Market Momentum: Your Weekly Financial Forecast & Market Prep

Issue 17 / What to expect Oct 14, 2024 thru Oct 18, 2024

The past week in the U.S. financial markets can be characterized by significant developments in both the labor market and the equity markets, highlighting the interplay between macroeconomic conditions and investor sentiment. One of the focal points for investors continues to be the unemployment rate, which ticked lower to 4.1% in September, though it remains well above its April 2023 cycle low of 3.4%. While a gradual increase in unemployment might initially spark concerns about a weakening labor market, deeper analysis suggests a different narrative. The rise in unemployment has been driven by an increase in the labor force as more people reenter the job market, rather than a decline in employment levels. This influx of workers has created a temporary imbalance, with job growth lagging behind labor force growth. Despite this, the U.S. economy added 254,000 jobs in September, while initial jobless claims and layoffs remained at historically low levels, signaling continued stability in the labor market.

Wage growth has also played a critical role in this story, increasing by 4.0% year-over-year in September and marking the 17th consecutive month in which wage gains have outpaced inflation. This indicates sustained demand for labor, with approximately 8 million job openings across the U.S. Even with a higher unemployment rate than a year ago, these real wage gains provide a solid foundation for consumer spending, which is essential for maintaining economic momentum. The outlook for the U.S. economy remains cautiously optimistic as long as layoffs remain subdued and wage growth continues to support consumer activity.

At the same time, equity markets continue to navigate through a bull market that is now two years old. Since the market bottom in October 2022, U.S. large-cap stocks have rallied approximately 60%, a performance that is in line with historical averages for past bull markets. This has provided a strong tailwind for investor sentiment, even as growth appears to be moderating. Historically, most bull markets last for at least three years, and while the pace of gains may slow, the current environment suggests there is still room for upward momentum. Notably, geopolitical factors and the U.S. election cycle could introduce short-term volatility, but the broader market outlook remains supported by strong fundamentals.

Inflation data, which has been a key driver of both market sentiment and Federal Reserve policy, showed a slight uptick in September. This minor increase is not expected to derail the Fed's current course, with quarter-point rate cuts anticipated at each upcoming meeting until policy rates settle around 3% to 3.5%. Importantly, inflation has come down significantly from its June 2022 peak of 9.1%, with headline inflation currently at 2.4% and core inflation at 3.3%. This progress has enabled the Fed to begin easing monetary policy, which has been a positive catalyst for equity markets over the past year. The focus for the Fed has shifted from inflation control to supporting the labor market, a transition that should help extend the economic expansion.

Corporate earnings remain another critical factor in market performance. The third-quarter earnings season began last week, with several major U.S. banks reporting better-than-expected results, providing a positive start to the season. Earnings growth is forecasted to rise by 4.2% for the quarter, marking the fifth consecutive quarter of earnings increases. A key development to watch will be whether the earnings growth of the top-performing mega-cap tech stocks begins to moderate while other sectors of the market pick up the slack. A broader leadership rotation in earnings growth, with cyclicals and value-oriented stocks contributing more significantly, could provide the next leg of market support.

The resilience of the U.S. economy, driven by strong labor market dynamics and a robust earnings environment, has defied widespread expectations of a recession that were prevalent over the past two years. Despite facing headwinds such as high inflation and rising interest rates, the consumer remains a driving force in the economy, buoyed by healthy balance sheets and rising wages. This strength is evident in U.S. GDP growth, which has averaged around 3% over the past two years, and is projected to come in at 3.2% for the third quarter, according to estimates from the Atlanta Fed. However, growth is expected to slow in the coming quarters, likely returning to a more sustainable long-term trend of around 2%. While economic expansion may decelerate, the foundation for continued corporate profitability remains intact, and this should help sustain the bull market in the near to medium term.

Looking forward, there are several risks on the horizon that investors should be mindful of. Elevated valuations across U.S. equities limit the potential for further multiple expansion, meaning that earnings growth will have to do the heavy lifting if the market rally is to continue. Additionally, geopolitical tensions, particularly in the Middle East, and the upcoming U.S. election cycle could introduce bouts of volatility. That said, these risks are balanced by an environment of easing monetary policy and resilient corporate earnings, which should provide a cushion against any significant market pullback.

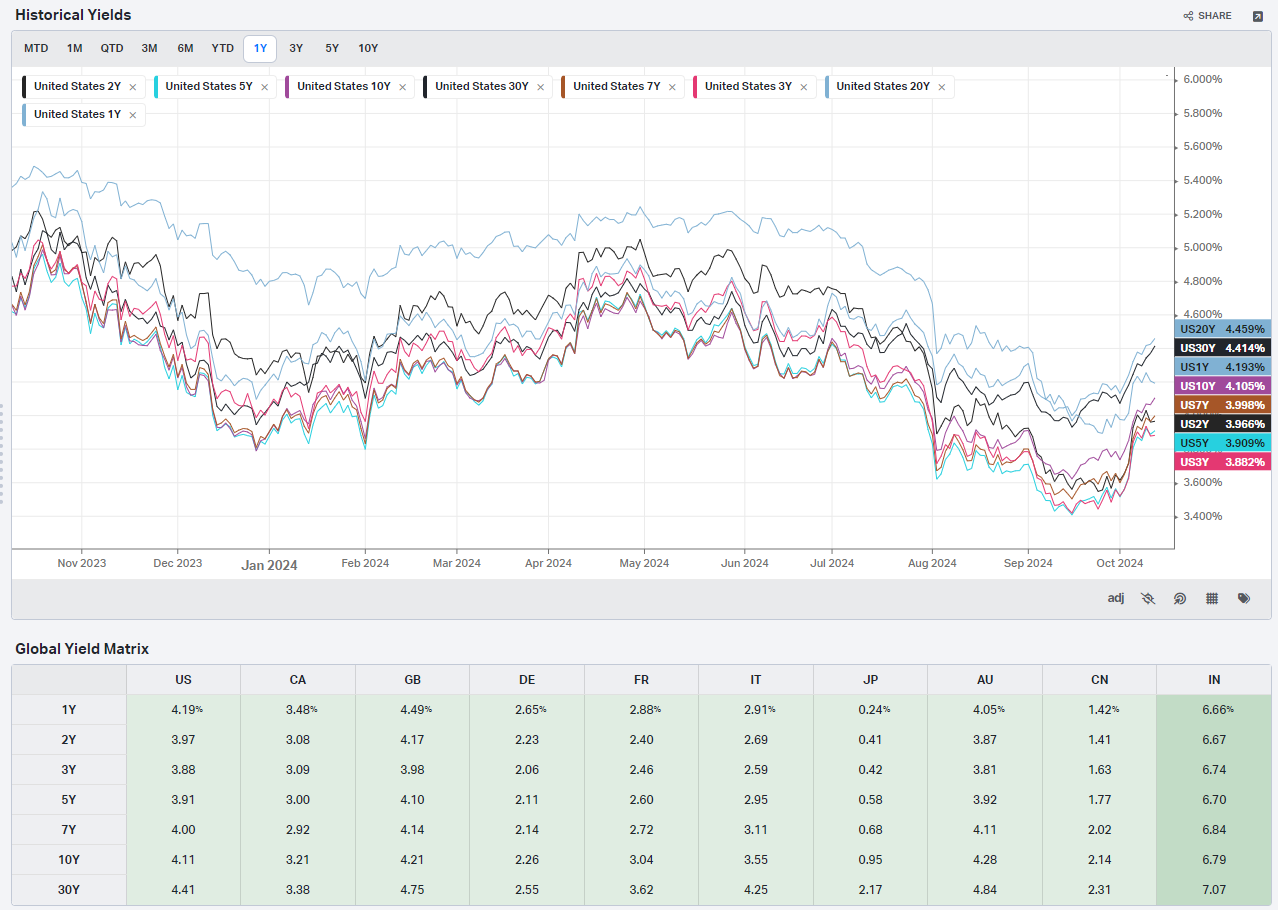

Interest rates have been another area of focus for market participants. The yield on the 10-year U.S. Treasury note climbed for the fourth consecutive week, closing at 4.08% on Friday, up from 3.98% the previous week. Rising yields reflect the market's reassessment of the pace of future rate cuts, particularly in light of higher-than-expected inflation readings. Despite this, the Fed remains committed to gradually lowering rates, which should provide ongoing support for equities as borrowing costs decline.

In terms of market breadth, the current rally appears to be healthy and widespread, with roughly 75% of S&P 500 components trading above their 200-day moving averages. Financials, industrials, and real estate have all seen solid gains, driven in part by rising yields and positive earnings surprises from the banking sector. Last week, shares of JPMorgan Chase and Wells Fargo rose sharply following their third-quarter earnings reports, which exceeded analyst expectations. This highlights the strength of the U.S. financial sector, even in a rising rate environment.

The U.S. consumer remains a key pillar of economic strength, supported by rising wages and excess savings accumulated during the pandemic. Retail sales data, which is expected to be released later this week, will provide further insight into the health of consumer demand. Recent reports have been positive, with sales rising modestly in August, and any continuation of this trend would bode well for fourth-quarter economic activity. However, consumer sentiment dipped slightly in October, according to the University of Michigan's Consumer Sentiment Index, which could be a signal that inflationary pressures are weighing on household confidence.

In summary, the U.S. financial markets have continued to build on the momentum of the past two years, with equity markets extending their recovery and the labor market remaining resilient despite some signs of cooling. Inflation has moderated significantly, allowing the Federal Reserve to begin easing monetary policy, which has provided a tailwind for stocks. Corporate earnings have continued to grow, and the market's leadership has started to broaden beyond the tech sector, signaling a healthier and more sustainable rally. While risks such as geopolitical tensions and elevated valuations remain, the overall outlook for the U.S. economy and financial markets remains positive, with strong fundamentals supporting continued growth into 2025.

over the next year.")

