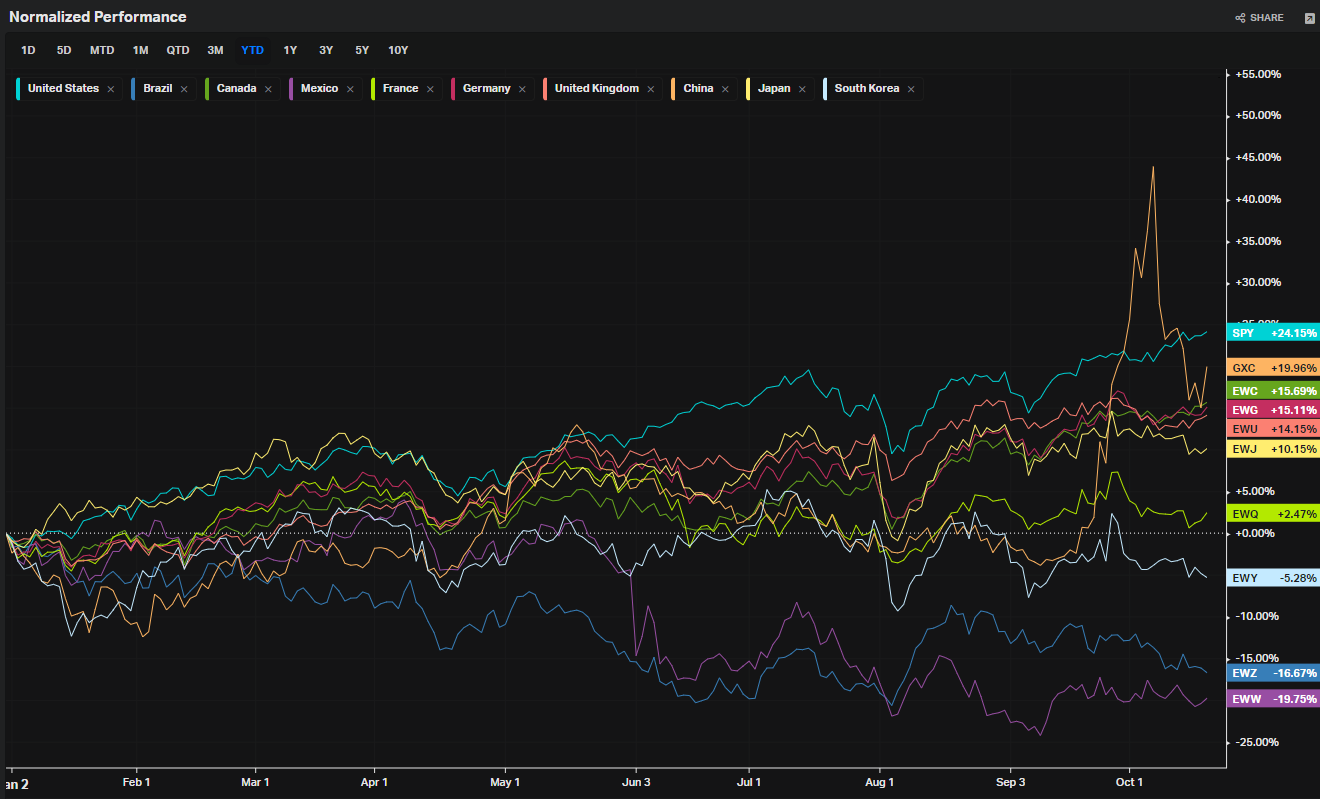

Country ETFs

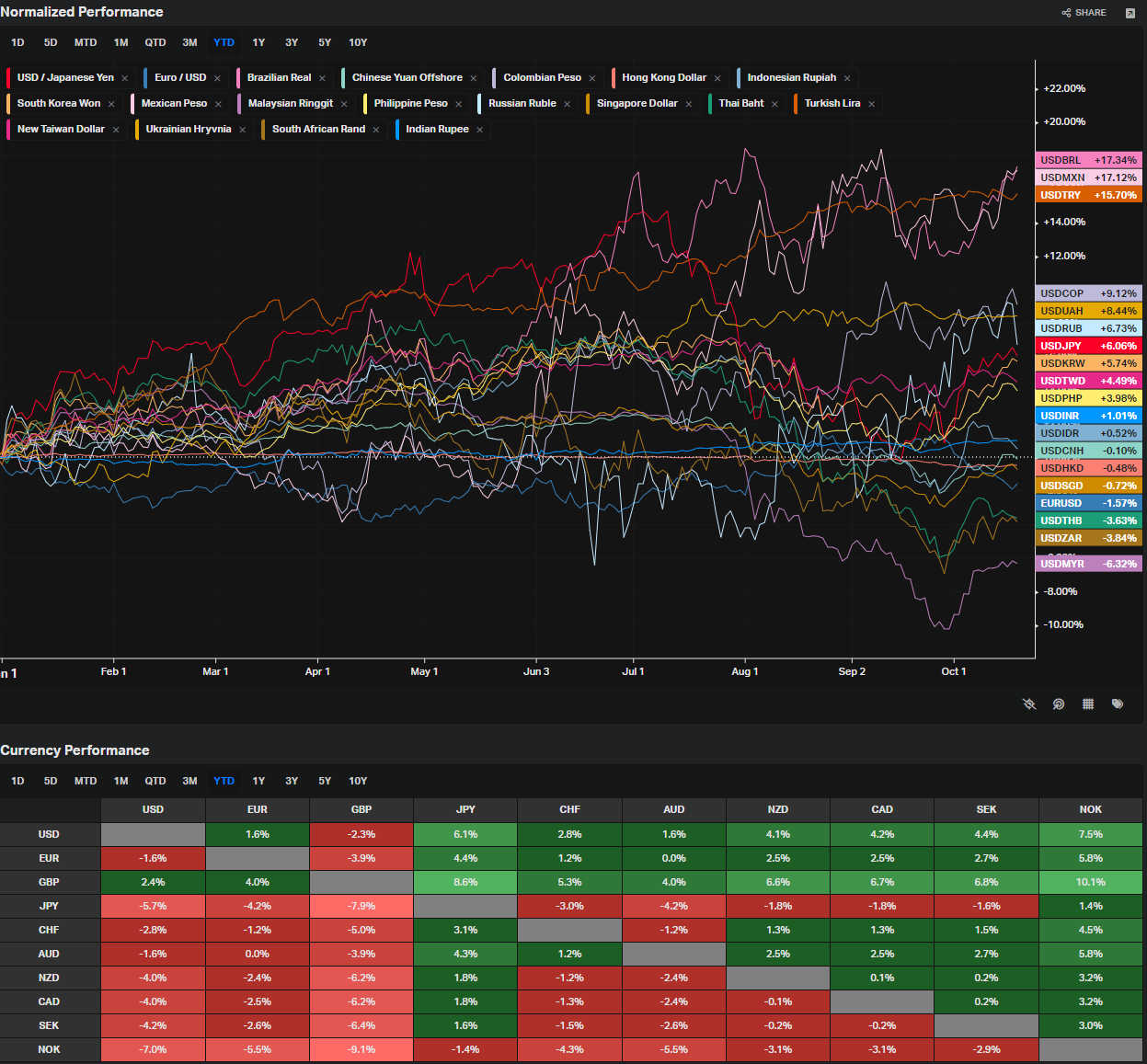

Currencies

Global Yields