Last Week At A Glance

Week-Over-Week Snapshots

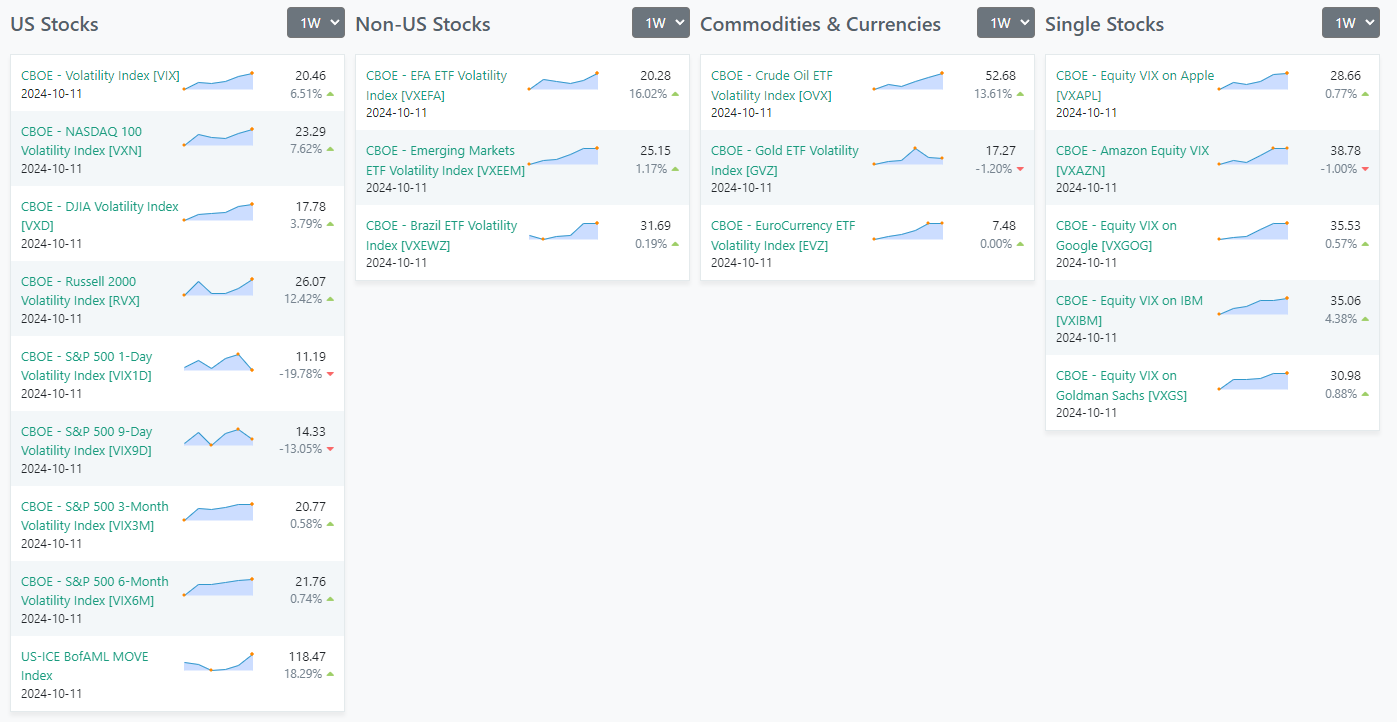

Volatility

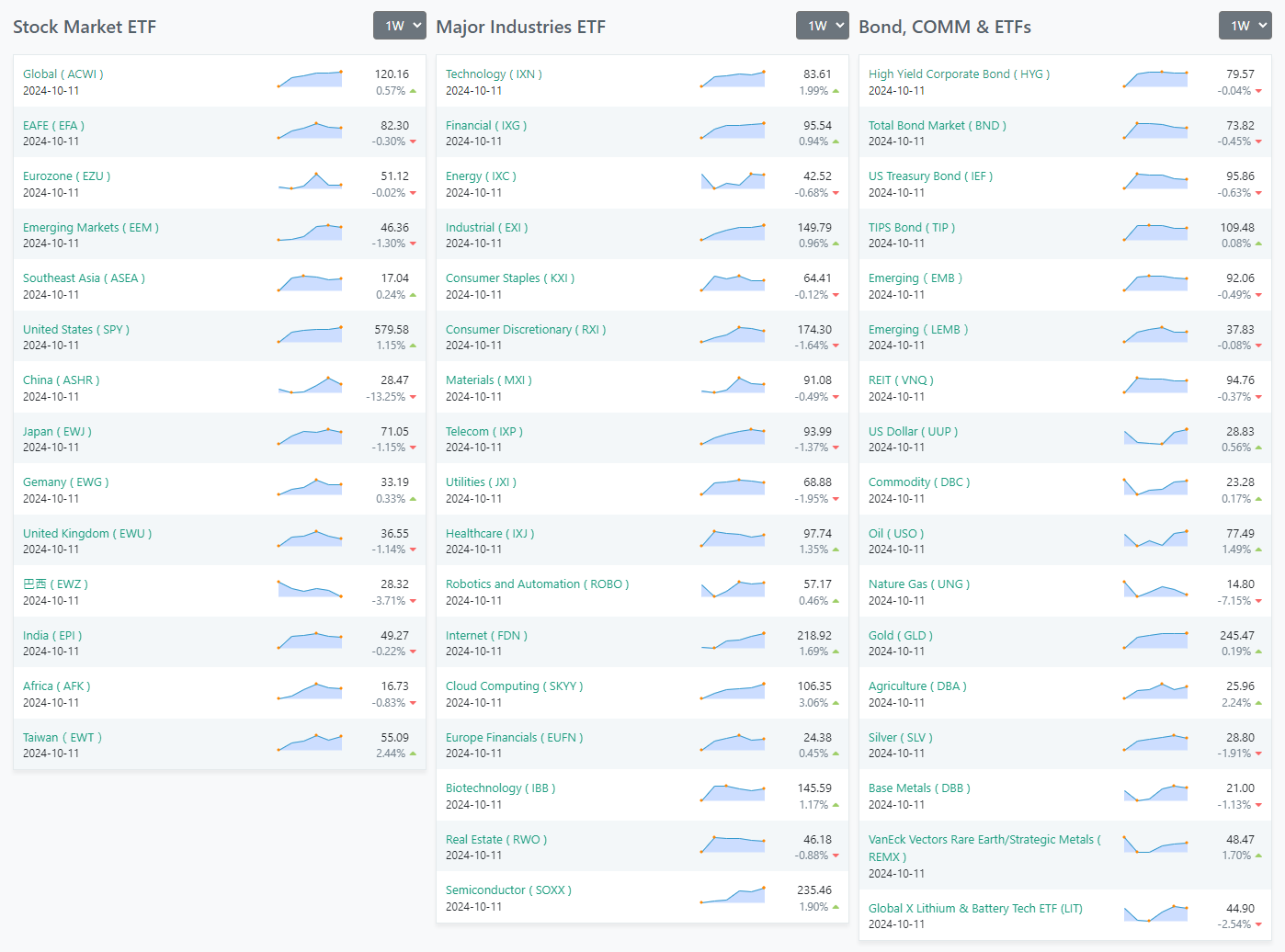

ETFs

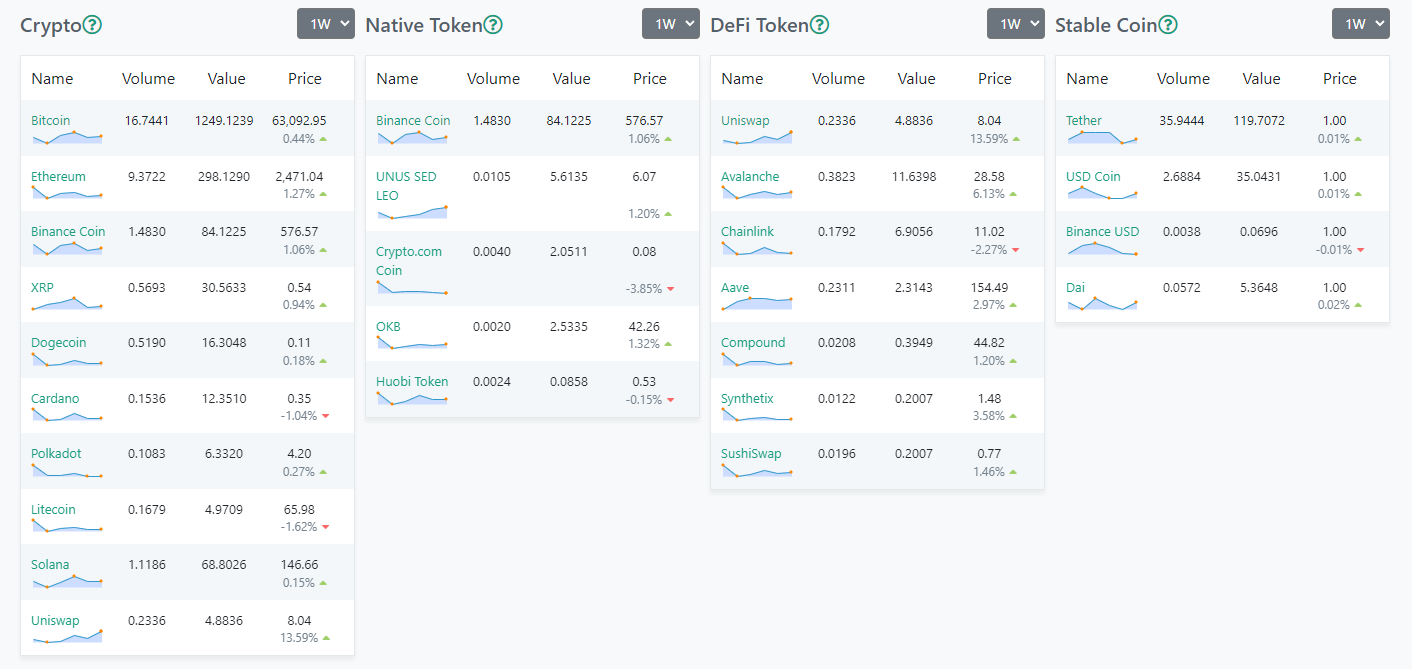

Crypto

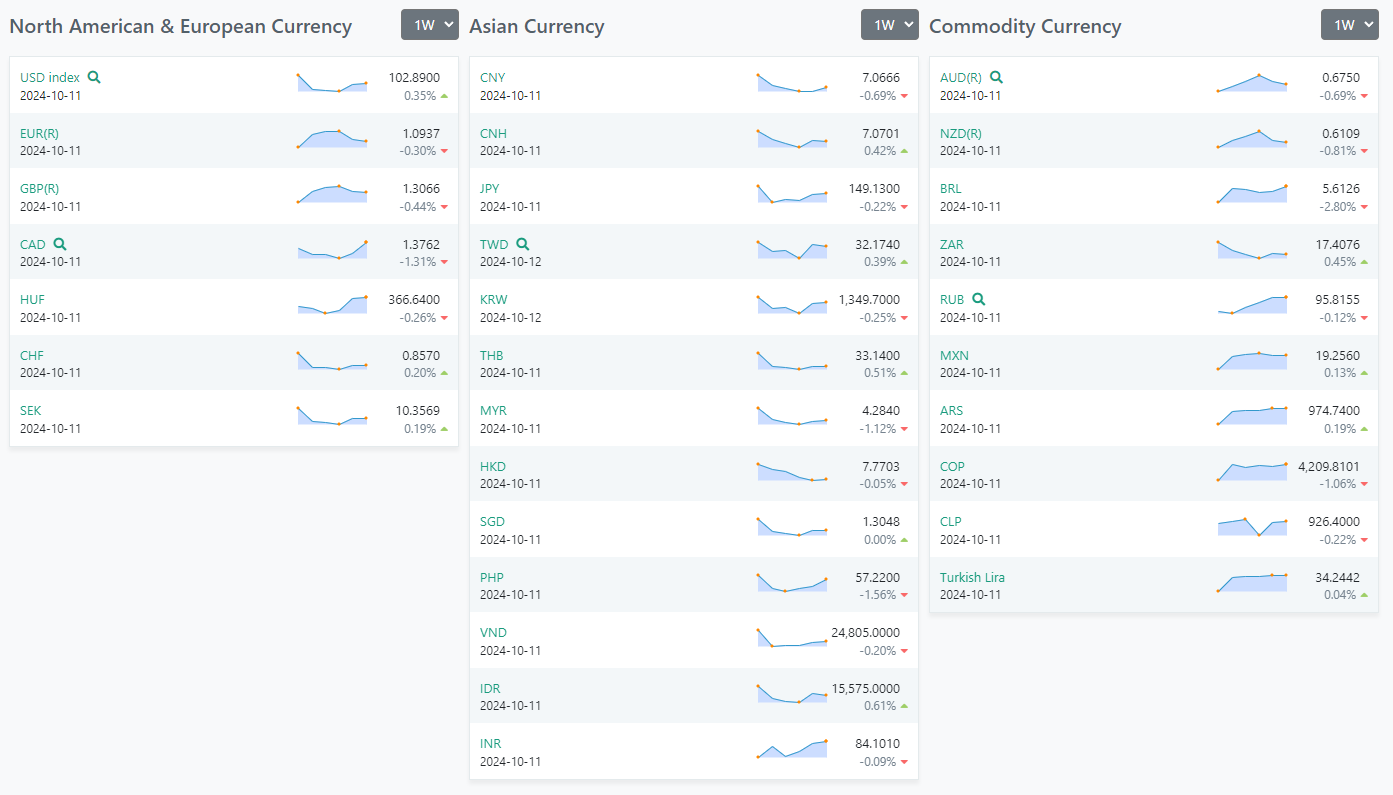

Forex

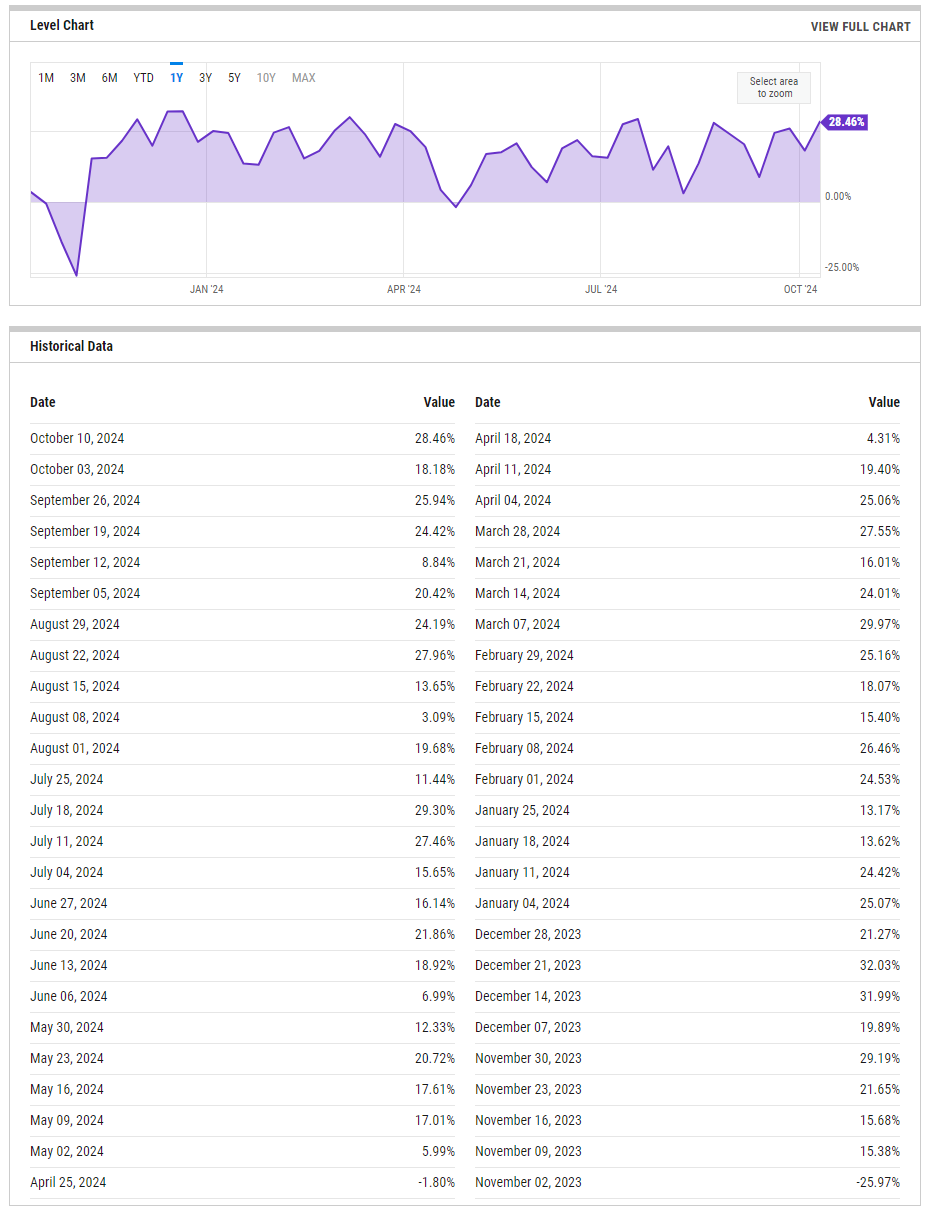

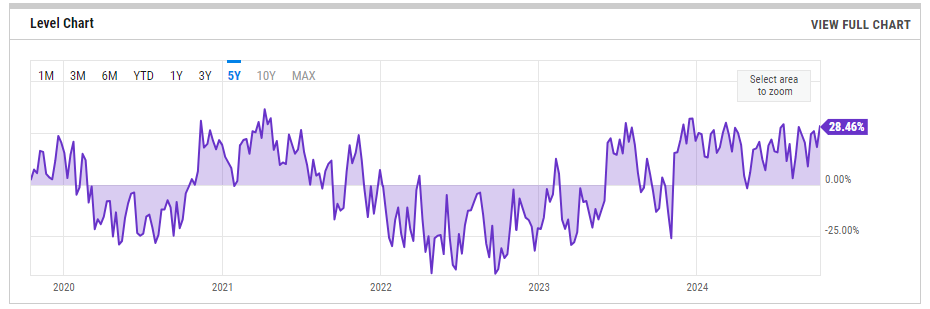

US Investor Sentiment

%Bull-Bear Spread

The %Bull-Bear Spread chart is a sentiment indicator that shows the difference between the percentage of bullish and bearish investors, often derived from surveys or sentiment data, such as the AAII (American Association of Individual Investors) sentiment survey. This spread tells investors about the prevailing mood in the market and can provide insights into market extremes and potential turning points.

Bullish or Bearish Sentiment:

When the spread is positive, it means more investors are bullish than bearish, indicating optimism about the market’s direction.

A negative spread indicates more bearish sentiment, meaning more investors expect the market to decline.

Contrarian Indicator:

The %Bull-Bear Spread is often used as a contrarian indicator. For example, extremely high levels of bullish sentiment might suggest that the market is overly optimistic and could be due for a correction.

Similarly, when bearish sentiment is extremely high, it might indicate that the market is overly pessimistic, and a rally could be on the horizon.

Market Extremes and Reversals:

Historically, extreme values of the spread (both positive and negative) can signal turning points in the market. A very high positive spread can signal market exuberance, while a very low or negative spread may indicate fear or capitulation.

1-Year View

5-Year View

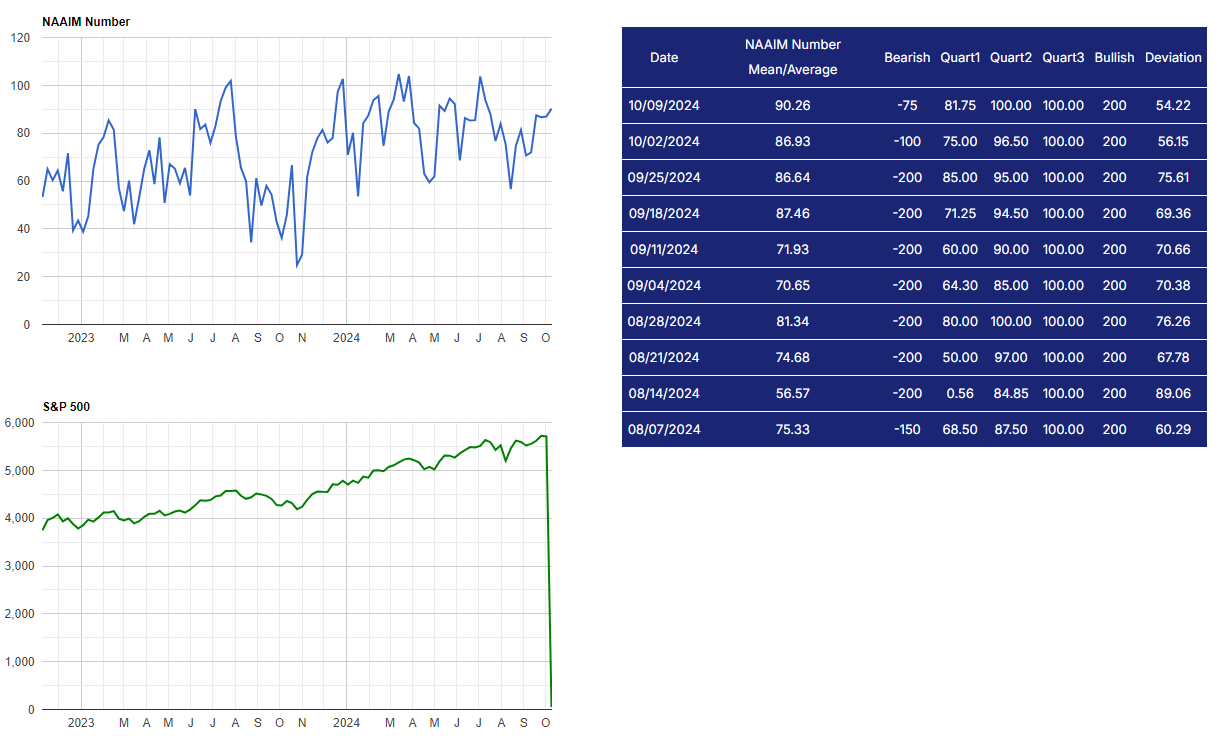

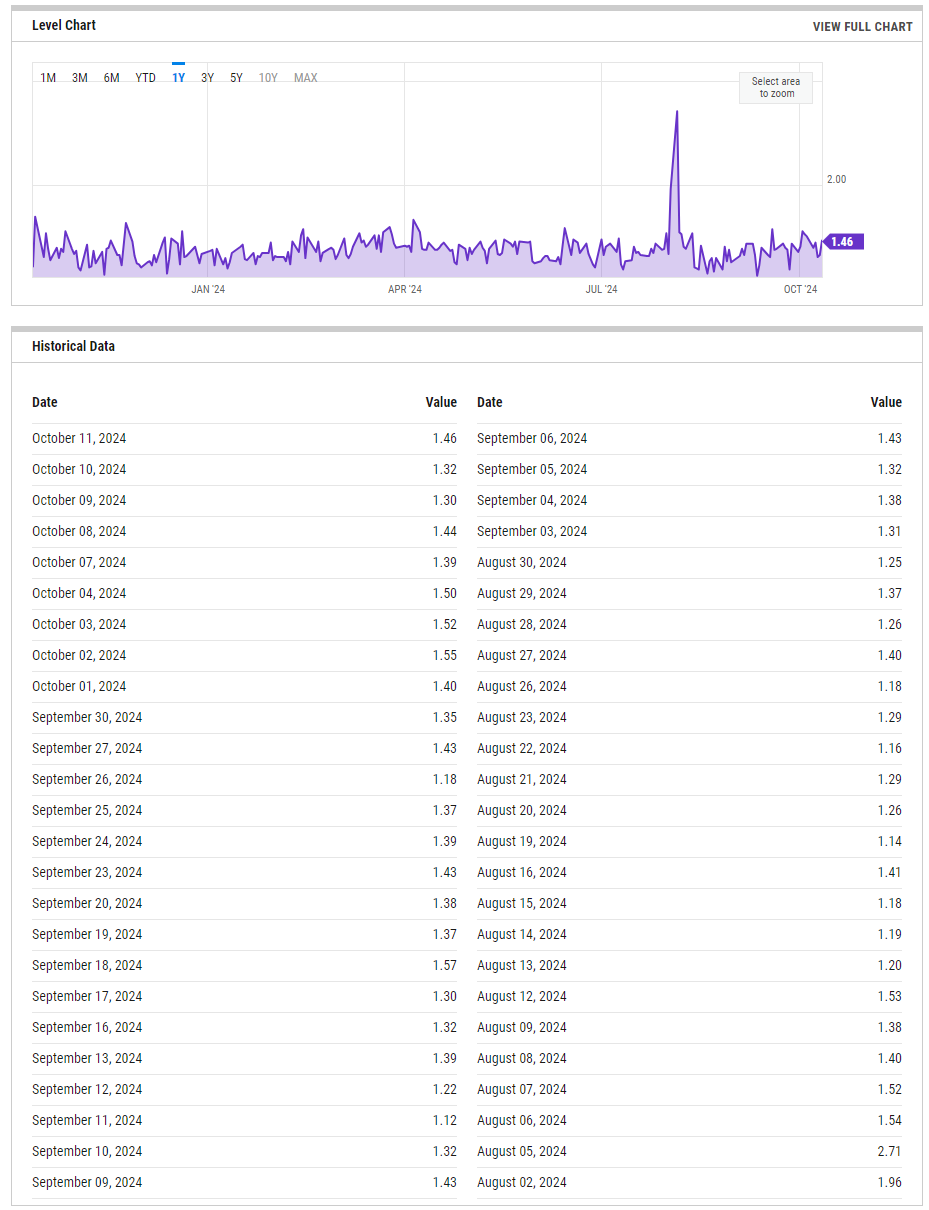

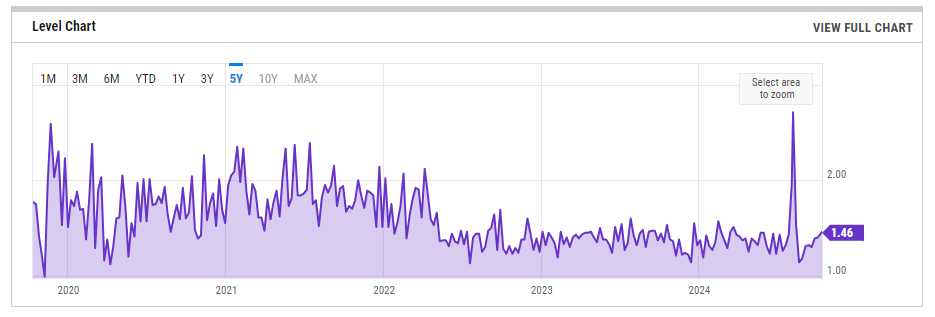

NAAIM Exposure Index

The NAAIM Exposure Index (National Association of Active Investment Managers Exposure Index) measures the average exposure to U.S. equity markets as reported by its member firms. These are typically active money managers who provide their equity exposure levels weekly. The index offers insight into how much these managers are investing in equities at any given time, ranging from being fully short (-100%) to leveraged long (up to +200%).