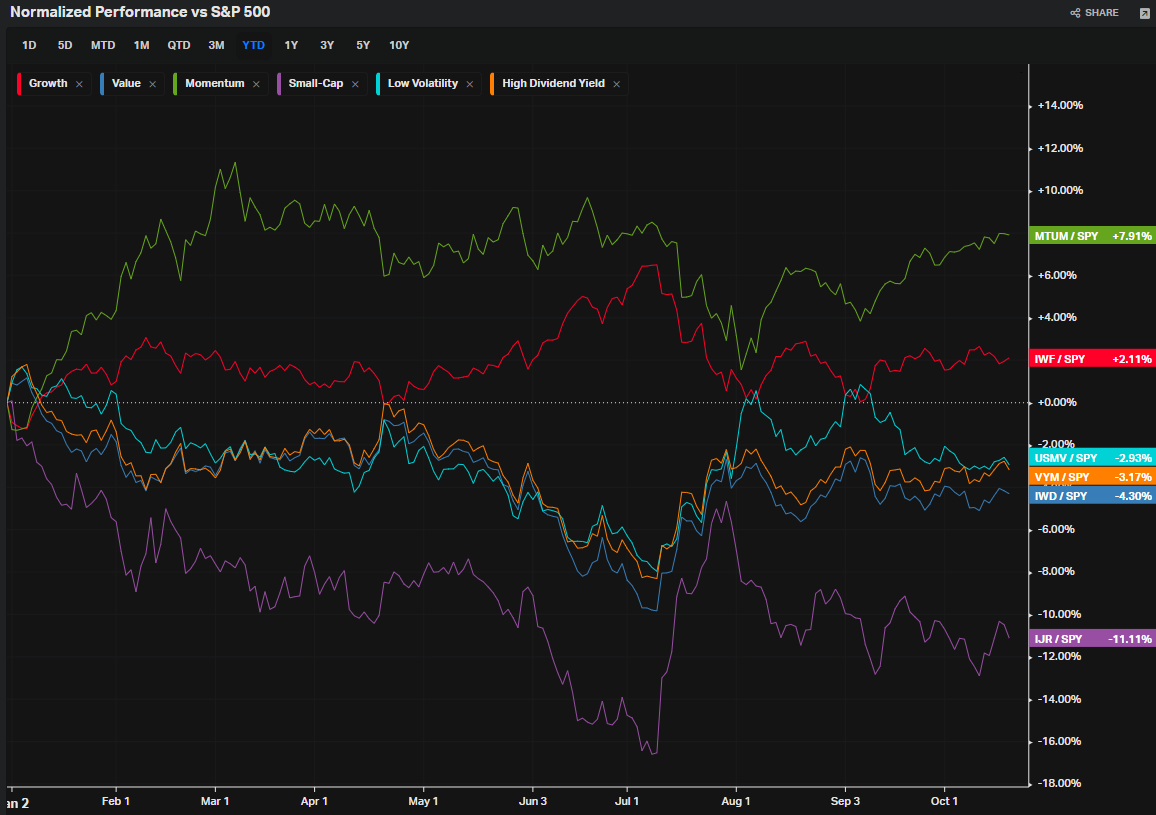

Factors: Size vs Value

Factors: Style

Factors: Qualitative

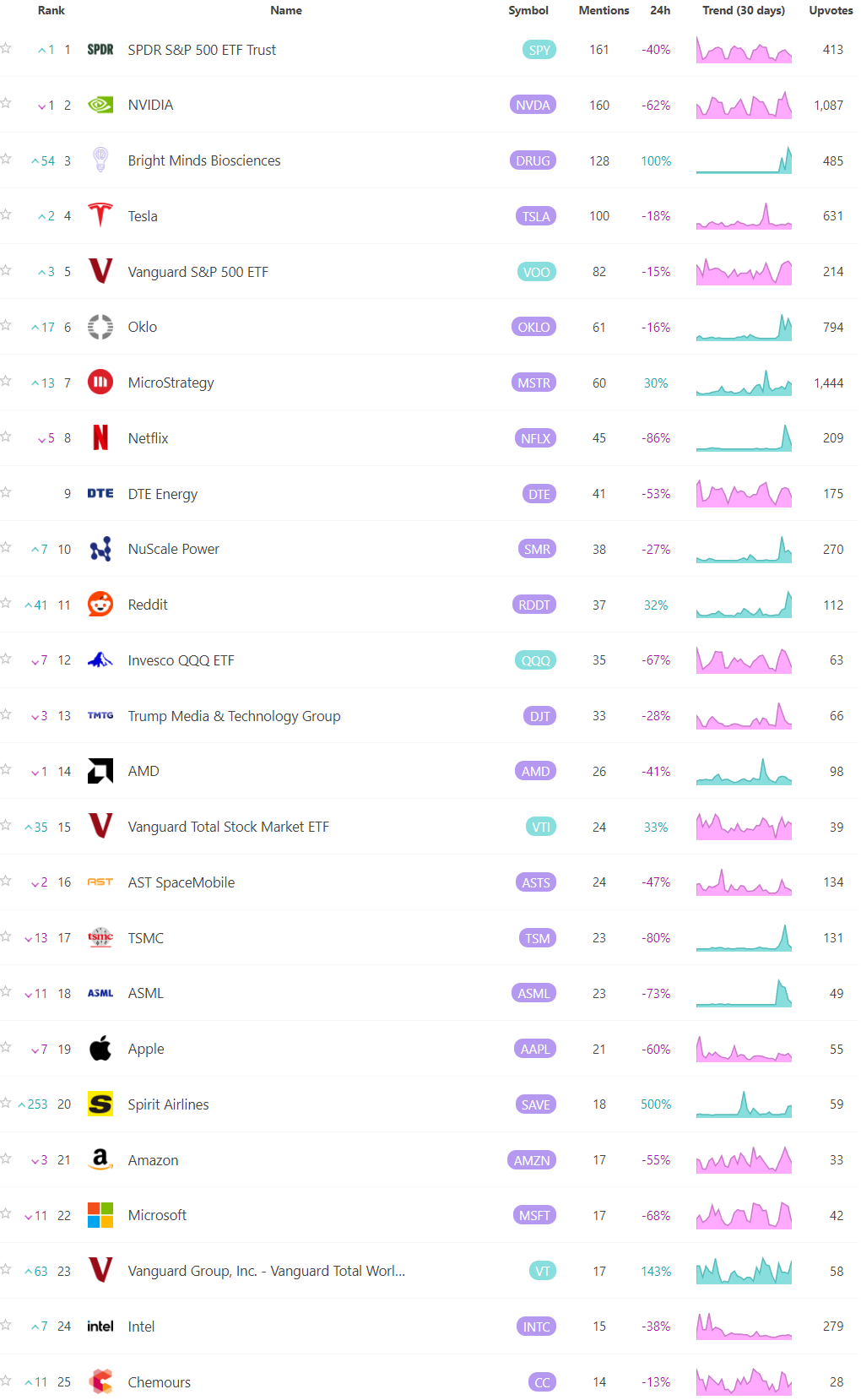

Social Media Favs

Most mentioned/discussed tickers on Reddit from some of the most active Subreddits for trading:

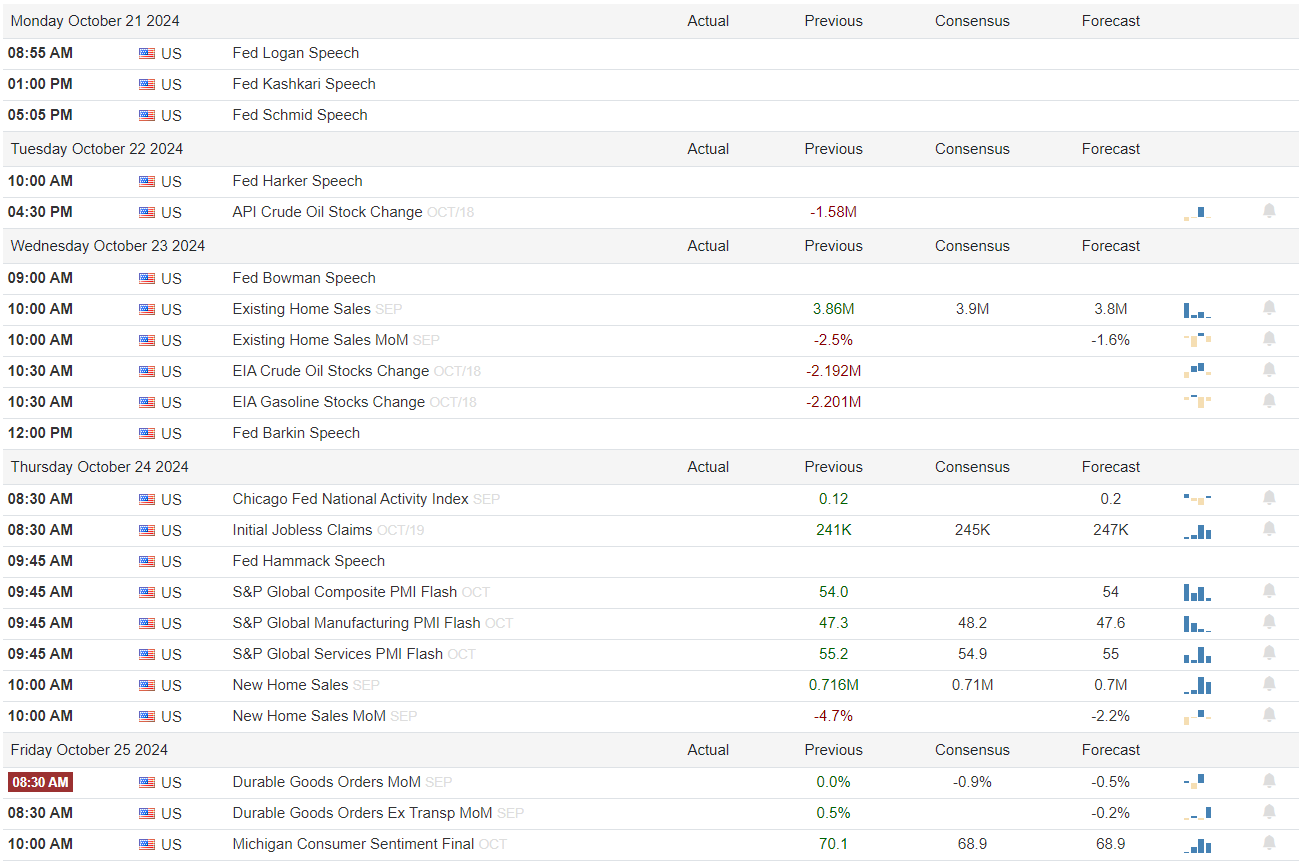

Events On Deck This Week

Here are key events happening this week that have the potential to cause outsized moves in the market or heightened short-term volatility.