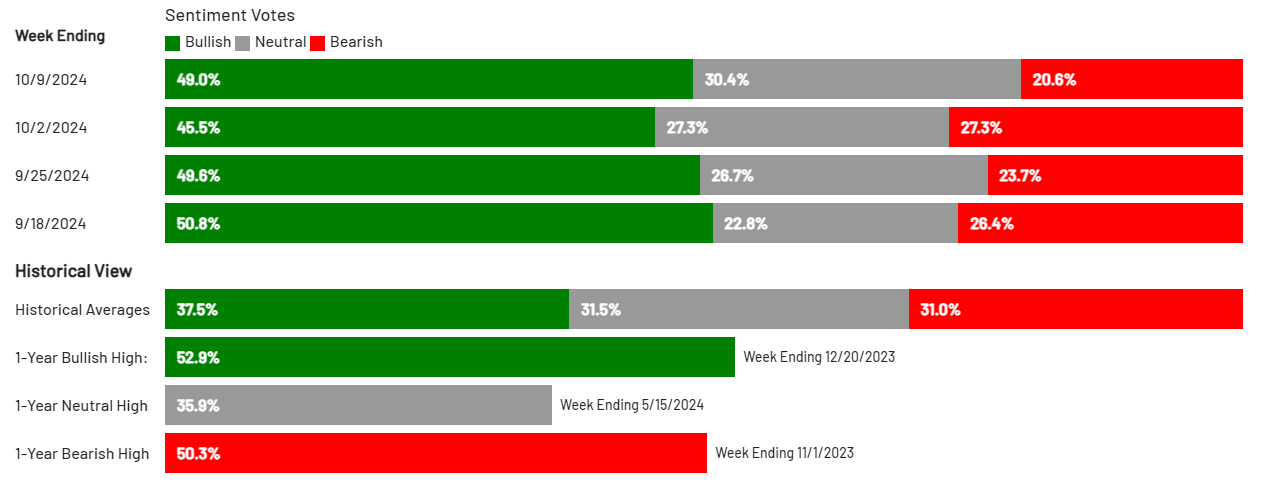

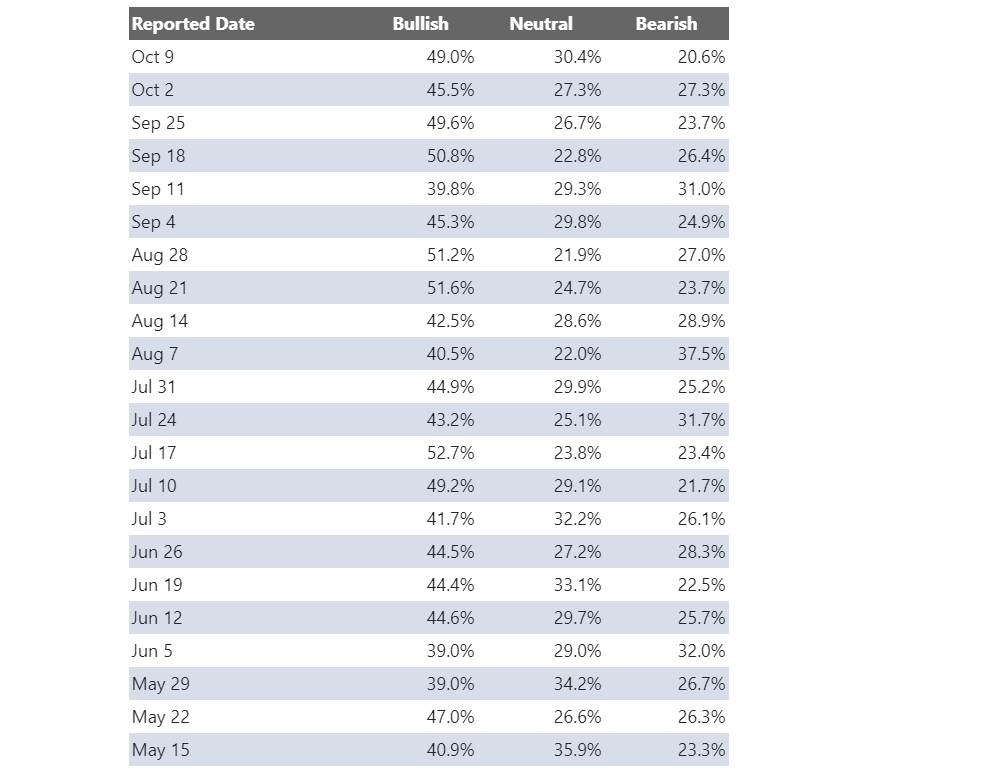

AAII Investor Sentiment Survey

The AAII Investor Sentiment Survey is a weekly survey conducted by the American Association of Individual Investors (AAII) to gauge the mood of individual investors regarding the direction of the stock market over the next six months. It provides insights into whether investors are feeling bullish (expecting the market to rise), bearish (expecting the market to fall), or neutral (expecting the market to stay about the same).

Key Points:

Bullish Sentiment: Reflects the percentage of investors who believe the stock market will rise in the next six months.

Bearish Sentiment: Represents those who expect a decline.

Neutral Sentiment: Reflects investors who anticipate little to no market movement.

The survey is widely followed as a contrarian indicator, meaning that extreme levels of bullishness or bearishness can sometimes signal market turning points. For example, when a large number of investors are overly optimistic (high bullish sentiment), it could suggest a market top, while excessive pessimism (high bearish sentiment) may indicate a market bottom is near.

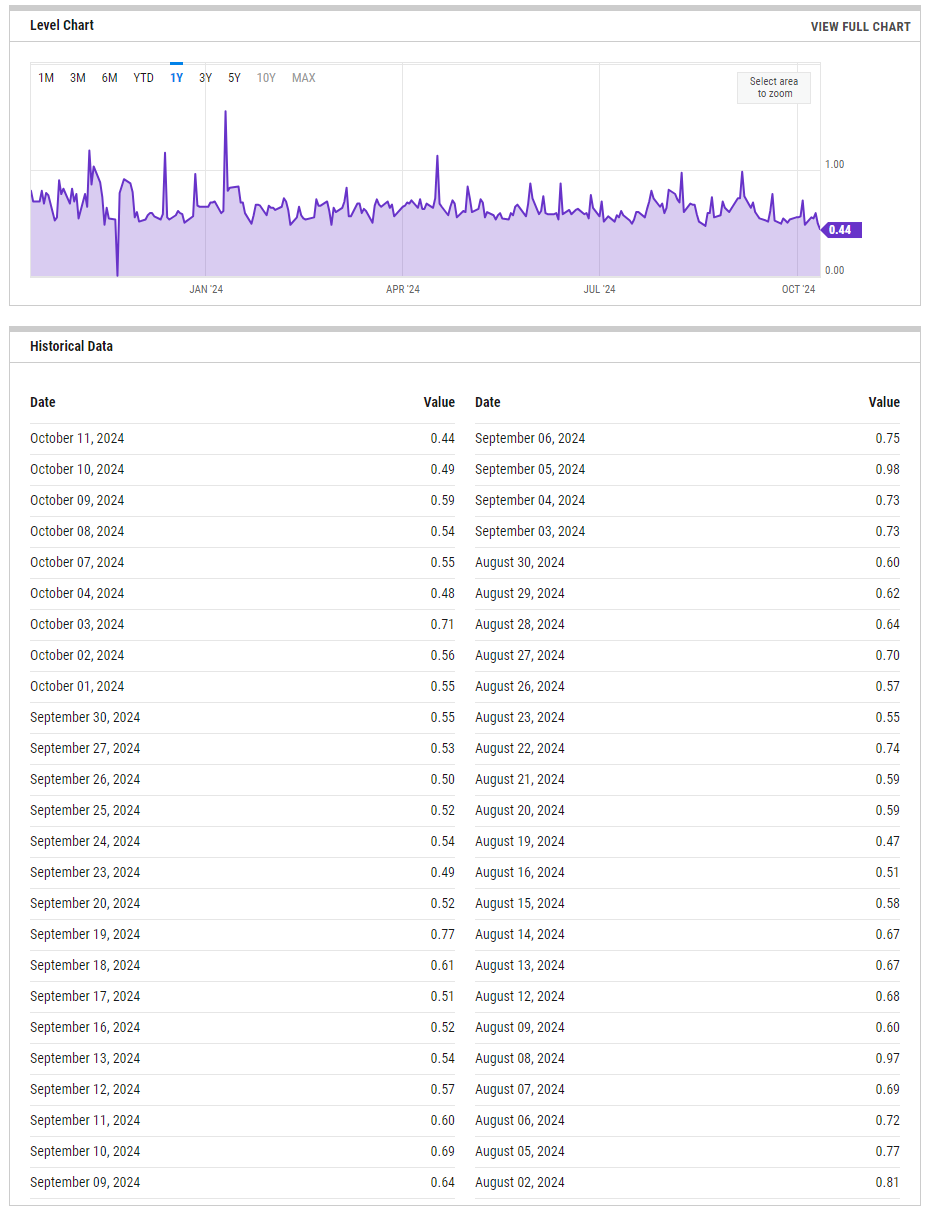

SPX Put/Call Ratio

The SPX Put/Call Ratio is an indicator that is used to gauge market sentiment. This is calculated as the ratio between trading S&P 500 put options and S&P call options. A high put/call ratio can indicate fear in the markets, while a low ratio indicates confidence. For example, in 2015, the Put-Call ratio was as high as 3.77 because of market fears stemming from various global economic issues like a GDP growth slowdown in China and a Greek debt default.

1-Year View

5-Year View

CBOE Equity Put/Call Ratio

1-Year View

5-Year View

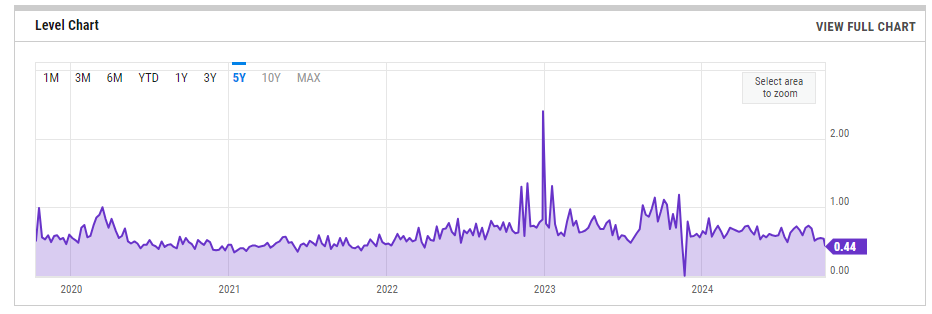

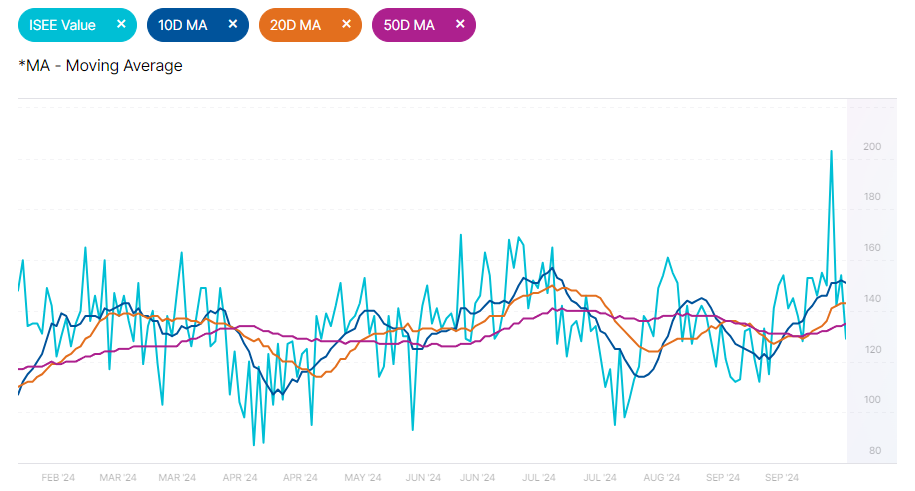

ISEE Sentiment Index

The ISEE (International Securities Exchange Sentiment) Index is a measure of investor sentiment derived from options trading. Unlike traditional put/call ratios, the ISEE Index focuses only on opening long customer transactions and is adjusted to remove market-maker and firm trades, providing a purer sentiment reading.

The ISEE Index typically ranges from 0 to 200, with readings above 100 indicating more call options being bought relative to put options, suggesting bullish sentiment. Conversely, readings below 100 suggest bearish sentiment, with more puts being purchased relative to calls.

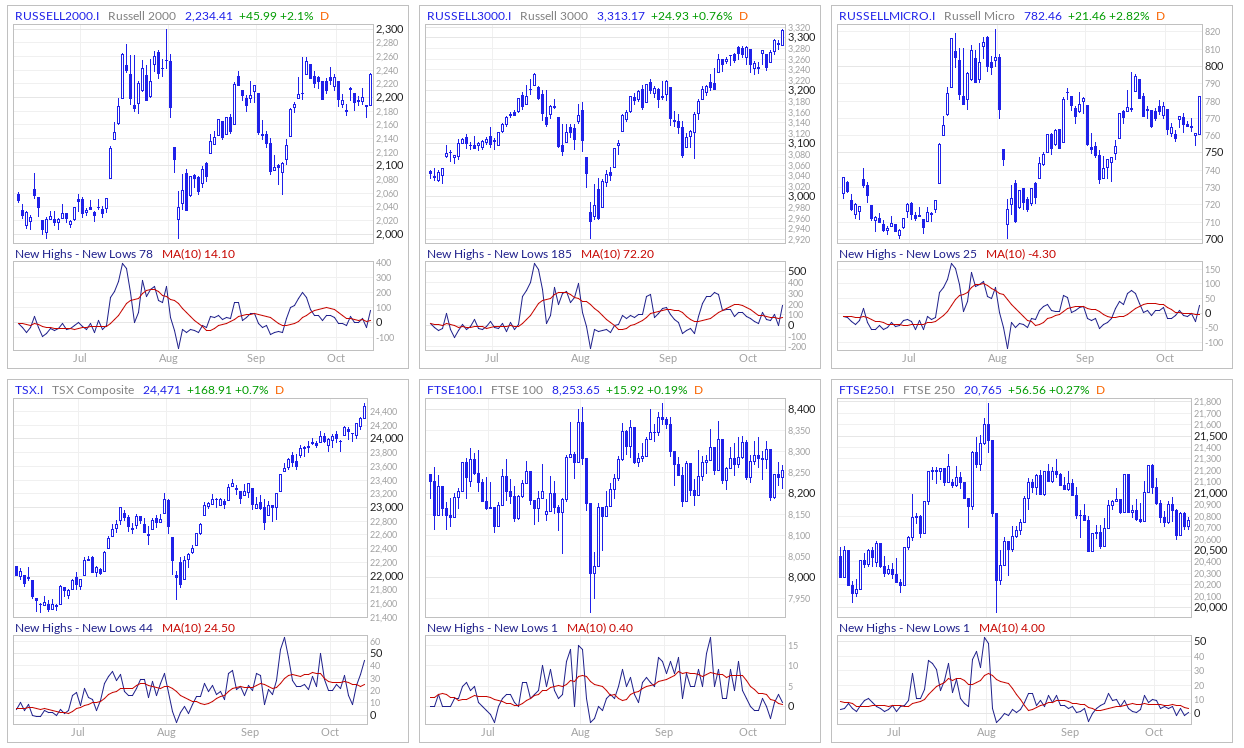

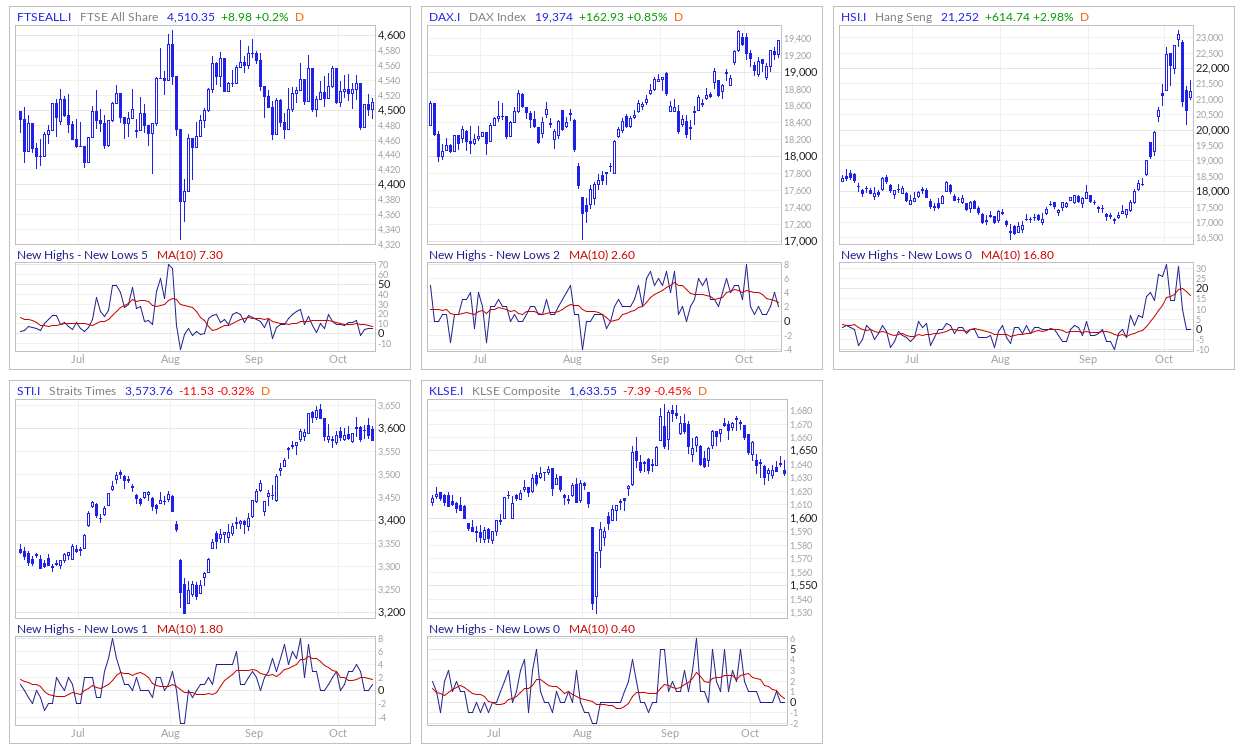

New Highs - New Lows

The New Highs - New Lows indicator (NH-NL) displays the daily difference between the number of stocks reaching new 52-week highs and the number of stocks reaching new 52-week lows. The NH-NL indicator generally reaches its extreme lows slightly before a major market bottom. As the market then turns up from the major bottom, the indicator jumps up rapidly. During this period, many new stocks are making new highs because it's easy to make a new high when prices have been depressed for a long time. The NH-NL indicator oscillates around zero. If the indicator is positive, the bulls are in control. If it is negative, the bears are in control. As the cycle matures, a divergence often occurs as fewer and fewer stocks are making new highs (the indicator falls), yet the market indices continue to reach new highs. This is a classic bearish divergence that indicates that the current upward trend is weak and may reverse.

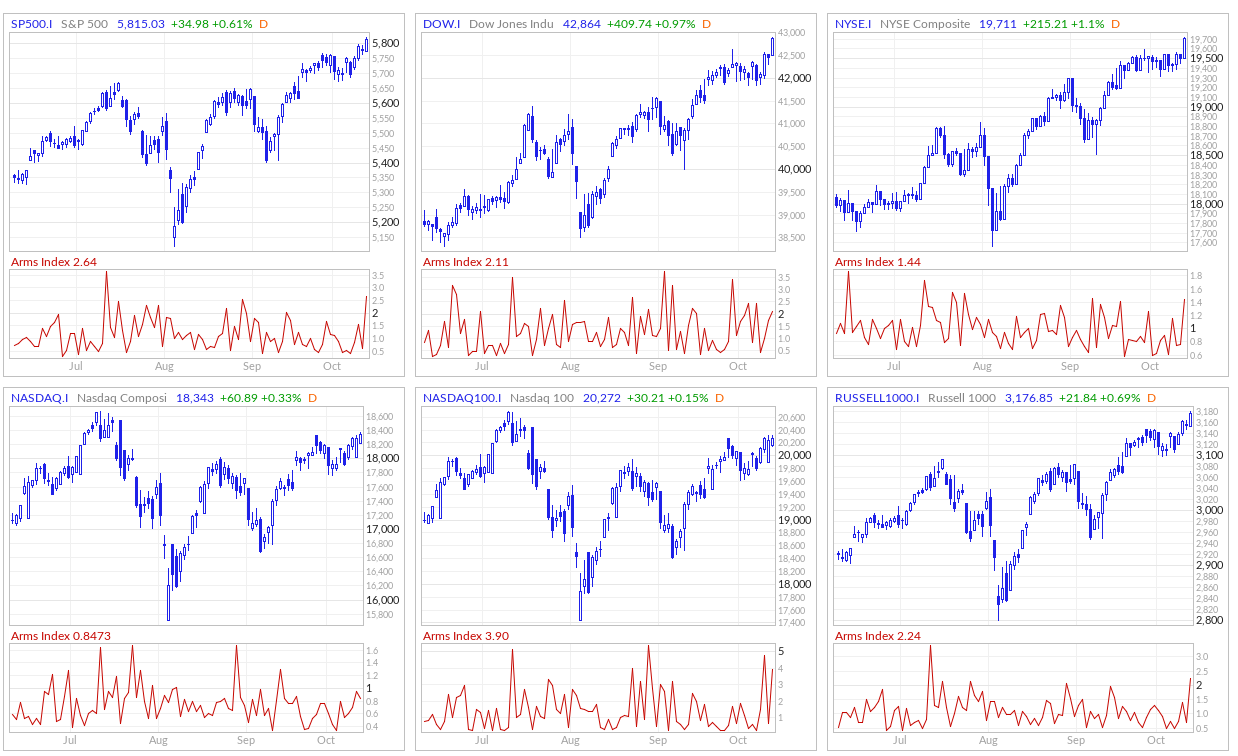

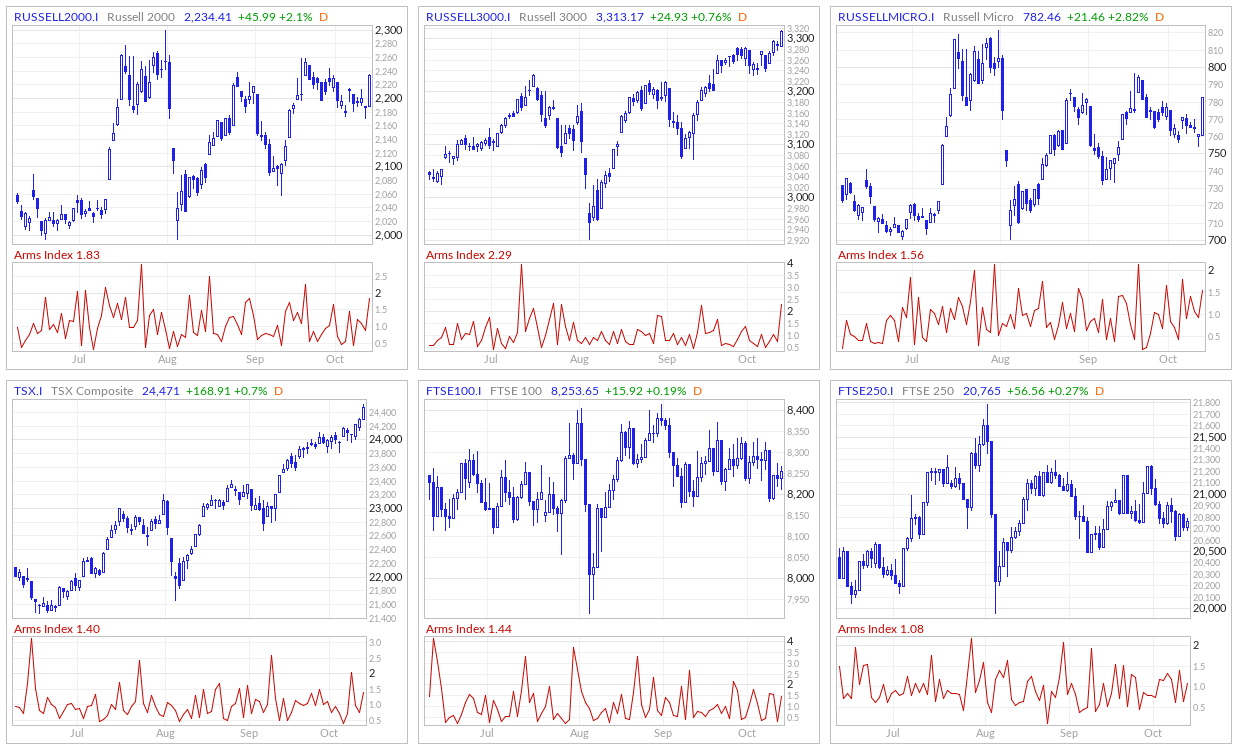

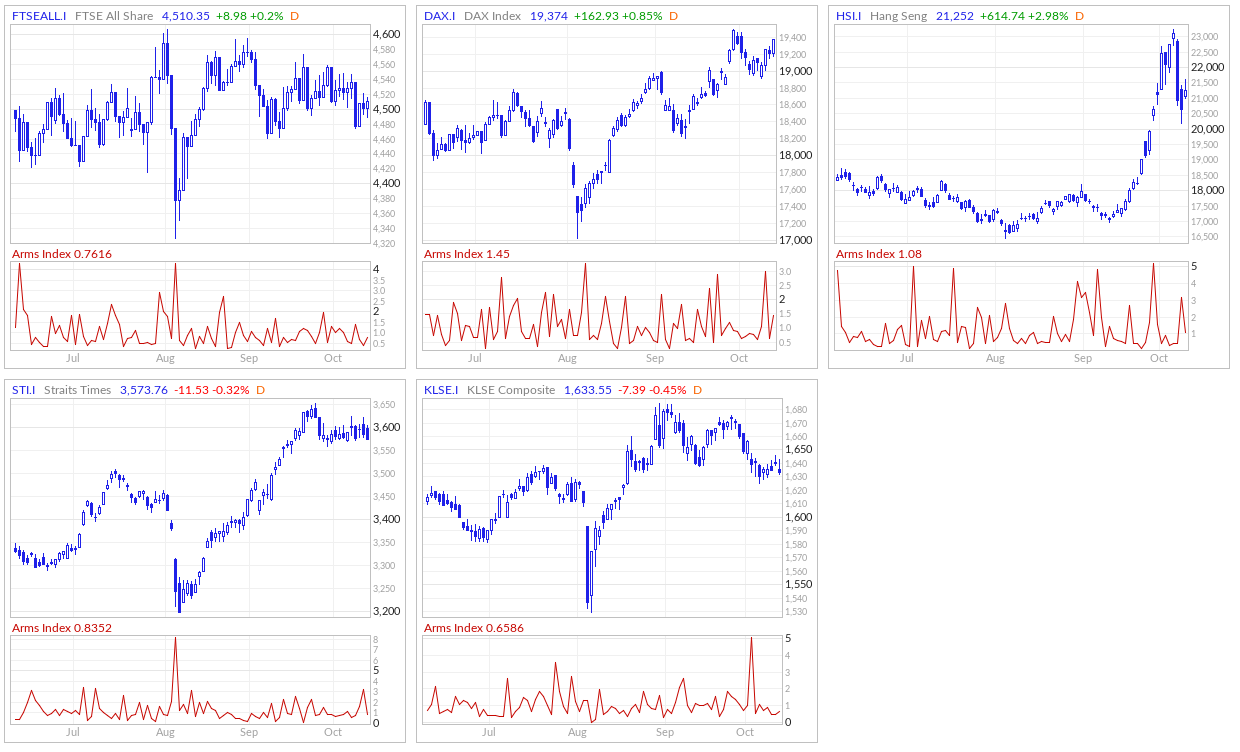

ARMS Index

The Arms Index, also known as the TRIN (Short-Term TRading INdex), was developed by Richard Arms in the 1960s. It is calculated by dividing the ratio of advancing stocks to declining stocks by the ratio of advancing volume to declining volume. Interpreting the Arms Index involves looking at its value in relation to certain thresholds. A value below "1" is considered bullish, indicating that advancing stocks and volume dominate the market. Conversely, a value above "1" is considered bearish, suggesting that declining stocks and volume are more prevalent. Extremely low values (below 0.5) or high values (above 2) are often seen as potential reversal signals.

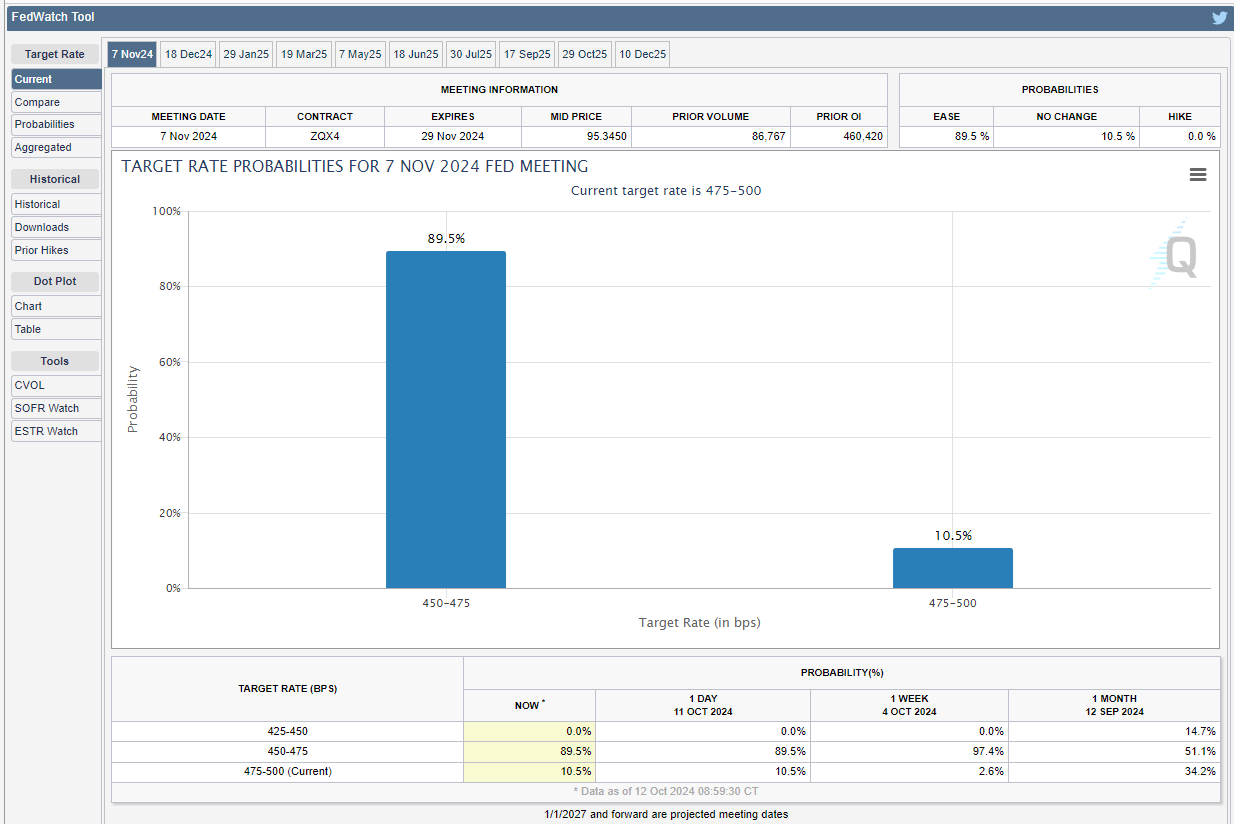

CME Fedwatch

What is the likelihood that the Fed will change the Federal target rate at upcoming FOMC meetings, according to interest rate traders? Use CME FedWatch to track the probabilities of changes to the Fed rate, as implied by 30-Day Fed Funds futures prices.

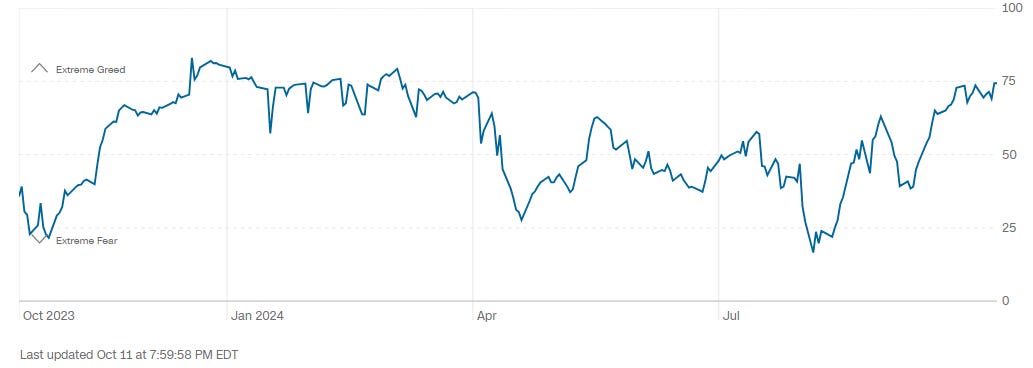

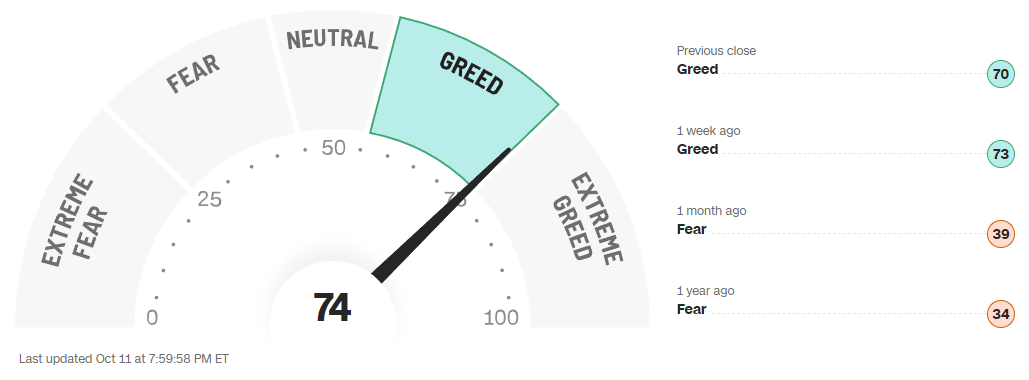

CNN 7 Fear & Greed Constituent Data Points + Composite Index

Final Composite Fear & Greed Index Reading

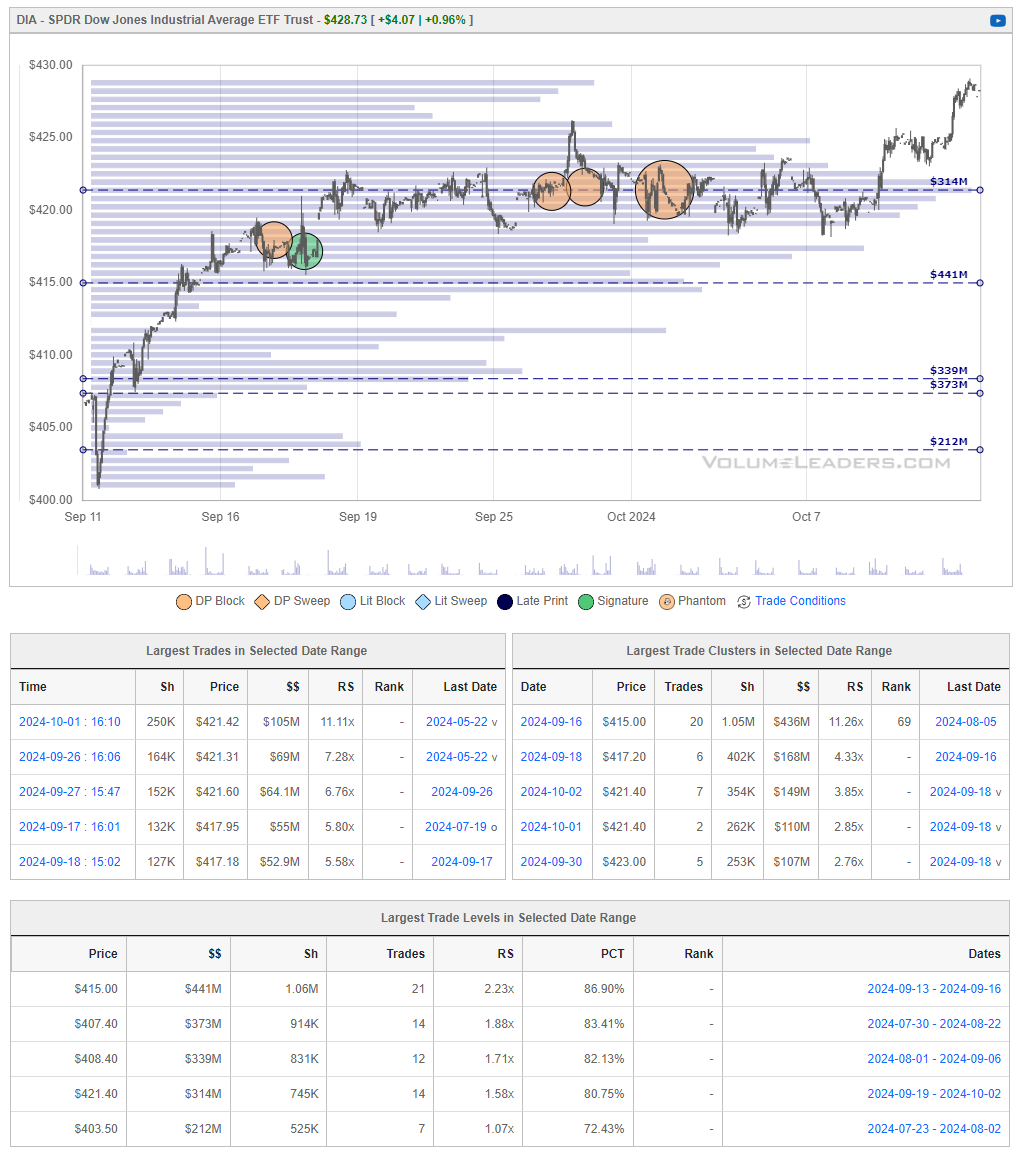

Institutional S/R Levels for Major Indices

When you’re a large institutional player, your primary goal is to find liquidity - places to do a ton of business with the least amount of slippage possible. VolumeLeaders.com automatically identifies and visually plots the exact spots where institutions are doing business and where they are likely to return for more. It’s one of the primary reasons “support” and “resistance” concepts work and truly one of the reasons “price has memory”.

Levels from the VolumeLeaders.com platform can help you formulate trades theses about:

Where to add or take profit

Where to de-risk or hedge

What strikes to target for options

Where to expect support or resistance

And this is just a small sample; there are countless ways to leverage this information into trades that express your views on the market. The platform covers thousands of tickers on multiple timeframes to accommodate all types of traders. Observe for yourself how accurate the levels are by marking-up your charts with the information in the “Trade Levels” boxes I’m giving for free below and play-along in real-time this week. These charts cover recent sessions, but subs will get new levels as they develop, see the latest trades and institutional positioning, have access to levels from other time frames and so much more. When you watch these levels this week, I’m confident you’ll see how clear, intuitive and actionable this information is for yourself.