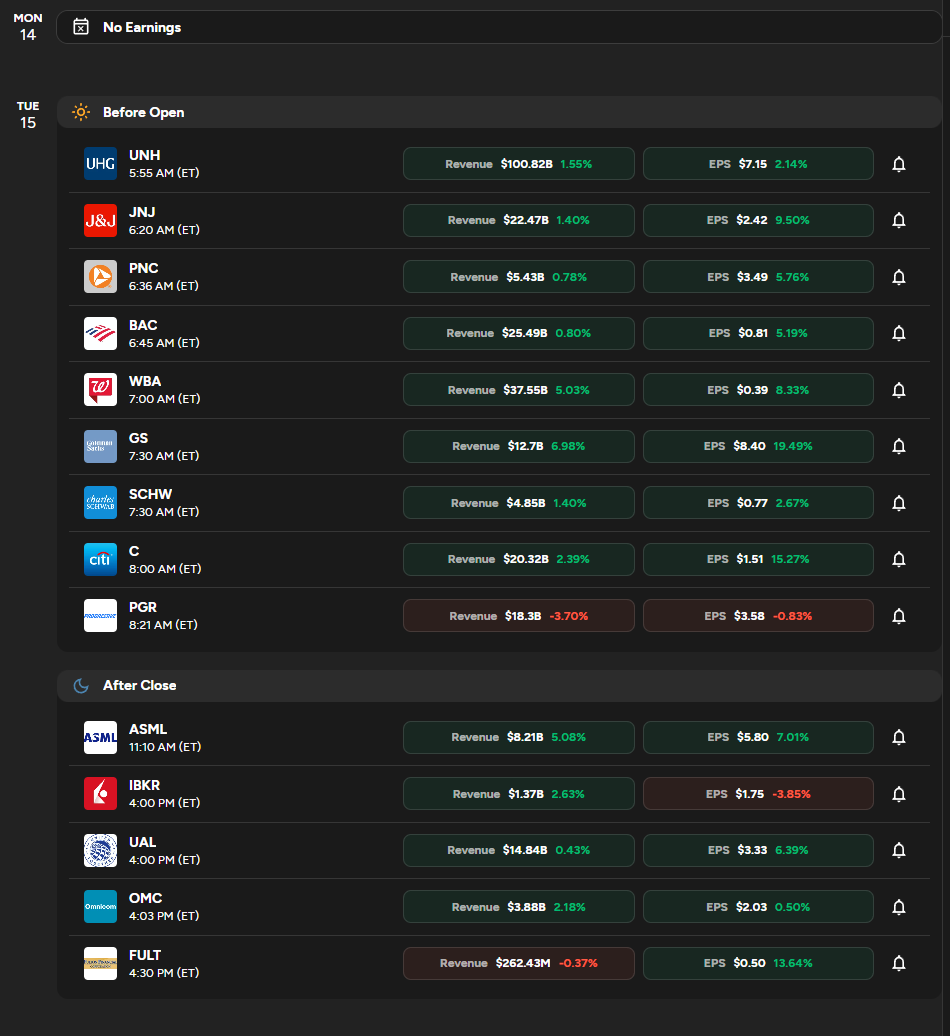

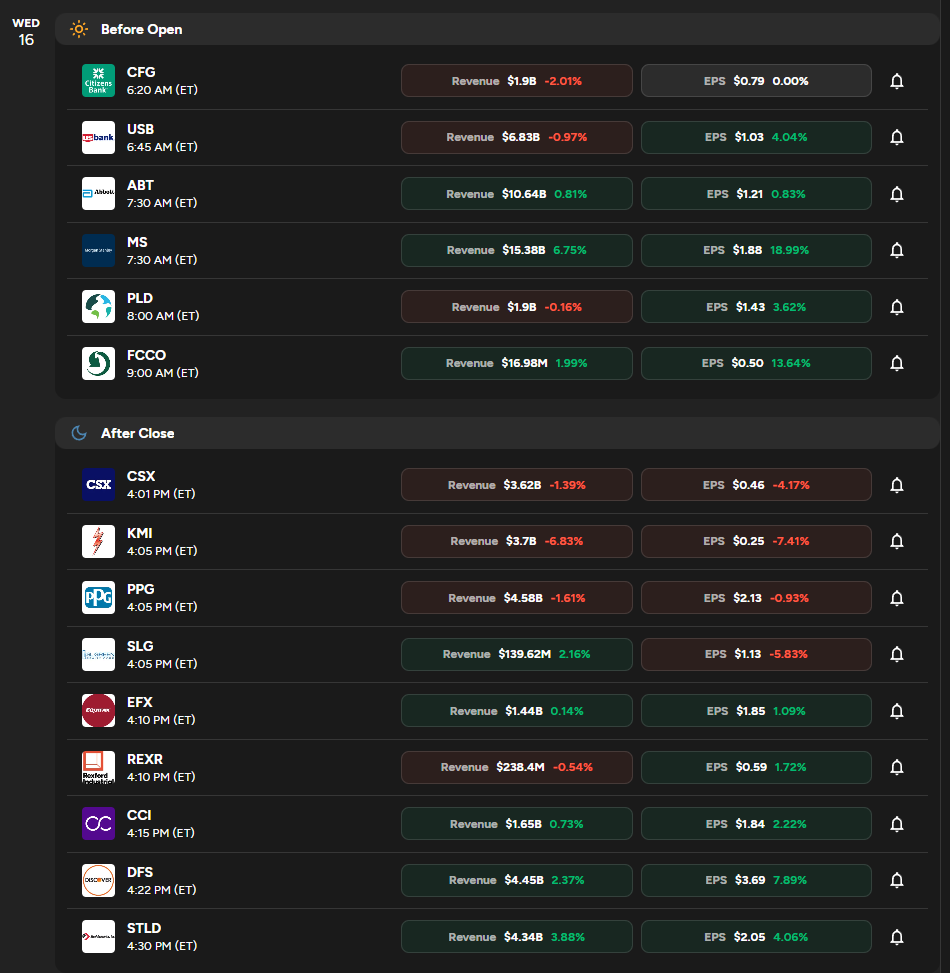

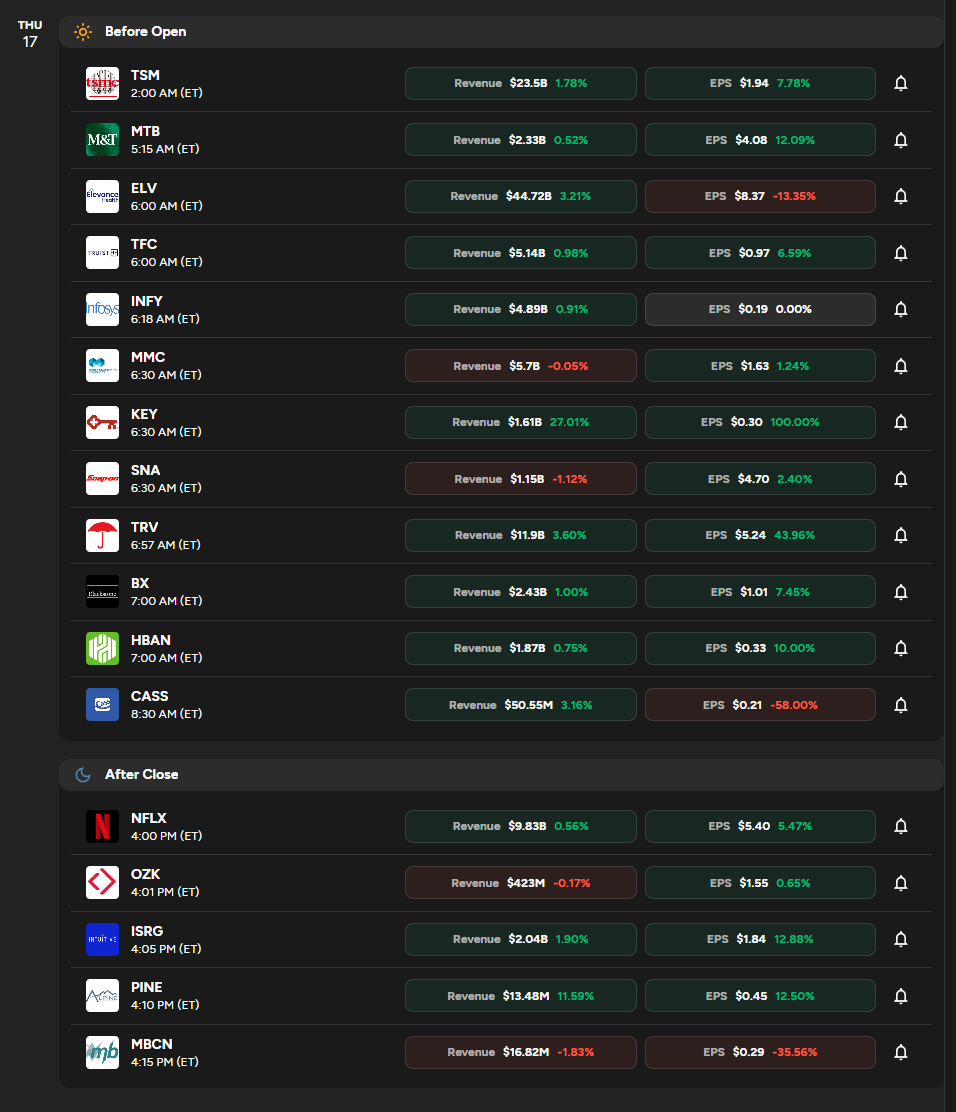

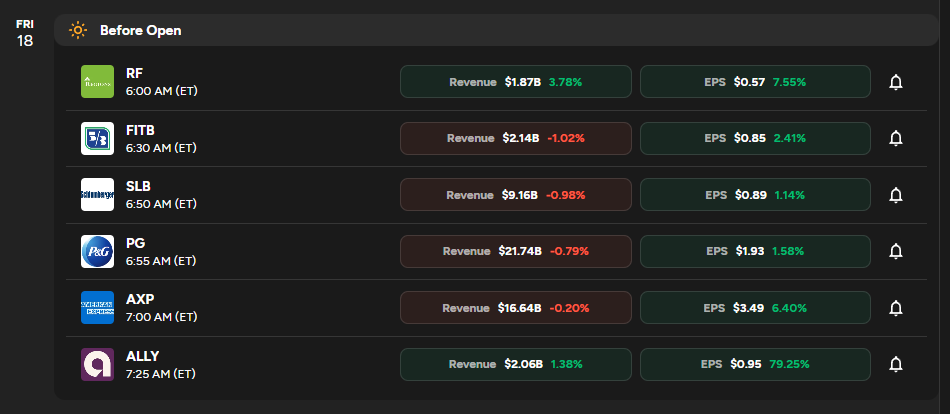

Econ Events By Day of Week

Anticipated Earnings By Day of Week

A Final Word

Thank you for reading this week's edition of Market Momentum. If you found value in this content, please consider sharing it with a friend or colleague, in a Discord or a Tweet. This small favor helps keep this stack free for you! Please check out VolumeLeaders.com for your own free trial of the platform that brings you the data powering this stack. Wishing you all a green week ahead filled with many bags ❤️💰.