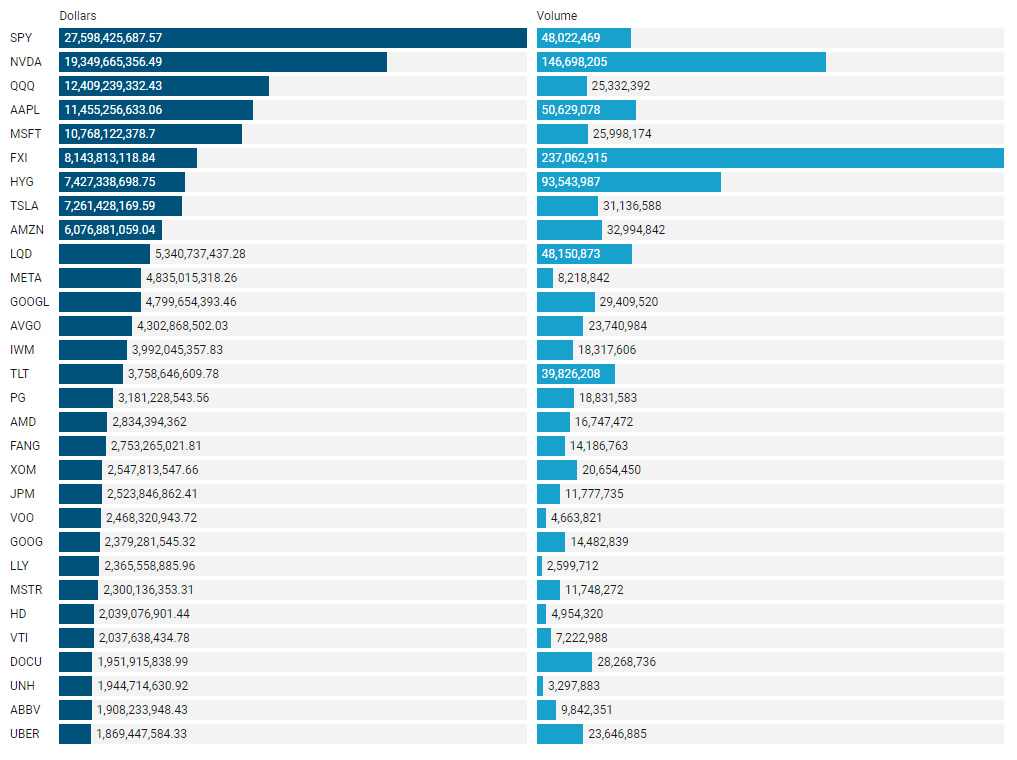

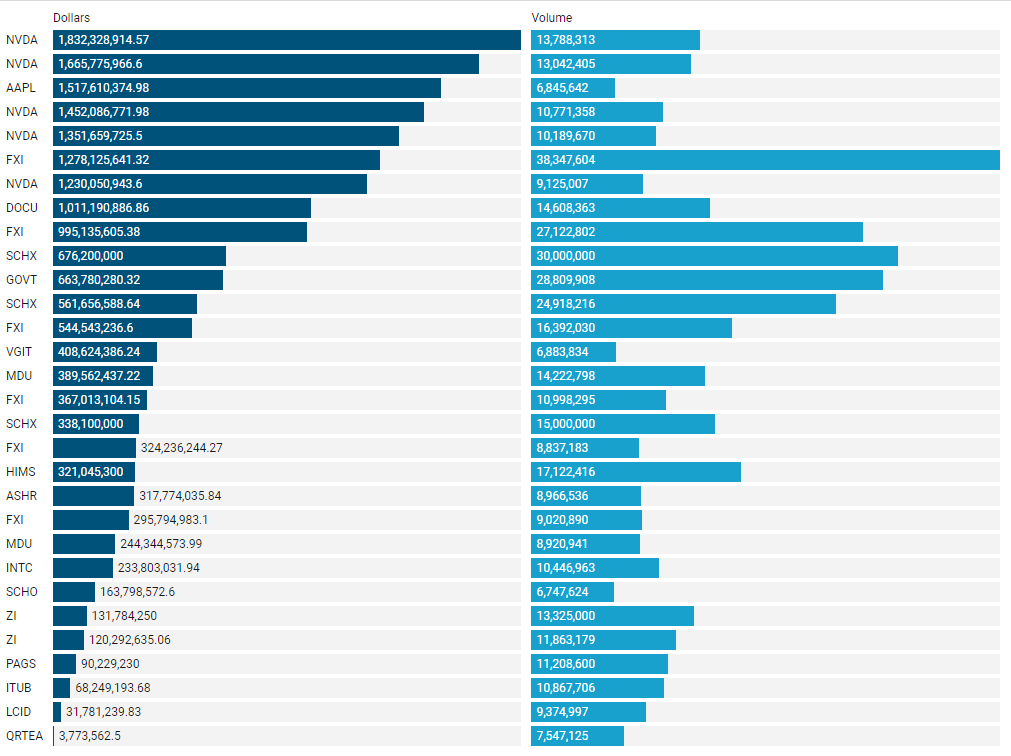

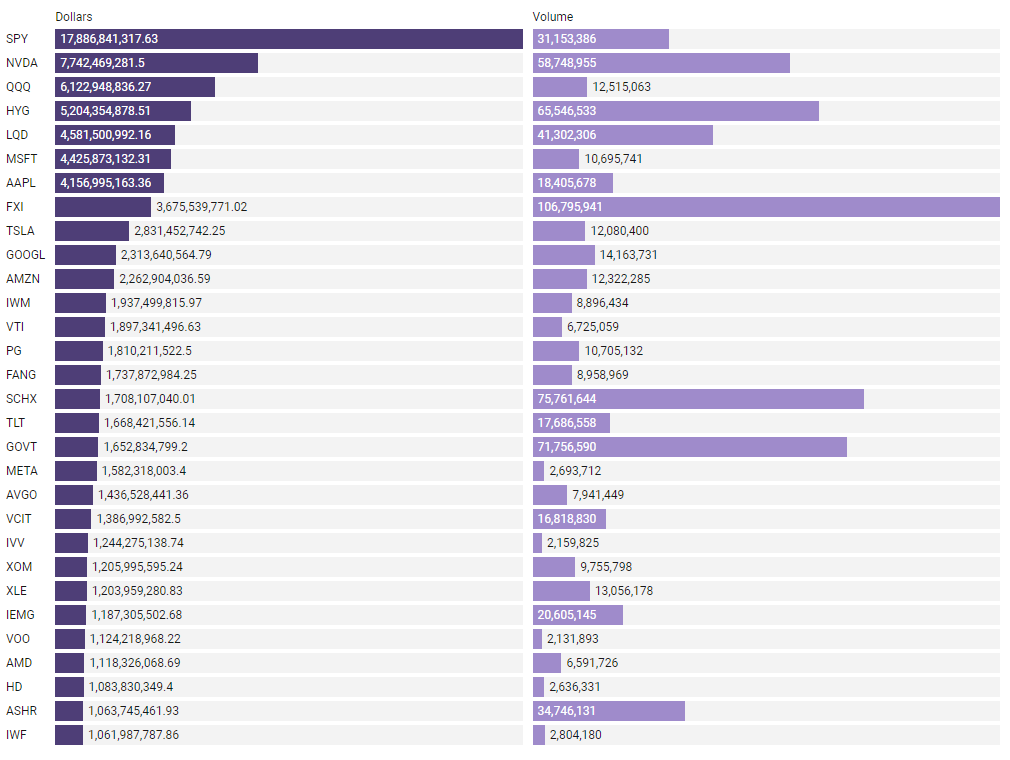

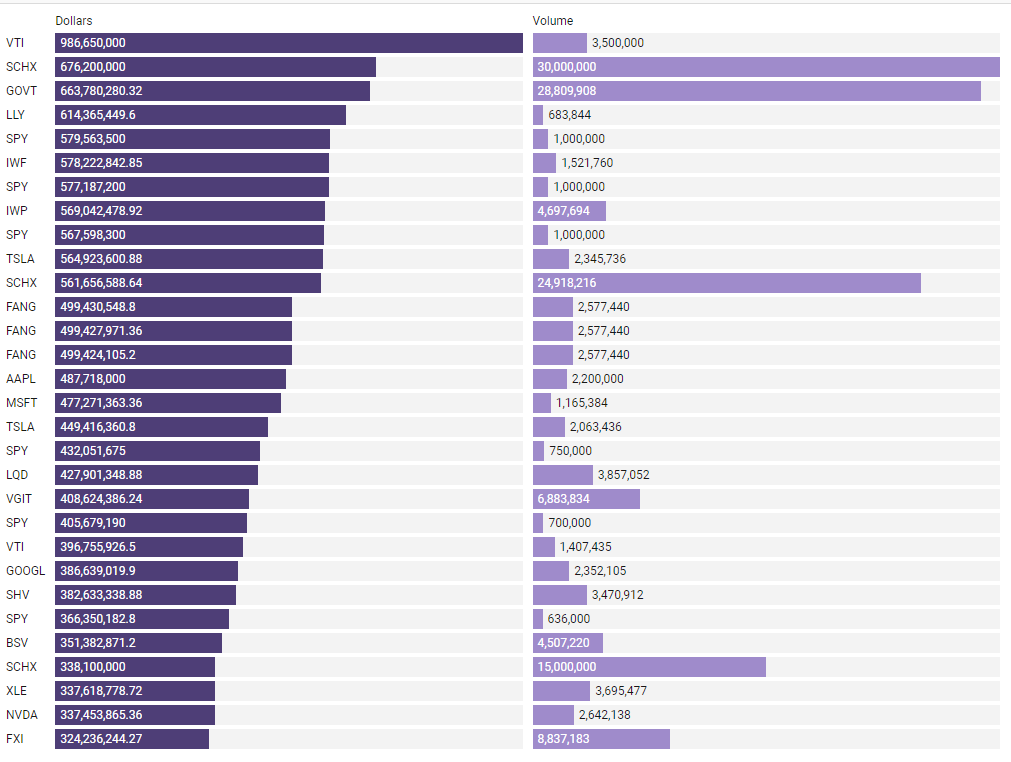

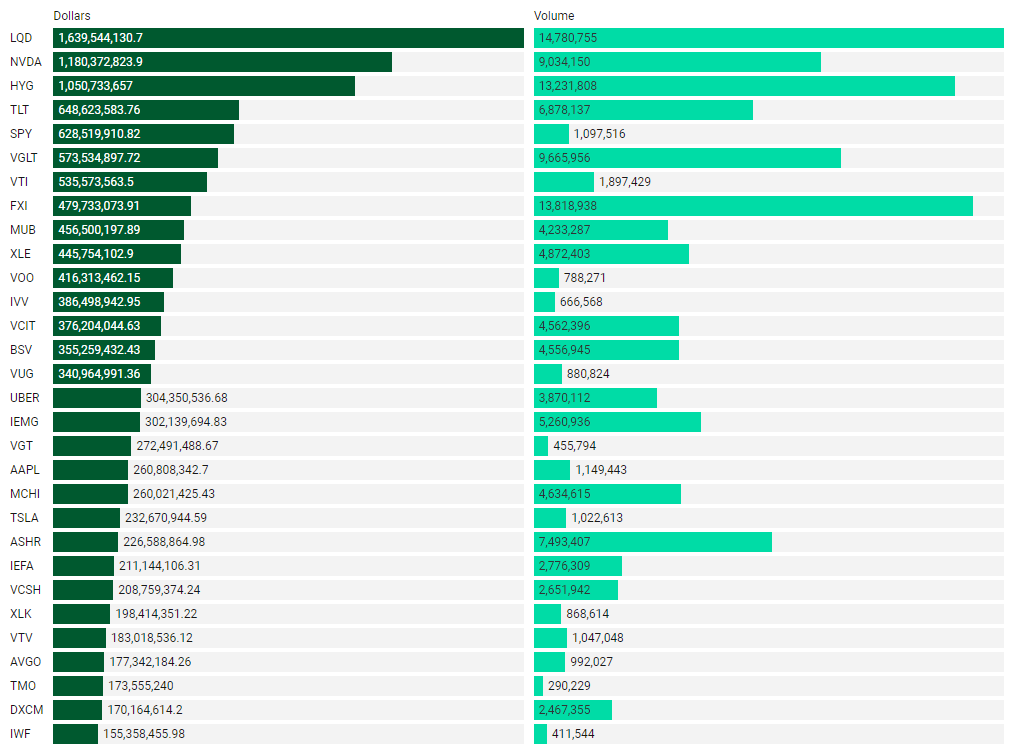

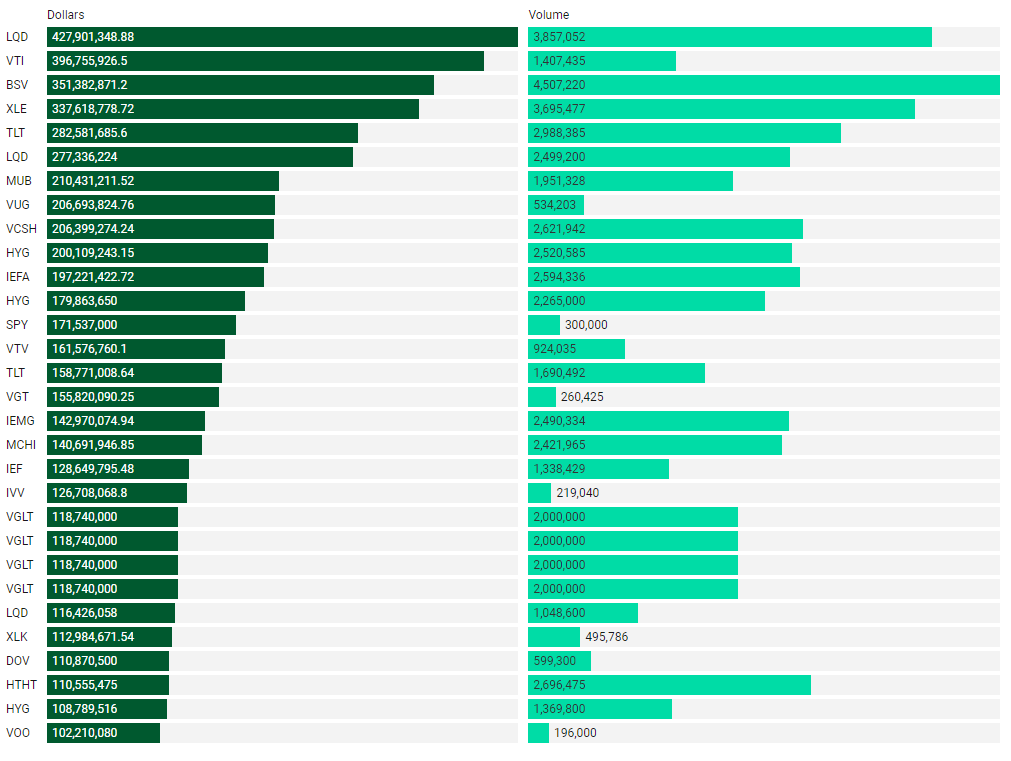

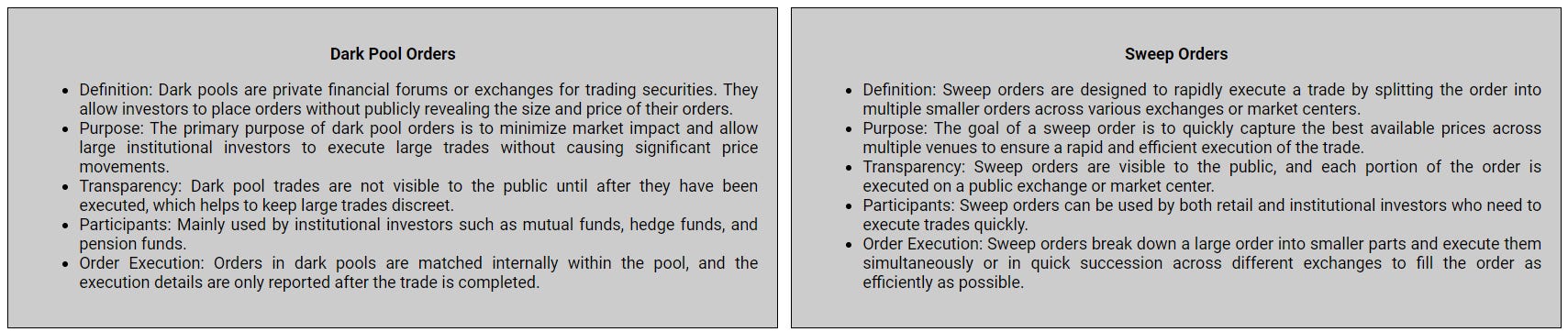

Top Institutional Order Flow

Many excellent trade ideas and sources of inspiration can be found in these prints. While only the top 30 from each group are displayed, the complete results are accessible in VolumeLeaders.com for your convenience to explore at any time. Remember to configure trade alerts within the platform to ensure you never overlook institutional order flows that capture your interest or are significant to you. The blue charts encompass all types of trades, including blocks on lit exchanges; the purple charts exclusively depict dark pool trades; and the green charts represent sweeps only.

Top Aggregate Dollars Transacted by Ticker

Largest Individual Trades by Dollars Transacted

Top Aggregate Dark Pool Activity by Ticker

Largest Individual Dark Pool Blocks by Dollars

Top Aggregate Sweeps by Ticker

Top Individual Sweeps by Dollars Transacted

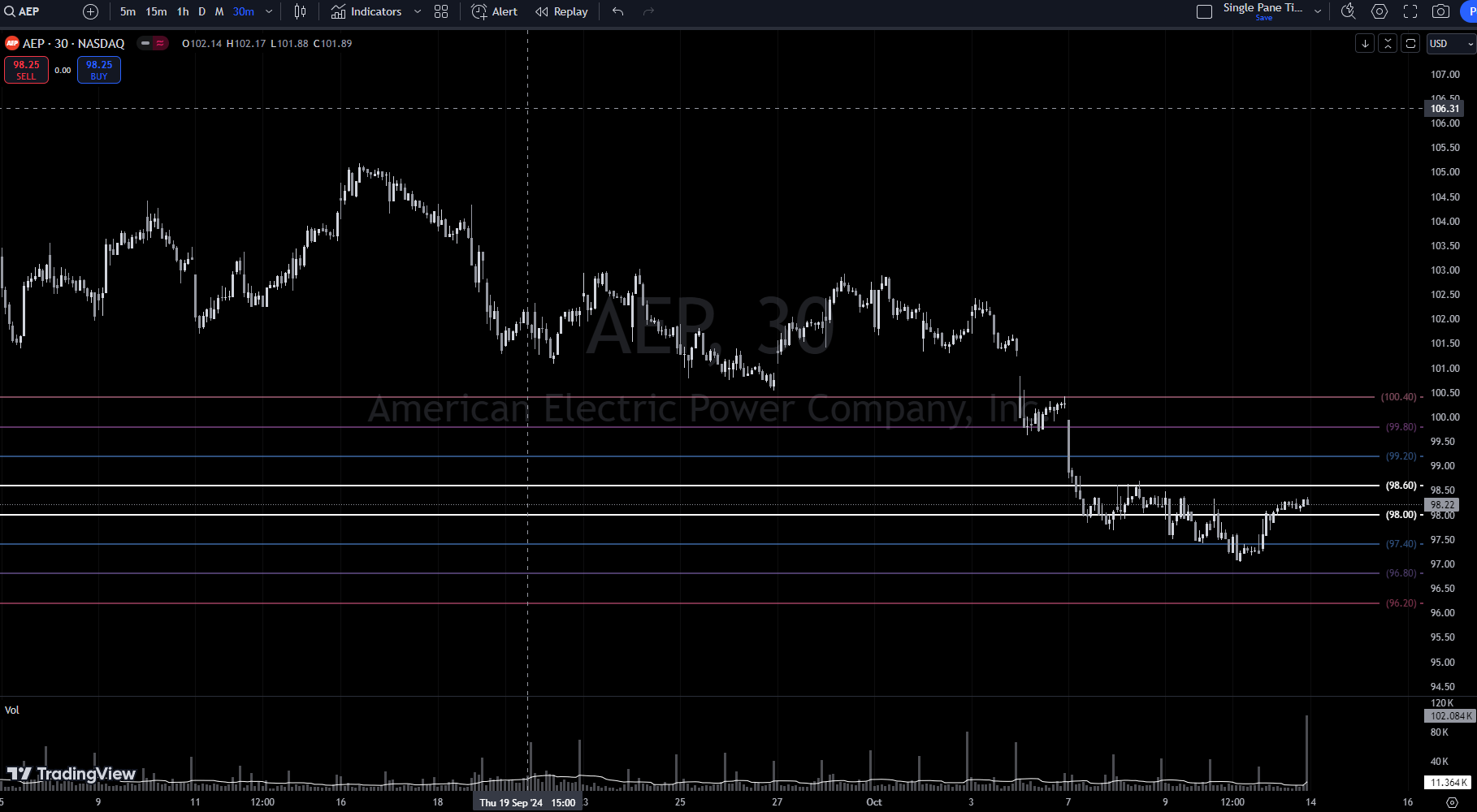

Institutional S/R Levels for Individual Tickers

Please read “Institutional S/R Levels For Major Indices” at the top of this stack to understand the nature and importance of what we’re looking at here visually. Institutions leave footprints that VolumeLeaders.com can illustrate for you while providing context to assess things like institutional conviction and urgency.

The ticker XLC represents the Communication Services Select Sector SPDR Fund, an exchange-traded fund (ETF) that aims to track the performance of the Communication Services sector within the S&P 500. This sector includes companies involved in telecommunications, media, entertainment, and interactive media & services.

Key Points:

Sector Focus: XLC provides exposure to large-cap communication services companies, including those in digital advertising, social media, streaming services, and telecommunications. Prominent holdings often include companies like Meta Platforms (Facebook), Alphabet (Google), Netflix, and Disney.

Top Holdings: The ETF is concentrated in a few large players, especially in the digital and tech spaces, making it somewhat sensitive to the performance of major tech stocks in the communication sector.

Performance Drivers: The fund benefits from trends like increasing digital consumption, growth in social media platforms, and rising demand for streaming and telecommunication services. Technological innovations and shifts in consumer behavior also influence the sector.

Risk Factors: XLC is sensitive to regulatory risks, especially concerning data privacy, content moderation, and antitrust laws, particularly for large tech firms. Additionally, the ETF may experience volatility due to its concentrated exposure to a few dominant companies.

Expense Ratio: XLC has a relatively low expense ratio (typically around 0.10%), making it a cost-effective way to invest in the communication services sector.

Ideal For:

XLC is suited for investors seeking exposure to growth-oriented companies within the communication services space, particularly those interested in digital media, social media, and entertainment. It’s a good option for long-term investors who want targeted exposure to this rapidly evolving sector without the need to pick individual stocks.

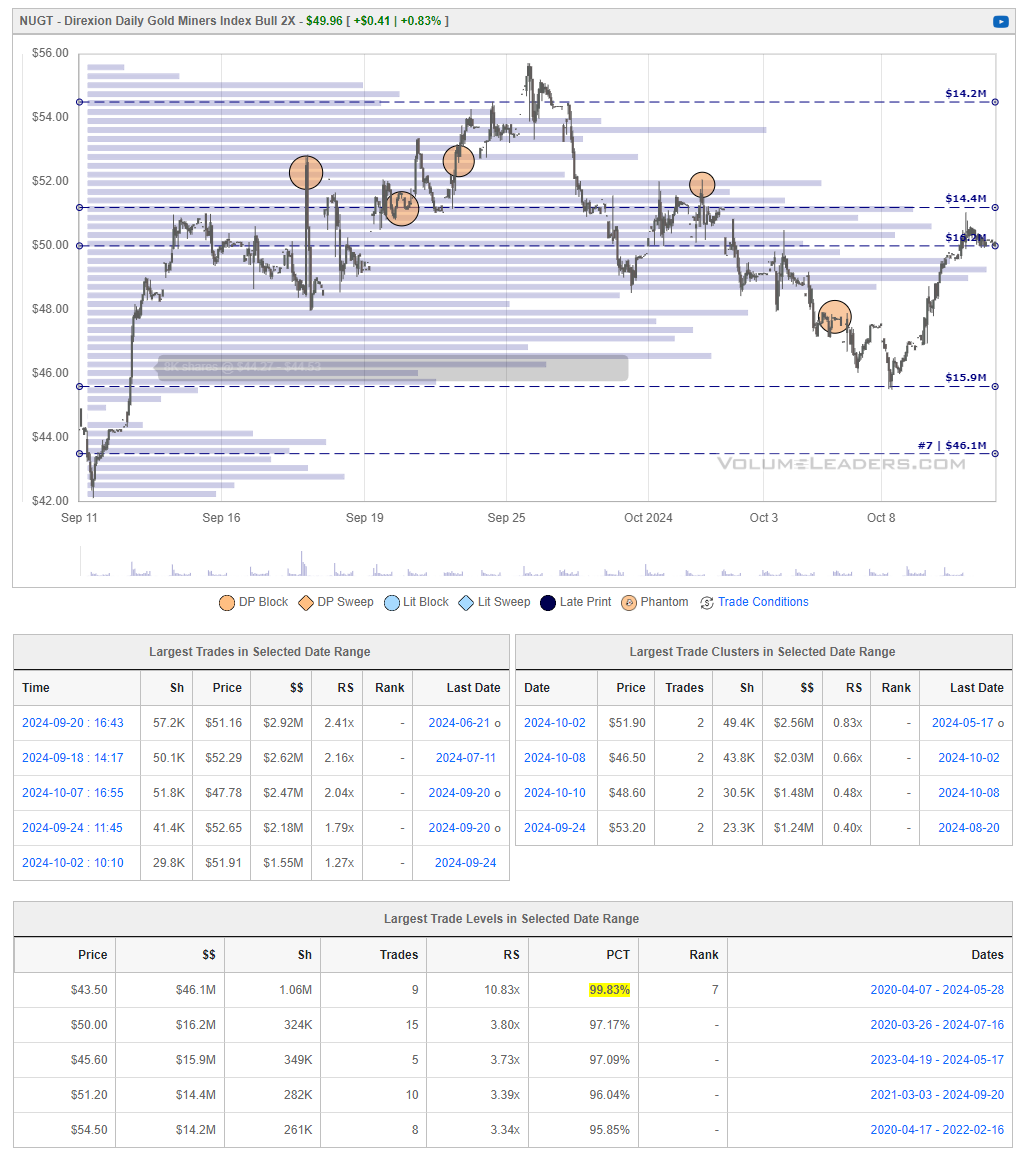

The ticker NUGT represents the Direxion Daily Gold Miners Index Bull 2X Shares, an exchange-traded fund (ETF) that seeks to provide 2x (twice) the daily performance of the NYSE Arca Gold Miners Index. Essentially, NUGT is a leveraged ETF that amplifies the returns (both gains and losses) of the gold mining sector.

Key Points:

Sector Focus: NUGT tracks companies involved in gold mining. It’s heavily influenced by the price of gold, as the profitability of gold miners is closely tied to gold prices.

Leverage: NUGT is designed to deliver twice the daily performance of its benchmark, meaning it is highly volatile and intended for short-term trading rather than long-term investing.

Risk: Due to its leverage, NUGT carries significant risk. While it can generate amplified gains if gold prices rise, it can also lead to large losses if the gold market declines.

Expense Ratio: NUGT typically has a higher expense ratio compared to non-leveraged ETFs, reflecting the costs associated with maintaining the leverage (around 1.14%).

Ideal For:

NUGT is suitable for traders who are looking to capitalize on short-term price movements in gold mining stocks, but it’s not recommended for buy-and-hold investors due to the risks associated with daily rebalancing and leverage.

The ticker USO represents the United States Oil Fund LP, an exchange-traded fund (ETF) that seeks to track the price movements of West Texas Intermediate (WTI) crude oil. The fund does this primarily by investing in near-term futures contracts on WTI crude, rather than holding physical oil.

Key Points:

Objective: USO aims to reflect the daily changes in the price of WTI crude oil. It gives investors a way to gain exposure to oil prices without having to directly trade in the futures market.

Investment Strategy: USO invests in futures contracts, not actual crude oil. This means the fund's performance is influenced by the "roll yield" when contracts expire and need to be replaced with new ones, which can impact returns (either positively or negatively, depending on market conditions).

Volatility: Oil prices can be highly volatile, influenced by factors like global supply and demand, geopolitical events, OPEC decisions, and changes in energy policy. Therefore, USO can experience significant price swings.

Expense Ratio: The fund has a relatively moderate expense ratio for a commodity ETF (typically around 0.83%), reflecting the costs associated with managing the fund’s oil futures contracts.

Ideal For:

USO is primarily used by traders and investors looking to gain exposure to oil price movements or hedge other oil-related investments. However, due to the complexities of the futures market and the risks associated with contango (when future prices are higher than the spot price), it’s not typically recommended for long-term investing.

The ticker DOW represents Dow Inc., a major global chemical company that produces a wide range of products, including chemicals, plastics, and agricultural products. It operates across several industries, including packaging, infrastructure, electronics, and consumer care.

Key Points:

Core Business: Dow Inc. is one of the largest chemical producers in the world, with its operations spanning basic chemicals, advanced materials, and specialty products. The company's products are used in a variety of sectors, such as construction, packaging, automotive, and consumer goods.

Market Exposure: As a cyclical stock, Dow’s performance is closely tied to global economic conditions. When the global economy is growing, demand for chemicals, plastics, and industrial materials tends to rise, boosting Dow’s revenues. Conversely, during economic downturns, demand for these products typically decreases.

Dividends: Dow Inc. is known for paying a relatively high dividend, making it attractive for income-seeking investors. The company prioritizes returning capital to shareholders through dividends and share buybacks.

Risk Factors: Being a major player in the chemicals industry, Dow is exposed to risks such as fluctuations in raw material costs (especially oil and natural gas), changes in global demand, regulatory risks related to environmental regulations, and geopolitical tensions that can affect global trade.

Innovation & Sustainability: Dow is also focusing on sustainability and innovation in materials, seeking to reduce the environmental impact of its operations and products while addressing growing demand for more sustainable solutions in industries like packaging and consumer goods.

Ideal For:

Dow Inc. appeals to investors looking for exposure to the industrial and materials sectors, particularly those interested in companies that provide essential materials for a wide range of industries. It is also attractive to income-oriented investors due to its reliable dividend payments. However, because it is sensitive to economic cycles, it may be more volatile during periods of economic uncertainty.

The ticker BITB represents the Bitwise Bitcoin ETF, a fund designed to provide investors with direct exposure to Bitcoin. It aims to track the price performance of spot Bitcoin, meaning it holds Bitcoin directly, secured through a multi-layer cold storage system. Launched in January 2024, it offers a simple way for investors to participate in Bitcoin’s price movements without needing to handle the complexities of buying and storing the cryptocurrency themselves.

Key Points:

Investment Objective: BITB seeks to mirror the daily price performance of Bitcoin by holding physical Bitcoin in custody. It gives traditional investors a way to gain Bitcoin exposure through an exchange-traded product.

Management: The ETF is passively managed and carries a low management fee of around 0.20%, one of the lowest in the market for Bitcoin ETFs.

Performance: Since its launch, BITB has seen significant growth, with year-to-date returns of around 34.73% as of September 2024. The ETF’s price reflects Bitcoin's volatility, making it more suitable for investors comfortable with crypto market swings.

Risk Considerations:

Volatility: Like Bitcoin, BITB is highly volatile and can experience significant price fluctuations. It’s primarily intended for investors with a high-risk tolerance.

Market Premium/Discount: BITB has occasionally traded at a premium or discount to its net asset value (NAV), which reflects short-term supply and demand dynamics in the ETF market.

This ETF provides a convenient route for investors to engage with Bitcoin, particularly those looking for a secure and regulated way to invest in the leading cryptocurrency.

The ticker VNQ represents the Vanguard Real Estate ETF, which provides exposure to the U.S. real estate sector. It aims to track the performance of the MSCI US Investable Market Real Estate 25/50 Index, a benchmark that covers a broad range of real estate-related companies, including real estate investment trusts (REITs).

Key Points:

Sector Focus: VNQ focuses on real estate, investing primarily in equity REITs that own and operate income-generating real estate, such as office buildings, malls, apartments, and other commercial properties. It also includes mortgage REITs and real estate development firms.

Holdings: The ETF holds a diversified portfolio of real estate companies and REITs, with some of its top holdings often including companies like American Tower Corp, Prologis, Crown Castle, and Equinix. These are large companies with significant influence in the U.S. real estate market.

Dividends: VNQ is known for offering relatively high dividend yields, making it attractive to income-focused investors. This is because REITs, by law, must distribute a large portion of their income to shareholders as dividends.

Expense Ratio: VNQ is highly cost-efficient, with a very low expense ratio (typically around 0.12%), which makes it one of the more affordable ways to gain diversified exposure to real estate.

Risk Factors: Like other REIT-based ETFs, VNQ is sensitive to interest rate changes. Rising interest rates can negatively impact the cost of borrowing for real estate companies and reduce the attractiveness of high-dividend investments. Economic downturns and changes in property values can also affect VNQ’s performance.

Ideal For:

VNQ is suitable for investors looking for diversified exposure to the real estate sector, those seeking regular dividend income, or those wanting a hedge against inflation, as real estate often holds value during inflationary periods. It is commonly used as a long-term holding in portfolios focused on income and growth.

Overall, VNQ offers a low-cost and diversified way to invest in the U.S. real estate market, particularly through REITs, providing both income and growth potential.

VL Precision Swings

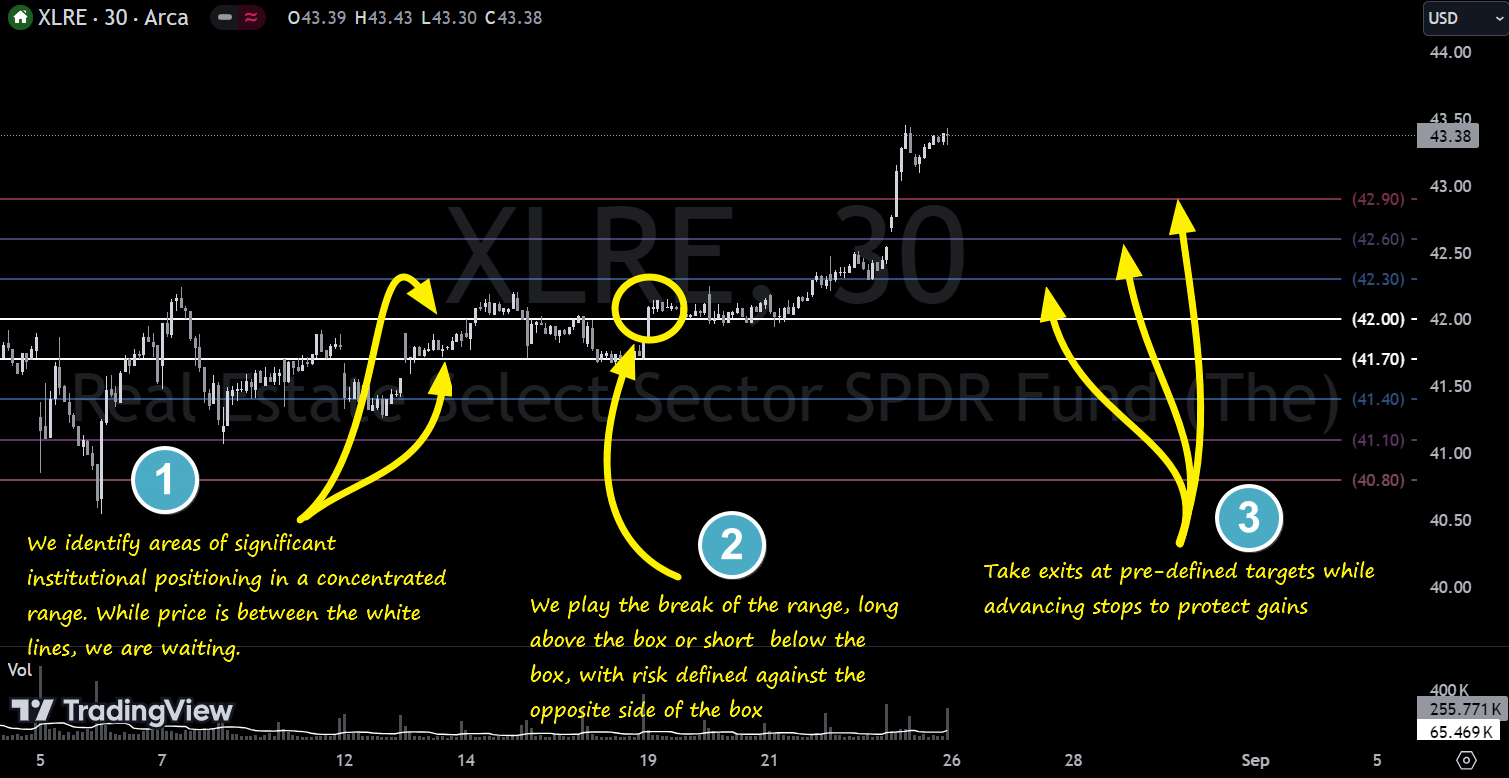

This week we’re featuring additional screened trade ideas from one of our backtested proprietary signals for tactical swings called IBB - Institutional Breakout Boxes. The IBB Setup identifies an area of significant institutional positioning within a tight, concentrated price range, forming what we call a breakout box. This setup captures the potential energy built up as large players accumulate or distribute positions, creating a high-probability opportunity for explosive moves once the price breaks out of this zone. The precision of this setup allows traders to capitalize on the momentum generated by institutional forces, with clearly defined risk and reward parameters. These trades typically last from 2-days to 2-weeks and given targets are designed for tactical swing/base hits; more patient, longer-term swing traders frequently find that these ideas often provide excellent entries that help them get into risk-free runners quickly that fully play out over a longer time horizon. I highly encourage you to revisit prior recommendations - each week produces a couple tickers that make a large move all at once but the others often have more juice to keep running, all due to the power of institutional positioning.

Note, these are shared for educational and entertainment purposes only and do not constitute financial advice.Here’s an example from XLRE:

Let’s see how last week’s setups played out:

BIDU: +3.17%, triggered short, no targets met, full position still on

QCOM: still stuck in the IBB

TXN: +.68%, triggered long, no targets met, full position still on

COIN: triggered short and stopped, no position, keep on watch

MO: +.4%, triggered short, no targets met, full position still on

WDAY: triggered long and stopped, no position, keep on watch

DGRO: +.92%, triggered long, first target met, runners still on for T2 and T3

LIN: +4.64%, first target met, runners still on for T2 and T3

VKTX: +1%, triggered long, no targets met, full position still on

AAPL: still stuck in the IBB, keep on watch

ALAB: +24.17, all targets met

Here are some of the Precision Swings we’re watching this week:

Institutionally-Backed Gainers & Losers

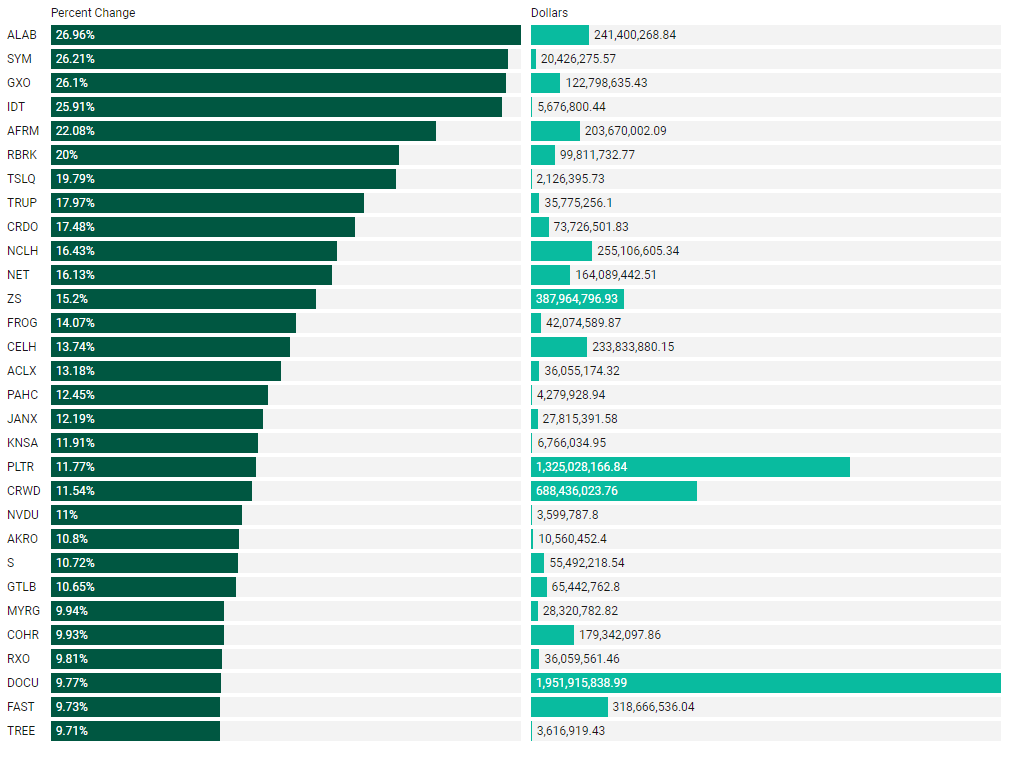

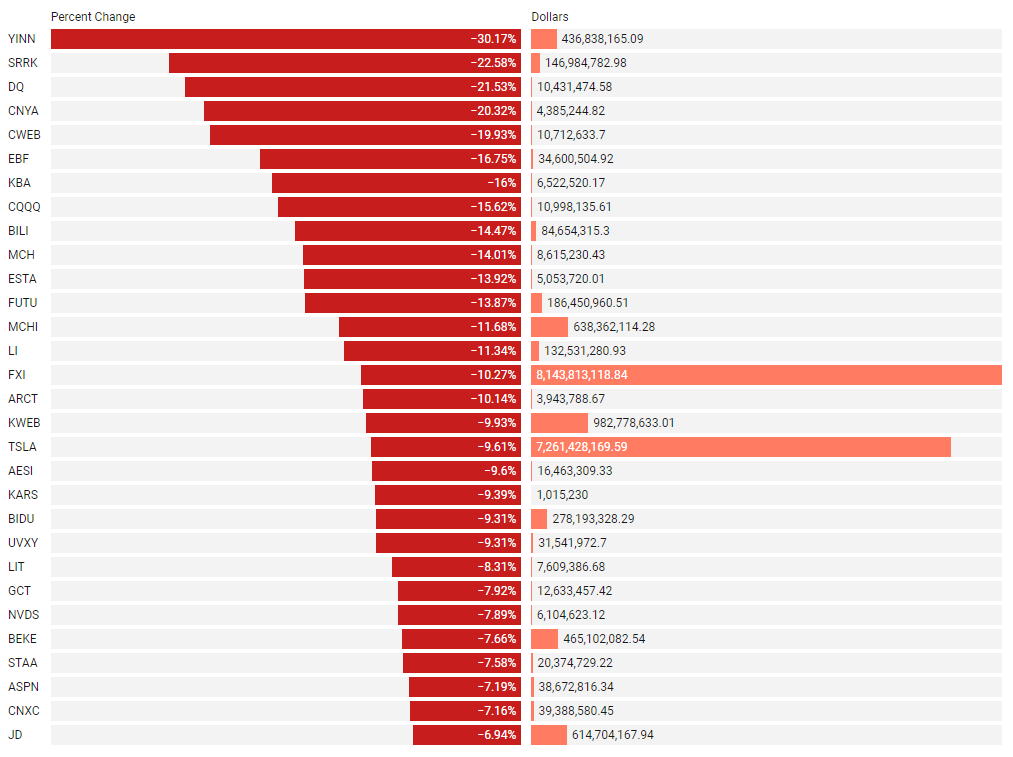

If you’re going to bet on a horse, consider one that is officially endorsed by an institution! These are the top percent gainers (green) and percent losers (red) from this week’s open-to-close that had a trade price greater than $20 and institutional involvement. Continue watching tickers from prior stacks as these frequently turn into multi-leg trades with a lot of movement!

Top Institutionally Backed Gainers

Top Institutionally Backed Losers

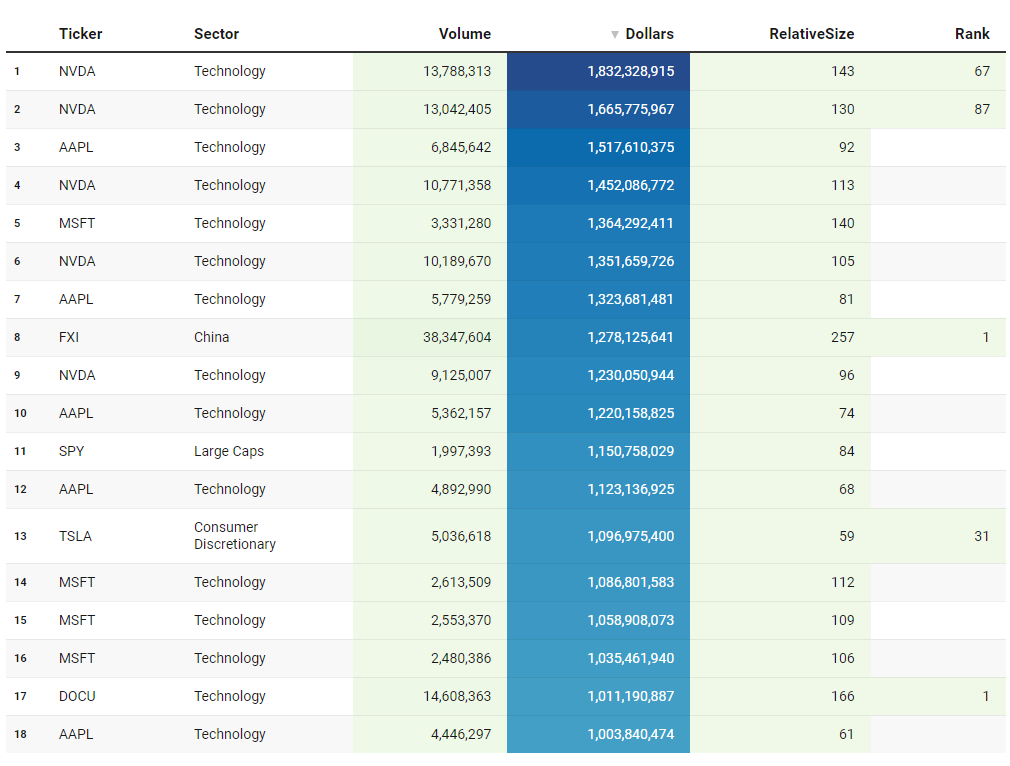

Billionaire Boys Club

Tickers that printed a trade worth at least $1B last week get a special shout-out… Welcome to the club. Subs should login to VolumeLeaders.com to get the exact trade price and relevant institutional levels around the trade - these are massive commitments by institutions that should not be ignored.

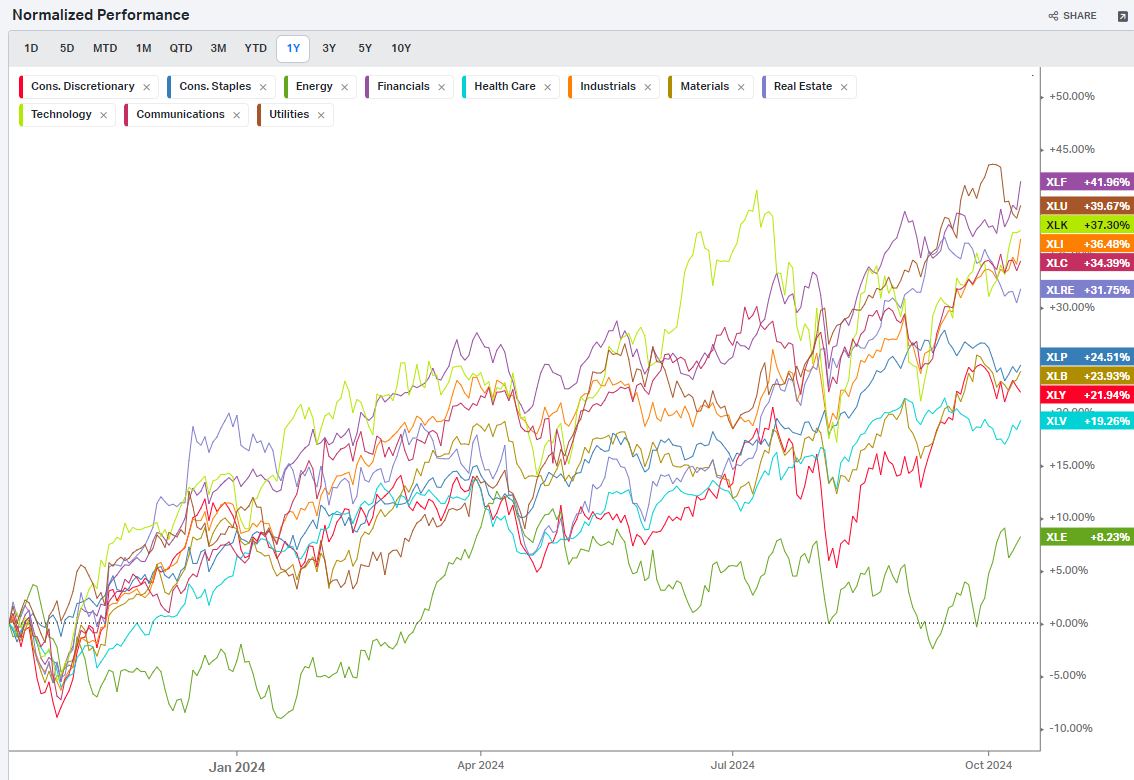

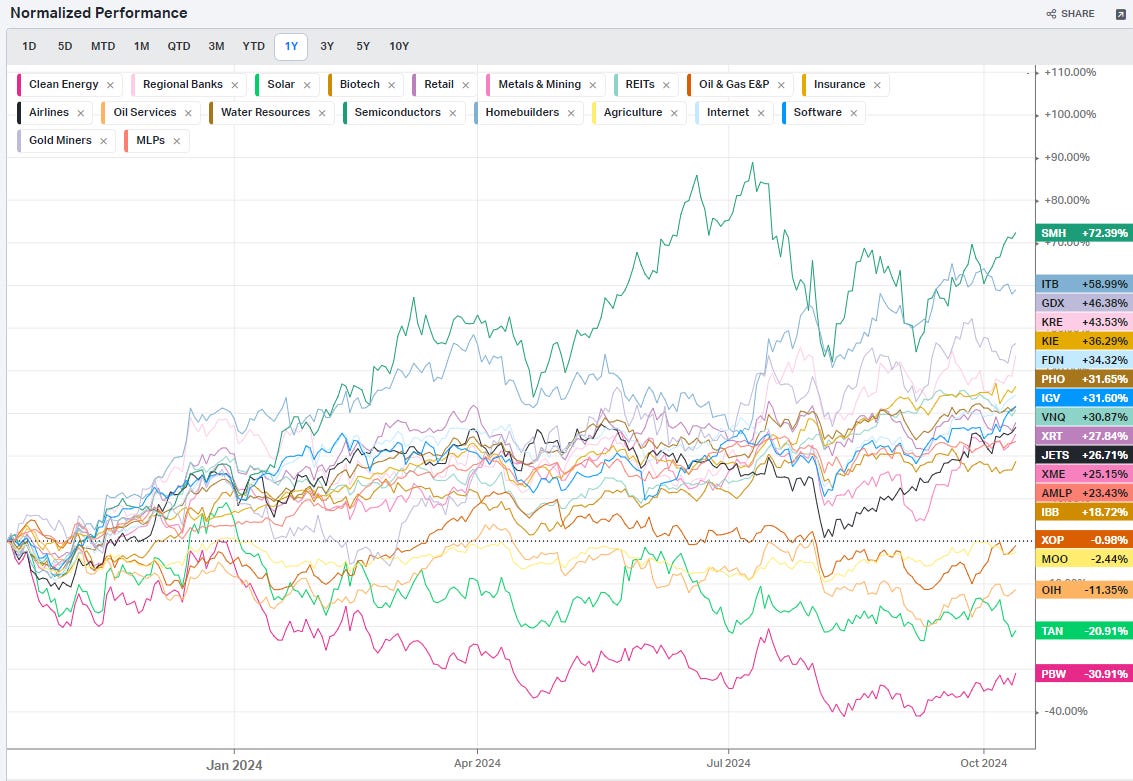

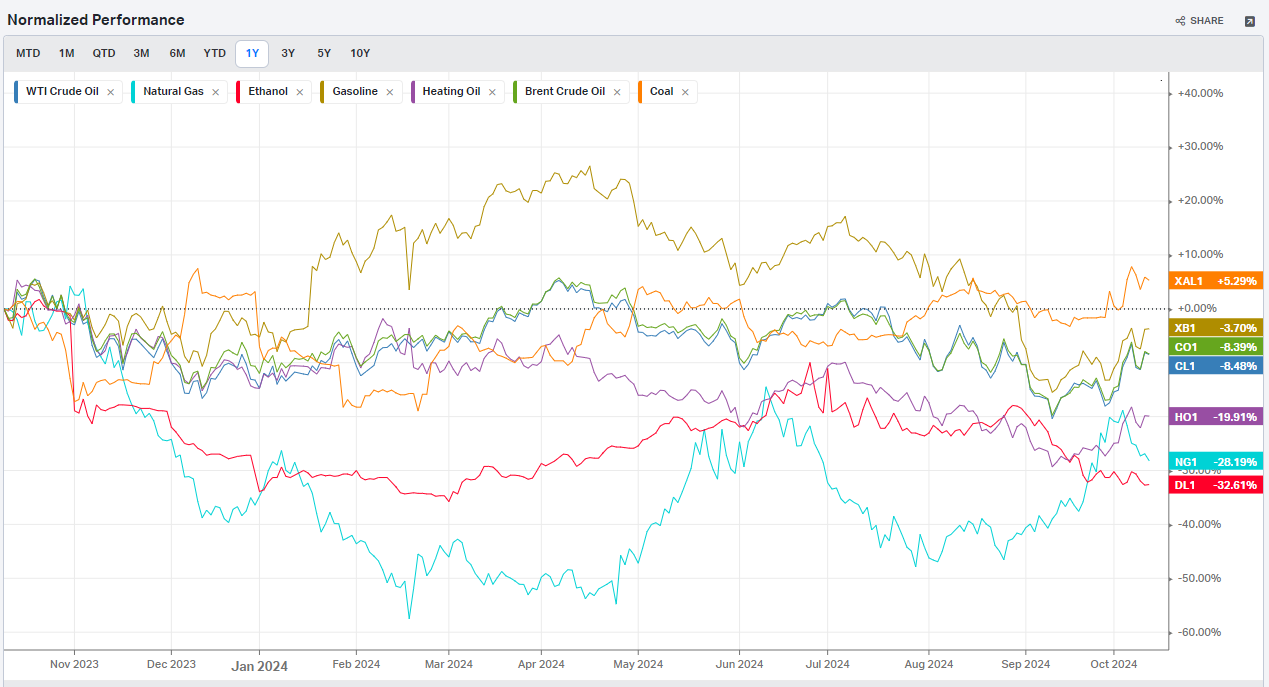

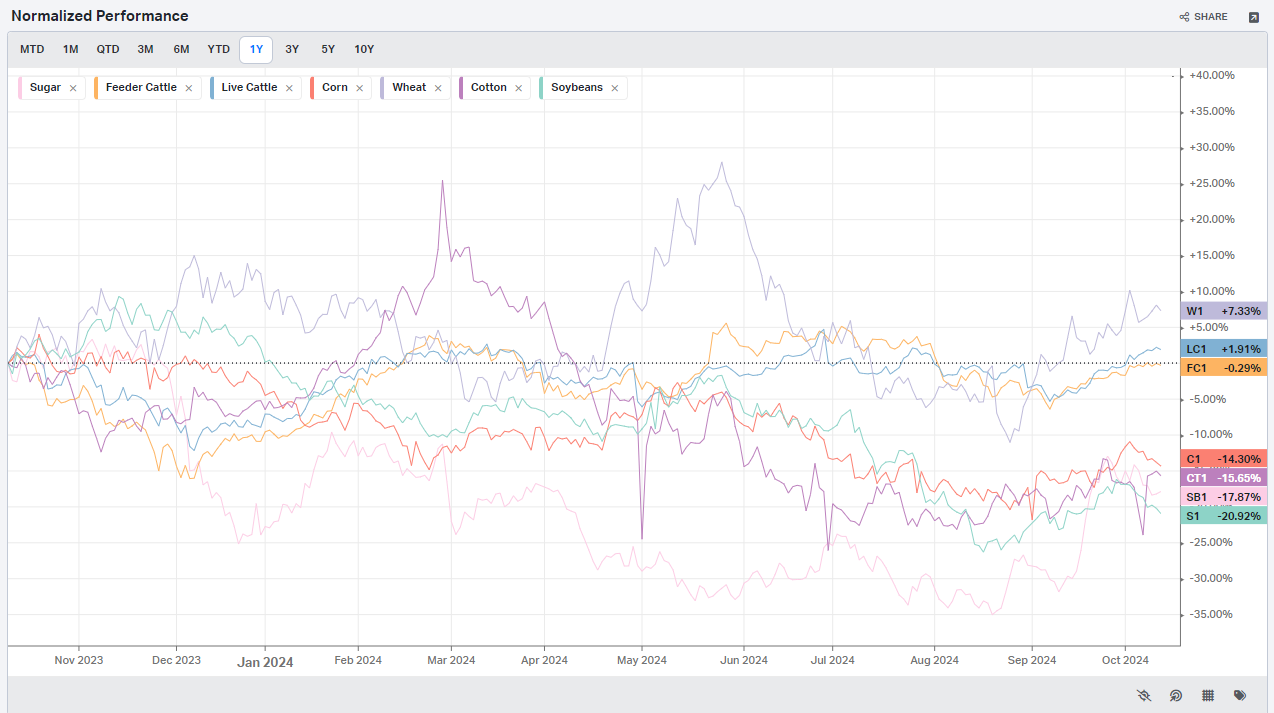

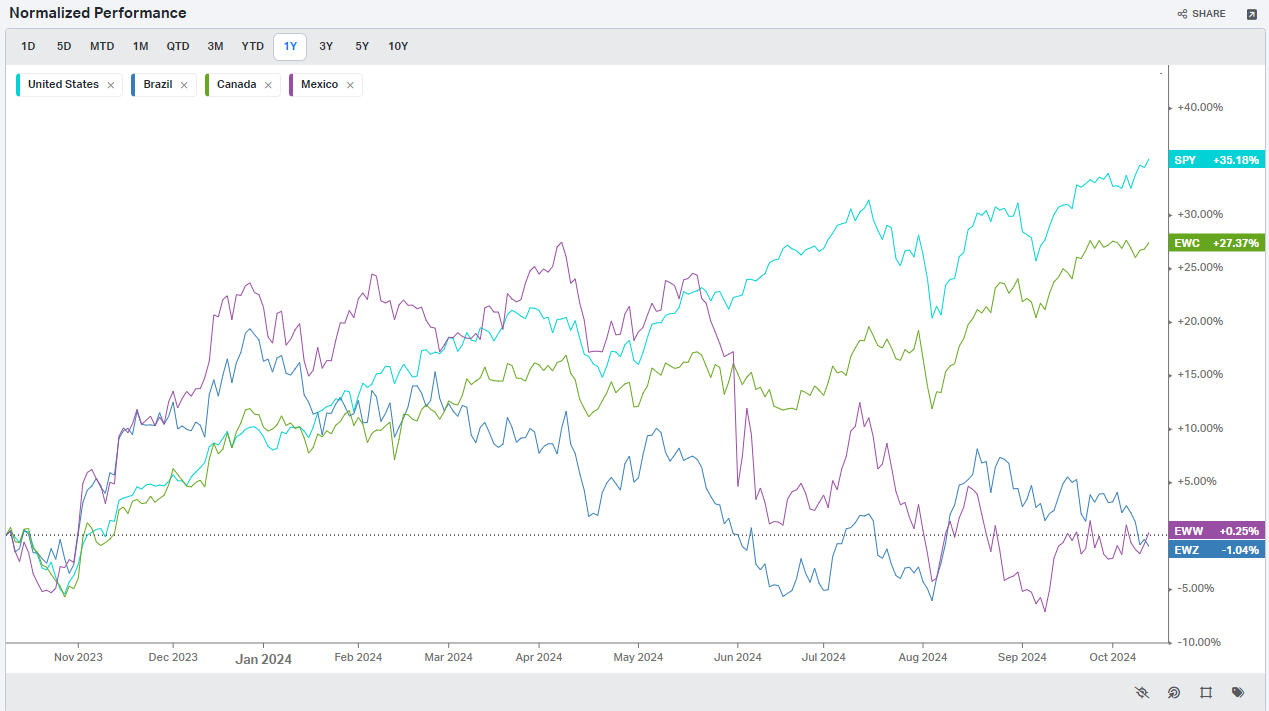

Summary Of Thematic Performance YTD

VolumeLeaders.com provides a lot of pre-built filters for thematics so that you can quickly dive into specific areas of the market. These performance overviews are provided here only for inspiration. Consider targeting leaders and/or laggards in the best and worst sectors, for example.

S&P By Sector

S&P By Industry

Energy

Metals

Agriculture

Country ETFs

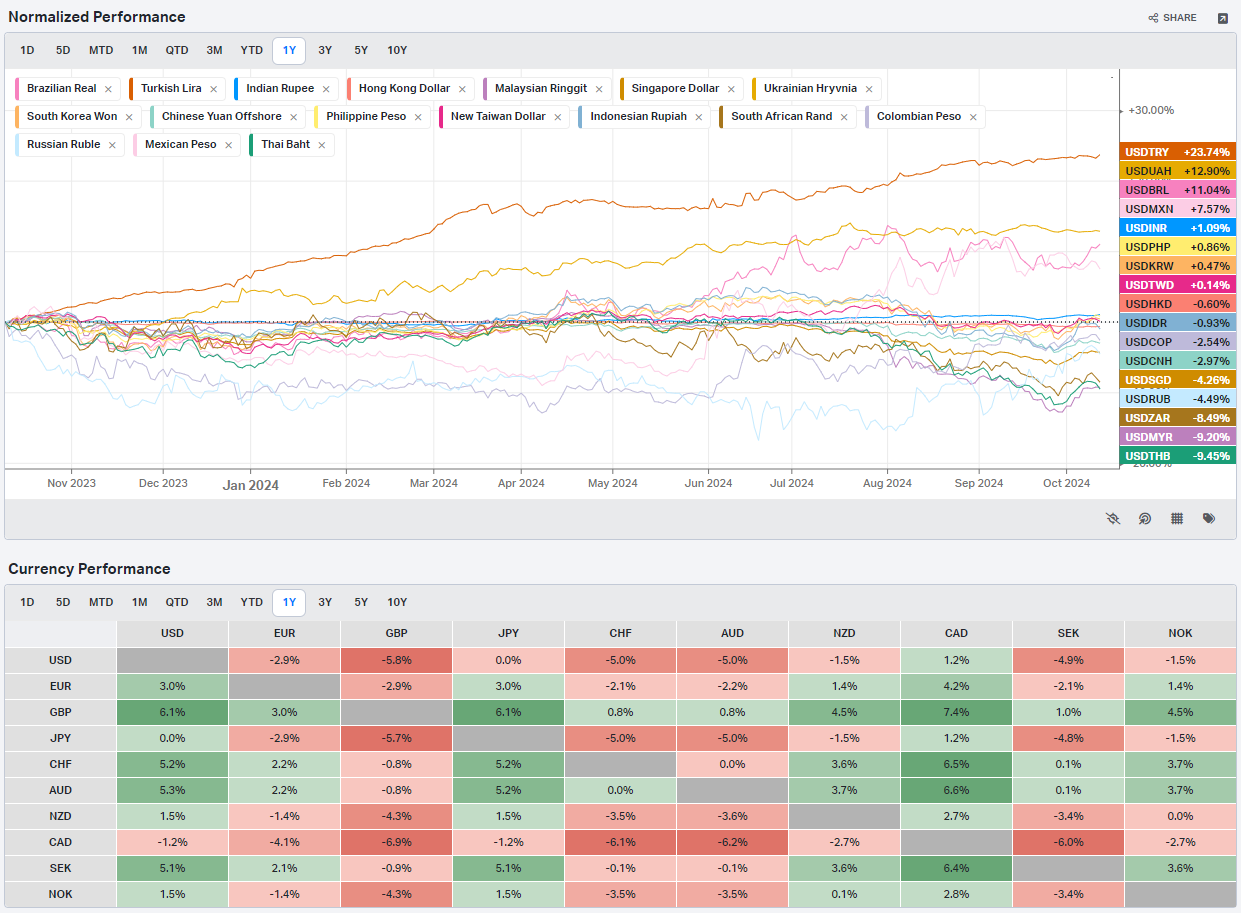

Currencies

Yields

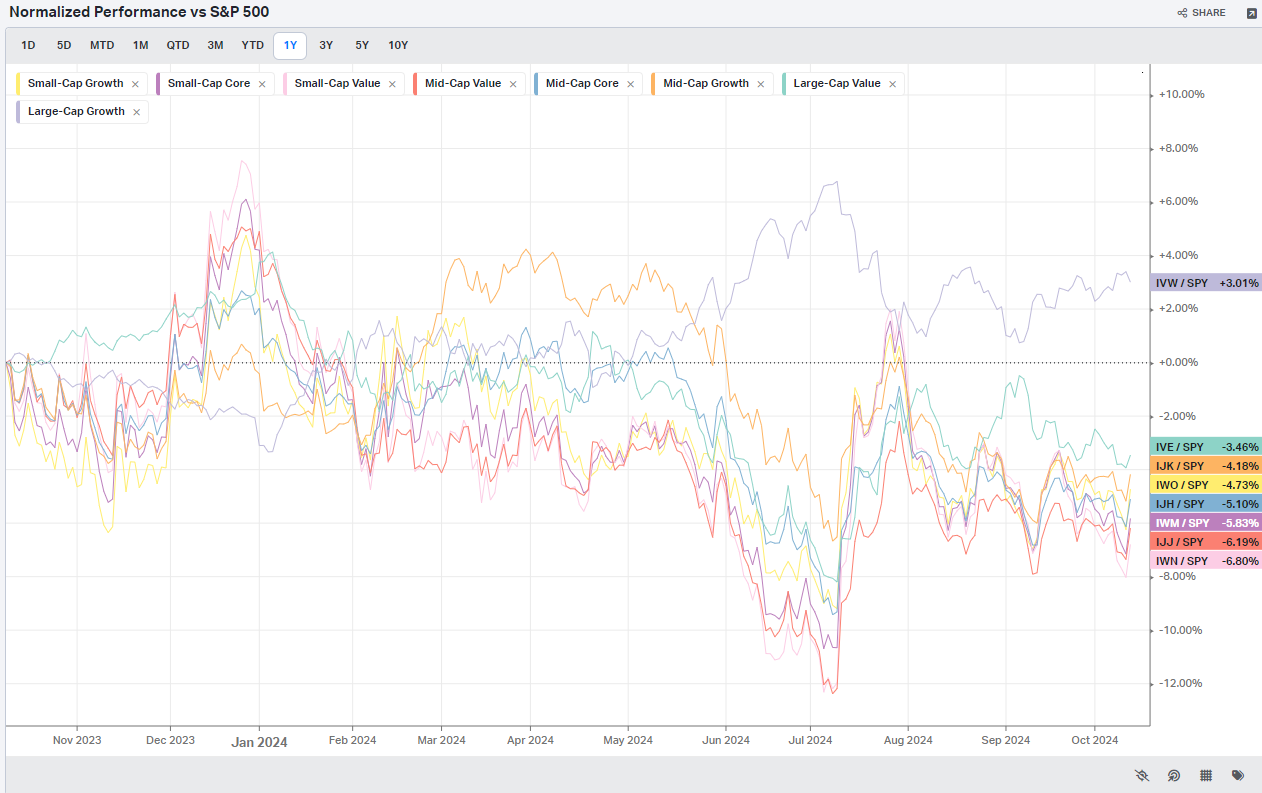

Factors: Size vs Value

Factors: Style

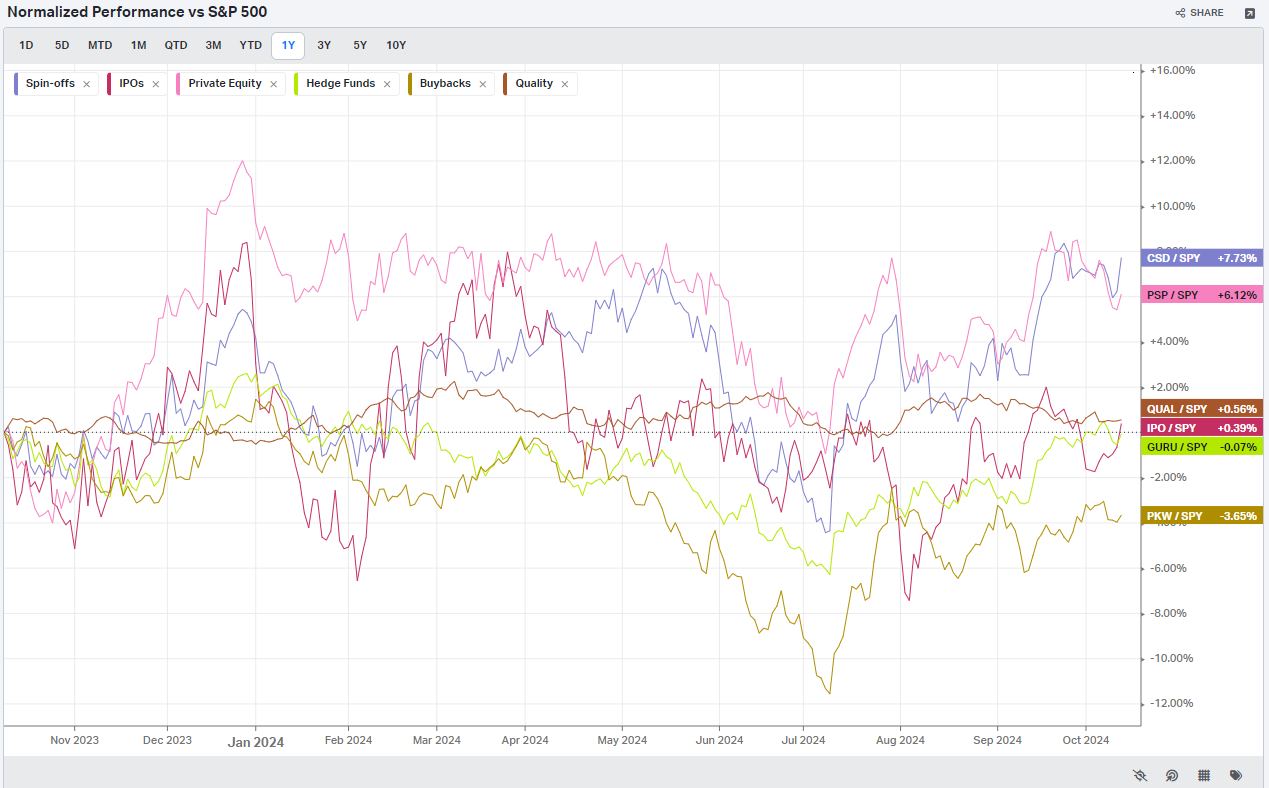

Factors: Qualitative

Social Media Favs

Most mentioned/discussed tickers on Reddit from some of the most active Subreddits for trading:

Events On Deck This Week

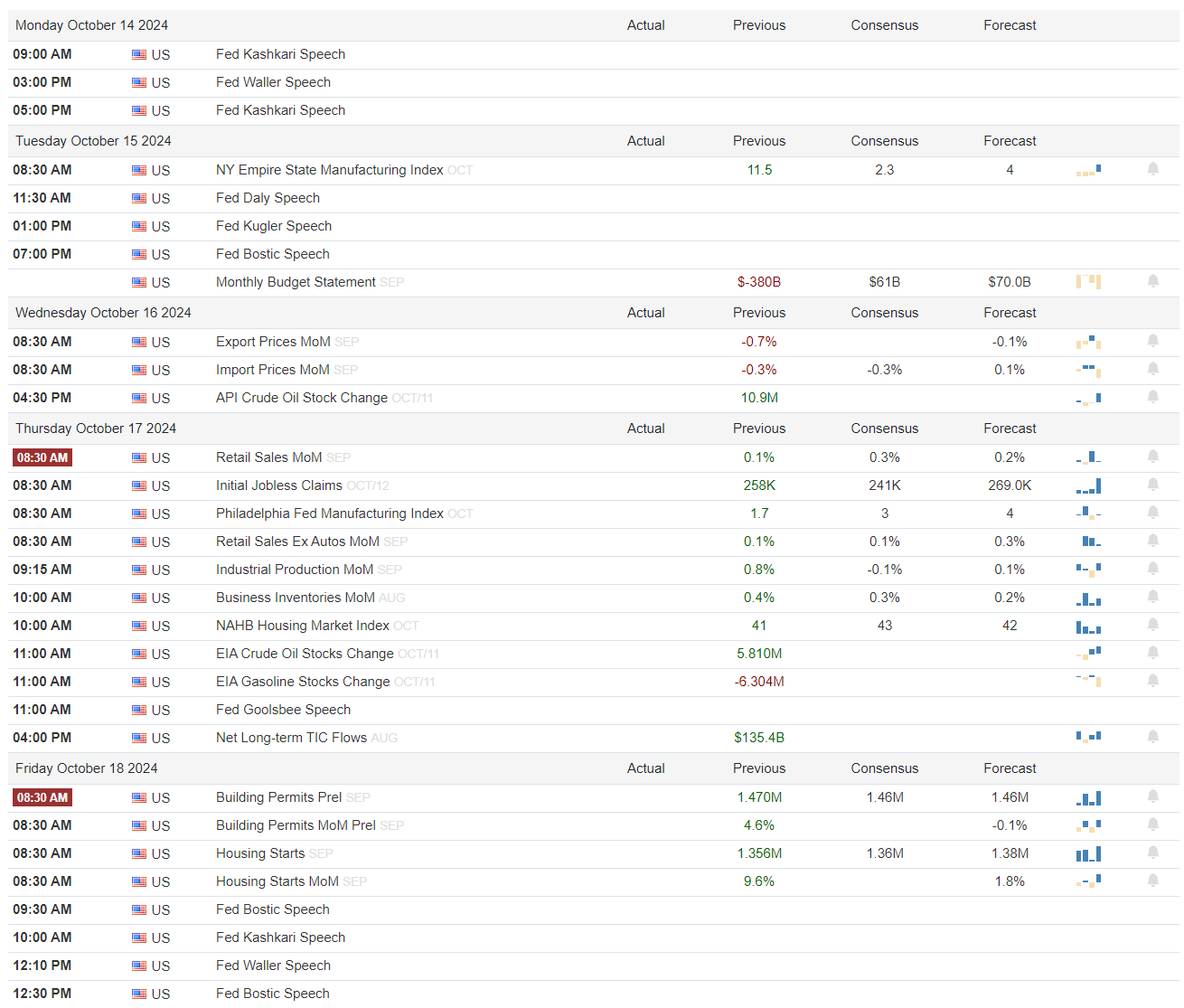

Here are key events happening this week that have the potential to cause outsized moves in the market or heightened short-term volatility.

Econ

Earnings

A Final Word

Thank you for reading this week's edition of Market Momentum. If you found value in this content, please consider sharing it with a friend or colleague, in a Discord or a Tweet. This small favor helps keep this stack free for you! Please check out VolumeLeaders.com for your own free trial of the platform that brings you the data powering this stack. Wishing you all a green week ahead filled with many bags ❤️💰.